Cell to Body Market Size, Share & Industry Analysis, By Propulsion Type (BEV and HEV), By Battery Type (Lithium Ion Battery and NI-MH Battery), and Regional Forecast, 2026-2034

Cell to Body Market Size and Future Outlook

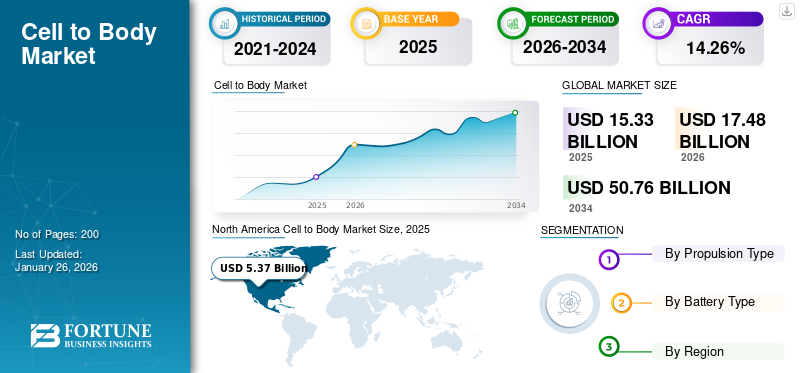

The global cell to body market size was valued at USD 15.33 billion in 2025. The market is projected to grow from USD 17.48 billion in 2026 to USD 50.76 billion by 2034, exhibiting a CAGR of 14.26% during the forecast period. North America dominated the global market with a share of 35.01% in 2025

Cell to body, also known as cell to chassis technology, involves integrating the battery cells directly into a car's structure. This approach reduces the vehicle's weight and creates additional space that would typically be taken up by a conventional, bulky battery pack.

The integration of cells of the battery directly into the vehicle's structure is gaining momentum for enhanced space utilization, reduced weight, and improved safety. Rising demand for longer EV ranges and better performance is pushing automakers to explore C2B solutions. These solutions aim to enable higher energy efficiency and reduce overall vehicle weight, driving market growth over a period of time.

The cell to body market is driven by key players such as Tesla, BYD, and Leapmotor, who are advancing battery integration for enhanced efficiency. Tesla leads with its innovative designs, setting benchmarks for vehicle performance and range. BYD focuses on scalable production, making strides in battery technology and vertical integration to meet increasing demand. Leapmotor, on the other hand, is making waves with its commitment to smart technology and affordability, targeting urban consumers with compact electric vehicles that boast advanced features and competitive pricing. Collectively, these companies are shaping the future of electric mobility through their distinct strategies and technological innovations.

Download Free sample to learn more about this report.

Cell to Body Market Key Takeaways

- 2025 Market Size: USD 15.33 Billion

- 2026 Market Size: USD 17.48 Billion

- 2034 Forecast Market Size: USD 50.76 Billion

- CAGR: 14.26% from 2026–2034

- North America dominated the market with a 35.01% share in 2025.

- The BEV segment is projected to dominate with a 64.53% share in 2026.

- The Lithium-ion Battery segment is projected to lead with a 64.72% share in 2026.

North America

The market was valued at USD 5.37 billion in 2025 and is projected to reach USD 6.10 billion in 2026.

Asia Pacific

The market was valued at USD 4.68 billion in 2025 and is projected to reach USD 5.37 billion in 2026.

Europe

The market was valued at USD 3.83 billion in 2025 and is projected to reach USD 4.37 billion in 2026.

U.S.

The market is projected to reach USD 3.64 billion by 2026.

Japan

The market is projected to reach USD 1.25 billion by 2026.

Read More

Market Dynamics

Market Drivers

Improved Energy Efficiency and Range to Propel Market Demand

By integrating battery cells directly into the vehicle's structure, automakers can reduce the weight and space occupied by traditional battery enclosures. This leads to more efficient energy storage and distribution, enhancing overall battery performance. As a result, EVs can achieve longer driving ranges with smaller, lighter batteries, which is crucial for addressing consumer demand for longer-lasting and more practical electric vehicles. Additionally, the reduction in weight improves energy efficiency, enabling vehicles to use less power to travel the same distance, further extending the range and enhancing the vehicle's performance. C2B integration offers a significant leap forward in achieving these goals, making it an attractive solution for automakers aiming to meet the growing demand for high-performance, long-range EVs. This drives the cell to body market growth during the forecast period.

Download Free sample to learn more about this report.

Market Restraint

Safety Concerns Significantly Hinder the Growth of Cell to Body (CTB) Technology

The integration of battery cells into the vehicle structure raises risks of thermal runaway, where excessive heat can lead to fires or explosions, particularly if a single cell fails. Additionally, the flammable electrolyte liquids used in lithium-ion batteries pose a fire hazard and can produce toxic substances, such as hydrofluoric acid, if leaked. Regulatory frameworks are still evolving, with many regions lacking stringent requirements to prevent cell-to-cell thermal propagation, which could exacerbate safety issues. These safety challenges contribute to consumer apprehension and regulatory scrutiny, ultimately slowing market adoption of CTB designs in the EV sector.

Market Opportunities

Rising Demand for Electric Vehicles Creating Opportunities for Cell to Body Technology

In 2023, electric car sales saw a 35% year-on-year increase, rising by 3.5 million units compared to 2022. Thus, as EV sales rise, manufacturers are compelled to innovate and enhance vehicle designs to meet consumer expectations for improved range and efficiency. CTB technology integrates battery cells directly into the vehicle's structure, reducing weight and freeing up space, which is crucial as larger batteries typically increase vehicle weight. This integration simplifies manufacturing and lowers production costs, making EVs more accessible. Furthermore, as the market EVs expands, CTB technology offers a competitive edge by improving performance and addressing range anxiety, thereby supporting the transition to sustainable transportation.

Market Challenge

Manufacturing and Assembly Complexities are Posing a Great Challenge to Market Development

Manufacturing and assembly challenges significantly restrain the growth of cell to chassis technology. The integration of cells of the battery directly into the vehicle structure complicates existing manufacturing processes, requiring new techniques and equipment that many manufacturers may not possess. This complexity can lead to increased production times and costs, hindering scalability. Furthermore, ensuring quality and safety during assembly becomes more challenging, as defects in battery integration could result in costly recalls. Additionally, the need for specialized training and equipment for workers adds to operational costs, making it difficult for manufacturers to transition smoothly to CTB systems while maintaining competitive pricing and quality standards in a rapidly evolving market.

Cell to Body Market Trends

Advancement in the Battery Technology to Boost Market Development

Progress in battery technology is crucial for accelerating the growth of cell to chassis integration in Electric Vehicles (EVs). Key innovations such as solid-state batteries, offer higher energy density and faster charging times, enhancing vehicle performance and reducing range anxiety for consumers. These batteries replace liquid electrolytes with solid ones, improving safety and longevity, which is crucial for structural integration into the vehicle body. Additionally, developments in silicon anodes and lithium-sulfur batteries promise greater efficiency and reduced weight, further optimizing the CBT design. As manufacturers adopt these advanced technologies, they can produce lighter, more efficient EVs that meet growing consumer demand for performance and sustainability, thereby accelerating market growth.

Impact of COVID-19

The COVID-19 pandemic significantly impacted the cell to body market by disrupting supply chains and altering consumer behavior. Initially, lockdowns led to a decline in EV sales due to halted production and reduced consumer demand, with overall car sales dropping by 14% globally. However, EV sales decreased by only 14%, highlighting their relative resilience. The pandemic also accelerated trends in the cell to body market, such as the indigenization and localization of battery production, prompting manufacturers to explore domestic sourcing for critical materials. Additionally, the rise of online sales channels emerged as a response to traditional distribution challenges, reshaping how consumers purchase EVs. Ultimately, while short-term disruptions occurred, the pandemic may have fostered long-term growth opportunities for the cell to chassis market.

Segmentation Analysis

By Propulsion Type

Better Efficiency of BEV Vehicles to Boost BEV Segment Growth

On the basis of propulsion type, the market is divided into BEV and HEV.

The BEV segment dominated the market in 2025, with the global demand for EV batteries surging significantly. BEVs accounted for the majority of this growth due to their higher efficiency compared to HEVs and low maintenance requirements. In 2023 alone, battery market demand for EVs reached over 750 GWh, 40% higher compared to 2022, primarily driven by increased BEV sales. This trend is expected to continue as manufacturers introduce new models and enhance production capabilities, which drives the growth of the segment. The segment held 64.53% of the market share in 2026.

The HEV segment is attributed to developing demand at a fastest-growing CAGR of 15.0% during the forecast period from 2025-2032. The availability of various hybrid configurations (mild hybrids, full hybrids, and plug-in hybrids) allows consumers to choose models that best fit their driving habits and needs. For instance, parallel hybrids can seamlessly switch between electric and ICE power, providing flexibility and efficiency during long-distance travel. This flexibility is expected to drive demand for the segment during the considered timeframe.

To know how our report can help streamline your business, Speak to Analyst

By Battery Type

Increasing Consumer Demand for Electric Mobility Solutions Propelled the Lithium-ion Battery Segment Growth

The market is divided into lithium-ion batteries and Ni-MH batteries, based on battery type.

The lithium-ion battery segment captured the largest market share in 2025 and is projected to experience the fastest growth rate during the forecast period. The global production capacity for lithium-ion batteries reached nearly 2000 GWh in 2023, with a significant portion dedicated to EVs. This rapid growth reflects the increasing consumer demand for electric mobility solutions. Moreover, different lithium-ion battery types serve various segments of the EV market. While NMC batteries are often used in high-performance vehicles due to their superior energy density, LFP batteries are preferred for budget-friendly models due to their cost-effectiveness and safety features. The segment is likely to capture 64.72% of the market share in 2026.

The NI-MH battery segment held a significant share of the market in 2024 and is likely to grow at the significant rate over the forecast period from 2025 to 2032. NiMH batteries have been widely used in HEVs, such as the Prius, Honda Insight, and others. Their successful application in these models has established them as a reliable choice for HEVs, fostering consumer confidence and encouraging further adoption within this segment, fueling market growth. This segment is expected to grow with a considerable CAGR of 13% during the forecast period (2025-2032).

Cell to Body Market Regional Outlook

In terms of region, the market is categorized into Europe, North America, the Asia Pacific, and the Rest of the World.

North America

North America Cell to Body Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America recorded a market size of USD 5.37 billion in 2025, capturing 35.01% of the global market share, and is projected to reach USD 6.1 billion in 2026. Major automotive manufacturers such as Tesla, General Motors, and Ford are investing heavily in EV production and battery technology innovations, including CTB designs. Their commitment to electrification drives competition and accelerates advancements in battery technologies within the region. Moreover, significant investments in research and development by automakers’ aim to improve battery performance and integrate new technologies such as CTB into their vehicle designs, thereby enhancing overall market growth. The U.S. market is poised to gain USD 3.64 billion in 2026.

Asia Pacific

The Asia Pacific market generated USD 4.68 billion in 2025, representing 30.53% of the global market landscape, and is expected to reach USD 5.37 billion in 2026. The outlook for the cell to body market in the Asia Pacific region is expected to experience the fastest growth rate during the forecast period. The overall electric vehicle market in Asia Pacific is expected to grow substantially. The Chinese market is poised to gain USD 1.24 billion in 2025. For example, the International Energy Agency projects that China, a key market for electric vehicles, will account for approximately 22.1 million EVs sold by 2035. This growth is driven by mounting consumer demand for EVs, which in turn fuels the need for innovative battery solutions such as CBT technology. India is foreseen to grow with a value of USD 1.06 billion in 2026, while Japan is set to acquire USD 1.25 billion in the same year.

Europe

In 2025, Europe represented USD 3.83 billion, accounting for 24.98% of the worldwide market, and is projected to grow to USD 4.37 billion in 2026. The European Union established ambitious goals to eliminate internal combustion engine (ICE) vehicles by 2035, providing a significant push for the adoption of electric vehicles. The U.K. market is anticipated to reach a market value of USD 0.56 billion in 2025. These regulations encourage automakers to invest in innovative technologies such as CTB to enhance vehicle performance and reduce emissions. There has been a significant increase in consumer interest in electric vehicles, with EV sales in Europe rising dramatically over recent years. In 2024, electric vehicles accounted for nearly 23% of newly registered passenger cars, indicating a robust market shift toward electrification. Germany is projected to reach a valuation of USD 1.62 billion in 2026, while France is expected to stand at USD 0.82 billion in the same year.

Rest of the World

The market in Rest of the World reached USD 1.45 billion in 2025, representing 9.50% of total market revenue, and is projected to reach USD 1.64 billion in 2026. The rest of the world includes regions such as Latin America, the Middle East and Africa. Countries such as Brazil are enhancing local production capabilities for EV components, including batteries. This focus on local manufacturing supports the feasibility of implementing advanced battery technologies such as CTB. Moreover, governments across Latin America and MEA are implementing various incentives to encourage the adoption of electric vehicles. These includes subsidies for EV purchases, tax breaks, and investments in charging infrastructure. Such policies enhance the attractiveness of innovative battery technologies such as CTB.

Competitive Landscape

Key Market Players

Companies are heavily investing in R&D to scale C2B technologies

The competitive landscape of cell to body technology in electric vehicles (EVs) is evolving rapidly, with several automakers and startups exploring its potential to enhance vehicle efficiency and reduce weight. C2B integrates the battery directly into the vehicle's structural components, eliminating the need for traditional battery enclosures. This innovation promises to lower costs, increase range, and improve safety. Key companies profiled in this space include established manufacturers such as Tesla, BYD, Xpeng, and Leapmotor, with other new entrants. Companies are heavily investing in research and development to scale C2B technologies. However, challenges such as battery performance, cost-effectiveness, and manufacturing complexity remain, which will shape the future competitive dynamics of the EV industry.

List of Key Companies Profiled in the Report

- Tesla (U.S.)

- BYD (China)

- Xpeng (China)

- Leapmotor (China)

- Xiaomi (China)

Key Industry Developments

- December 2024- BYD, in partnership with XCMG, China's largest construction machinery producer, launched three new battery models for construction vehicles. These batteries—Super-hybrid, Super-fast charging, and Super-integration—are based on BYD's lithium iron phosphate Blade battery and aim to give BYD a strong presence in this emerging market. The Super-hybrid battery has 120 Wh/kg energy density, 17.3 kWh capacity, and a 4C charge rate. The Super-fast charging battery offers 160 Wh/kg energy density, 37.7 kWh capacity, a 400 A charge/discharge current, and a lifespan of 7,000 cycles. It can charge in 10 minutes for 1.5 hours of use, though its 2C charge rate is not considered "super-fast." The super-integration battery is designed for cell to body integration, has 320 Wh/l energy density and 97.7 kWh capacity, and can withstand six times more vibration than standard packs.

- November 2024: BYD launched the Yuan Pro in Mexico, the country's most affordable electric SUV, aimed at young urban drivers. Powered by a 177-horse-powered electric motor with 213 lb-ft of torque, it achieves 0-100 km/h in 7.9 seconds. Equipped with a 45 kWh Blade battery, it offers a driving range of up to 380 km and supports fast charging, reaching 30% to 80% in 20 minutes. The battery's high-strength steel design and BYD's cell to body (CTB) technology enhance durability and stability. Extensive safety testing ensures the vehicle meets high impact resistance standards.

- October 2024: BYD launched its high-performance Seal EV at the Philippine Electric Vehicle Summit, furthering its commitment to sustainable transport. Key features include the performance of 530 horsepower, 0-100 km/h in 3.8 seconds, and all-wheel drive. E-Platform 3.0 and cell to body (CTB) for better battery efficiency and safety. Range up to 580 km (NEDC) with BYD's Blade Battery. DiPilot Advanced Assistance, Intelligent Cruise Control, and a 360º camera.

- September 2024- Volvo showcased the battery cell to body technology for upcoming Volvo models built on the SPA3 architecture.

- January 2024, Xiaomi launched the Xiaomi SU7 Max, with a battery made by Xiaomi that integrates Cell to Body (CTB) design.

Investment Analysis and Opportunities

Enhancing Growth Opportunities through Brand Investments and Collaborations in the Cell to Body Market

increasing brand investments and strategic collaborations with various stakeholders play a pivotal role in unlocking significant growth opportunities. As automakers, battery manufacturers, and technology firms recognize the advantages of integrating battery systems into structural vehicle components, they are increasingly pooling resources and expertise to streamline innovation. Collaborative efforts between automotive companies and research institutions can accelerate the development of advanced materials and manufacturing techniques, such as lightweight composites and scalable production methods. Furthermore, partnerships with technology firms specializing in automation and artificial intelligence can enhance efficiency in production processes and supply chain management. These collaborative investments not only help to share the financial burden and mitigate risks associated with new developments but also facilitate knowledge transfer and foster a culture of innovation. As brands align their interests with key stakeholders, the C2B market is positioned for robust growth, leading to enhanced vehicle performance, sustainability, and consumer satisfaction.

REPORT COVERAGE

The cell to body market report provides an in-depth analysis and highlights crucial aspects such as prominent companies, regional and market segmentation, competitive landscape, propulsion type, and battery type. Besides this, the report provides insights into the market trends and highlights significant industry developments. In addition to this, the report encompasses several factors contributing to the market growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 14.26% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Propulsion Type, By Battery Type, and By Region |

|

Segmentation |

By Propulsion Type

By Battery Type

|

|

By Region

|

Frequently Asked Questions

The global cell to body market size was valued at USD 15.33 billion in 2025. The market is projected to grow from USD 17.48 billion in 2026 to USD 50.76 billion by 2034, exhibiting a CAGR of 14.26% during the forecast period.

Fortune Business Insights says that the global market value stood at USD 15.33 billion in 2025.

The global market will exhibit a CAGR of 14.26% over the forecast period.

By battery type, the lithium ion battery segment dominated the market.

Improved energy efficiency and range is a key factor propelling market growth.

Tesla, BYD, Xpeng, and Leapmotor are some of the leading players globally.

In 2025, North America led the global market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us