Combined Heat and Power (CHP) Market Size, Share & Industry Analysis, By Fuel Type (Natural Gas, Coal, Biomass, and Others), By Technology (Combined Cycle, Steam Turbine, Gas Turbine, Reciprocating Engine, and Others), By Capacity (Up to 10 MW, 10-150 MW, 151-300 MW, and Above 300 MW), By Application (Utilities, Residential, and Commercial & Industrial), and Regional Forecast, 2026-2034

Combined Heat and Power (CHP) Market Size

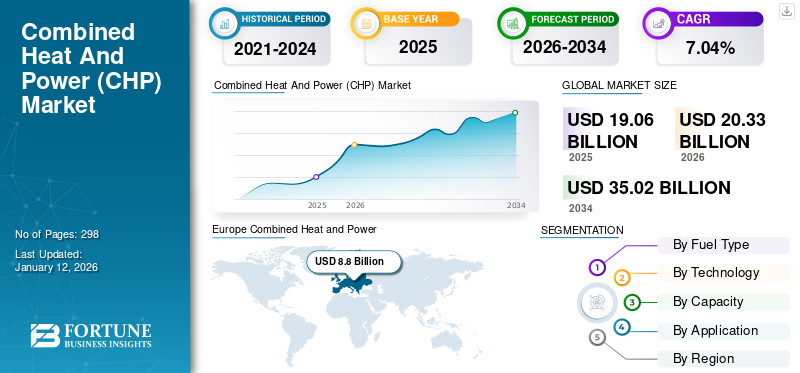

The global combined heat and power (CHP) market size was valued at USD 19.06 billion in 2025 and is expected to grow from USD 20.33 billion in 2026 to USD 35.02 billion by 2034, exhibiting a CAGR of 7.04% during the forecast period. Europe dominated the global market with a share of 46.18% in 2025. Industry growth is driven by decentralized energy systems, industrial efficiency demand, carbon reduction mandates, natural gas transition, distributed generation expansion, and grid resilience investments.

Combined heat and power (CHP) offers a productive and clean way to generate electric power and thermal power from a single fuel source. CHP power plants are often close to the end user's site so that the heat released from power generation can be utilized to meet the user's heat necessities while the power produced meets all or a part of the site's energy needs. Applications with consistent electricity and thermal energy demand are great monetary focuses for CHP deployment.

Industrial applications, especially in businesses with consistent handling and high steam requirements, are exceptionally profitable and address a huge portion of existing CHP capacity today. Moreover, hospitals, nursing homes, laundries, and lodgings with large hot water requirements are well-suited for the commercial applications of combined heat and power systems. Institutional applications such as universities and schools, prisons, and private and sporting offices have incredible possibilities for CHP deployment.

The global combined heat and power (CHP) market is positioned as a critical component of distributed energy systems, driven by the need for energy efficiency, emissions reduction, and grid resilience. CHP systems, also referred to as cogeneration, simultaneously generate electricity and useful thermal energy from a single fuel source, improving overall energy utilization efficiency compared to conventional generation methods.

The combined heat and power market size continues to expand across industrial, commercial, and utility applications, supported by rising energy costs and tightening environmental regulations. Industrial users, particularly in energy-intensive sectors such as chemicals, refining, and manufacturing, represent a dominant share of CHP deployment due to their continuous thermal and power requirements.

Natural gas-based CHP systems currently dominate the market due to favorable economics, lower emissions compared to coal, and established infrastructure. However, biomass and renewable-integrated CHP systems are gaining traction in regions prioritizing carbon neutrality. From an institutional perspective, CHP investments are evaluated based on payback period, fuel availability, regulatory incentives, and operational efficiency gains. Industrial operators prioritize systems that reduce energy costs while ensuring supply reliability.

Regional dynamics vary significantly. Europe demonstrates mature CHP deployment supported by district heating infrastructure, while Asia-Pacific exhibits strong growth driven by industrial expansion and urbanization. North America remains stable, with increasing focus on modernization and efficiency upgrades.

The outbreak of COVID-19 and the lockdowns negatively impacted the global combined heat and power (CHP) market. Many CHP stakeholders reported that several critical CHP projects were behind schedule due to disruptions caused by the COVID-19 crisis. For instance, in November 2020, Virt Energy GmbH, the Germany-based franchisor of Virt biogas systems, announced the commissioning of the Virt Mobile biogas demonstration plant in Sri City, Andhra Pradesh, India. Due to pandemic-related lockdowns, the company reported delays of about six months, as about 80% of the work was completed before the pandemic.

Download Free sample to learn more about this report.

COMBINED HEAT AND POWER (CHP) MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 12.84 Billion

- 2026 Market Size: USD 14.99 Billion

- 2034 Forecast Market Size: USD 51.68 Billion

- CAGR: 16.7% from 2026–2034

- Asia Pacific dominated the automotive AI market with a 56.7% share in 2025.

- The commercial vehicles segment is projected to grow at a CAGR of 17.6%.

- The autonomous driving systems segment is projected to grow at a CAGR of 19.4%.

North America

North America ranked third, driven by autonomous vehicle testing and AI innovation.

Europe

Europe held the second-largest market share and is projected to grow at a CAGR of 14.9%.

Asia Pacific

Asia Pacific led the market, supported by EV production and connected vehicle adoption.

U.S.

The market is estimated at USD 1.86 billion in 2026, accounting for 12.4% of global revenue.

Japan

The market is estimated at USD 1.26 billion in 2026, accounting for 8.4% of global revenue.

Read More

Combined Heat and Power (CHP) Market Trends

Growing Inclination Toward Smart Heating Systems is the Latest Trend

Increasing inclination toward smart heating systems and the rising investments in research and development of technology programs are considered to be the latest trends in this industry. The industry is witnessing increased adoption of gas-powered systems derived from low-fossil fuel by-products, combined with evolving customer inclination toward cleanliness, in countries around the world. Substituting conventional energy-producing systems with highly efficient cogeneration plants is expected to help business development across countries.

The combined heat and power market is undergoing a structural shift toward decentralized and efficiency-driven energy systems. CHP is increasingly positioned as a bridging technology between conventional thermal generation and low-carbon distributed energy models. Adoption trends reflect a gradual transition from centralized power generation toward localized energy solutions, particularly in industrial and urban infrastructure settings. Natural gas-based CHP systems continue to dominate installations, supported by relatively lower emissions and established fuel supply networks. However, there is a noticeable shift toward integrating renewable energy sources such as biomass and biogas into CHP systems. This transition aligns with broader decarbonization objectives across developed markets.

Urban energy systems are also evolving, with CHP playing a central role in district heating networks. European markets, in particular, demonstrate strong integration of CHP with municipal energy infrastructure. These systems enhance overall energy efficiency while reducing transmission losses. Another notable trend involves digital optimization. Advanced control systems and predictive analytics are being integrated into CHP operations, improving system efficiency and maintenance planning. Industrial operators increasingly prioritize these capabilities to enhance operational reliability.

Moreover, the government in the U.S. is substantially investing in research and development for various prime mover technologies to run the combined heat and power (CHP) units economically. The U.S. national administration has introduced several economic benefits to customers to sustain the installation. For instance, the U.S. Internal Revenue Code (IRC) Section 48 provides an investment tax credit (ITC) for certain energy-related investments. The government aims to support sustainable energy development programs by offering subsidies and tax credits to investors and citizens to adopt efficient and clean energy sources. Under the ITC program, there is a 30% permanent credit rate for solar, while combined heat & power accounts for a 10% credit rate till 2022.

In October 2020, the U.K. Administration announced the introduction of a new biomass strategy for the year 2022 to progress bioenergy usage to support renewable revolutions. The new publication was drafted by the Department of Business, Energy and Industrial Strategy (BEIS) of the U.K., as per the findings of the Committee on Climate Change’s (CCC) progress report. In its 2018 publication, CCC directed the potential for the usage of biomass, wood, and waste by 2050. In addition, the National Renewable Energy Association (REA) projected that bioenergy sources are capable of meeting up to 16% of the total primary energy generation by 2032.

Download Free sample to learn more about this report.

Key Market Dynamics

Combined Heat and Power Market Growth Factors

Prodigious Demand for Heat and Power to Boost Combined Heat And Power (CHP) Market Growth

Energy is essential for paving the way for nurturing economies. It not only ensures continuous investment, innovation, and expansion of industries but also generates employment, inclusive growth, and shared prosperity for entire economies. So, there is a massive requisition for heat and power to meet the economic targets. Combined heat and power (CHP) units are deployed in several IT parks, hospitals, schools, universities, airports, malls, and commercial spaces, among others, to generate heat and power economically in order to generate independent energy producers.

The growing commercial sectors, owing to the inflation of economies, may increase the demand for heat and power, which is set to accelerate the demand for CHP. As per the International Energy Agency, the global sales of heat pumps grew by around 11% in 2022 across the world, owing to the rising requirements of heating and cooling. European countries, the U.S., and China have been the major market leaders in the world for selling heat pumps.

Drift Toward Sustainable Energy Development to Mitigate Increasing GHG Emissions to Spur the Market Growth

The requirement for power and electricity is continuously growing across the globe due to the surging population and expansion of residential, commercial, and industrial sectors. According to the International Energy Agency (IEA), the total energy consumption across the globe increased by about 2% in 2023 and is expected to rise further to around 3.3% in 2024. To curb this growing power demand, governments of various countries, such as India, Saudi Arabia, China, Brazil, and others, are taking various initiatives and making investments to expand their power generation capacities. For the expansion of the power generation capacities, the governments of the countries are primarily focused on renewable energy sources to achieve net-zero carbon emissions by 2050, as discussed in the Paris Agreement.

According to the International Renewable Energy Agency, the total installed renewable capacity at the end of 2022 was around 3,372GW, which has grown by around 295GW from the previous year, thus representing a growth of approximately 9.6%. In addition, the CHP or cogeneration power-producing facilities also serve as a medium for reducing carbon emissions to a much greater extent than thermal power generation and traditional heat-producing technologies.

The combined heat and power market growth is driven by a combination of economic, regulatory, and operational factors. Energy efficiency remains the primary driver, as CHP systems can achieve significantly higher overall efficiency compared to conventional power generation. This efficiency translates directly into cost savings for industrial and commercial users.

Rising energy costs further strengthen the business case for CHP adoption. Industrial operators seek to reduce dependence on grid electricity and improve energy cost predictability. CHP systems provide a reliable solution by generating both power and thermal energy onsite.

Restraining Factors

Constrained Application and High Initial Investment May Hamper the Market Growth

The combined heat and power (CHP) system implementation requires a huge capital investment, which becomes non-feasible without any government funds or financial assistance that may hinder the combined heat and power (CHP) market growth. In addition, varying prices between the different prime technologies create a reluctance among customers to shift their choices from existing alternatives. CHP is mainly adopted in densely populated areas to integrate the systems on a large scale to manage overall installation costs. However, the low-populated residents are hesitant to incorporate advanced combined heat and power (CHP) units due to the high initial costs of installation.

Despite favorable growth drivers, the combined heat and power market faces several structural constraints that affect adoption. High initial capital investment remains one of the most significant barriers. CHP systems require substantial upfront expenditure, including equipment, installation, and integration with existing energy infrastructure. This capital intensity can deter small and medium enterprises, particularly in markets with limited access to financing. Even for large industrial users, investment decisions are often influenced by payback periods and internal rate of return thresholds.

Fuel dependency represents another critical constraint. Natural gas remains the dominant fuel for CHP systems, exposing operators to price volatility and supply disruptions. In regions with limited natural gas infrastructure, CHP deployment becomes less economically viable. Regulatory variability also impacts market development. Inconsistent policy frameworks, changing incentive structures, and permitting complexities can delay project implementation and reduce investor confidence.

Operational complexity further influences adoption. CHP systems require technical expertise for installation, operation, and maintenance. Industrial operators must ensure adequate technical capabilities to manage system performance effectively.

In addition, a lack of awareness, along with deficient technical knowledge regarding the benefits of CHP, may limit the market growth. For example, as per the U.S. Environmental Protection Agency (EPA), the installation costs for various prime movers fueled by biomass range from USD 350 per kW to USD 10,000 per kW. The prices are highly dependent on the demonstration, introduction, and commercialization statuses and available models across the market. Furthermore, the availability of prime mover technologies operating on other fuels such as natural gas, oil, diesel, and hydrogen may also act as a restraining factor to the market growth.

Market Opportunities

The combined heat and power market presents several strategic opportunities driven by evolving energy systems and decarbonization priorities. One of the most significant opportunities lies in the integration of CHP with renewable energy sources. Hybrid systems combining CHP with solar, wind, or biomass can enhance overall system efficiency while reducing carbon emissions.

District energy systems represent another key opportunity. Urbanization and population growth increase demand for efficient heating and cooling solutions. CHP systems integrated into district heating networks can deliver centralized thermal energy with improved efficiency and reduced environmental impact.

Emerging markets offer considerable growth potential. Industrialization and infrastructure development in Asia-Pacific, Latin America, and parts of Africa create demand for reliable and efficient energy solutions. CHP systems can address these needs while supporting economic development. Technological innovation also presents opportunities. Advances in microturbines, fuel cells, and digital control systems improve CHP efficiency and operational flexibility. These technologies enable deployment across a wider range of applications, including smaller-scale installations.

Combined Heat and Power (CHP) Market Segmentation Analysis

By Fuel Type Analysis

Natural Gas-Based CHP Units Dominate the Market Owing To Rising Adoption of Clean Fuel

Based on fuel type, the market is segmented into natural gas, coal, biomass, and others.

Natural Gas

Natural gas dominates the market due to its high efficiency and low cost compared to other fuel types. Moreover, an increase in funding and assistance from government and private players for the development of highly efficient natural gas power plant projects is likely to boost realistic gas-based CHP deployment. The Natural Gas segment is expected to account for 67.29% of the market in 2026.

Natural gas remains the dominant fuel within the combined heat and power market, accounting for a substantial share of global installations. Its widespread availability, relatively lower carbon emissions compared to coal, and compatibility with existing infrastructure make it the preferred fuel for CHP systems across industrial and commercial applications.

Industrial facilities with continuous energy demand often favor natural gas CHP due to its predictable performance and cost structure. Additionally, regulatory frameworks in many regions support natural gas as a transitional fuel within broader decarbonization strategies.

Coal

The continuous adoption of clean fuel, with concern over rising carbon emissions from burning coal to produce steam, has led to a decline in the utilization of coal-based CHPs. A significant proportion of coal-fired combined heat and power (CHP) plants have been fitted with low-NOX burners to minimize NOX emissions, and some units have been equipped with flue gas desulphurization equipment.

Coal-based CHP systems have historically played a significant role in regions with abundant coal resources, particularly in parts of Asia. These systems are often deployed in large industrial complexes where coal remains a primary energy source. However, environmental concerns and regulatory pressure are reducing the attractiveness of coal-based CHP systems. Stringent emission standards and carbon reduction targets are accelerating the shift toward cleaner alternatives.

Biomass

The biomass combined heat and power (CHP) demand is expected to grow at a significant rate over the forecast period. The setup of new projects with wooden and agricultural fuel, high calorific value, established acceptability, efficient operations, and substantial energy production are some of the key features favoring the segment's growth.

Biomass-based CHP systems are gaining traction as a renewable alternative within the combined heat and power industry. These systems utilize organic materials such as agricultural residues, wood waste, and industrial by-products to generate energy. Biomass CHP is particularly relevant in regions with strong agricultural or forestry sectors. These systems support circular economy models by converting waste materials into usable energy.

The coal-fired power generation sector has also progressively closed down its older power stations as more efficient plants have come on-stream.

To know how our report can help streamline your business, Speak to Analyst

By Technology Analysis

Combined Cycle Segment to Dominate Owing to Higher Electrical Efficiency

Based on technology, the combined heat and power (CHP) market is categorized into combined cycle, steam turbine, gas turbine, reciprocating engine, and others.

Combined Cycle

The combined cycle segment is expected to lead the global CHP market, accounting for 51.50% market share in 2026. These systems typically use a gas turbine to drive an electrical generator and recover waste heat from the turbine's exhaust to produce steam. Steam from the waste heat is passed through a steam turbine to provide additional power. The overall electrical efficiency of a combined cogeneration system is typically in the 50-60% range, which is a significant improvement over the approximately 33% efficiency of a simple open-cycle cogeneration application.

Combined cycle CHP systems represent one of the most efficient technologies within the combined heat and power market. These systems utilize both gas and steam turbines to maximize energy extraction from fuel inputs. Combined cycle systems are typically deployed in high-capacity installations where efficiency gains justify higher capital investment.

Steam Turbine

The steam turbine segment also holds a substantial portion of the market share after the combined cycle. However, the major hindrance to the segment growth is that steam cogeneration is a high-temperature HVAC that requires high usage and demand in order to be practical. Steam turbine CHP systems are widely used in industrial applications, particularly where steam is already required for production processes. These systems are compatible with multiple fuel types, including coal, biomass, and natural gas. Steam turbines remain a reliable choice for large industrial facilities with continuous thermal demand.

Gas Turbine

Gas turbine CHP systems are commonly used in medium to large-scale applications. These systems provide a balance between efficiency and operational flexibility, making them suitable for industrial and commercial users. Gas turbines are particularly relevant in regions with strong natural gas infrastructure.

Reciprocating Engine

Reciprocating engine CHP systems are widely used in small to medium-scale applications. These systems are suitable for distributed generation and decentralized energy solutions. Reciprocating engines play a critical role in expanding CHP adoption beyond large industrial facilities.

By Capacity Analysis

151-300 MW Segment Dominates Owing to the Huge Preference for Industrial Applications

Based on capacity, the combined heat and power (CHP) market is segmented into up to 10 MW, 10-150 MW, 151-300 MW, and above 300 MW.

Up to 10 MW

The up to 10 MW segment is anticipated to be the fastest-growing segment during the forecast period. The capacity mainly plays specific roles in the application segment. CHP technologies can help manufacturing facilities, federal and other government facilities, commercial buildings, institutional facilities, and communities reduce energy costs and emissions and provide more resilient and reliable electric power and thermal energy.

Small-scale CHP systems are typically deployed in commercial buildings, hospitals, and small industrial facilities. These systems support localized energy generation and improve efficiency in distributed settings.

10–150 MW

Medium-scale CHP systems represent a significant portion of installations, particularly in industrial and district energy applications. These systems balance capacity and efficiency, making them suitable for diverse use cases.

151–300 MW

The 151-300 MW segment is anticipated to hold a dominant market share of 37.92% in 2026. The 151-300 MW is the dominating segment among other capacity types, as 151-300 MW is majorly preferred for commercial, industrial, and utility applications. This capacity range offers significant scale efficiencies while still being manageable in terms of installation and operation compared to larger systems. Industries and district heating applications often require CHP systems in this capacity range to meet their combined electricity and heat demands efficiently. Large-scale CHP systems are primarily used in heavy industrial applications and utility-supported projects. These systems require substantial capital investment but offer significant efficiency gains.

Above 300 MW

Very large CHP systems are typically associated with major industrial complexes or integrated energy facilities. These installations are less common but play a critical role in energy-intensive sectors.

By Application Analysis

Expanding Commercial Sector to Augment the Commercial & Industrial Segment Growth

Based on application, the market is segmented into utilities, residential, and commercial & industrial.

Utilities

Utility-based CHP systems are often integrated into district heating and cooling networks. These systems support centralized thermal energy distribution while improving overall system efficiency. The utility segment also grabbed a notable share in the market in 2023 due to the fact that utilities are particularly well-suited to help CHP deployment rise because they are uniquely capable of making and encouraging long-term, cost-effective investments for the greater efficiency of the grid.

Residential

The residential segment is also witnessing a steady expansion owing to the increase in the adoption of CHP systems for emergency power backup units in the residential sector. A similar trend is foreseen in Europe as several nations are embracing clean and energy-efficient technology to heat and power their residential buildings. Residential CHP adoption remains limited but is gradually expanding in regions with strong policy support. Micro-CHP systems are used to provide localized heating and electricity for households.

Commercial & Industrial

The commercial and industrial segment dominates the combined heat and power market share. Industrial facilities benefit from continuous energy demand, making CHP systems economically viable. This segment will continue to drive combined heat and power market growth due to its strong economic fundamentals and operational alignment.

In 2026, the commercial & industrial segment is projected to lead the market with a 76.93% share. The commercial & industrial segment holds the dominant share in the market due to the expansion of the commercial sector, underpinned by industrialization, for generating high GDP in countries across the globe. The governments of several countries worldwide have been focusing on the expansion of these sectors by making huge investments and framing initiatives to attract high FDI.

REGIONAL INSIGHTS

Based on region, the market is divided into North America, the Asia Pacific, Europe, the Middle East & Africa, and Latin America.

Europe Combined Heat and Power (CHP) Market Size, 2025

To get more information on the regional analysis of this market, Download Free sample

North America Combined Heat and Power Market Analysis

North America demonstrates mature combined heat and power market adoption, driven by industrial efficiency requirements and regulatory incentives. The region benefits from established natural gas infrastructure and supportive policy frameworks promoting energy efficiency. CHP deployment remains concentrated in industrial and institutional facilities, including healthcare and universities. Grid resilience concerns and rising energy costs further support distributed generation investments across the United States and Canada, sustaining long-term market stability. In 2025, the North America market stood at USD 5.63 billion, representing 29.53% of global demand, and is projected to grow to USD 6.04 billion in 2026.

The installations of CHPs have further been magnified due to the expansion of commercial, residential, and industrial sectors in these regions. In North America, the U.S. is the leading country in the CHP market due to the increasing investments in developing large-scale projects, establishing a robust policy framework, and the availability of colossal infrastructure, among other factors. The U.S. market is projected to reach USD 4.61 billion by 2026. Moreover, in 2023, the Canadian government awarded a USD 35 million contract to develop a 6.5 MW CHP plant and connect it to a local diesel microgrid.

United States Combined Heat and Power Market

The United States leads regional deployment, supported by strong industrial demand and federal efficiency initiatives. CHP systems are widely implemented across manufacturing, chemicals, and district energy systems. Policy incentives and state-level programs continue to encourage adoption. Natural gas availability strengthens economic feasibility. However, regulatory fragmentation and permitting complexity influence project timelines, requiring careful evaluation by investors and developers assessing long-term deployment strategies.

Europe Combined Heat and Power Market Analysis

Europe represents a highly developed combined heat and power market, supported by stringent emission regulations and advanced district heating networks. CHP systems are deeply integrated into urban energy infrastructure. Policy alignment with decarbonization goals drives adoption, particularly in Northern and Western Europe. The region emphasizes renewable-integrated CHP systems, including biomass and waste-to-energy solutions, reinforcing its leadership in sustainable energy deployment.

The Europe region captured 46.18% of the global market in 2025, generating USD 8.8 billion in revenue, and is projected to reach USD 9.32 billion in 2026. It is expected to continue to dominate during the forecasted years as well, owing to the strict rules and regulations in this region regarding carbon emissions & sustainability. Europe’s directives on energy efficiency & renewable energy promotion, along with feed-in tariffs and carbon pricing mechanisms, significantly influence CHP deployment. For instance, the U.K. reduced its VAT from 20% to 5% on domestic CHP installation, while Germany provides the KWKG allowance to promote cogeneration.

Germany Combined Heat and Power Market

Germany maintains a strong position within the combined heat and power market, supported by its energy transition strategy and district heating infrastructure. CHP systems play a central role in balancing renewable energy integration. Industrial users and municipal utilities continue to invest in efficient cogeneration systems. Policy incentives and carbon reduction targets reinforce deployment, although rising fuel costs and regulatory adjustments influence investment decisions. The German market is projected to reach USD 2.62 billion by 2026.

United Kingdom Combined Heat and Power Market

The UK market is projected to reach USD 0.98 billion by 2026. The United Kingdom's combined heat and power market reflects moderate but stable adoption, particularly in industrial and commercial sectors. CHP systems are used to enhance energy efficiency and reduce operational costs. Government initiatives supporting low-carbon technologies encourage deployment. However, evolving energy policies and uncertainty around long-term incentives create variability in investment decisions, requiring careful project evaluation by stakeholders.

Asia-Pacific Combined Heat and Power Market Analysis

Asia Pacific maintained a strong presence in the global market, reaching USD 3.4 billion in 2025, accounting for 17.82% share, and is expected to reach USD 3.69 billion in 2026. In addition, the Asia Pacific prioritized control of carbon emissions and has implemented various initiatives to control them.

Asia-Pacific represents the fastest-evolving combined heat and power market, driven by industrial expansion and rising energy demand. Countries such as China, Japan, and South Korea lead adoption. CHP systems support industrial efficiency and urban energy infrastructure. Government policies promoting energy security and emission reduction accelerate deployment. Rapid urbanization further strengthens demand for district energy solutions across major metropolitan regions. The Indian market is projected to reach USD 0.39 billion by 2026.

Japan Combined Heat and Power Market

The Japanese market is projected to reach USD 0.65 billion by 2026. Japan demonstrates advanced CHP adoption, particularly in industrial and commercial sectors. Energy security concerns and limited domestic energy resources support distributed generation strategies. CHP systems are integrated into industrial facilities and urban infrastructure. Technological innovation, including fuel cells and micro-CHP systems, enhances efficiency. Government support for energy resilience and decarbonization continues to drive steady market expansion.

China Combined Heat and Power Market

The Chinese market is projected to reach USD 1.39 billion by 2026, and the Middle East & Africa. China dominates the regional combined heat and power market in terms of scale, driven by industrial demand and urban heating requirements. CHP systems are widely deployed in district heating networks and industrial complexes. Government policies emphasizing energy efficiency and emission reduction support continued growth. Transition toward cleaner fuels, including natural gas and biomass, is gradually reshaping the market landscape.

Latin America Combined Heat and Power Market Analysis

In 2025, Latin America represented USD 0.79 billion, accounting for 4.15% of the worldwide market, and is projected to grow to USD 0.83 billion in 2026. Latin America presents emerging opportunities within the combined heat and power market, supported by industrial growth and energy diversification efforts. Adoption remains limited but is increasing in sectors such as food processing and manufacturing. Natural gas availability influences deployment potential. Economic constraints and infrastructure limitations pose challenges, although gradual policy development is expected to improve long-term market prospects.

Middle East & Africa Combined Heat and Power Market Analysis

The Middle East and Africa combined heat and power market remains nascent but shows potential in industrial and energy-intensive sectors. Abundant fuel resources support CHP feasibility. Adoption is driven by efficiency improvement and energy cost optimization. However, limited regulatory support and infrastructure constraints slow widespread deployment, requiring strategic investments and policy alignment.

The Middle East & Africa market accounted for USD 0.44 billion in 2025, representing 2.32% of the global industry, and is expected to reach USD 0.46 billion in 2026. The Middle East & Africa region is also gaining gradual traction toward the deployment of combined heat and power in sectors such as oil refineries, petrochemicals, and district cooling systems. Government policies aiming at energy diversification, renewable energy targets, and enhancing energy efficiency drive the adoption of CHP in select industries.

KEY INDUSTRY PLAYERS

Companies Focus on Catering to Specific Demands of the End-use Industry to Strengthen Their Position

The global CHP market is significantly fragmented into numerous players offering varied products and services across the global value chain. Numerous companies are actively operating in the region to meet the specific demands of the end-use industry, mostly in power generation.

Siemens AG and General Electric are expected to have a significant market share because they have been active in the industry for a long time, and the operational potential of the portfolio has been improved. In addition, the company operates hundreds of cogeneration plants globally, offering the advantages of both heavy-duty gas turbines and gas engines. Other major participants also include Kawasaki Heavy Industries, Mitsubishi Power, Wärtsilä, and Cummins, among many others, which are present with various technologies across the industry to stay connected with the top-performing players.

List of Top Combined Heat and Power (CHP) Companies:

- MAN Diesel & Turbo (Germany)

- Wärtsilä (France)

- General Electric (U.S.)

- Kawasaki Heavy Industries, Ltd. (Japan)

- Mitsubishi Heavy Industries, Ltd. (Japan)

- Bosch Thermotechnology (Germany)

- Viessmann Werke (Germany)

- FuelCell Energy (U.S.)

- Cummins (U.S.)

- Veolia (France)

- BDR Thermia (Netherlands)

- CENTRAX Gas Turbines (U.K.)

- 2G Energy Services (Germany)

- ABB (Switzerland)

- Siemens (Germany)

KEY INDUSTRY DEVELOPMENTS:

- October 2023- Malarenergi partnered with ABB to upgrade its switchgear, along with retrofit solutions, at its cogeneration plant located in Vasteras. Malarenergi’s CHP plant has 98% of all local properties connected to the district heating system. The retrofit process was carried out in three different stages with customized solutions for each of CHP's switchgear cabinets. By modernizing its switchgear, Malarenergi aims to maintain predictable delivery to its customers and increase safety for both personnel and equipment.

- July 2023- Mitsubishi Power received an order for two gas turbines for a 1,600MW Class GTCC Power Plant in Uzbekistan. Mitsubishi Power supplied a range of equipment, including a series of orders for the H-25 series of small and medium-sized gas turbines for an urban distributed natural gas-fired cogeneration (CHP) facility being developed in Tashkent.

- May 2022- Wärtsilä collaborated with Capwatt on a green hydrogen blending project in Portugal, which started in the first quarter of 2023 and aims to test mixtures with up to 10% green hydrogen by volume. The CHP plant, which supplies energy to the Sonae Campus and the national grid, is currently powered by a natural gas-powered Wärtsilä 34SG engine.

- January 2022- Veolia signed a new 15-year contract with Total Fitness to reduce energy consumption and carbon emissions at 17 different health and fitness centers in the North of England and Wales. Under the agreement, Veolia will help Total Fitness reduce its gas consumption by 32% using CHP. The latest technology installed increases electrical efficiency by 22% compared to existing cogeneration equipment, lowers energy costs, and further reduces CO2 emissions in the 134,000 m2 building area.

- June 2019- BDR Thermea Group declared to launch the first-ever hydrogen-powered domestic boiler across the globe. The breakthrough is to be deployed in a pilot project in Rozenburg, Netherlands, and is set to use hydrogen fuel derived from solar and wind energy to curb any release of harmful CO2.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product/service types, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Growth Rate |

CAGR of 7.04% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Fuel Type

|

|

By Technology

|

|

|

By Capacity

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights study shows that the global market was USD 20.33 billion in 2026.

The global market is projected to grow at a CAGR of 7.04% during the forecast period.

The market size of Europe stood at USD 9.32 billion in 2026.

By fuel type, the natural gas segment accounts for a leading proportion of the market.

The global market size is expected to reach USD 35.02 billion by 2034.

The key market drivers are the increasing demand for heat and power and the drift toward sustainable energy development.

The top players in the market are Siemens AG and General Electric, among others.

- 2021-2034

- 2025

- 2021-2024

- 298

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us