Catalysts Market Size, Share & Industry Analysis, By Type (Heterogeneous Catalysts, Homogeneous Catalysts, and Others), By Application (Environmental, Chemical Synthesis, Polymer Catalysis, Petroleum Refining, and Others), and Regional Forecast, 2026-2034

CATALYSTS MARKET SIZE AND FUTURE OUTLOOK

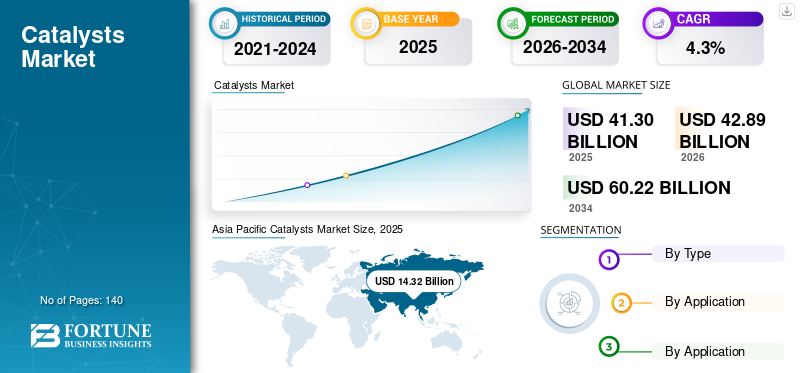

The catalysts market size was valued at USD 41.30 billion in 2025. The market is projected to grow from USD 42.89 billion in 2026 to USD 60.22 billion by 2034, exhibiting a a CAGR of 4.3% during the forecast period. Asia Pacific dominated the catalysts market with a market share of 34.67% in 2025.

A catalyst is a substance that increases the rate of a chemical reaction without being permanently consumed in the overall response. It works by providing an alternative reaction pathway with lower activation energy, so the reaction happens faster or under milder conditions.

The market comprises production and sale of catalytic materials used to accelerate and optimize chemical reactions across refining, petrochemicals, chemical synthesis, polymer manufacturing, and environmental treatment applications. The market growth is driven by tightening emission norms, rising demand for higher process efficiency, expansion of petrochemical and specialty chemical production, and increasing investment in hydrogen, ammonia, renewable fuels, and other lower-carbon industrial pathways. Key players in the market include BASF SE, Clariant AG, Johnson Matthey plc, Honeywell, and Topsoe A/S.

Download Free sample to learn more about this report.

CATALYSTS MARKET TRENDS

Shift Toward Low-Emission Processing and Application-Specific High-Performance Solutions is Emerging Market Trend

A major trend in the market is the shift from conventional volume-driven supply toward application-specific, efficiency-oriented, and lower-emission catalyst systems. Catalyst suppliers are increasingly positioning their portfolios around energy efficiency, higher selectivity, longer cycle life, and lower carbon intensity across hydrogen, ammonia, methanol, refining, petrochemicals, polymers, and emissions control. Clariant, for example, stated that its upgraded syngas catalyst portfolio is designed to improve plant economics and reduce carbon emissions, while enabling more energy-efficient production of blue hydrogen and green ammonia.

Similarly, the market is noticing a stronger circularity and critical-material recovery trend, especially in precious-metal-containing catalyst systems. BASF reported that its Environmental Catalyst and Metal Solutions business provides full-loop services that combine mobile emissions catalysts with precious metals trading and recycling, indicating that catalyst suppliers are moving beyond pure product sales toward integrated recovery and reuse models. This trend is becoming significant as producers and customers seek to improve raw-material security, reduce lifecycle emissions, and manage exposure to platinum-group-metal supply concentration.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Tightening Emission Standards and Broad-Based Industrial Need for Process Efficiency to Drive Market Growth

One of the strongest drivers for the catalysts market growth is the tightening of emission-control requirements across automotive and industrial systems. BASF describes its Environmental Catalyst and Metal Solutions division as a global market leader in mobile emissions catalysts and notes that leading OEMs rely on its systems to meet increasingly stringent current and upcoming emissions regulations around the world. The European Union adopted the Euro 7 regulation in 2024, while India mandated BS-VI nationwide from April 1, 2020. These policy moves continue to sustain demand for catalysts that reduce hydrocarbons, carbon monoxide, nitrogen oxides, and particulate matter in vehicle exhaust and related applications.

This driver remains important as catalysts are also central to industrial productivity and energy efficiency, not just compliance. Heterogeneous catalysts dominate due to their use in large-scale industrial operations such as refining, petrochemicals, polymer production, and environmental treatment, where ease of separation, higher thermal stability, and compatibility with continuous processing improve operational economics. In practical terms, catalysts help plants increase conversion, improve selectivity, reduce waste formation, and lower energy intensity, which makes them indispensable across both mature and emerging chemical value chains.

MARKET RESTRAINTS

Dependence on Critical and Precious Metals to Restrict Market Growth

A major restraint for the market is its dependence on critical raw materials and precious metals, especially platinum-group metals in emission-control and certain chemical-process applications. The U.S. Geological Survey states that the leading domestic use for PGMs was in catalytic converters to decrease harmful emissions from automobiles, and that PGMs are also used in catalysts for bulk chemical production and petroleum refining sector. This is significant as catalyst economics can be affected not only by end-market needs, but also by fluctuations in the availability and pricing of platinum, palladium, rhodium, and related metals.

This restraint is strategically important as raw-material exposure can compress margins, complicate customer pricing, and lengthen procurement cycles in catalyst-intensive sectors. Even though companies such as BASF have built recycling and metal-management capabilities to mitigate some of this risk, the market remains sensitive to cost swings and concentrated upstream supply. As a result, catalyst suppliers must continuously balance performance targets with metal thrift, substitution, and recovery strategies in order to remain competitive.

MARKET OPPORTUNITIES

Hydrogen, Ammonia, Renewable Fuels, and Lower-Carbon Chemical Processing Create New Growth Opportunities

One of the biggest opportunities in the market is the expansion of catalysts used in low-carbon hydrogen, ammonia, methanol, and renewable fuels. Clariant stated that its Plus-series syngas catalysts support more energy-efficient production of blue hydrogen and green ammonia, while also improving the economics of existing assets. Additionally, Topsoe reported that it grew its market position in 2024 with catalyst and technology solutions for renewable fuels as well as conventional fuel segments. These developments show that catalysts are increasingly positioned as enabling technologies for decarbonization, not just for traditional refining and chemical synthesis.

This opportunity is likely to become more important as energy and chemical producers pursue lower-emission production pathways without fully replacing installed assets. Johnson Matthey’s published product-and-market structure highlights catalyst exposure across hydrogen, sustainable aviation fuels, syngas technologies, ammonia, methanol, petrochemicals, and biocatalysis, reflecting the breadth of future product demand. That showcases that catalyst suppliers with strong process know-how and application-specific R&D are well placed to benefit from both retrofits of existing plants and capacity investments in new-energy and sustainable-chemicals projects.

MARKET CHALLENGES

Managing Supply Risk, Recycling, and Performance Expectations Across Diverse End Uses Challenges Market Growth

A major challenge for the market is that catalyst suppliers must simultaneously manage supply security, recycling efficiency, and increasingly demanding performance requirements across different end uses. BASF’s ECMS business explicitly combines catalyst manufacturing with precious-metals trading and recycling, which reflects how tightly catalyst performance is linked to material recovery and metal stewardship in practice. At the same time, customers increasingly expect catalysts to deliver longer operating cycles, higher selectivity, lower pressure drop, and lower emissions without raising overall process cost.

This challenge is especially relevant as many catalyst applications are not simple one-time product sales and they involve long qualification cycles, embedded process performance guarantees, and replacement economics tied to uptime and throughput. Clariant’s upgraded syngas catalysts, for example, were positioned as drop-in solutions to improve plant economics and reduce carbon emissions, illustrating how innovation must satisfy multiple technical and sustainability criteria at once.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D in the market is increasingly focused on lower-emission process intensification, catalyst durability, and circular material management. Clariant’s recent syngas catalyst upgrades were designed to improve plant economics, reduce emissions, and support blue hydrogen and green ammonia, showing that innovation is moving toward better heat transfer, lower pressure drop, and lower lifecycle emissions rather than simple activity gains alone. BASF’s business positioning around full-loop services and precious-metal recycling also shows that catalyst innovation is extending into recovery, reuse, and raw-material optimization.

SEGMENTATION ANALYSIS

By Type

Heterogeneous Catalysts Dominate Due to Their Extensive Use in Large-Scale Continuous Industrial Operations

Based on type, the market is segmented into heterogeneous catalysts, homogeneous catalysts, and others.

Among these, the heterogeneous catalysts segment holds the dominant catalysts market share. The growth is supported by its extensive use in refining, petrochemicals, polymer production, and environmental treatment. These catalysts are preferred in many large-scale applications as they are easier to separate from reaction products, more compatible with continuous processing, and better suited for industrial operating conditions where cycle life and handling simplicity is crucial.

The homogeneous catalysts segment accounts for a significant market share, supported by its strong role in high-selectivity reactions used in specialty chemicals, fine chemicals, pharmaceuticals, and emerging bio-based processes. Advances in ligand design, improved recyclability, and greener homogeneous systems are supporting steady segment growth. The segment is expected to grow at a CAGR of 4.0% during the forecast period.

The others segment includes biocatalysts, organocatalysts, and specialized catalyst formats used in niche or emerging applications where conventional classifications do not fully capture commercial use patterns.

By Application

To know how our report can help streamline your business, Speak to Analyst

Environmental Applications Lead Due to Regulation, Scale, and Process-Efficiency Needs

Based on application, the market is segmented into environmental, chemical synthesis, polymer catalysis, petroleum refining, and others.

The environmental segment is leading the market. This is mainly driven by catalyst demand in automotive and industrial emission-control systems. BASF states that it is a global market leader in mobile emissions catalysts, and leading OEMs rely on its technologies to meet increasingly stringent standards and upcoming regulations worldwide. The broad need to control hydrocarbons, carbon monoxide, nitrogen oxides, and particulates supports strong structural demand for environmental catalysts.

The chemical synthesis segment represents significant growth application area. Johnson Matthey’s and Clariant’s public portfolios show strong catalyst exposure across syngas, ammonia, methanol, hydrogen, formaldehyde, and related process chains, while Topsoe also highlighted growth in catalyst and technology solutions for renewable fuels and conventional fuel segments. This demonstrates that catalysts remain fundamental to core industrial chemistry, especially where yield, selectivity, and energy efficiency directly shape plant economics. The segment expected to grow at a CAGR of 4.5% during the forecast period.

Others segment includes applications such as pharmaceuticals, food processing, and emerging sustainable-chemicals routes.

CATALYSTS MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Catalysts Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the dominant share of the market. This is due to its strong concentration of chemical production, refining capacity, and rapidly expanding petrochemical infrastructure. Countries such as China, India, Japan, and South Korea continue to support demand through large-scale manufacturing, fuels, chemicals, polymers, and environmental applications. The region also benefits from rising domestic consumption, industrial investment, and tighter environmental regulation, which together strengthen product demand across multiple end-use sectors.

China Catalysts Market

China’s market is one of the largest globally, with 2025 revenue at USD 7.89 billion, representing roughly 19.1% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America registers significant demand for the product, supported by refining, petrochemicals, industrial chemicals, environmental applications, and ongoing technology development linked to hydrogen and cleaner processing routes. The region also benefits from established catalyst regeneration, recycling, and precious-metals capabilities. This demand is supported by emission-control requirements and continued need for high-performance catalysts in process industries.

U.S. Catalysts Market

In 2025, the U.S. market was valued at USD 7.73 billion, driven primarily by strong demand from the industrial sector. The U.S. accounts for roughly 18.7% of global market sales.

Europe

Europe registers significant growth during the forecast period. Europe maintains a strong position in the market due to its established chemicals base, emissions-control requirements, refinery and petrochemical operations, and active decarbonization agenda. Germany remains one of the major markets in Europe due to its strong industrial, chemical, and automotive manufacturing base. The country’s role in high-value chemicals and engineering-intensive production supports consistent demand for catalysts used in emission control, specialty chemistry, and industrial process optimization.

Germany Catalysts Market

The Germany market in 2025 was valued at around USD 2.25 billion, representing roughly 5.4% of global market revenues.

U.K. Catalysts Market

The U.K. market in 2025 was valued at around USD 1.37 billion, representing roughly 3.3% of global market revenues.

Latin America

The market in Latin America is supported by demand from refining, fuels, chemicals, and selected industrial manufacturing activities. Brazil represents one of the leading country markets in Latin America due to its refining base, industrial demand, and role in regional chemicals and fuels value chains.

Brazil Catalysts Market

Brazil market in 2025 was valued at around USD 1.63 billion, representing roughly 3.9% of global market revenues.

Middle East & Africa

The Middle East & Africa market is supported mainly by refining, petrochemicals, gas processing, and industrial expansion. Demand is especially strong where large hydrocarbon-processing assets require catalysts for upgrading, treatment, and efficiency improvement. Over time, low-carbon hydrogen, ammonia, and cleaner-fuels investments may also create additional product demand in parts of the region.

GCC Catalysts Market

GCC market in 2025 was valued at around USD 2.00 billion, representing roughly 4.8% of global market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players are Expanding Catalyst Portfolios to Strengthen Their Market Positions

Competitive intensity is being shaped by portfolio reshaping and energy-transition positioning. Leading companies are adopting organic andinorganic growth strategies which shows how the market is growing with process technology and digital/service capabilities. At the same time, companies such as Clariant, BASF, Grace, Evonik, Axens, and Topsoe are using product launches, low-carbon ammonia and renewable-fuels initiatives, polypropylene catalyst licenses, and refinery-performance improvements to defend share and move into higher-value niches.

LIST OF KEY CATALYSTS COMPANIES PROFILED

- BASF SE (Germany)

- Clariant AG (Switzerland)

- Johnson Matthey plc (U.K.)

- Honeywell (U.S.)

- Topsoe A/S (Denmark)

- R. Grace & Co. (U.S.)

- Albemarle Corporation (U.S.)

- Evonik Industries AG (Germany)

- Axens (France)

- Sinopec Catalyst Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- November 2024: Clariant announced that its upgraded Plus series syngas catalysts had been successfully introduced to the market. The company said the new catalysts were designed as drop-in solutions to improve plant economics and reduce carbon emissions in syngas-linked applications.

- August 2024: BASF announced the commercial launch of Fourtiva, a new FCC catalyst for gasoil to mild-resid feedstock. BASF said the catalyst is designed to maximize butylene yields and selectivity over propylene while improving naphtha octane and limiting coke and dry gas formation.

- July 2024: Clariant Catalysts and KBR expanded their strategic collaboration in ammonia to support traditional ammonia production as well as low-carbon and carbon-free green ammonia projects, combining Clariant’s AmoMax catalysts with KBR’s K-GreeN technology.

REPORT COVERAGE

The catalysts market report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, type, and application. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report also covers several factors contributing to market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) |

| Growth Rate | CAGR of 4.3% from 2026 to 2034 |

| Segmentation | By Type, By Application, By Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 41.30 billion in 2025 and is projected to reach USD 60.22 billion by 2034.

Recording a CAGR of 4.3%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The environmental application segment is expected to lead the market during the forecast period.

Asia Pacific held the highest market share in 2025.

Tightening emission standards and broad-based industrial need for process efficiency to drives the market.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us