Green Hydrogen Market Size, Share & Industry Analysis, By Technology (PEM Electrolyzer, Alkaline Electrolyzer and Others), By Power Source (Solar-Powered Electrolysis, Wind-Powered Electrolysis, Hydropower-Based Electrolysis and Others), By Application (Transportation, Power Generation, Industrial and Others), and Regional Forecast, 2026-2034

Green Hydrogen Market Size and Future Outlook

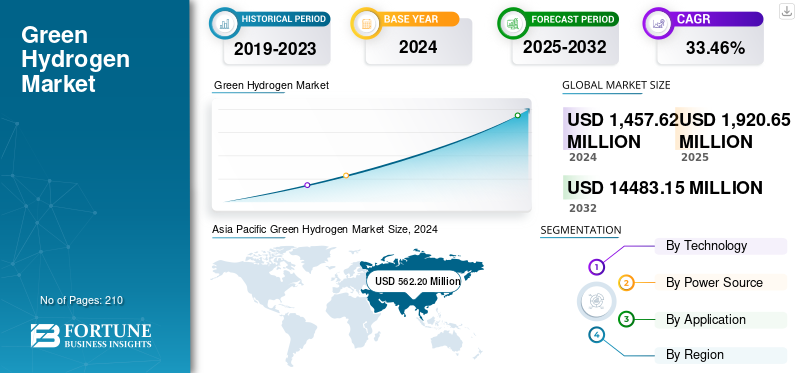

The global green hydrogen market size was valued at USD 1.92 billion in 2025 and is projected to grow from USD 2.53 billion in 2026 to USD 27.52 billion by 2034, exhibiting a CAGR of 34.74% during the forecast period. Asia Pacific dominated the global green hydrogen market with a market share of 38.64% in 2025. Countries are prioritizing green hydrogen to reduce carbon emissions and enhance energy independence.

Green hydrogen is a clean energy carrier produced through the electrolysis of water, where renewable electricity sources, such as solar, wind, or hydropower, are used to split water into hydrogen and oxygen. This method is carbon-neutral as it does not emit greenhouse gases during the production process, making it an environmental friendly alternative to hydrogen produced from fossil fuels.

Key market drivers include supportive government policies and incentives, growing investments in renewable energy sources such as solar and wind (which lower production costs), and advancements in electrolysis technology.

- For instance, Saudi Arabia is aggressively advancing its green hydrogen sector, with a USD 10 billion investment plan led by the Public Investment Fund to develop manufacturing facilities. The NEOM Green Hydrogen Project, slated to be the world's largest utility-scale facility, is expected to produce 250,000 tons annually by 2026. Such developments are expected to place hydrogen as a key energy source in the coming years.

Linde plc holds a leading and prominent position in market, leveraging its extensive expertise and infrastructure across the entire hydrogen value chain. The company is a key global player, actively investing in and developing large-scale production, processing, storage, and distribution solutions for clean hydrogen. Moreover, large players such as ENGIE, Mitsubishi Power, Enapter, Snam S.P.A. Cummins Inc. and other are also contributing to the market growth.

Download Free sample to learn more about this report.

GREEN HYDROGEN MARKET KEY TAKEAWAYS:

- 2025 Market Size: USD 1.92 billion

- 2026 Market Size: USD 2.53 billion

- 2034 Forecast Market Size: USD 27.52 billion

- CAGR: 34.74% from 2026–2034

- Asia Pacific dominated the green hydrogen market with a 38.64% share in 2025.

- The alkaline electrolyzer segment is projected to hold a 46.64% market share in 2026.

- The solar-powered electrolysis segment is expected to account for 54.94% of the market in 2026.

North America

North America was valued at USD 0.24 billion in 2025 and is projected to reach USD 0.32 billion in 2026, benefiting from government incentives, hydrogen hub investments, and expanding clean energy infrastructure.

Europe

Europe generated USD 0.57 billion in 2025 and is expected to reach USD 0.74 billion in 2026, supported by carbon neutrality targets and growing electrolyzer capacity across major economies.

Asia Pacific

Asia Pacific accounted for USD 0.74 billion in 2025 and is projected to reach USD 1.0 billion in 2026, driven by large-scale renewable energy investments and strong hydrogen development policies across China, Japan, India, and Australia.

U.S.

The green hydrogen market is forecast to reach USD 0.24 billion by 2026, fueled by federal support programs, renewable-powered electrolyzer projects, and increasing demand from transportation and industrial sectors.

Japan

The market is projected to attain USD 0.11 billion by 2026, supported by national hydrogen strategies, fuel cell deployment initiatives, and investments in clean energy infrastructure.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Decarbonization Mandates and Net-Zero Targets Drive Market Growth

Decarbonization mandates and net-zero targets are pivotal drivers for the green hydrogen market growth. Governments worldwide are enforcing stringent carbon reduction policies and sustainability commitments, prompting industries such as steel, refining, and transportation to adopt clean hydrogen as an alternative. This regulatory pressure accelerates investment in green hydrogen infrastructure and technology, facilitating large-scale production.

- For instance, in 2022, the European Commission announced that the sale of new CO2-emitting cars and vans would be banned across the EU by 2035 as part of its goal to achieve climate neutrality by 2050. Targets include a 55% reduction in CO2 emissions for cars and a 50% reduction for vans by 2030, compared to 2021 levels. From 2035 onward, all new cars and vans must have zero emissions, ensuring the transport sector becomes carbon-neutral.

Additionally, rising global climate ambitions and corporate ESG goals further bolster demand for green hydrogen. Green hydrogen’s zero-emission profile when produced via renewable-powered electrolysis makes it an essential solution for achieving deep decarbonization across hard-to-abate sectors. Combined with falling renewable energy costs and rapid advancements in electrolyzers, these mandates are transforming green hydrogen into a scalable, cost-competitive cornerstone of the global clean energy transition. This is driving innovation, fostering partnerships, and promoting cross-border hydrogen trade initiatives, thereby ensuring sustained market growth.

Industrial & Mobility Integration is Expected to Boost Market Growth

Industrial and mobility integration serve as critical market drivers for the green hydrogen sector, enabling decarbonization of heavy industries and transportation. Green hydrogen offers a clean alternative for sectors such as steelmaking, refining, chemical production, and shipping, which traditionally relied on fossil fuels and faced significant emissions challenges. It enables the replacement of carbon-intensive processes, such as use of coke in reduced iron production and fossil-derived hydrogen in refineries.

In mobility, hydrogen fuel cells power heavy vehicles, ships, and trains, offering longer range and faster refueling than batteries. Growing policy support, advances in electrolyzer technology, and declining renewable energy costs are amplifying the role of green hydrogen in the industrial and transportation sectors, driving demand for scalable, zero-emission solutions that align with global net-zero ambitions and sustainable development goals.

MARKET RESTRAINTS

Limited Hydrogen Production Infrastructure to Restraint Market Growth

Limited hydrogen production infrastructure significantly restricts the growth of market. The current global infrastructure, including production facilities, storage, pipelines, and refueling stations, remains underdeveloped and capital-intensive to expand. The industry faces challenges such as high initial investments, a lack of standardized regulations, and logistical complexities in transportation and distribution. The scarcity of large-scale electrolyzer manufacturing and insufficient integration with existing energy systems further hamper scalability.

Additionally, infrastructure gaps limit the reliable supply and commercial viability needed to meet growing industrial and mobility demand. Without robust policy support, public-private partnerships, and coordinated international efforts, infrastructure limitations pose a substantial barrier to the widespread adoption and market expansion of green hydrogen, despite rising demand and technological advancements. Addressing these issues is crucial for unlocking the full potential of green hydrogen in the global energy transition.

MARKET OPPORTUNITIES

Energy Storage & Grid Balancing to Create Opportunities

Energy storage and grid balancing present significant opportunities for the market. Green hydrogen can store excess renewable energy generated from intermittent sources, such as solar and wind, providing a stable, long-term energy reservoir that enhances grid reliability. Unlike batteries that discharge energy over hours, hydrogen stores energy for months without significant loss, enabling supply during periods of low renewable generation.

- In November 2025, Enectron launched large-scale Battery Energy Storage Systems (BESS) for utility and commercial, and industrial applications, integrating advanced lithium-ion technology and intelligent controls. Their scalable systems support India’s renewable energy goals by enabling reliable, round-the-clock clean power, which is crucial for country’s target of 500 GW of renewables by 2030.

This capability supports deeper integration of renewables, reduces curtailment, and stabilizes power supply. Additionally, green hydrogen’s versatility across various sectors, including industrial feedstocks, fuel cells for transportation, and residential heating, creates diverse market applications. As governments invest in hydrogen infrastructure and storage technologies, these factors collectively boost demand and foster innovation, positioning green hydrogen as a critical enabler of a resilient, decarbonized energy system globally.

MARKET CHALLENGES

Supply-Chain Concentration Creates Challenges the Market Growth.

Concentration in the green hydrogen supply chain poses significant challenges to market growth. Key issues include reliance on a limited number of suppliers for critical components, such as electrolyzers, catalysts, and renewable energy inputs, which can lead to bottlenecks and price volatility. Geographic concentration in regions with strong policy support or advanced manufacturing capabilities further increases the risk of supply disruptions due to geopolitical tensions, trade barriers, or natural disasters.

Moreover, immature logistics for hydrogen storage, transport, and distribution complicate timely delivery, increasing costs and limiting scalability. The lack of standardized technologies and regulations adds complexity to the integration of global supply chains. Overcoming these challenges requires diversification of suppliers, robust infrastructure investments, and coordinated international cooperation to ensure the production and deployment of resilient, efficient, and sustainable green hydrogen worldwide.

GREEN HYDROGEN MARKET TRENDS

Shift to Gigawatt-Scale Electrolyzer Projects is Emerging as a Key Trend

The market is witnessing a significant trend toward gigawatt-scale electrolyzer projects, driven by the need to meet growing industrial and mobility demand for clean hydrogen. Major energy companies and technology providers are scaling up electrolyzer manufacturing capacity through advanced automated factories, with production capacities reaching multiple gigawatts annually.

- In September 2024, the Government of India announced the installation of 1.1 GW of electrolyzer manufacturing capacity, marking progress toward its annual target of 3 GW. The country aims to produce 5 million metric tonnes of green hydrogen annually by 2030, supported by 125 GW of renewable energy production capacity.

This shift enables economies of scale, reducing costs per unit and improving operational efficiency. Large-scale projects facilitate integration with renewable energy sources, stabilizing grids, and supporting industry decarbonization.

Download Free sample to learn more about this report.

IMPACT OF TARIFFS

Tariffs have a significant impact on the market, increasing production costs and disrupting supply chains, particularly for critical imported components such as electrolyzers and membranes. Trade tensions and retaliatory tariffs can hinder international collaboration and impede the adoption of new technologies. Higher tariffs lead to increased capital and operational expenses, potentially delaying project development or raising end-user prices, which affects market competitiveness and demand growth. While tariffs may protect local industries temporarily, they risk fragmenting the market and reducing efficiency gains from economies of scale.

SEGMENTATION ANALYSIS

By Technology

Alkaline Electrolyzers Dominated Market Due their Lower Costs

Based on technology, the market is segmented into PEM Electrolyzer, Alkaline Electrolyzer, and Others.

The alkaline electrolyzer segment is projected to dominate the market with a share of 46.64% in 2026, due to its cost-effectiveness, mature technology, and established manufacturing base. They are preferred for larger-scale, industrial hydrogen production, as they benefit from lower capital costs and widespread supplier availability.

- In September 2025, Accelera by Cummins supplied its largest electrolyzer system to date—a 35 MW proton exchange membrane (PEM) electrolyzer—at an industrial hydrogen facility in New York.

Meanwhile, PEM Electrolyzers are experiencing significant growth with a CAGR of 36.80%, driven by their rapid response to changing renewable energy inputs and ability to produce high-purity hydrogen.

By Power Source

Solar-Powered Electrolysis Segment Dominated Market Due Tto its Large-Scale Adoption

Based on power source, the market is segmented into Solar-Powered Electrolysis, Wind-Powered Electrolysis, Hydropower-Based Electrolysis, and Others.

The solar-powered electrolysis segment will account for 54.94% market share in 2026, due to the abundance of solar resources and declining photovoltaic costs. This renewable synergy allows efficient, low-carbon hydrogen production ideal for remote and off-grid applications.

- In April 2025, Cornell University researchers developed a solar-powered device producing low-cost, carbon-free green hydrogen directly from seawater, also generating potable water as a byproduct. Using a hybrid solar distillation-water electrolysis system, it efficiently utilizes sunlight, potentially reducing the cost of green hydrogen to USD 1/kg within 15 years, advancing clean energy and water sustainability.

Furthermore, wind-powered electrolysis demand in the market is growing due to falling wind energy costs and abundant resources. It allows cost-effective, carbon-free hydrogen production, supports grid stability, and integrates seamlessly with renewable systems, thus boosting global adoption.

By Application

Industrial Segment Led Market Due to Prominence of Decarbonization of Manufacturing Processes

Based on the application, the market is segmented into Transportation, Power Generation, Industrial, and Others.

The Industrial segment is anticipated to hold a dominant market share of 36.36% in 2026. Green hydrogen is increasingly in demand for industrial applications, such as steelmaking, refining, ammonia production, and chemical manufacturing. It plays a crucial role in decarbonizing core sectors, reducing emissions, and supporting sustainable industrial growth, driven by policies, technological innovations, and the quest for energy transition leadership.

Chemicals and petrochemicals represent a significant growth segment. Governments worldwide support hydrogen fuel cell vehicles (FCEVs) through subsidies and infrastructure development, thereby accelerating their adoption. Hydrogen’s high energy density and zero emissions make it a sustainable solution, particularly where battery electric vehicles face limitations.

To know how our report can help streamline your business, Speak to Analyst

GREEN HYDROGEN MARKET REGIONAL OUTLOOK

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Green Hydrogen Market Size, 2024 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific held 38.64% of the global market, reaching a valuation of USD 0.74 Billion, and is projected to grow to USD 1.0 Billion in 2026. Key drivers include aggressive decarbonization targets, significant investments in renewable energy, and increasing demand for industrial and transportation applications. China leads in production, boasting a large electrolyzer capacity and effective renewable energy integration, while countries such as Japan, South Korea, Australia, and India actively develop green hydrogen projects and policies. China is accelerating its green hydrogen industry with new policies that support low-carbon hydrogen production and its application in transportation, shipping, and aviation. The government’s national hydrogen pilot program aims to achieve commercial-scale readiness by 2028, providing subsidies to stimulate investment and technology development. The Japan market is projected to reach USD 0.11 billion by 2026, the China market is projected to reach USD 0.43 billion by 2026, and the India market is projected to reach USD 0.16 billion by 2026.

Europe

The Europe market was valued at USD 0.57 Billion in 2025, capturing 29.68% of global revenue, and is estimated to reach USD 0.74 Billion in 2026. Driven by stringent climate policies aiming for carbon neutrality by 2050, Europe is focusing on decarbonizing its heavy industries, transport, and energy sectors. Germany, France, the Netherlands, and Spain are leading the growth in electrolyzer capacity and renewable integration. The UK market is projected to reach USD 0.12 billion by 2026, and the Germany market is projected to reach USD 0.15 billion by 2026.

North America

North America accounted for USD 0.24 Billion in 2025, representing 12.58% of the global market share, and is projected to reach USD 0.32 Billion in 2026, led primarily by the U.S. It is rapidly expanding, driven by strong government incentives, such as the Inflation Reduction Act, and investments in renewable-powered electrolyzers and hydrogen hubs. Moreover, The U.S. green hydrogen market is experiencing rapid growth, driven by climate goals, government support (like the National Clean Hydrogen Strategy), and demand from sectors like chemicals and transportation (FCEVs). The U.S. market is projected to reach USD 0.24 billion by 2026.

Latin America

The Latin America region captured 7.02% of the global market in 2025, generating USD 0.13 Billion in revenue, and is projected to reach USD 0.17 Billion in 2026. The market for Biomass Power Generation in Latin America is driven by the region’s abundant renewable energy resources, particularly solar and wind, which enable cost-effective green hydrogen production. Leading countries include Chile, Brazil, Argentina, Colombia, and Mexico, with a focus on both domestic decarbonization and becoming major hydrogen exporters.

Middle East & Africa

Middle East & Africa contributed approximately USD 0.23 Billion to the global market in 2025, accounting for 12.07% share, and is expected to reach USD 0.3 Billion in 2026. The Middle East & Africa market is experiencing significant growth, with a CAGR of 25.03%, driven by abundant solar and wind resources, strategic geographic positioning, and large-scale projects such as Saudi Arabia’s NEOM and Namibia’s Hyphen.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Acquiring Large-Scale Production Projects to Increase Market Share

The competitive landscape is fragmented, with key players including Siemens Energy, Nel ASA, ITM Power, Ballard Power Systems, Air Liquide, and others. For instance, in November 2025, IFF launched the fragrance industry's first on-site green hydrogen facility at its Benicarló, Spain site, powered by renewable energy from Iberdrola. The facility produces 100 metric tons of green hydrogen annually, reducing 2,000 tons of CO2 emissions and supporting the sustainable production of fragrance ingredients. Green hydrogen market players focus on cost reduction (tech innovation, scale), vertical integration (renewables to end-use), strategic partnerships/M&A and more. Such developments are expected to foster market growth over the forecast period.

List of the Key Green Hydrogen Companies Profiled:

- Siemens Energy (Germany)

- Nel ASA (Norway)

- ITM Power (U.K.)

- Ballard Power Systems (Canada)

- Plug Power (U.S.)

- McPhy Energy (France)

- Hydrogenics Corporation (Canada)

- Air Products and Chemicals, Inc. (U.S.)

- Linde PLC (Germany)

- ENGIE (France)

- Mitsubishi Power (Japan)

- Enapter (Germany)

- Snam S.P.A. (Italy)

- Cummins Inc. (U.S.)

- Green Hydrogen Systems (Denmark)

KEY INDUSTRY DEVELOPMENTS:

- In November 2025, JSW Energy commissioned India’s largest green hydrogen plant in Karnataka, supplying 3,800 TPA of green hydrogen to JSW Steel under a seven-year agreement for steel production. The facility, under India’s National Green Hydrogen Mission, is expected to expand to 85,000–90,000 TPA by 2030.

- In November 2025, NEOM’s mega green hydrogen plant in Saudi Arabia is expected to begin commercial production in 2027, producing 600 tonnes daily from 4 GW of wind and solar power. The project aims to export green ammonia globally and cut 5 million tonnes of CO₂ annually.

- In August 2025, ACWA Power announced plans to develop a gigawatt-scale green hydrogen plant in Yanbu, targeting an annual output of 400,000 metric tons of green hydrogen and 2.8 million tons of green ammonia, with commercial operations expected to begin in 2030.

- In June 2025, Stargate Hydrogen signed an MoU with Saudi Arabia's RDI to launch its regional HQ in Riyadh, localize electrolyser technology, and foster innovation partnerships, supporting Saudi Vision 2030’s goal to be a global green hydrogen and deep-tech leader.

- In June 2025, the NEOM Green Hydrogen Project at Oxagon, Saudi Arabia, reached 80% construction completion across all sites by early 2025. The 4 GW wind and solar-powered facility aims to produce 600 tonnes of green hydrogen daily, which will be converted into green ammonia for global export, starting in 2027.

REPORT COVERAGE

The Global Green Hydrogen Market report delivers a detailed insight into the market. It focuses on key aspects, such as leading companies in the Market. Additionally, the report provides regional insights and global market trends, as well as pressure ranges, and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several other factors and challenges that contributed to the market's growth and decline in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 33.74% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Technology

By Power Source

By Application

By Region

|

Frequently Asked Questions

According to a Fortune Business Insights study, the market size was USD 1.92 billion in 2025.

The market is likely to grow at a CAGR of 33.74% over the forecast period (2026-2034).

The Industrial segment is expected to lead the market over the forecast period.

The market size of the Asia Pacific stood at USD 0.74 billion in 2025.

Decarbonization Mandates and Net-Zero Targets Drives the Market Growth

Some of the top players in the market are Siemens Energy, Nel ASA, ITM Power, Ballard Power Systems, and others.

The global market size is expected to reach USD 27.52 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us