Fuel Cell Vehicle Market Size, Share and Global Trend, By Vehicle Type (Passenger Cars, Commercial Vehicles, Buses & Coaches), By End-User (Private, Commercial), and Regional Forecast, 2026-2034

Fuel Cell Vehicle Market Size and Industry Overview

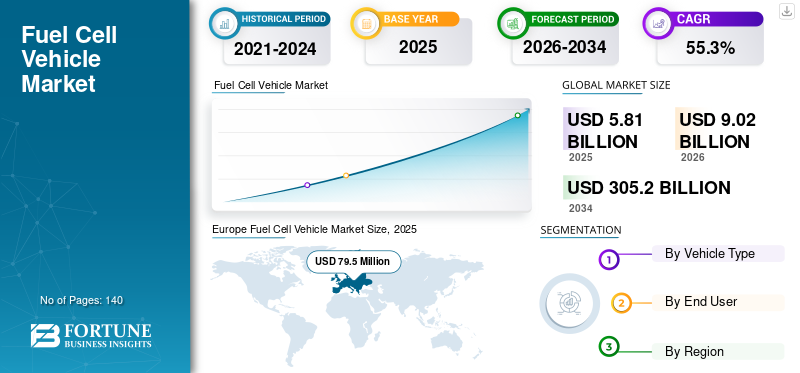

The global fuel cell vehicle market size was valued at USD 5.81 billion in 2025. The market is projected to grow from USD 9.02 billion in 2026 to USD 305.20 billion by 2034, exhibiting a CAGR of 55.30% during the forecast period. Europe dominated the fuel cell vehicle market with a market share of 17.79% in 2025

The global fuel cell vehicle market is shaped by decarbonization mandates, hydrogen infrastructure investment, and advances in fuel cell durability. Adoption remains concentrated in regions with supportive policy frameworks, notably East Asia, Europe, and selected North American corridors. Governments view fuel cell vehicles as complementary to battery electric models, particularly for heavy-duty transport where range, refueling speed, and payload efficiency matter.

Market growth is supported by sustained public funding, hydrogen corridor development, and automotive partnerships focused on cost reduction. Original equipment manufacturers are prioritizing scalable platforms that serve buses, trucks, and specialty fleets before broader passenger adoption. Improvements in stack longevity, power density, and cold-start performance are narrowing cost and performance gaps with internal combustion and battery alternatives.

Commercial fleet operators represent the strongest near-term demand segment. Logistics firms, transit agencies, and municipal fleets value predictable refueling times and centralized depot operations. These use cases improve the total cost of ownership economics when supported by regional hydrogen production and distribution. Passenger vehicle adoption remains constrained by infrastructure availability but shows progress in early-adopter markets.

The competitive landscape is shaped by collaboration between automakers, energy companies, and component suppliers. Partnerships increasingly focus on integrated hydrogen ecosystems rather than standalone vehicle sales. Technology differentiation centers on stack efficiency, balance-of-plant optimization, and fuel cell system durability under variable operating conditions.

The need to conserve natural resources and protect the environment is driving many vehicle manufacturers to take the lead in developing new, more efficient, and cleaner powertrains. Fuel cell vehicles are driven by the electricity generated onboard through a fuel cell stack by passing hydrogen gas. This fuel cell technology has the capacity to power passenger cars and commercial vehicles. Also, standards implemented by the U.S. Department of Energy for the usage of a hydrogen fuel cell in vehicles, owing to this, the automakers are making huge progress in the advancement of fuel cell vehicles.

Download Free sample to learn more about this report.

Fuel Cell Vehicle Market Key Takeaways

- 2025 Market Size: USD 5.81 billion

- 2026 Market Size: USD 9.02 billion

- 2034 Forecast Market Size: USD 305.20 billion

- CAGR: 55.30% from 2026–2034

- Europe dominated the fuel cell vehicle market with a 17.79% share in 2025.

- The passenger car segment is anticipated to dominate the market over the forecast period.

- The private end-user segment is expected to lead the market during the forecast period.

Asia Pacific

Asia Pacific is expected to dominate the global fuel cell vehicle market during the forecast period.

Europe

Europe is the second-largest regional market and is projected to witness significant growth.

North America

North America is expected to record steady growth driven by increasing hydrogen mobility initiatives.

U.S.

The market is projected to reach USD 331.3 million by 2026, supported by hydrogen infrastructure and fleet adoption.

Japan

Government subsidies and strong policy support continue to accelerate fuel cell vehicle adoption.

Read More

Key Market Dynamics

FUEL CELL VEHICLE MARKET TRENDS

Economic and Social Benefits of Hydrogen Fuel Cells have led to a significant Market Trend.

Hydrogen-based energy has many benefits, such as decarbonizing transportation, which helps to decarbonize building heating and power, distribute energy across regions and sectors, and also provide clean feedstock for industry. Hydrogen gas has been used successfully and safely in industrial procedures for generations. Since all these solutions support and complement each other, the hydrogen economy is experiencing exponential growth by attracting significant interest.

Increasing Use of Fuel Cell Vehicles by Government Bodies to Drive the Market

Increasing usage of fuel cell vehicles in government departments in some countries is expected to drive the fuel cell vehicle market trends. For example, in the U.K., in 2018, the metropolitan police added 21 Toyota Mirai fuel cell vehicles to their emergency response team, forming the world’s first hydrogen-powered fleet.

The fuel cell vehicle market is increasingly shaped by strategic partnerships between automakers, energy providers, and technology developers. Collaborative platforms are accelerating commercialization by sharing infrastructure costs and technical expertise. Fleet-focused deployments, particularly in logistics, transit, and municipal services, are emerging as early commercialization anchors.

Hydrogen ecosystem development is another defining trend. Governments and private stakeholders are aligning vehicle rollouts with hydrogen production, storage, and distribution investments. This integrated approach reduces operational risk and improves long-term viability. Concurrently, advancements in proton exchange membrane technology are enhancing efficiency, durability, and cold-start performance.

Digital integration is also influencing market evolution. Predictive maintenance, remote diagnostics, and energy management systems are being embedded into fuel cell platforms to optimize uptime and lifecycle performance. These capabilities support fleet operators seeking data-driven efficiency gains.

Regional specialization is becoming more pronounced, with Asia-Pacific focusing on large-scale deployment, Europe emphasizing regulatory alignment, and North America advancing pilot programs tied to clean energy corridors. Together, these trends signal a gradual but sustained transition toward commercial maturity.

MARKET DRIVERS

Stringent Government Emission Regulations to Drive the Growth of this Market

Vehicle emissions have led to an adverse impact on the environment and human life; therefore, several government bodies are implementing stringent emission standards for vehicles. As fuel cell vehicles are zero-emission vehicles are likely to have high demand in the market as they comply with government standards. The rising awareness among automakers about the effect of vehicle emissions on the environment by developing alternative powertrains is also expected to drive the growth of the market over the forecast period.

Rising Government Funding for Hydrogen Refueling Infrastructure to Drive the Market

Governmental funding for the development and installation of the hydrogen refueling stations is expected to boost the fuel cell vehicle market growth. The main objective of the governments of developed nations is to develop a strategic plan for the commercial rollout of fuel cell technology. This funding is expected to support the purchase of fuel cell vehicles. Many nations are aiming for full coverage of hydrogen refueling stations nationwide by 2030. The hydrogen fuel cell vehicles have the advantage of fast refueling. All these factors are likely to drive the growth of this market over the forecast period.

The global fuel cell vehicle market is primarily driven by tightening emission regulations and long-term decarbonization targets across major economies. Governments are increasingly promoting hydrogen-powered mobility to complement battery-electric solutions, particularly for heavy-duty and long-range applications. National hydrogen strategies in Asia-Pacific, Europe, and parts of North America are accelerating investments in refueling infrastructure, pilot corridors, and public–private demonstration projects.

Advancements in fuel cell stack efficiency, catalyst durability, and system integration have steadily improved vehicle performance while reducing the total cost of ownership. Automakers are leveraging modular fuel cell platforms that support multiple vehicle classes, from passenger cars to heavy commercial fleets. The ability to refuel quickly and maintain long driving ranges offers operational advantages for logistics operators, public transit agencies, and emergency fleets.

In parallel, declining costs of green hydrogen production through electrolysis are improving long-term economic viability. As renewable energy capacity expands, hydrogen produced from solar and wind sources strengthens the environmental case for fuel cell vehicles. These combined technical and policy drivers continue to reinforce market momentum across both developed and emerging economies.

MARKET RESTRAINT

The Initial Cost of Fuel Cell Vehicles to Restrain the Growth of the Market

Fuel cell vehicles are expensive, and the cost of hydrogen per kilo is high in some regions. These two factors are expected to restrain the fuel cell vehicle market demand over the forecast period. However, many automakers are working on the development of platinum-free metal components for fuel cells to combat the high pricing. This may lower the cost of vehicle production.

Despite progress, the fuel cell vehicle market faces structural and economic constraints that limit near-term adoption. High upfront vehicle costs remain a significant barrier, driven by expensive materials such as platinum catalysts and complex powertrain components. Although costs are gradually declining, price parity with internal combustion and battery-electric vehicles remains uneven across regions.

Limited hydrogen refueling infrastructure represents another major constraint. Sparse station networks restrict consumer confidence and complicate fleet deployment planning. Infrastructure buildout requires high capital investment, coordinated policy frameworks, and long payback periods, which can delay private sector participation.

Technical challenges also persist, including fuel cell durability under varying operating conditions and performance degradation over extended usage cycles. Cold-weather operation and hydrogen storage efficiency continue to require engineering optimization. Additionally, regulatory uncertainty around hydrogen standards, safety codes, and cross-border harmonization can slow large-scale deployment.

Market Opportunities

Significant growth opportunities exist across heavy-duty transportation segments where battery-electric solutions face operational limitations. Long-haul trucking, port logistics, and intercity buses represent high-potential use cases due to their predictable routes and centralized refueling needs. Expanding hydrogen corridor initiatives further enhances the feasibility for these applications.

Emerging markets offer additional opportunities as governments seek alternatives to fossil fuel dependence while modernizing transportation infrastructure. Public–private partnerships can accelerate deployment by reducing upfront capital barriers and sharing risk across stakeholders. As hydrogen production scales, localized supply chains can improve cost competitiveness and resilience.

Technological innovation also opens new avenues. Advances in catalyst efficiency, lightweight materials, and modular fuel cell stacks are enabling broader vehicle integration. Integration with renewable energy systems supports green hydrogen production, aligning fuel cell vehicles with broader decarbonization goals.

Policy incentives, including purchase subsidies, tax credits, and zero-emission mandates, continue to shape demand. As regulatory clarity improves and infrastructure expands, fuel cell vehicles are positioned to capture a growing share of the zero-emission mobility landscape, particularly in commercial and public transport segments.

FUEL CELL VEHICLE MARKET SEGMENTATION ANALYSIS

By Vehicle Type Analysis

To know how our report can help streamline your business, Speak to Analyst

Passenger Car Segment to Experience Significant Growth During the Forecast Period

Based on vehicle type, the market is segmented into passenger cars, commercial vehicles, and buses & coaches.

The passenger car segment is anticipated to dominate the market over the forecast period. Increasing sales of passenger cars in Japan and South Korea are likely to drive the growth of this segment in the market. Fuel cell passenger cars represent the most visible segment in terms of public awareness, although they account for a smaller share of total deployments compared to commercial fleets.

Adoption remains concentrated in regions with supportive hydrogen infrastructure and policy incentives. Automakers position fuel cell passenger vehicles as zero-emission alternatives offering extended driving range and rapid refueling compared to battery-electric options.

Consumer adoption remains sensitive to vehicle pricing, hydrogen availability, and resale confidence. While early adopters value environmental performance and driving range, mass-market penetration depends on infrastructure density and cost reductions across fuel cell stacks and hydrogen storage systems. In mature markets, passenger fuel cell vehicles increasingly serve as technology demonstrators that support broader ecosystem development.

The commercial vehicles represent the fastest-growing segment within the fuel cell vehicle market. Medium- and heavy-duty trucks benefit significantly from hydrogen fuel cells due to high payload capacity, predictable routes, and centralized refueling. Logistics operators increasingly favor fuel cell platforms for long-haul and regional transport, where battery-electric solutions face range and downtime constraints.

Fleet operators value the operational continuity offered by rapid refueling and extended range. Fuel cell trucks are also gaining traction in port operations, warehouse logistics, and intercity freight corridors. Government incentives and emissions regulations targeting freight decarbonization further strengthen adoption prospects within this segment.

The buses & coaches segment is projected to show significant growth in the market, owing to the rising government deployment of fuel cell buses in some countries. Public transportation agencies are increasingly deploying fuel cell buses as part of zero-emission transit strategies. These vehicles offer quiet operation, long range, and consistent performance across varying climates. Unlike battery-electric buses, fuel cell buses maintain operational efficiency in cold environments and during continuous daily operation.

Municipal procurement programs often support fuel cell buses through subsidies and long-term service contracts. As transit authorities seek to modernize fleets while meeting sustainability mandates, fuel cell buses are gaining traction, particularly in regions with established hydrogen supply chains.

By End-User Analysis

Private Segment to Show Exponential Growth in the Market over the Forecast Period

By end-user, the market segments include private and commercial.

The private end-user segment is expected to dominate the market over the forecast period. Government subsidies for the purchase of fuel cell vehicles for consumers are driving the growth of this segment in the market. Private enterprises constitute a growing share of fuel cell vehicle adoption, particularly in logistics, manufacturing, and energy sectors. Corporations with sustainability targets increasingly deploy fuel cell fleets to reduce emissions and meet environmental commitments. Warehousing, port operations, and industrial campuses benefit from predictable routes and centralized refueling, making hydrogen-powered vehicles operationally viable.

Private fleet operators also value fuel cell technology for its scalability and compatibility with existing fleet management systems. As hydrogen infrastructure expands, private sector adoption is expected to accelerate, particularly among organizations with long-term decarbonization strategies.

The commercial end-user segment is projected to show good growth in the market, owing to rising governmental funding for the usage of fuel cell vehicles, such as buses and light-heavy-duty vehicles, for public use. Government agencies remain central to early fuel cell adoption through pilot programs, public transport initiatives, and infrastructure funding. Municipal transit authorities, postal services, and utility fleets often serve as early adopters, leveraging public funding to offset initial costs.

Policy alignment plays a decisive role in this segment. Regions with hydrogen roadmaps, zero-emission mandates, and public procurement incentives demonstrate higher deployment rates. Government-backed demonstration projects also serve as validation platforms for broader commercial rollout.

Segment-Level Adoption Dynamics

Adoption patterns vary significantly by geography and use case. In the Asia-Pacific region, fuel cell buses and commercial trucks dominate due to coordinated government planning and industrial collaboration. Europe emphasizes hydrogen corridors and cross-border transport initiatives, while North America focuses on heavy-duty trucking and port logistics.

Cost trajectories, infrastructure availability, and regulatory clarity remain the key determinants of adoption speed. As hydrogen production scales and technology matures, cross-segment convergence is expected, with increasing overlap between public and private applications.

Competitive Implications Across Segments

Manufacturers increasingly tailor product portfolios to address specific segment requirements. Modular vehicle platforms allow OEMs to customize powertrains, storage capacities, and control systems for different use cases. This modular approach reduces development costs and accelerates time-to-market.

Partnerships between vehicle manufacturers, energy companies, and infrastructure providers are becoming central to market expansion. Integrated offerings that bundle vehicles, fueling access, and maintenance services are gaining traction, particularly among fleet operators seeking predictable operating costs.

FUEL CELL VEHICLE MARKET REGIONAL ANALYSIS

Europe Fuel Cell Vehicle Market Size, 2025

To get more information on the regional analysis of this market, Download Free sample

By region, the market has been segmented into Europe, North America, Asia-Pacific, and the Rest of the World.

Asia-Pacific Fuel Cell Vehicle Market Analysis

Asia-Pacific is expected to dominate the fuel cell vehicle market share over the forecast period. Japan and South Korea are key driver countries for the growth of this market in this region. Government initiatives in Japan for the usage of fuel cell vehicles and support to consumers through subsidies for the purchase of the vehicles are driving the growth of the market in this region.

Asia-Pacific remains a key growth engine for fuel cell vehicles, driven by coordinated national roadmaps and large-scale manufacturing capacity. Governments prioritize hydrogen as part of broader energy transition goals. Strong investment in infrastructure and supply chains supports expanding adoption across multiple countries.

Japan Fuel Cell Vehicle Market

Japan sustains a leadership position in fuel cell vehicle deployment through long-standing hydrogen strategies and consistent policy backing. Automotive manufacturers continue expanding fuel cell offerings, supported by a well-established refueling network and public acceptance of hydrogen mobility.

China Fuel Cell Vehicle Market

China’s fuel cell vehicle sector is advancing through regional demonstration programs and industrial cluster development. Government incentives focus on commercial fleets, logistics vehicles, and heavy-duty transport. Expanding domestic manufacturing capabilities supports scalable deployment across key provinces.

North America Fuel Cell Vehicle Market Analysis

North America represents a technologically advanced fuel cell vehicle market, supported by federal decarbonization initiatives and sustained infrastructure investment. The United States leads regional deployment through pilot corridors, public–private partnerships, and early commercial adoption. Strong policy alignment and ongoing research programs continue to accelerate market development across freight and transit segments.

North America is expected to show steady growth in the fuel cell vehicle market over the forecast period, owing to the lower number of fuel cell vehicles. The Fuel Cell Vehicle Market in the U.S. is projected to grow significantly, reaching an estimated value of USD 331.3 million by 2026

United States Fuel Cell Vehicle Market

The United States remains a key hub for fuel cell vehicle innovation, particularly in heavy-duty transport and fleet operations. Federal incentives, state-level zero-emission mandates, and hydrogen hub funding support deployment at scale. California remains central, while expanding interest from logistics operators drives broader geographic adoption.

Europe Fuel Cell Vehicle Market Analysis

Download Free sample to learn more about this report.

Europe maintains steady progress in fuel cell vehicle adoption, supported by coordinated hydrogen strategies and cross-border infrastructure planning. The region prioritizes decarbonizing freight corridors and public transit fleets. Consistent policy frameworks and funding mechanisms encourage long-term investment across member states.

Europe is the second-largest region in the market and is estimated to show significant growth in the market over the forecast period. France is a leader in this region owing to a massive deployment of commercial vehicles in the country for public and government usage.

Germany Fuel Cell Vehicle Market

Germany plays a leading role in Europe’s hydrogen mobility landscape, supported by industrial policy and strong manufacturing capabilities. National hydrogen strategies encourage fuel cell deployment across logistics, public transport, and municipal fleets. Collaborative programs between industry and government accelerate commercialization pathways.

United Kingdom Fuel Cell Vehicle Market

The United Kingdom continues to advance fuel cell mobility through targeted pilot programs and regulatory incentives. Public transit electrification and hydrogen bus deployments support early adoption. Strategic partnerships between government agencies and technology providers reinforce long-term market momentum.

Latin America Fuel Cell Vehicle Market Analysis

Latin America shows early-stage adoption of fuel cell mobility, driven by clean energy strategies and pilot initiatives. Countries such as Chile and Brazil explore hydrogen-powered transport within broader decarbonization agendas. Infrastructure limitations remain a constraint, though policy momentum is building.

Middle East & Africa Fuel Cell Vehicle Market Analysis

The Middle East and Africa region is in the early phase of fuel cell vehicle adoption, supported by national hydrogen strategies and sustainability initiatives. Gulf nations prioritize hydrogen development, while selected African markets explore pilot projects aligned with long-term energy diversification goals.

Competitive Landscape

Toyota Motor Corporation has Developed Fuel Cell Technology for Maritime Applications.

The competitive landscape depicts that the fuel cell market is dominated by the Toyota Motor Corporation. Toyota’s fuel cell technology demonstrates the adaptability to a variety of maritime applications.

Toyota is also developing technologies for a hydrogen-based society, as stated in its Environmental Challenge 2050. This project is also supporting the vision and aim of a hydrogen-based society.

The fuel cell vehicle market features a concentrated group of global automotive manufacturers, energy companies, and specialized technology providers shaping commercial deployment and innovation pathways. Market leadership is influenced by vertical integration capabilities, hydrogen supply chain access, and long-term policy alignment.

Major automotive OEMs maintain strong positions through in-house fuel cell development, system integration expertise, and large-scale pilot deployments. These companies focus on improving power density, extending vehicle range, and reducing total system costs to accelerate commercialization across passenger and commercial segments. Strategic partnerships with hydrogen infrastructure providers remain central to market expansion.

Specialized fuel cell technology firms contribute advanced stack designs, membrane electrode assemblies, and power control systems. Their role is critical in improving efficiency, durability, and thermal performance. Many collaborate with automotive OEMs through joint development agreements or licensing models.

Energy companies and industrial gas suppliers increasingly shape the competitive landscape by investing in hydrogen production, storage, and distribution networks. Their involvement reduces infrastructure bottlenecks and supports long-term ecosystem stability.

Technology collaborations, government-backed demonstration programs, and cross-sector alliances define current competitive dynamics. Market participants prioritize scalability, regulatory alignment, and cost optimization to secure long-term positioning in a rapidly evolving hydrogen economy.

LIST OF KEY COMPANIES PROFILED IN THE REPORT:

- Toyota Motor Corporation (Toyota, Aichi, Japan)

- Hyundai Motor Company (Seoul, South Korea)

- Nissan Motor Corporation (Yokohama, Kanagawa, Japan)

- Daimler AG (Stuttgart, Baden-Württemberg)

- AUDI AG (Zwickau, Germany)

- BMW AG (Munich, Germany)

KEY INDUSTRY DEVELOPMENTS:

- March 2024 – Toyota Motor Corporation: Toyota expanded its hydrogen fuel cell production capacity to support next-generation commercial vehicles. The initiative focuses on improving stack efficiency, durability, and cost competitiveness for heavy-duty transport applications.

- June 2024 – Hyundai Motor Group: Hyundai launched an upgraded fuel cell system platform designed for long-haul trucks and buses. The system enhances power density and thermal efficiency, supporting broader commercial fleet deployment.

- September 2024 – Bosch and Cellcentric Partnership: Bosch and Cellcentric advanced joint development of scalable fuel cell modules for commercial vehicles. The collaboration emphasizes standardized components to accelerate industrial manufacturing and reduce system costs.

- February 2025 – Toyota and Isuzu Collaboration: Toyota and Isuzu expanded their fuel cell truck development program, targeting zero-emission logistics operations. The partnership focuses on optimizing vehicle range, refueling efficiency, and fleet integration.

- April 2025 – Hyundai Hydrogen Mobility Expansion: Hyundai announced the expansion of its hydrogen mobility ecosystem across selected international markets. The initiative includes integrated vehicle deployment, fueling infrastructure, and digital fleet management platforms to support commercial adoption.

REPORT COVERAGE

The fuel cell vehicle market report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading applications of the product. Besides this, the report offers insights into the market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD million) |

|

Segmentation |

By Vehicle Type

|

|

By End User

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 5.81 billion in 2025 and is projected to reach USD 305.2 billion in 2034.

In 2025, the market value stood at USD 5.81 billion.

Growing at a CAGR of 55.3%, the market will exhibit exponential growth in the forecast period (2026-2034).

The passenger car segment is expected to be the leading segment in this market during the forecast period.

Stringent government emission regulations is the key factor driving the fuel cell vehicle market.

Toyota Motor Corporation is the leading player in the global market.

Asia Pacific dominated the market share in 2025.

The rising Government funding for the hydrogen refueling stations along with stringent government regulations are likely to open new market spaces for the fuel cell vehicle.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us