Sustainable Aviation Fuel Market Size, Share & Industry Analysis, By Type (Biofuel and Synthetic Fuel), By Technology (HEFA-SPK (Hydro processed Esters and Fatty Acids Synthetic Paraffinic Kerosene), FT-SPK (Fischer-Tropsch Synthetic Paraffinic Kerosene), ATJ-SPK (Alcohol-to-Jet Synthetic Paraffinic Kerosene), and Others), By Blending Capacity (5 to 30%, 30 to 50%, and Above 50%), By End Use (Commercial Aviation, Military Aviation, and Others), By Application (Fixed-Wing Aircraft and Rotary-Wing Aircraft), and Regional Forecast, 2026-2034

Sustainable Aviation Fuel Market Size & Share

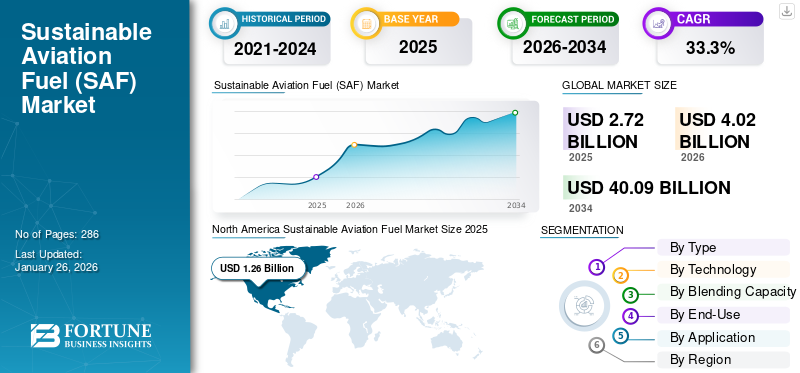

The global sustainable aviation fuel market size was valued at USD 2.72 billion in 2025 and is projected to grow from USD 4.02 billion in 2026 to USD 40.09 billion by 2034, exhibiting a CAGR of 33.3% during the forecast period. North America dominated the sustainable aviation fuel market, accounting for 46.43% of the market share in 2025.

The sustainable aviation fuel market is emerging as a critical component of aviation sector decarbonization strategies. Aviation contributes a meaningful share of global transport emissions, and regulatory pressure to reduce carbon intensity is accelerating investment in low-carbon fuel alternatives. Sustainable aviation fuel (SAF) represents the most technically feasible near-term pathway for emissions reduction because it can be blended with conventional jet fuel without requiring major aircraft redesign.

The sustainable aviation fuel market size remains relatively small compared with global jet fuel demand, yet it is expanding rapidly as airlines commit to long-term carbon reduction targets. Governments in North America and Europe have introduced policy incentives, blending mandates, and tax credits designed to accelerate SAF production capacity. These frameworks are shaping capital allocation decisions across refining companies, biofuel producers, and emerging synthetic fuel developers.

Sustainable aviation fuel market trends indicate increasing vertical collaboration between airlines, energy companies, and technology providers. Strategic partnerships are emerging to secure feedstock supply, reduce production risk, and accelerate refinery conversion projects.

Sustainable Aviation Fuel (SAF) acts as an alternative to traditional jet fuel. It is derived from non-petroleum feedstocks and plays a significant role in reducing emissions from air travel. Based on the production method and feedstock, SAF can be blended with conventional fuels at levels ranging from 10% to 50%. In 2024, the International Civil Aviation Organization (ICAO) reported that more than 360,000 commercial flights had utilized SAF across 46 airports, primarily in the U.S. and Europe.The

Globally, aviation is responsible for approximately 2% of total carbon dioxide (CO2) emissions and accounts for 12% of emissions from the transportation sector. The ICAO's Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) aims to limit the net aviation CO2 emissions to 2020 levels until 2035. Moreover, the international aviation sector has set an ambitious target to achieve net-zero carbon emissions by 2050.

Download Free sample to learn more about this report.

Sustainable Aviation Fuel (SAF) Market Key Takeaways

- 2025 Market Size: USD 2.72 billion

- 2026 Market Size: USD 4.02 billion

- 2034 Forecast Market Size: USD 40.09 billion

- CAGR: 33.3% from 2026–2034

- North America dominated the sustainable aviation fuel market with a 46.43% share in 2025.

- The biofuel segment held the largest market share of 86.03% in 2025.

- The HEFA-SPK segment is projected to lead the market with an 87.53% share in 2026.

North America

North America market is projected to grow to USD 1.88 billion in 2026, supported by strong SAF production capacity and favorable policy initiatives.

Europe

Europe accounted for 32.55% of the global market in 2025, driven by increasing aviation decarbonization efforts and regulatory mandates.

Asia Pacific

Asia Pacific held a 16.66% market share in 2025 and is expected to witness strong growth due to expanding airline investments in sustainable fuels.

U.S.

The market is projected to reach USD 1.57 billion in 2026, supported by the growing adoption of low-carbon aviation fuel solutions.

Japan

The sustainable aviation fuel market is expected to attain USD 0.21 billion in 2026, driven by the country’s commitment to reducing aviation emissions.

Read More

Sustainable Aviation Fuel (SAF) Market Dynamics

Market Trends

Corporate Sustainability Initiatives

Many airlines and aviation companies are increasingly integrating sustainability into their corporate strategies. They are investing in SAF as they have aimed for net-zero carbon emissions by 2050. This commitment will drive investment in SAF as it is a critical component of their sustainability plans. Moreover, the rise in focus on achieving these ambitious targets has encouraged partnerships between airlines and fuel producers. For instance, in November 2024, Neste and Air Canada entered a significant agreement for the supply of 60,000 tons (approximately 77.6 million liters) of Neste MY Sustainable Aviation Fuel, marking the first time that this fuel will be supplied to Canada. This initiative was made to support Air Canada's commitment to sustainability as it aims for SAF to comprise 1% of its estimated jet fuel usage by 2025. Therefore, such partnerships and agreements will foster the adoption of SAF and enhance the sustainable aviation fuel market growth.

- North America witnessed sustainable aviation fuel market growth from USD 569.5 million in 2023 to USD 848.8 million in 2024.

Sustainable aviation fuel market trends are increasingly shaped by long-term airline procurement strategies and strategic alliances across the aviation value chain. Airlines are signing multi-year offtake agreements with producers to secure supply certainty and support project financing. These agreements provide demand visibility and help de-risk large capital investments in refining infrastructure.

Refinery conversion is emerging as a key industry trend. Several traditional petroleum refineries are being retrofitted to produce renewable fuels, including SAF. This approach reduces capital requirements compared with constructing entirely new facilities while accelerating production timelines. Another notable trend involves the expansion of technology pathways beyond the currently dominant Hydroprocessed Esters and Fatty Acids Synthetic Paraffinic Kerosene (HEFA-SPK) process. Fischer-Tropsch and alcohol-to-jet technologies are receiving increasing investment as the industry seeks scalable alternatives that rely on more abundant feedstocks.

Corporate sustainability participation is also growing. Large corporations are purchasing sustainable aviation fuel certificates to offset business travel emissions. This voluntary market contributes incremental demand and reinforces long-term sustainable aviation fuel market growth.

Download Free sample to learn more about this report.

Market Drivers

Rising Demand for Alternative Fuels to Propel Market Growth

There is a rise in the awareness of climate change across the world and the urgent need to reduce greenhouse gas (GHG) emissions. The aviation industry contributes significantly to global CO2 emissions. Thus, it is increasingly adopting more sustainable practices to reduce its emissions. SAF offers a cleaner alternative to conventional jet fuels, reducing emissions by up to 80% depending on the feedstock and production method used. Jet fuel consumption produces CO2 at a defined ratio (3.16 kilograms of CO2 per 1 kilogram of fuel consumed), regardless of the phase of flight. According to the IATA estimates, SAF could account for around 65% of the reduction in emissions produced by the aviation industry to reach net-zero in 2050. And this transition needs a significant increase in production to meet demand. Therefore, the growing demand for sustainable aviation fuel is driven by increasing regulatory pressures and consumer preferences for greener travel options, prompting airlines to invest in SAF technologies.

Below is the table indicating the SAF required to achieve the goal of net-zero carbon dioxide (CO2) emissions by 2050. The long-term outlook of Sustainable Aviation Fuel is promising, with projections indicating substantial growth as more airlines commit to integrating this fuel.

Download Free sample to learn more about this report.

Therefore, the demand for SAF is increasing to help airlines fulfill their commitment to achieving net-zero emissions by 2050. Moreover, in late 2022, ICAO member states adopted a long-term global aspirational goal (LTAG) to achieve net-zero carbon emissions from international aviation by 2050. The agreement aims to reduce emissions within the sector itself. Thus, the rise in demand for alternative fuels, such as SAF, driven by environmental imperatives and corporate responsibility commitments, will create a favorable environment for the growth of the SAF market in the aviation industry. Therefore, Sustainable Aviation Fuel market trends indicate a significant shift toward increased production capabilities and technological innovations.

SAF Mandates and Regulatory Initiatives to Accelerate Market Growth

Government policies play an essential role in the deployment of SAF. There has been a rise in the formulation of policies and incentives to accelerate SAF deployment. As SAF is in the early stages of development, mandates are adopted as a means to increase the production of this fuel and are complemented with incentive programs that facilitate innovation, expansion in production capacity, and unit cost reduction. Various countries across the globe are implementing SAF mandates to regulate the usage of this fuel in the aviation industry. For instance, in December 2024, the U.K. finalized a Sustainable Aviation Fuel mandate, which is set to take effect on January 1, 2025. This initiative aims to significantly reduce greenhouse gas emissions from the aviation sector and promote the use of greener fuels. According to this mandate, 2% of all jet fuel used in the U.K. will be sourced from sustainable aviation fuels starting in 2025. By setting clear targets for SAF usage, these mandates create a predictable demand for sustainable fuels, incentivizing producers to invest in SAF production facilities and technologies. This demand is essential for scaling up the production capabilities and reducing costs associated with SAF.

Moreover, subsidies for Sustainable Aviation Fuel (SAF) play a crucial role in promoting the development and use of lower-emission fuels in the aviation sector. Governments aim to make the production of SAF more economically viable, thereby encouraging more producers to enter the market. For instance, in May 2024, the Biden administration of the U.S. released guidance on its Sustainable Aviation Fuel (SAF) subsidy program, which allows corn-based ethanol to qualify for SAF subsidies, provided it is sourced from farms employing climate-friendly agricultural practices. Such subsidies are expected to stimulate the market’s growth during the forecast period.

In addition, regulatory bodies are increasingly implementing SAF mandates and regulatory initiatives that require airlines and fuel suppliers to incorporate a certain percentage of SAF into their fuel mix. For instance, the EU's ReFuelEU Aviation Regulation mandates a gradual increase in SAF usage, starting with 2% in 2025 and reaching 70% by 2050. Such mandates by various countries and regions will create a conducive environment for the development and adoption of sustainable aviation fuels, boosting the growth of the sustainable aviation fuel industry.

New Technologies for Making SAF to Act as a Catalyst For Market Growth

New technologies for the production of Sustainable Aviation Fuel are acting as a catalyst for the market’s growth as they enhance production efficiency and reduce costs. The production of SAF is evolving beyond the widely used Hydroprocessed Esters and Fatty Acids (HEFA) technology, with several emerging technologies. For instance, in April 2024, Honeywell introduced innovative technologies aimed at enhancing the production of SAF with biomass. The company’s hydrocracking technology allows the conversion of biomass into SAF, producing fuel that is 90% less carbon-intensive than traditional fossil-based jet fuels. This technology increases SAF yield by 3-5% while enabling a cost reduction of up to 20% compared to conventional hydroprocessing methods.

Moreover, technologies, such as Alcohol-to-Jet and Fischer-Tropsch (FT) synthesis, are expected to gain traction in the coming years. Companies are increasingly dedicating resources and establishing facilities to produce Sustainable Aviation Fuel (SAF) using alternative technologies, reflecting a significant shift in the aviation fuel landscape. For instance, in January 2024, LanzaJet officially opened the Freedom Pines Fuels facility in Soperton, Georgia, marking a significant milestone as the world’s first commercial production plant for ethanol-based alcohol-to-jet sustainable aviation fuel. The emergence of these diverse production technologies is essential for fueling the SAF market and meeting the increasing global demand driven by regulatory mandates and environmental concerns.

Market Restraints

High Cost of SAF and Limited Feedstock Availability to Stifle Market Growth

The high cost of Sustainable Aviation Fuel (SAF) and limited feedstock availability are significant restraints that are expected to hamper the growth of the sustainable aviation fuel market. According to the IATA, SAF can cost between two and seven times more than traditional jet fuel, with prices around USD 2,500 per ton in 2023. This is approximately 2.8 times higher than the conventional aviation fuel prices. Such a substantial price difference creates a barrier for airlines that are highly sensitive to fuel costs. Aviation fuel expenses account for about 30-31% of their operating costs. Therefore, many airlines may feel hesitant to switch to SAF due to its high cost.

Moreover, SAF production facilities require significant capital investment, often running into hundreds of millions or even billions of dollars, depending on the technology and scale. The complexity of the manufacturing process necessitates the use of advanced infrastructure and technology, which further drives up costs. SkyNRG estimates that the global Sustainable Aviation Fuel (SAF) capacity could reach approximately 250 million tons by 2050, provided that new pathways utilizing biomass feedstocks and green hydrogen are effectively developed and de-risked. To achieve this production level, 500 to 800 SAF facilities would be necessary, requiring a cumulative investment of around USD 1 trillion, with each facility costing about USD 2 billion. This translates to an average annual capital expenditure of USD 40 billion from 2025 to 2050, which is roughly 8% of the global annual upstream oil & gas capital expenditure incurred in 2019. The high costs associated with establishing these production facilities pose a significant challenge to the rapid growth of the market.

A significant portion of the SAF currently produced is derived from feedstocks, such as used cooking oils and animal fats, which have limited availability and are often diverted for biodiesel production. This competition for feedstocks can drive up prices and limit the quantity available for SAF production. Therefore, the high cost of SAF combined with limited feedstock availability presents significant challenges that could stifle the sustainable aviation fuel market's growth.

Production economics remain the most significant constraint within the sustainable aviation fuel market. SAF production costs are typically several times higher than conventional jet fuel due to feedstock prices, refining complexity, and limited economies of scale. Airlines operating under tight margin structures are sensitive to fuel cost volatility, which slows widespread adoption without regulatory incentives.

Feedstock availability also limits production scalability. Many current SAF pathways rely on waste oils, animal fats, and agricultural residues. These materials are finite and already utilized in other biofuel industries. Competition for feedstock increases price volatility and restricts the expansion of the sustainable aviation fuel market size.

Market Opportunities

Significant opportunities within the sustainable aviation fuel market are emerging from regulatory alignment and aviation sector decarbonization commitments. Governments are increasingly implementing blending mandates requiring airlines to incorporate minimum SAF percentages within their fuel supply. These policies create guaranteed demand and encourage investment in production capacity.

Refinery diversification offers another opportunity pathway. Traditional oil and gas companies are exploring SAF production as part of broader energy transition strategies. Existing refining infrastructure and global fuel distribution networks position these firms to scale sustainable aviation fuel market growth efficiently.

Feedstock innovation represents a critical opportunity area. Technologies capable of converting agricultural waste, municipal solid waste, and non-food biomass into jet fuel could dramatically expand feedstock supply. Diversification would reduce reliance on limited waste oil streams and strengthen long-term sustainable aviation fuel market size expansion.

Emerging economies also represent underdeveloped opportunity zones. Regions with strong biomass resources and growing aviation sectors may become future SAF production hubs. Strategic investment in refining capacity and logistics infrastructure could position these markets as export suppliers.

Market Segmentation Analysis

By Type Analysis

Biofuel Held Largest Market Share in 2024 Due to Strong Push Toward Sustainability and Reduced Carbon Emissions

On the basis of type, the market is classified into biofuel and synthetic fuel.

Biofuel

The biofuel segment held the largest share of 86.03% in 202 of the Sustainable Aviation Fuel (SAF) market, driven by its compatibility with the existing aircraft and infrastructure, which allows for easier integration compared to other fuel types, such as hydrogen or synthetic fuels. There is a strong global push to reduce greenhouse gas emissions and combat climate change, which is encouraging airlines to adopt SAF to achieve these environmental goals.

Biofuel-derived products currently dominate the sustainable aviation fuel market due to their technological maturity and relatively established production pathways. Most commercial SAF supply is produced using biological feedstocks such as used cooking oil, animal fats, agricultural residues, and certain non-food oil crops. These materials are converted through processes including hydroprocessing and catalytic upgrading to produce drop-in jet fuel substitutes.

The leading technology associated with this category is Hydroprocessed Esters and Fatty Acids Synthetic Paraffinic Kerosene (HEFA-SPK). This pathway benefits from operational experience within renewable diesel production and requires relatively modest technological adaptation to produce aviation-grade fuels. As a result, HEFA-based fuels account for the majority of the current sustainable aviation fuel market size.

Biofuel SAF adoption is strongly supported by regulatory frameworks designed to reduce aviation emissions. Governments frequently provide production credits, tax incentives, or blending mandates that improve the economic viability of biofuel pathways. These incentives have been particularly influential in North America and Europe, where policy frameworks emphasize near-term carbon reduction strategies.

Synthetic Fuel

The synthetic fuel segment is expected to grow faster during the forecast period. The development of innovative production technologies, particularly the Fischer-Tropsch (FT) process, has made it possible to convert a wide range of feedstocks - including natural gas, coal, biomass, and municipal solid waste — into synthetic aviation fuels. Moreover, airlines are increasingly committing to sustainability goals by producing synthetic SAF to meet the growing demand for cleaner aviation fuels. For instance, in September 2024, Gevo, Inc. announced a definitive agreement to acquire the ethanol production plant and Carbon Capture and Sequestration (CCS) assets of Red Trail Energy, LLC for USD 210 million. This strategic acquisition is expected to significantly enhance Gevo's capabilities in producing Sustainable Aviation Fuel and further its commitment to carbon abatement.

Synthetic fuels represent a rapidly developing segment within the sustainable aviation fuel market. These fuels are produced through chemical synthesis processes that combine hydrogen and carbon sources to create liquid hydrocarbons compatible with aviation engines. Unlike biofuel pathways, synthetic fuel production does not rely on biological feedstocks and therefore offers theoretically scalable supply potential.

The most widely discussed synthetic fuel approach involves power-to-liquid technology. Renewable electricity powers electrolyzers that produce hydrogen from water. This hydrogen is then combined with captured carbon dioxide to synthesize liquid fuels through catalytic processes such as Fischer-Tropsch conversion. The resulting fuel can be refined into aviation-grade kerosene compatible with existing aircraft infrastructure. Synthetic fuels present several strategic advantages. Feedstock constraints are significantly reduced because the primary inputs—renewable electricity, water, and captured carbon—can be produced at a large scale. This characteristic supports the long-term expansion of the sustainable aviation fuel market size beyond the limitations of biological resources.

By Technology Analysis

HEFA-SPK Segment to Hold Largest Market Share Due to Its Established Production Processes and Flexibility in Feedstock Use

On the basis of technology, the sustainable aviation fuel market is classified into HEFA-SPK (Hydroprocessed Esters and Fatty Acids Synthetic Paraffinic Kerosene), FT-SPK (Fischer-Tropsch Synthetic Paraffinic Kerosene), ATJ-SPK (Alcohol-to-Jet Synthetic Paraffinic Kerosene), and others. Others include HFS-SIP (Hydroprocessed Fermented Sugars to Synthetic Isoparaffins), Co-processing, Electro-fueled sustainable aviation fuel, and other technologies used to develop SAF.

HEFA-SPK (Hydroprocessed Esters and Fatty Acids Synthetic Paraffinic Kerosene)

The HEFA-SPK (Hydroprocessed Esters and Fatty Acids Synthetic Paraffinic Kerosene) segment is projected to remain dominant in the global sustainable aviation fuel (SAF) market with a share of 87.53% in 2026, due to the availability of diverse feedstocks, such as waste fats and oils, and regulatory support promoting renewable fuels. There is also a rise in the development of low-carbon intensity feedstocks from waste oils, which will drive the growth of the segment.

Hydroprocessed Esters and Fatty Acids Synthetic Paraffinic Kerosene (HEFA-SPK) represents the most commercially established pathway within the sustainable aviation fuel market. The technology converts lipid-based feedstocks such as used cooking oil, animal fats, and certain vegetable oils into hydrocarbon fuels through hydrogenation and catalytic refining processes. Because the pathway closely resembles existing renewable diesel production methods, HEFA-SPK facilities benefit from operational familiarity and refinery integration advantages.

HEFA-SPK fuels have already received widespread regulatory certification for blending with conventional jet fuel. Aviation authorities permit blending ratios typically up to 50 percent, enabling airlines to utilize the fuel without modifications to aircraft engines or fuel infrastructure. This drop-in compatibility has accelerated early sustainable aviation fuel market growth. The pathway also benefits from existing industrial capacity. Several renewable diesel facilities have been adapted to produce aviation-grade fuels through relatively modest process adjustments. As a result, HEFA-SPK currently contributes the majority of the global sustainable aviation fuel market size.

FT-SPK (Fischer–Tropsch Synthetic Paraffinic Kerosene)

Fischer–Tropsch Synthetic Paraffinic Kerosene (FT-SPK) represents a flexible and scalable technology pathway within the sustainable aviation fuel market. The Fischer–Tropsch process converts carbon-containing feedstocks such as municipal solid waste, agricultural residues, forestry biomass, or captured carbon dioxide into liquid hydrocarbons through gasification and catalytic synthesis.

The process begins with the conversion of feedstocks into synthesis gas, a mixture of carbon monoxide and hydrogen. This gas is then passed over specialized catalysts that assemble hydrocarbon molecules suitable for jet fuel production. The resulting fuel can be refined into aviation-grade kerosene compatible with existing aircraft engines and fuel systems.

One of the key advantages of FT-SPK technology is feedstock diversity. Unlike HEFA-based production, Fischer–Tropsch processes can utilize a broader range of raw materials. This flexibility enhances the long-term scalability of the sustainable aviation fuel market and reduces dependence on limited biological feedstocks.

However, capital intensity remains a significant barrier. Gasification plants and synthesis facilities require large-scale infrastructure investment, and project development timelines can be lengthy. Feedstock logistics and supply chain management also add operational complexity.

Despite these challenges, FT-SPK is gaining increasing investor interest. Several demonstration and commercial-scale projects are under development globally. As these facilities reach operational maturity, the technology could contribute meaningfully to long-term sustainable aviation fuel market growth.

ATJ-SPK (Alcohol-to-Jet Synthetic Paraffinic Kerosene)

The ATJ-SPK (Alcohol-to-Jet Synthetic Paraffinic Kerosene) segment is estimated to record the highest CAGR during the forecast period. The development of advanced technologies, such as the PureSAFSM technology, has expanded the range of alcohols that can be used as feedstocks for ATJ-SPK production. This technology allows the use of various alcohols (ethanol, propanol, butanol, and pentanol) either individually or in mixtures, enhancing flexibility and cost-effectiveness in SAF production. In addition, the ATJ method is being actively employed in both commercial production and experimental settings. For instance, in December 2023, a test flight was conducted demonstrating the conversion of methanol to SAF. This event took place in Dubai during the COP28 climate conference and involved collaboration among several key players, including Masdar, TotalEnergies, the UAE General Civil Aviation Authority, Airbus, Falcon Aviation Services, and technology licensor Axens. The FT-SRK segment is expected to hold a 4.7% share in 2024.

Alcohol-to-Jet Synthetic Paraffinic Kerosene (ATJ-SPK) technology converts alcohol-based feedstocks such as ethanol or isobutanol into aviation fuel through catalytic upgrading processes. The pathway involves dehydration, oligomerization, and hydrogenation steps that transform alcohol molecules into hydrocarbon chains compatible with jet fuel specifications. This technology benefits from the extensive global ethanol production infrastructure. Many regions already produce large volumes of ethanol derived from corn, sugarcane, or cellulosic biomass. Converting a portion of this supply into aviation fuel could significantly expand the sustainable aviation fuel market size.

The ATJ pathway also provides feedstock flexibility. Both agricultural and cellulosic alcohols can serve as inputs, enabling producers to utilize a wide range of biomass sources. This diversity supports the potential long-term expansion of the sustainable aviation fuel market.

To know how our report can help streamline your business, Speak to Analyst

By Blending Capacity

30 to 50% Segment Held Largest Market Share in 2024 Due to Rapid Transition Toward Higher Use of SAF to Achieve Net Zero Targets

On the basis of blending capacity, the market is classified into 5% to 30%, 30% to 50%, and above 50%.

5–30%

The 5–30 percent blending category currently represents the most widely utilized range within the sustainable aviation fuel market. Most airlines operating SAF today rely on blends within this range due to regulatory certifications and operational familiarity. Aviation authorities have approved several SAF pathways for blending with conventional jet fuel at varying limits, but airlines often begin with lower blending ratios during early adoption phases.

This blending range allows airlines to reduce lifecycle carbon emissions while maintaining operational stability across existing fleets. Because sustainable aviation fuels are chemically compatible with conventional jet fuel, these blends can be transported through standard fuel distribution systems and utilized without aircraft engine modification.

Airlines typically adopt lower blending ratios when supply availability is limited. SAF production remains significantly lower than total jet fuel demand, which means operators must distribute available supply across multiple routes or flights. Consequently, 5–30 percent blends provide a practical approach for scaling sustainable aviation fuel market growth while supply constraints persist. Another advantage of this range lies in cost management. SAF remains more expensive than conventional jet fuel, and lower blending ratios help airlines balance sustainability commitments with fuel cost control. As production capacity increases and economies of scale improve, higher blending levels may become economically viable.

30–50%

The 30% to 50% segment is projected to dominate the market with a share of 73.76% in 2026. The segment’s dominance is attributed to the net-zero commitment taken by various airlines and airports. Many airlines are adopting sustainability as a core element of their business strategies, which includes increasing the use of SAF. For instance, in April 2023, Ryanair, Europe’s prominent airline, announced a significant expansion of its partnership with Neste, a leading supplier of sustainable aviation fuel. Starting April 1, 2023, Ryanair committed to powering 100% of its flights from Amsterdam Airport Schiphol (AMS) with a 40% SAF blend. The segment with a blending capacity of 30% to 50% is particularly attractive as it allows airlines to transition gradually toward higher SAF usage while maintaining operational reliability.

The 30–50 percent blending range represents a transitional stage within the sustainable aviation fuel market as the aviation industry moves toward deeper decarbonization targets. Several SAF pathways, including HEFA-SPK and Fischer–Tropsch synthetic kerosene, have received certification for blending up to 50 percent with conventional jet fuel. Airlines pursuing aggressive sustainability commitments are increasingly experimenting with higher blend ratios within this range. Demonstration flights and pilot programs have shown that these blends maintain safe operational performance while significantly reducing lifecycle carbon emissions compared with conventional fuels.

However, supply limitations remain a key constraint. Producing sufficient SAF volumes to support large-scale adoption of 30–50 percent blends requires significant expansion of refining capacity. Current production infrastructure remains insufficient to support widespread high-blend deployment across global airline networks. Cost considerations also influence adoption. Higher blending ratios increase fuel expenses because SAF carries a price premium over traditional jet fuel. Airlines often rely on government incentives, tax credits, or corporate sustainability partnerships to offset these costs.

Above 50%

The above 50% segment is estimated to be the fastest-growing segment owing to regulatory support and government initiatives. Many governments are implementing stringent regulations aimed at reducing carbon emissions in the aviation sector. These regulations often encourage or mandate the use of higher blends of SAF, pushing airlines to adopt fuels that exceed 50% SAF content to comply with future emissions targets.

Blending ratios above 50 percent represent the long-term vision for the sustainable aviation fuel market, although current regulatory certifications generally limit most SAF pathways to 50 percent blends with conventional jet fuel. Achieving higher blend levels will require additional technological validation and regulatory approval processes. Research and testing programs are exploring the potential for 100 percent sustainable aviation fuel usage. Several demonstration flights using fully synthetic or bio-derived fuels have been completed under controlled conditions. These tests aim to confirm compatibility with aircraft engines, fuel systems, and safety standards.

From a sustainability perspective, higher blending levels offer substantial emissions reduction potential. Lifecycle carbon reductions can exceed 80 percent depending on feedstock type and production pathway. Consequently, airlines and policymakers view higher blends as a critical step toward achieving long-term net-zero aviation goals. However, large-scale adoption faces multiple barriers. Production capacity must expand dramatically to supply sufficient SAF volumes for widespread high-blend operations. Certification processes also require extensive testing across aircraft platforms and engine types.

By End Use Analysis

Commercial Aviation Segment Held the Largest Market Share in 2024 Due to Rising Awareness Of Sustainability and Environmental Effects of Traditional Jet Fuel

On the basis of end use, the market is classified into commercial aviation, military aviation, and others. Others include business and general aviation.

Commercial Aviation

The commercial aviation segment is expected to lead the market, contributing 69.69% globally in 2026 due to increasing awareness about sustainability and the environmental impact of traditional jet aviation fuel. There is a rise in the recognition of the aviation sector's impact on climate change, prompting both consumers and airlines to pursue more sustainable alternatives to traditional jet fuels. As passengers become more environmentally conscious, airlines are responding by integrating SAF into their operations.

Commercial aviation represents the dominant demand segment within the sustainable aviation fuel market. Airlines are under increasing pressure from regulators, investors, and customers to reduce carbon emissions associated with air travel. Sustainable aviation fuel provides the most immediate decarbonization pathway because it can be used within existing aircraft fleets without requiring structural redesign.

Large commercial carriers have announced ambitious carbon reduction targets for 2030 and net-zero commitments for 2050. These commitments are translating into long-term fuel procurement strategies. Many airlines have already entered into multi-year SAF offtake agreements with producers, ensuring supply while supporting project financing for new production facilities.

Passenger aviation accounts for the majority of jet fuel consumption globally, which naturally positions this segment as the primary contributor to the sustainable aviation fuel market size. Airlines are gradually incorporating SAF blends into scheduled flights as production volumes increase. Airport infrastructure is also evolving to accommodate SAF distribution. Fuel suppliers and airport operators are investing in blending and storage facilities that allow sustainable fuels to be integrated into existing supply chains.

Military Aviation

The military aviation segment is estimated to be the fastest-growing segment owing to the rise in defense budgets and an increase in investment in sustainable technologies. Many countries are ramping up their defense spending, which includes investments in sustainable technologies. Moreover, military and commercial aviation companies are collaborating, which is expected to drive the development of SAF. For instance, in October 2024, Norwegian Airlines and the Norwegian Armed Forces participated in a significant initiative to promote the use of SAF at Ålesund Airport Vigra. This event marked a pivotal step in developing the SAF market in Norway, showcasing a collaborative effort to reduce carbon emissions in aviation.

In addition, there is growing recognition of the importance of sustainability in defense operations. For instance, in August 2024, the Royal Air Force (RAF) made significant strides in integrating SAF into its operations, particularly with its Typhoon fighter jets and P-8A Poseidon submarine hunters. Such developments are expected to drive the growth of the sustainable aviation fuel market.

Military aviation represents a smaller but strategically important segment of the sustainable aviation fuel market. Defense organizations worldwide are exploring alternative fuels to enhance energy security while reducing operational carbon footprints. Military aircraft fleets consume substantial volumes of aviation fuel, particularly during training exercises and operational deployments. Incorporating SAF blends into these operations can reduce reliance on conventional petroleum supply chains and improve long-term fuel resilience.

Several defense departments have initiated pilot programs to evaluate the performance of sustainable aviation fuels across different aircraft platforms. These programs focus on compatibility testing, operational reliability, and supply chain logistics. Military adoption patterns differ from commercial aviation. Defense procurement processes typically emphasize fuel security and performance reliability rather than purely economic considerations. As a result, governments may support SAF research and procurement even when costs remain higher than conventional alternatives.

By Application Analysis

Fixed-Wing Aircraft Segment Held the Largest Market Share Due to Supportive Governments' Incentives and Subsidies

On the basis of application, the market is classified into fixed-wing aircraft and rotary-wing aircraft.

Fixed-Wing Aircraft

The fixed-wing aircraft segment dominated the global market in 2024. Various governments are providing incentives and subsidies for the development and use of SAF, encouraging airlines operating fixed-wing aircraft to adopt these fuels. Various fixed-wing aircraft manufacturers are focused on developing and testing aircraft for the use of SAF to make a clear pathway for fixed-wing aircraft to operate on 100% SAF. For instance, in November 2024, Deutsche Aircraft and Pratt & Whitney Canada conducted test flights using a fully synthetic Fischer-Tropsch fuel in the D328® UpLift research aircraft. The synthetic Fischer-Tropsch fuel used in these flights can potentially reduce carbon emissions by up to 95% compared to conventional jet fuels.

Fixed-wing aircraft account for the overwhelming majority of demand within the sustainable aviation fuel market. Commercial airliners, cargo aircraft, and military transport platforms all rely on fixed-wing propulsion systems, which collectively consume the largest share of global aviation fuel. As a result, this segment represents the dominant contributor to the sustainable aviation fuel market size.

The compatibility of SAF with existing turbine engines used in fixed-wing aircraft is a primary factor supporting adoption. Certified SAF blends can be utilized within current aircraft fleets without modifications to engines, fuel tanks, or airport fueling infrastructure. This drop-in capability significantly lowers barriers to entry compared with alternative propulsion technologies. Commercial airlines represent the most significant source of SAF demand within this category. Passenger transport networks require large fuel volumes, making them central to sustainable aviation fuel market growth. Cargo aviation operators are also gradually incorporating SAF blends as logistics companies pursue supply chain decarbonization initiatives.

Rotary-Wing Aircraft

The rotary-wing aircraft segment is estimated to be the fastest-growing segment during the forecast period. The use of helicopters in emergency services creates a stable demand for aviation fuel. Transitioning these operations to SAF can significantly reduce emissions generated from critical services. Moreover, the rise in partnerships between helicopter manufacturers, fuel suppliers, and regulatory bodies is fostering innovation and investment in SAF production tailored for rotary-wing aircraft. For instance, in February 2023, Air bp announced an ongoing supply of sustainable aviation fuel to the Austrian rescue helicopter operator, Christophorus Flugrettungsverein (CFV). The initial delivery of SAF was made in October 2022 at CFV's heliport in Innsbruck.

Rotary-wing aircraft, including helicopters used in civil, emergency response, offshore energy, and military operations, represent a smaller but specialized segment of the sustainable aviation fuel market. Although total fuel consumption in rotary aviation is lower than in fixed-wing aircraft, these platforms offer important early adoption opportunities for SAF deployment.

Helicopter operations frequently occur in environments where environmental considerations and regulatory compliance are highly visible. Offshore energy transport, search and rescue operations, and medical evacuation services often operate under strict environmental oversight. Incorporating sustainable aviation fuel can help reduce operational emissions while maintaining existing aircraft performance characteristics. Many rotary-wing aircraft utilize turbine engines similar to those found in fixed-wing aviation, enabling compatibility with certified SAF blends. As a result, adoption does not require major aircraft design modifications, which simplifies implementation.

Regional Insights

The global market is segmented on the basis of region into North America, Europe, Asia Pacific, the Middle East, Africa, and Latin America.

North America Sustainable Aviation Fuel Market Size 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The

In 2025, the North America market stood at USD 1.26 billion, representing 46.43% of global demand, and is projected to grow to USD 1.88 billion in 2026, and is likely to remain dominant throughout the forecast period due to the stringent emission regulations and supportive government initiatives and incentives. The U.S. government has implemented various policies, including tax incentives and the Sustainable Aviation Fuel Grand Challenge, aiming to produce at least 3 billion gallons of SAF annually by 2030.

North America represents the most advanced region within the sustainable aviation fuel market due to strong policy support, airline commitments, and refinery conversion initiatives. Federal tax incentives and state-level low-carbon fuel standards encourage production expansion. Major energy companies are investing in SAF refining capacity. As supply chains mature and airline offtake agreements expand, the region will continue contributing significantly to sustainable aviation fuel market growth.

Moreover, the presence of prominent SAF suppliers, such as Neste and Shell, is expected to promote the adoption of SAF in the region. The Sustainable Skies Act, introduced in May 2021 by U.S. Congressman Brad Schneider, aims to significantly enhance the use of SAF in the aviation sector. This legislation is part of a broader effort to reduce greenhouse gas (GHG) emissions from air travel, which currently accounts for approximately 2.5% of global carbon emissions. Therefore, fuel producers are incentivized to invest in SAF technologies and infrastructure, which drives the growth of the market in North America during the forecast period.

United States sustainable aviation fuel market

The United States dominates the North American sustainable aviation fuel market, supported by federal incentives, corporate sustainability initiatives, and strong airline demand. Several refinery conversion projects and new production facilities are under development. Long-term offtake agreements between airlines and fuel producers strengthen supply certainty. Continued policy support and private investment position the country as a key driver of global sustainable aviation fuel market size expansion. The U.S. market is poised to be valued at USD 1.57 billion in 2026.

Europe Sustainable Aviation Fuel Market Analysis

Europe plays a central role in the sustainable aviation fuel market growth through stringent aviation decarbonization policies. Regulatory initiatives such as SAF blending mandates are encouraging airlines and fuel suppliers to accelerate adoption. European energy companies are investing heavily in renewable fuel production facilities. Collaborative projects between airlines, governments, and technology developers are strengthening regional sustainable aviation fuel market share and advancing industry innovation.

The Europe region captured 32.55% of the global market in 2025, generating USD 0.89 billion in revenue, and is projected to reach USD 1.31 billion in 2026. The region is increasingly progressing in the adoption of SAF, which is supported by stringent regulations aimed at reducing carbon emissions.

The European Union has set ambitious targets for SAF usage in aviation, including the requirement for a minimum share of e-kerosene by 2030. The ReFuelEU Aviation Regulation, enacted in 2023, highlights a significant step taken by the EU toward decarbonizing the aviation sector. This regulation establishes mandatory targets for the use of Sustainable Aviation Fuel as a blend with conventional jet fuel, aiming to reduce CO2 emissions from air travel. Such commitments to reduce carbon emissions in the aviation industry are expected to act as a booster for the Sustainable Aviation Fuel (SAF) market growth. Germany is expected to grow with a value of USD 0.42 billion in 2026, while France is expected to reach USD 181.52 million in 2025.

United Kingdom sustainable aviation fuel market

The U.K. market is projected to acquire USD 0.45 billion in 2026. The United Kingdom sustainable aviation fuel market is expanding through government-backed incentives and aviation sector decarbonization commitments. National policy frameworks are encouraging investment in domestic SAF production capacity. Airlines and fuel suppliers are collaborating on long-term supply agreements. As new production facilities are developed, the United Kingdom is expected to strengthen its position within the broader sustainable aviation fuel market.

Germany's sustainable aviation fuel market

Germany is emerging as a strategic contributor to the European sustainable aviation fuel market. The country’s strong industrial base and advanced research infrastructure support SAF technology development. Partnerships between airlines, energy companies, and research institutions are driving pilot projects and refinery innovation. As national climate policies strengthen, Germany is expected to contribute steadily to sustainable aviation fuel market growth within the region.

Asia-Pacific Sustainable Aviation Fuel Market Analysis

Asia Pacific maintained a strong presence in the global market, reaching USD 0.45 billion in 2025, accounting for 16.66% share, and is expected to reach USD 0.66 billion in 2026. The region is witnessing significant growth potential due to increasing air traffic and environmental concerns. Countries, such as Japan and Australia, are beginning to invest in SAF production technologies. For instance, in 2023, the Airbus H125 helicopter operated by State Grid Space Technology Co., Ltd (SGST) completed the first helicopter flight using Sustainable Aviation Fuel (SAF) in China. The Chinese market is estimated to attain USD 0.23 billion in 2026. This flight demonstration took place at the Hefei Shiwan Airport and utilized a blend of 40% SAF provided by China National Aviation Fuel (CNAF). Various countries are increasingly implementing eco-friendly practices, which encourage more developments in the use of sustainable fuels in aviation. India is predicted to stand at USD 0.14 billion in 2026.

Asia-Pacific represents an emerging growth region within the sustainable aviation fuel market. Rapid expansion of air travel and rising environmental awareness are encouraging regional governments to explore SAF adoption strategies. Several countries are initiating pilot production facilities and research programs. As aviation demand continues to grow, the Asia-Pacific region is expected to contribute increasingly to the global sustainable aviation fuel market size expansion.

Japan's sustainable aviation fuel market

Japan is actively advancing sustainable aviation fuel adoption as part of broader carbon reduction strategies. Airlines, energy companies, and government agencies are collaborating to develop domestic SAF production capacity. The country’s strong technology ecosystem supports innovation in advanced fuel conversion pathways. These initiatives are expected to contribute gradually to sustainable aviation fuel market growth across the Asia-Pacific region. Japan is expected to reach USD 0.21 billion in the same year.

China's sustainable aviation fuel market

China is exploring sustainable aviation fuel as part of its broader energy transition strategy. Research institutions and energy companies are investigating multiple production pathways, including biomass conversion and synthetic fuel technologies. Growing aviation demand and increasing environmental policy focus may accelerate SAF adoption in the coming decade, supporting the gradual expansion of the sustainable aviation fuel market within the country.

Rest of the World

The Rest of the World market generated USD 0.12 billion in 2025, representing 4.37% of the global market landscape, and is expected to reach USD 0.17 billion in 2026. Furthermore, research into alternative fuels is gaining traction in Latin America and Africa, where there is potential for using agricultural residues and waste oils for SAF production. Various countries in Latin America are implementing mandates to encourage and regulate the adoption of sustainable aviation fuel. For instance, in October 2024, the Brazilian government approved the “Fuel of the Future” law, which promotes the production and use of sustainable aviation fuels, positioning Brazil as a leader in global aviation decarbonization. In addition, the International Air Transport Association (IATA) has urged South Africa to prioritize the development of SAF, highlighting the country's potential to produce between 3.2 and 4.5 billion liters annually from abundant feedstocks, such as sugarcane by-products and biomass waste. Such a push toward the use of SAF through several strategic initiatives and advocacy efforts is anticipated to fuel the growth of the market.

Latin America possesses significant potential within the sustainable aviation fuel market due to abundant biomass resources and agricultural feedstock availability. Several countries are evaluating SAF production opportunities linked to regional aviation demand. Although current adoption remains limited, strategic investments in refining infrastructure and export-oriented production could support future sustainable aviation fuel market growth.

The Middle East and Africa region is gradually exploring opportunities within the sustainable aviation fuel market. Aviation hubs in the Gulf region are evaluating SAF supply partnerships to support airline decarbonization commitments. Investment in renewable energy and hydrogen production could enable synthetic fuel development, potentially strengthening the region’s role in future sustainable aviation fuel market growth.

Sustainable Aviation Fuel Industry Competitive Landscape

Key Players Focus On the Development of Technologically Advanced Products and Acquisition Strategies to Drive Growth

Prominent market players are prioritizing the advancement of their product offerings. The development of a diverse range of solutions and heightened investment in research & development are key factors contributing to the market dominance of these players. The market is led by several players operating in this industry. Major players are aiming to invest heavily in SAF production technologies and facilities to increase their sustainable aviation fuel (SAF) market share. They are working on innovative projects that capture CO2 and convert it into usable materials, thereby aligning with their sustainability goals.

The sustainable aviation fuel market features a complex competitive structure involving energy companies, biofuel technology developers, refining firms, and aviation stakeholders. Competition centers on feedstock access, refining capacity, technology pathways, and long-term airline supply agreements. Because SAF production remains capital-intensive, market leadership is typically held by organizations capable of integrating fuel production, logistics infrastructure, and aviation partnerships.

Large energy companies are currently the most influential participants in the sustainable aviation fuel market. Their existing refining infrastructure, global fuel distribution networks, and capital resources enable rapid scaling of SAF production. Many traditional refiners are converting or retrofitting petroleum facilities to process renewable feedstocks. This transition allows them to leverage existing assets while participating in sustainable aviation fuel market growth.

Biofuel technology companies represent another important competitive layer. These firms focus on developing advanced fuel conversion technologies such as hydroprocessed esters and fatty acids, synthetic paraffinic kerosene, Fischer–Tropsch synthetic paraffinic kerosene, and alcohol-to-jet synthetic paraffinic kerosene. Their innovations improve production efficiency, diversify feedstock options, and enhance fuel yield. Technology licensing partnerships between these developers and large refiners are increasingly common.

Airlines are also becoming strategic participants within the sustainable aviation fuel market ecosystem. Many carriers have entered long-term offtake agreements with fuel producers to secure SAF supply. These contracts provide demand certainty for producers while helping airlines meet carbon reduction commitments. Such agreements significantly influence sustainable aviation fuel market share distribution among producers.

LIST OF TOP SUSTAINABLE AVIATION FUEL (SAF) COMPANIES:

- Neste (Finland)

- World Energy (U.S.)

- Gevo, Inc. (U.S.)

- Alder Fuels (U.S.)

- SkyNRG (Netherlands)

- Air BP (U.K.)

- Shell Aviation (Netherlands)

- TotalEnergies (France)

- Vitol Aviation (Switzerland)

- LanzaTech (U.S.)

- Fulcrum Bioenergy (U.S.)

Latest Sustainable Aviation Fuel Industry Developments

January 2025: Neste – Expanded its renewable fuel production capacity through upgrades at its Singapore refinery to increase sustainable aviation fuel output. The strategic purpose was to strengthen supply availability for global airline customers and support rising SAF demand. The expansion utilizes hydroprocessed esters and fatty acids synthetic paraffinic kerosene (HEFA-SPK) technology to convert waste oils and fats into aviation-grade renewable fuel.

October 2024: World Energy commissioned additional SAF processing capacity at its California renewable fuel facility to increase supply for commercial airlines operating in North America. The initiative aims to address accelerating sustainable aviation fuel market growth and secure long-term supply contracts with airline operators. The project incorporates advanced hydrotreating processes designed for renewable jet fuel production.

July 2024:TotalEnergies announced the conversion of selected European refining units to support large-scale sustainable aviation fuel production. The strategic objective is to expand renewable fuel capacity while aligning refinery operations with aviation decarbonization goals. The facility upgrade integrates biomass processing capabilities and advanced fuel conversion technologies.

May 2024: Shell strengthened its sustainable aviation fuel supply network through agreements with major airline operators to expand SAF distribution at key international airports. The initiative supports aviation industry carbon reduction commitments while strengthening Shell’s position within the sustainable aviation fuel market. The program integrates bio-based feedstock processing and global fuel logistics infrastructure.

March 2024: BP initiated development of an integrated renewable fuels project designed to increase sustainable aviation fuel production using waste-based feedstocks. The project aims to supply SAF to airline partners under long-term offtake agreements while expanding low-carbon fuel capabilities. The facility incorporates hydroprocessing technology optimized for renewable aviation fuel synthesis.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on important aspects, such as key players, types, technologies, and applications, depending on various regions. Moreover, it offers deep insights into the market trends, competitive landscape, market competition, product pricing, and market status, and highlights key industry developments. Also, it encompasses several direct and indirect factors that have contributed to the growth of the global market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 33.3% from 2025 to 2034 |

|

Segmentation |

By Type, Technology, Blending Capacity, End Use, and Application |

|

By Type · Biofuel · Synthetic Fuel |

|

|

By Technology · HEFA-SPK (Hydroprocessed Esters and Fatty Acids Synthetic Paraffinic Kerosene) · FT-SPK (Fischer-Tropsch Synthetic Paraffinic Kerosene) · ATJ-SPK (Alcohol-to-Jet Synthetic Paraffinic Kerosene) · Others |

|

|

By Blending Capacity · 5 to 30% · 30 to 50% · Above 50% |

|

|

By End Use · Commercial Aviation · Military Aviation

|

|

|

By Application · Fixed-Wing Aircraft

|

|

|

By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 2.72 billion in 2025 and is projected to reach USD 40.09 billion by 2034.

Registering a CAGR of 33.3%, the market will exhibit significant growth over the forecast period of 2026-2034.

By type, the biofuel segment led the market.

Neste is the leading player in the market.

North America dominated the market in terms of share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 286

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us