Fuel Cell Market Size, Share & Industry Analysis, By Type (Proton Exchange Membrane Fuel Cell, Solid Oxide Fuel Cell, Phosphoric Acid Fuel Cell and Others), By Application (Transport, Stationary and Portable), and Regional Forecast, 2026-2034

Fuel Cell Market Insights

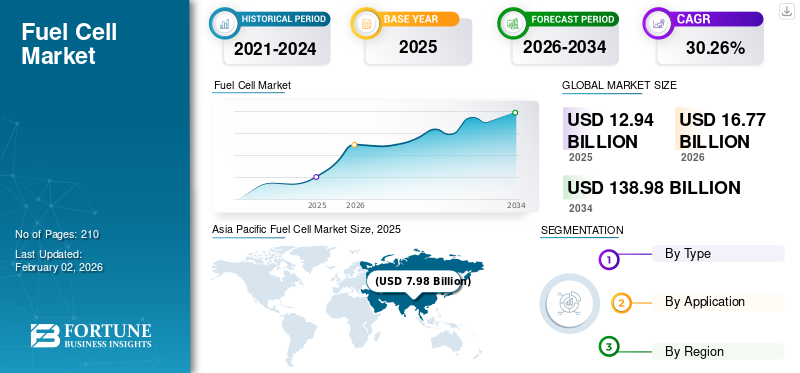

The Global Fuel Cell Market size was valued at USD 12.94 billion in 2025 and is expected to reach USD 16.77 billion in 2026. Furthermore, the market is projected to reach USD 138.98 billion by 2034 exhibiting a CAGR of 30.26% during the forecast period of 2026-2034. Moreover, the Asia Pacific region accounts for the largest market share of 61.62% in 2025. Countries are prioritizing Fuel cells to reduce carbon emissions and enhance energy independence.

A Fuel Cell (FC) can be defined as a device comprising a cathode and an anode immersed in electrolyte medium, which conducts and produces electricity efficiently. These units also operates as a battery, providing essential power to the system. However, it uses hydrogen-based fuel instead of charging for several periods. These systems operate on an elementary electrochemical mechanism that converts chemical energy into electrical energy. Supporting regulatory policies and increase in demand for green energy sources promotes the market expansion.

In March 2025, the Government of India approved five pilot projects to deploy 37 hydrogen-based vehicles (15 fuel cell and 22 internal combustion engine) with 9 refueling stations across 10 routes, supporting the National Green Hydrogen Mission for scaling up clean transportation within 18-24 months.

Bloom Energy is the leader in the market, holding a significant global share. At the same time, Plug Power is a another prominent player in the market, particularly for commercial mobility and stationary applications. Other key leaders include Ballard Power Systems, Doosan Fuel Cell, FuelCell Energy, and Ceres Power.

Download Free sample to learn more about this report.

Fuel Cell MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 12.94 Billion

- 2026 Market Size: USD 16.77 Billion

- 2034 Forecast Market Size: USD 138.98 Billion

- CAGR: 30.26% from 2026–2034

- Asia Pacific dominated the fuel cell market with a 61.62% share in 2025.

- The Proton Exchange Membrane Fuel Cell (PEMFC) segment is projected to account for 67.35% of the market in 2026.

- The transport segment is expected to hold a 63.52% market share in 2026.

North American

North America is witnessing rising fuel cell adoption across transportation and stationary power applications.

Europe

Europe is expanding its fuel cell market through clean energy initiatives and decarbonization efforts.

Asia Pacific

Asia Pacific led the global market with a 61.62% share in 2025.

U.S.

Growing investments in hydrogen infrastructure and fuel cell technologies are supporting market growth.

Japan

Strong government support and hydrogen economy initiatives continue to drive fuel cell adoption.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Favorable Regulatory Policies to Support Product Deployment to Drive Market Growth

Fuel cell systems are increasingly installed to produce Combined Heat & Power (CHP) for powering and heating small households and commercial spaces such as hotels, hospitals, educational centers, public buildings and others. Consequently, various state and federal authorities have introduced favorable legislative frameworks and subsidy schemes to propel the integration of devices in different applications. For instance, the government of the state of New Jersey has updated its financial benefits for FC CHP installations on or after October 1st, 2020. Its CHP-FC Program structure is designed to propel manufacturers with a monetary aid of up to USD 3 million per project for the producers.

In April 2025, the Chinese Ministry of Finance announced that China had allocated USD 321 million in 2025 to boost regional hydrogen fuel cell vehicle deployment. This funding supports the expansion of hydrogen infrastructure, vehicle adoption, and technology development across key cities and provinces as part of China’s strategy for growing its hydrogen economy.

Additionally, several governments globally, are offering tax breaks and grants to promote the adoption of fuel cell technology. These supportive initiatives are expected to reduce financial barriers for enterprises that deploy fuel cells, thereby aiding in boosting overall market growth.

Growing Need for Clean Energy Sources to Boost Market Proliferation

Carbon emissions contribute to climate change, which reflects serious consequences for humans and environment. Solid Oxide Fuel Cell (SOFC) are used in mobile and stationary applications. This strengthens and diversifies energy infrastructure, providing a reliable, clean, and advanced energy-efficient solution to meet surging power demand. Thus, better fuel efficiency and rising adoption of zero-emission equipment will surge the demand for fuel cells in CHP application during the forecast period.

Rising concerns about climate change and energy security are driving increased interest in renewable energy, boosting the businesses significantly. This change is being supported by rising government and industry investment in green technology, particularly hydrogen as a clean energy carrier.

MARKET RESTRAINTS

Increasing Demand for Electric Vehicles and Difficulty in Managing Bulk Hydrogen Stations to Hinder Market Growth

The demand for electric vehicles, which includes battery electric vehicles and plug-in hybrid electric vehicles, is increasing significantly due to various advantages, such as higher efficiency, no polluting byproducts, cost efficiency, and energy security, which may hinder market expansion.

Furthermore, the lack of standardized infrastructure for hydrogen filling stations, combined with the high costs of establishing and maintaining them, remains a significant barrier to the widespread use of hydrogen fuel cells. To overcome these issues, public and private players must work closely and build clear, consistent regulatory frameworks.

The high cost associated with producing and delivering hydrogen fuel to service stations, along with the complex management of bulk fueling stations, might obstruct market expansion. Additionally, the planning and construction of new stations require huge investments that are dependent on multiple factors affecting market dynamics.

MARKET OPPORTUNITIES

Zero-Emission Mandates Pushing Fleet Operators toward Hydrogen Trucks Creates Lucrative Opportunities

Zero-emission mandates are accelerating the adoption of hydrogen fuel cell trucks as fleet operators strive to comply with increasingly stringent climate regulations. Governments worldwide are phasing out diesel vehicles and incentivizing clean mobility through subsidies, tax credits, and the establishment of low-emission zones.

Hydrogen trucks, offering long range, fast refueling, and high payload capacity, are becoming a practical solution for decarbonizing heavy-duty transport. This shift is creating strong market opportunities especially for fuel cell manufacturers, hydrogen refueling infrastructure developers, and logistics companies transitioning to sustainable operations, positioning hydrogen as a key enabler of zero-emission freight mobility in regions emphasizing net-zero targets.

MARKET CHALLENGES

The High Capital Cost of Fuel Cell Systems Creates Challenges for Market Growth

The high capital cost of fuel cell systems remains a major challenge that restrains the fuel cell market growth. Expensive components, such as proton exchange membranes, catalysts, and hydrogen storage tanks, significantly increase system prices compared to diesel or battery-electric alternatives. Limited economies of scale and complex manufacturing processes further increase costs, making large-scale deployment less feasible for fleet operators.

Additionally, the lack of widespread refueling infrastructure adds to the total investment costs. Addressing these cost barriers through technological innovation, supply chain expansion, and government support is crucial for enabling mass adoption of fuel cell mobility solutions.

FUEL CELL MARKET TRENDS

Accelerated Deployment of Stationary Mw-Scale Fuel Cells is Emerging as a Key Trend

The growing need for clean, reliable power in industrial, commercial, and utility applications drives the accelerated deployment of stationary MW-scale fuel cells. These fuel cells provide stable, efficient energy with low emissions, enabling organizations to meet their sustainability and decarbonization targets.

In November 2024, Bloom Energy announced the world’s largest single-site solid oxide fuel cell (SOFC) installation: an 80 MW project in North Chungcheong Province, South Korea. Developed in collaboration with SK Eternix and financed by the Korea Development Bank, it powers two ecoparks. It marks a milestone in scalable, reliable clean energy, with commercial operations set to commence in 2025.

Increasing grid instability and the demand for uninterrupted power supply in critical infrastructure, such as data centers and hospitals, are driving adoption. Technological improvements, supportive policies, and integration with renewable energy sources further enhance their appeal. As companies prioritize energy resilience and environmental responsibility, stationary fuel cells are becoming a practical and scalable solution for on-site power generation.

Download Free sample to learn more about this report.

IMPACT OF TARIFFS

Tariffs negatively impact the global market by increasing production costs and consumer prices for vehicles and components, which slows market adoption and reduces profitability for manufacturers. Tariffs also cause supply chain disruptions and can deter foreign investment, forcing companies to shift production and diversify suppliers to mitigate risks strategically. While domestic manufacturers may initially gain a temporary advantage, the overall impact of trade barriers leads to a rise in cost of achieving clean energy goals.

SEGMENTATION ANALYSIS

By Type

PEMFCs Segment to Lead Backed by Low Cost and Flexibility in Input Fuel

By type, the market is segmented into proton exchange membrane fuel cells, solid oxide fuel cells, phosphoric acid fuel cells, and others.

The Proton Exchange Membrane Fuel Cell (PEMFC) segment is anticipated to hold a dominant market share of 67.35% in 2026. The demand for PEMFCs is higher due to their various benefits over other types. Benefits, such as flexibility in input fuel, compact design, lightweight construction, low cost, and solidity of electrolyte, will aid segment growth.

In April 2025, HORIBA launched the C05-LT, an entry-level 100W PEM benchtop fuel cell test station designed for single-cell testing. It delivers precise temperature, pressure, and flow control with plug-and-play software, supporting accelerated research in fuel cell performance, durability, and component development.

The Solid Oxide Fuel Cell (SOFC) segment is estimated to grow significantly with a CAGR of 32.44% during the forecast period. SOFC has been gaining significant share in the Ene-Farm program due to fuel cell stack's higher efficiency and higher-grade heat. The net increase in SOFC shipment capacity is associated with an increase in bloom units for prime power shipments in the U.S. and Korea. Other suppliers, such as Ceres/Bosch, contribute to the segment growth.

By Application

Transport Segment to Grow at the Highest CAGR Due to Rising Demand for DMFCs & PEMFCs in the Automotive Sector

By application, the market has been segmented into transport, stationary, and portable.

The transport segment is anticipated to hold a dominant market share of 63.52% in 2026. The segment is expected to register rapid growth during the forecast period. The inclination toward clean transportation is increasing worldwide. Various countries are investing in an emission-free environment, which is further boosting the transport sector.

The portable segment is also expected to experience strong growth, driven by increasing demand for fuel cell–powered backup systems and portable energy storage solutions. As these fuel cells become smaller and more affordable, their applications in consumer electronics, military gear, and emergency power systems are likely to increase.

To know how our report can help streamline your business, Speak to Analyst

FUEL CELL MARKET REGIONAL OUTLOOK

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Fuel Cell Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market accounted for USD 7.98 billion in 2025, representing 61.62% of the global industry, and is expected to reach USD 10.55 billion in 2026. The Asia Pacific The region is striving to become a global leader in hydrogen infrastructure, supported by major companies such as Toyota and Honda, which are investing heavily in hydrogen-powered vehicles and fuel cell innovations in Japan and South Korea. Japan’s focus on utilizing fuel cells across both residential and commercial sectors is expected to accelerate market growth further. For instance, in September 2025, Toyota announced its third-generation fuel cell system (3rd Gen FC System), designed with durability comparable to diesel engines and improved fuel efficiency. It targets commercial vehicles and heavy-duty applications, with plans to enter markets in Japan, Europe, North America, and China starting after 2026. The Japan market is projected to reach USD 12.16 billion by 2026, and the China market is projected to reach USD 3.55 billion by 2026.

North America

The region is increasing its investment in fuel cell installations due to the enhanced capacity for FC installations in the transport segment. The installation of portable applications is also increasing across the region. Moreover, the U.S. Market was valued at USD 2.57 billion in 2025 driven by federal clean energy policies (like the Infrastructure Law and incentives) and a push for decarbonization. The U.S. market is projected to reach USD 4.57 billion by 2026. North America maintained a strong presence in the global market, reaching USD 3.78 billion in 2025, accounting for 29.24% share, and is expected to reach USD 4.81 billion in 2026.

Europe

In 2025, Europe generated USD 1.14 billion, contributing 8.80% to global market revenue, and is projected to grow to USD 1.36 billion in 2026. The installation of FCs in Europe has increased significantly. The region is investing substantial amounts of money in achieving zero-emission targets and expanding its hydrogen infrastructure. The adoption of energy-efficient solutions is also increasing rapidly across the region. Berlin Airport in Germany has installed one of the first combined heat and power CHP to run entirely on hydrogen. The UK market is projected to reach USD 0.33 billion by 2026, and the Germany market is projected to reach USD 0.44 billion by 2026.

Rest of the World

Rest of the World accounted for USD 44.24 billion in 2025, representing 0.34% of the global market share, and is projected to reach USD 51 billion in 2026. The demand and installation of fuel cells are rapidly increasing worldwide. Key investment hubs in the regions such as Middle East are increasingly focusing on integrating hydrogen into their energy portfolios, particularly as part of their Vision 2030 goals. Countries such as Saudi Arabia and the UAE are planning large-scale hydrogen production facilities and fuel cell projects to leverage the region’s vast renewable energy resources, which could significantly boost demand for fuel cell technologies in the area.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Focus on New Product Launches to Increase Market Share

The competitive landscape is fragmented, with key players including Ballard Power Systems, Bosch, Horizon Fuel Cell Technologies, ElringKlinger, Hydrogenics, and others. In September 2025, Ballard Power Systems launched its new FCmove-SC fuel cell module at Busworld 2025, specifically designed for city transit buses. It offers 30% more power, 25% higher volumetric power density, simplified integration, improved thermal management, lower lifecycle cost, and supports predictive maintenance to approach diesel parity in total cost of ownership. Fuel cell market players are adopting strategies focused on cost reduction through R&D and manufacturing efficiency, forming strategic partnerships & M&As, expanding into transport (buses, trucks, FCVs) & critical backup power. Such developments are expected to foster market growth over the forecast period.

List of the Key Fuel Cell Market Companies Profiled:

- Ballard Power Systems (Canada)

- Bosch (Germany)

- Horizon Fuel Cell Technologies (Singapore)

- ElringKlinger (Germany)

- Hydrogenics (Canada)

- Ceres Power (U.K.)

- AVL (Austria)

- Pragma Industries (France)

- Mitsubishi Hitachi Power Systems (Japan)

- W.L. Gore & Associates (U.S.)

- Nedstack Fuel Cell Technology (Netherlands)

- Proton Motor Fuel Cell GmbH (Germany)

- Bloom Energy (U.S.)

- AISIN (Japan)

- Convion (Finland)

- ITM Power (U.K.)

- Plug Power (U.S.)

- Nuvera Fuel Cells, LLC (U.S.)

- FuelCell Energy (U.S.)

- Elcogen (Estonia)

- Nexceris LLC (U.S.)

- SFS Energy AG (Germany)

- Blue World Technologies (Denmark)

- Roland Gumpert (Germany)

KEY INDUSTRY DEVELOPMENTS:

- In November 2025, Doosan Fuel Cell signed a USD 96.4 billion deal with KEPCO to supply hydrogen power over a 20-year period. This long-term agreement supports South Korea’s expansion of its hydrogen economy, with Doosan delivering and maintaining hydrogen fuel cell power systems, thereby reinforcing stable revenue and sustainable energy growth.

- In November 2025, S-Fuelcell launched the GFOS platform, a modular fuel cell system designed for AI data centers. It operates initially on natural gas but is hydrogen-ready for future transitions, addressing grid capacity limits and ensuring reliable, scalable power.

- In August 2025, Honda began production of its 2025 CR-V e:FCEV, the first plug-in hydrogen fuel cell electric vehicle made in the U.S., featuring a next-generation fuel cell system developed in collaboration with GM. It offers a 270-mile range, plus an additional 29 miles from a 17kWh battery, and a hydrogen tank capacity of 4.3kg at 10,000 PSI.

- In August 2025, Honda, Tokuyama, and Mitsubishi Corporation initiated a joint demonstration in Yamaguchi, Japan, utilizing by-product hydrogen and repurposed stationary power fuel cells from advanced fuel cell electric vehicles to power a data center. The project aims to optimize backup power sources, including off-grid solutions, peak shaving, and grid balancing, thereby advancing the green transformation of data centers and supporting digital transformation for local businesses.

- In June 2025, Airbus and MTU Aero Engines signed a Memorandum of Understanding at the 2025 Paris Airshow to jointly develop hydrogen fuel cell propulsion for commercial aviation. Their three-step roadmap includes maturing key technologies via joint research, aligning R&T roadmaps, and potentially developing a full-scale fuel cell engine.

REPORT COVERAGE

The Fuel Cell Market report delivers a detailed insight into the market. It focuses on key aspects, such as leading companies in the Market. Additionally, the report provides regional insights and global market trends, as well as pressure ranges, and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several other factors and challenges that contributed to the market's growth and decline in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Global Fuel Cell Market Scope | |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 30.26% from 2026 to 2034 |

| Unit | Volume (MW) & Value (USD Billion) |

| Segmentation |

By Type

|

|

By Application

|

|

|

By Region

|

|

Frequently Asked Questions

According to a Fortune Business Insights study, the market size was USD 12.94 billion in 2025.

The market is likely to grow at a CAGR of 30.26% over the forecast period (2026-2034).

The Transport segment is expected to lead the market over the forecast period.

The market size of the Asia Pacific stood at USD 7.98 billion in 2025.

Decarbonization Mandates and Net-Zero Targets Drive the Market Growth

Some of the top players in the market are Siemens Energy, Nel ASA, ITM Power, Ballard Power Systems, and others.

The global market size is expected to reach USD 138.98 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us