District Heating Market Size, Share & Industry Analysis, By Heat Source (Coal, Natural Gas, Renewables, Oil & Petroleum Products, and Others), By Plant Type (Boiler, CHP, and Others), By Application (Residential, Commercial, and Industrial), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

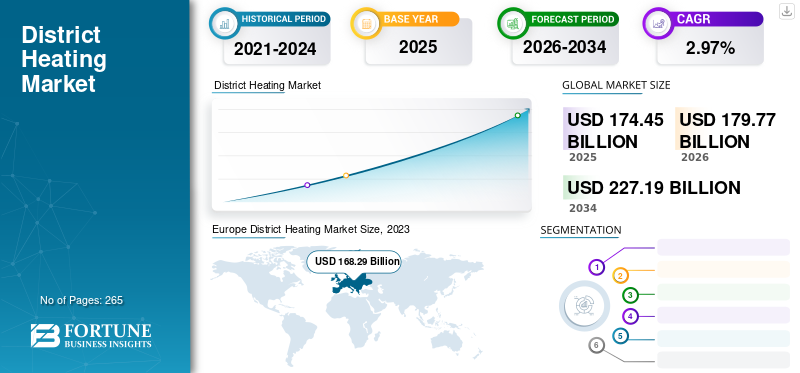

The global district heating market size was valued at USD 174.45 billion in 2025 and is projected to grow from USD 179.77 billion in 2026 to USD 227.19 billion by 2034, exhibiting a CAGR of 2.97% during the forecast period. Europe dominated the district heating industry with a market share of 17.51% in 2025. The district heating market in the U.S. is projected to grow significantly, reaching an estimated value of USD 7.24 billion by 2032, driven by the rising demand for space heating applications coupled with renewable energy policies and incentives. By application, the residential segment has contributed 59.39% market share in 2023.

A district energy system is used to provide heat for monitoring temperature in industrial, residential, and business areas. The heat energy is produced at a central heat plant and then distributed through well-established district heat networks of insulated pipes. The heat generation is controlled via combined heat and power systems, boilers, or heat pumps. These systems facilitate scaling back the greenhouse emissions as the heat is generated at the central plant, which can meet the growing demand for heat for a massive variety of consumers.

On the bright side, renewable energy sources have gained the upper hand in energy production during the lockdown period. As per the study conducted by the International Renewable Energy Agency (IRENA) on the impact of COVID-19 on the renewable energy sector, the existing renewable energy projects in operation have witnessed higher utilization rates than ever before. In Europe, during the first quarter of 2020, renewables accounted for 41% of total energy production, which indicates an increase of 16% compared to the first quarter of previous years.

The COVID-19 crisis considerably affected the entire power sector across the globe. Throughout the COVID-19 pandemic, several countries imposed nationwide lockdowns to prevent the spread of the deadly virus, which has interrupted many activities, including construction, new infrastructure development, installation of turbines, and others.

Download Free sample to learn more about this report.

District Heating Market Trends

Focus on Decreasing Greenhouse Gas Emissions Will Grow the Market in Forecast Years

The increasing focus on greenhouse gas emissions and meeting climate change goals will drive the market in the coming years. The International Energy Agency’s District Heating and Cooling, including Combined Heat and Power (DHC TCP), conducts policy analysis, research & development, and international collaboration to enhance the market penetration of district cooling and heating systems with minimal environmental effect. For instance, in 2021, as per the Natural Resources Canada’s- CanmetENERGY project on Large-scale Thermal Storage for District Heating and Cooling, modern district cooling and heating systems are a significant technology for the energy transition toward a green economy.

Industrial sectors and projects are the focused areas where greenhouse gas emissions can be controlled. District heating is one of the essential equipment for several heating applications. Such rising emphasis on climate change integrated with the new technology in the marketplace will boost the district heating market.

Download Free sample to learn more about this report.

District Heating Market Growth Factors

Rising Need to Diminish the Carbon Emission will Augment Growth in the Market

Population across the globe has risen at an exponential rate in recent years, which led to increased urbanization being witnessed across different regions. This has directly increased the demand for energy from various end-use sectors. District heating is capable of producing a large amount of energy at a central plant, and further transmitting it to different end-use industries acts as an effective solution for sufficing the heat demand.

The world is struggling with threats due to unprecedented carbon emissions and global warming, resulting in an increased inclination toward renewable energy resources. The U.K. has proclaimed an incentive package of USD 2 billion investment for the heating sector from 2015-to 2025. Germany has announced an investment of around 1 billion by 2030. Similar packages are expected in Denmark, Netherlands, and China in the coming years. Poland has broadcasted an investment of USD 5 billion from 2018 to 2028 in the heating sector

Flexibility in the Source of Heat Generation and Cost-effectiveness to Propel Growth

District heating provides the choice of heat generation using numerous sources such as coal, renewables, gas, oil & crude product, and alternative accessible sources. Recent trends witnessed renewables and gas to be progressively employed in district heating systems as these resources directly facilitate reducing gas emissions and serve in achieving energy targets. These operational advantages will drive the district heating market growth in the coming years.

RESTRAINING FACTORS

High Initial Capital Investment for Infrastructure May Restrict Market Growth

The setting up of a district heating capacity requires an initial hefty capital investment as installing a safe transmission and distribution lines network is very costly. The insulated pipes and their underground laying require a considerable investment, which is a major obstacle for investors. Also, lack of required infrastructure and availability of other economical options for space heating and water heating may hamper the growth of the market in the coming years.

District Heating Market Segmentation Analysis

By Heat Source Analysis

Renewable Segment Dominated Global Market in 2023 Due to High Installation Globally

Based on heat source, the market is segmented into coal, natural gas, renewables, oil & petroleum products, and others. The renewables segment is projected to dominate the market in the coming years. Power utilities are upgrading to clean energy from fossil fuel to increase power generation capacity as the awareness concerning environmental safety is increasing among folks, and thus the government is imposing strict regulations for emissions and pollution. This will increase the installation of renewable sources for heat generation around the world. The benefits of the conception, such as higher potency and negligible carbon emissions, have driven the expansion of this section.

The gas section is likely to expand considerably throughout the forecast period. Exploration activities are rising around the world, and gas plants are significantly efficient and have less harmful effects on the surroundings in contrast to fossil fuels. Gas is extravagantly accessible, and the installation of such plants is increasing globally.

By Plant Type Analysis

CHP Segment to Expand at a Highest Rate Owing to High Efficiency than Others

Based on plant type, the market is segmented into boilers, Combined Heat and Power Plants (CHP), and others. CHP systems modify electricity generation alongside heat being created for the heating systems. This can be the most important considering the expansion of the CHP segment’s market share in recent years. The other factor contributing to the growth of this segment is the increasing electricity demand across the world. Further, CHP systems have higher efficiency as compared to normal boilers and diminish the prices as they avoid distribution and transmission losses. Also, support from governments in promoting the use of the CHP systems has power-assisted the expansion of the market.

The boiler section is projected to witness growth throughout the forecast period as a result of increasing demand for electricity around the world. The installation of various energy plants is additionally increasing around the world.

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Residential Segment to Dominate Global Market Due to High Demand for Warmer Spaces

In terms of application, the market is segmented into residential, commercial, and industrial. The residential segment holds the largest market share, owing to the increased requirement for heating networks at residential locations for various uses such as space heating and water heating. Also, there has been a rise in the number of construction projects in the residential sector, owing to increasing urbanization, which has been the catalyst for the segment growth.

Industrialization is widely increasing around the world. Infrastructure development is also increasing in the industrial sector with the ongoing revolution. This increases the implementation of heating spaces in the industrial sector. This drives the market growth in this segment.

The residential segment holds the largest market share, owing to the rising demand for heating networks in residential areas for numerous uses such as house heating and water heating. Also, there has been an increase in the range of construction within the residential sector due to increasing urbanization, which has been the catalyst for this segment’s growth.

The industrial segment is estimated to grow rapidly in the forecast period, owing to rapid industrialization around the world. Infrastructure development is additionally increasing within the industrial sector with the continuing revolution. This will increase the implementation of heating areas within the industrial sector. This drives the market growth in this segment during the forecast period.

REGIONAL INSIGHTS

Geographically, the global district heating market has been analyzed across four key regions, including North America, Europe, Asia Pacific, and the rest of the world.

Europe

Europe District Heating Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Europe market was valued at USD 136.86 billion in 2025, capturing 17.51% of global revenue, and is estimated to reach USD 140.87 billion in 2026. Europe has dominated the market as the region has low-temperature conditions for most of the year. Europe consists of large industries and power plants from which heat is generated that goes to waste. Such heat is utilized to meet all heating demands within the region. The installation of renewable sources of energy is also increasing, and the waste heat from such plants is widely used for heating purpose only due to extreme weather conditions. This drives the market growth in Europe during the forecast period.

North America

North America accounted for USD 6.82 billion in 2025, representing 3.91% of the global market share, and is projected to reach USD 7.07 billion in 2026. North America is projected to grow significantly during the forecast period. The demand for heating and electricity is increasing widely in the region. The region even faces low temperatures for a long time in a year, which increases the demand for heating water in residential, commercial, and industrial spaces. The U.S. holds a dominant district heating market share in this region.

Asia Pacific

In 2025, Asia Pacific held 78.45% of the global market, reaching a valuation of USD 30.54 billion, and is projected to grow to USD 31.59 billion in 2026. Asia Pacific positions as the most lucrative market for district heating. China is increasing investments in heating networks. China, which experiences low temperatures, has witnessed maximum deployment of heating plants. The installation of renewable heating plants is also increasing in this region, and along with China, other countries, including South Korea, are also increasing their heating capacities.

Rest of the World

Rest of the World maintained a strong presence in the global market, reaching USD 0.24 billion in 2025, accounting for 0.14% share, and is expected to reach USD 0.25 billion in 2026. The rest of the world would observe slow growth in the market as these systems stand as a new concept and have started deployment as a cost-effective measure for power in several countries. The temperature in various parts of the world is not much lower to require centralized heating.

List of Key Companies in District Heating Market

Key Players Concentrating on New Contracts and Enhancing Product Portfolio

The competitive landscape of the market portrays a fragmented market with producers and service providers, such as Ramboll, Danfoss Group, and Veolia, occupying a considerable share in the global market. These companies have been successful over the years in acquiring new and long-term contracts from different countries in every region. The market also includes other players, such as Helen, Alfa Level, GE COWI, Statkraft, and others, who are increasing their customer reach and establishing a strong footprint in the market.

- In 2021 – Serbia signed a coal boilers replacement contract for a district heating system in Kragujevac with a consortium of local companies, Energotehnika, Reming, Jadran, and AG Institut.

- In 2020 – Savosolar Plc won a contract to supply two systems of solar heating to NewHeat SAS in France. After purchasing heating systems, the company will sell the heat generated by such systems to the DH companies of Pons and Narbonne.

LIST OF KEY COMPANIES PROFILED:

- Danfoss Group (Denmark)

- Ramboll (Denmark)

- Dall Energy (Denmark)

- Veolia (France)

- Helen (Finland)

- Alfa Level (Sweden)

- GE (U.S.)

- Statkraft (Norway)

- Uniper (Germany)

- ENGIE (France)

- FVB Energy Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- February 2024 – Evonik and Uniper formally launched the Technical Options for Thermal Energy Recovery (TORTE) project in Gelsenkirchen. The TORTE project will deliver industrial waste heat from isophorone generation into the district heating network. Over 1,000 homes in the Ruhr region will be delivered by the end of 2024.

- October 2023 - South Korea’s Naepo District Heating Plant jumps commercial operation, powered by GE Vernova’s H-Class combined cycle equipment. The new district heating plant based on a gas turbine will replace a previously planned solid refuse fuel boiler plant.

- October 2023 - Gradska toplana, the district heating system operator in the Serbian city, is about to build a heat pump that will use water from the Nišava River for heating purposes. The management announced several projects for the replacement of local fossil fuel-fired boilers with cleaner solutions.

- March 2021 – SWEP signed a multi-year contract with Kvitebjørn Varme AS. Under the contract, the company will provide Energy Transfer Stations (ETS) to progress the expansion of DH from an energy supplier based in Norway.

- December 2021, ENGIE and GASAG have been granted a significant project in Germany for distributed energy, mobility solutions, digitalization, and integrated services, as part of the "Das neue Gartenfeld" low-carbon smart district project in Spandau, a district in Berlin's northwestern suburbs. To accomplish this ground-breaking initiative, ENGIE and its local partner GASAG have partnered to build, connect, and run a highly efficient distributed energy infrastructure that will also deliver mobility and energy supply services.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, plant types, heat sources, and leading applications of the system. Besides this, the report offers insights into the market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of this market in recent years.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 2.97% from 2026-2034 |

|

Unit |

Volume (GWth) and Value (USD Billion) |

|

Segmentation |

By Heat Source

|

|

By Plant Type

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 174.45 billion in 2025.

Growing at a CAGR of 2.97%, the market will exhibit healthy growth over the forecast period (2026-2034).

The renewables segment is expected to be the leading segment in this market during the forecast period.

The rising initiatives to diminish the carbon emission is a key factor driving the market.

Ramboll, Danfoss Group, and Veolia are among the leading players in the global market.

Europe dominated the market in 2026.

The operational advantages, which lead to efficient energy production with economic advantages will drive the construction of DC networks.

- 2021-2034

- 2025

- 2021-2024

- 265

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us