Cellular Glass Market Size, Share & Industry Analysis, By Product Type (Block & Shell and Foam Glass Gravel), By Application (Industrial, Construction, and Others), and Regional Forecast, 2026-2034

Cellular Glass Market Size and Future Outlook

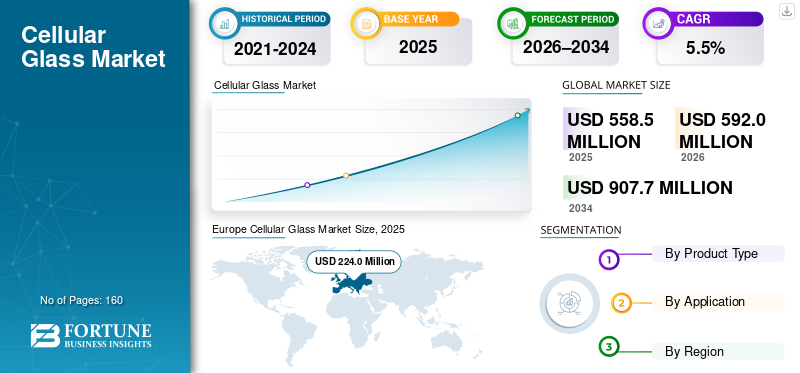

The global cellular glass market size was valued at USD 558.5 million in 2025. The market is projected to grow from USD 592.0 million in 2026 to USD 907.7 million by 2034, exhibiting a CAGR of 5.5% during the forecast period. Europe dominated the cellular glass market with a market share of 40.11% in 2025.

Cellular glass (also known as foam glass) is a rigid, closed-cell insulation material produced by foaming recycled glass and forming it into products such as blocks, shells, boards, or granules. It is non-combustible, water- and vapor-tight, dimensionally stable, and offers high compressive strength compared with many insulation alternatives. It is widely used across various end uses, including construction, industrial process insulation, and other specialty applications where long-term thermal performance and moisture resistance are critical.

The market’s growth is driven by stricter building safety and energy-efficiency requirements, rising preference for non-combustible insulation systems, and continued investment in industrial and cryogenic infrastructure that benefits from vapor-tight insulation.

Furthermore, the market comprises several major players, including Owens Corning, Wedge India, PINOSKLO, ZHEJIANG ZHENSHEN INSULATION TECHNOLOGY CORP.LTD., and Tianjin Huali Thermal Insulation Building Material Co., Ltd. A broad portfolio, innovative product launches, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

Cellular Glass Market Key Takeaways

- 2025 Market Size: USD 558.5 million

- 2026 Market Size: USD 592.0 million

- 2034 Forecast Market Size: USD 907.7 million

- CAGR: 5.5% from 2026-2034

- Europe dominated the cellular glass market with a 40.11% share in 2025.

- The block & shell segment accounted for the largest market share in 2025.

- The industrial segment held a 53.7% share in 2025.

Europe

Europe was valued at USD 224.0 million in 2025 and is projected to reach USD 238.7 million in 2026.

Asia Pacific

Asia Pacific is expected to reach USD 126.7 million in 2026, supported by growing industrial and construction activities.

North America

North America is projected to grow at a CAGR of 5.7% and reach USD 151.7 million by 2026, driven by infrastructure and commercial insulation demand.

U.S.

The market reached USD 126.5 million in 2025, supported by strong demand from industrial processing and infrastructure projects.

Japan

Increasing focus on energy-efficient buildings and industrial insulation solutions is supporting market growth.

Read More

CELLULAR GLASS MARKET TRENDS

Fire-Safe Building Envelopes, Circular Recycled-Glass Insulation, and Cryogenic Projects

Cellular glass demand continues to be shaped by the construction sector’s need for non-combustible, moisture-resistant insulation solutions for roofs, façades, and below-grade assemblies, particularly where codes and specifications prioritize fire safety and long-term durability. At the same time, suppliers are strengthening circularity narratives by increasing recycled-glass content and publishing product environmental documentation, which supports adoption in sustainability-led procurement. In parallel, industrial demand remains anchored by projects requiring insulation performance across extreme temperature ranges, including LNG and other cryogenic systems, where vapor-tight insulation helps reduce condensation risks and corrosion under insulation.

- For instance, the revised Energy Performance of Buildings Directive (EU/2024/1275) entered into force on 28 May 2024 and emphasizes faster renovation and higher energy performance in the EU building stock, supporting durable insulation demand (European Commission

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Non-Combustible, Vapor-Tight Insulation Needs, and Load-Bearing Performance Requirements, Drive Market Growth

Cellular glass is increasingly specified where non-combustibility, long-life thermal stability, and moisture impermeability are mandatory, including flat roofs, foundations, and industrial systems exposed to harsh operating conditions. Unlike many polymeric insulation materials, cellular glass maintains performance under wet conditions and supports high compressive loads, which are relevant for roof decks, equipment-bearing assemblies, and below-grade insulation designs. In industrial applications, consistent performance requirements and specification-led procurement support repeat adoption in process plants and cryogenic assets.

- For instance, ASTM C552 defines performance requirements for cellular glass thermal insulation intended for commercial and industrial systems

MARKET RESTRAINTS

Higher Installed Cost Versus Commodity Insulation and a Limited Producer Base Limit Wider Adoption

Cellular glass is typically positioned as a premium insulation material, and adoption can be constrained in cost-sensitive projects where polymer foams or mineral wool are accepted substitutes. The market also has a limited number of specialized manufacturers, and logistics can be restrictive for foam glass gravel due to the economics of bulk transport. In addition, specification and contractor familiarity can be uneven across regions, increasing qualification and installation learning burdens for certain project teams. Collectively, these factors may restrain product adoption, impeding the cellular glass market growth.

MARKET OPPORTUNITIES

Renovation Programs and LNG/Cryogenic Capacity Expansion to Create Lucrative Growth Opportunities

Policy-led renovation programs and strengthened energy-performance rules create opportunities for cellular glass in roofs, foundations, and moisture-sensitive assemblies, where its long service life and low water uptake reduce lifecycle risk. On the industrial side, expansion of LNG capacity and broader investment in cryogenic infrastructure support demand for vapor-tight insulation that maintains structural integrity across extreme temperature gradients. Opportunities also exist to expand the adoption of foam glass gravel as a circular, load-bearing insulation and lightweight fill material in foundations and infrastructure projects.

- The International Energy Agency’s Global LNG Capacity Tracker highlights ongoing liquefaction capacity additions through 2030, supporting insulation demand linked to LNG infrastructure

MARKET CHALLENGES

Substitution Risk in Standard Construction Uses and Project Cyclicality in Industrial End Uses, May Hamper Market Growth

In standard building insulation applications, cellular glass competes with lower-cost insulation materials, and the substitution risk remains high where non-combustibility or vapor-tightness is not a strict requirement. For industrial and cryogenic applications, demand can be project-driven, with procurement tied to capex cycles in the LNG, refining, and process industries. Additionally, energy cost volatility can influence manufacturing economics, while region-specific approvals and contractor practices can slow adoption in new geographies.

Segmentation Analysis

By Product Type

Block & Shell Segment Leads Due to its High Use in Industrial Insulation and Roof and Building Applications

Based on product type, the market is segmented into block & shell and foam glass gravel.

The block & shell segment accounted for the largest cellular glass market share in 2025. The segment is driven by use in industrial insulation systems and demanding roof and building applications where non-combustibility and vapor-tight performance are critical.

The foam glass gravel segment is expected to grow favorably throughout the forecast period, is supported by use as load-bearing insulation and lightweight fill in foundations, roofs, and infrastructure. Its growth aligns with circular construction practices and the increasing interest in recycled-glass-based aggregates for insulation and drainage. The foam glass gravel segment is projected to grow at a 5.1% CAGR during the study period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Industrial Application Dominates Due to the Extensive Use of Cellular Glass

By application, the market is categorized into industrial, construction, and others.

The industrial segment accounted for the largest cellular glass market share of 53.7% in 2025. The segment’s growth is primarily driven by cellular glass specifications in process plants, refineries, chemical facilities, and cryogenic systems, where moisture impermeability and long-life thermal performance reduce operational risks.

The construction segment is also expected to experience a CAGR of 5.2% over the projected period. The segment's growth is supported by premium roof and below-grade assemblies, particularly where non-combustibility, compressive strength, and water resistance are critical.

Cellular Glass Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Europe

Europe Cellular Glass Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Europe held the dominant share in 2025, valued at USD 224.0 million, and is expected to maintain the leading share in 2026, with USD 238.7 million. The region's growth is driven by stringent building energy-performance requirements and strong adoption of non-combustible insulation solutions in renovation and new-build projects.

Germany Cellular Glass Market

Germany’s market reached approximately USD 59.1 million in 2025, equivalent to around 6.4% of global sales.

To know how our report can help streamline your business, Speak to Analyst

U.K. Cellular Glass Market

The U.K. in 2025 achieved USD 29.3 million, representing approximately 5.3% of global market revenue.

North America

North America is expected to experience significant growth of 5.7% over the forecast period and reach USD 151.7 million in 2026. The region benefits from mission-critical roofing specifications, industrial insulation requirements, and continued investment in energy and process-industry assets.

U.S. Cellular Glass Market

In 2025, the U.S. market garnered USD 126.5 million as the country accounts for the majority of regional consumption through upstream and midstream infrastructure, industrial processing assets, and high-performance commercial building insulation projects.

Asia Pacific

Asia Pacific is also a significant contributor with the market estimated to reach USD 126.7 million in 2026. The region’s growth is supported by industrial investment, selective adoption in high-performance building envelopes, and expansion of cold-chain and process infrastructure. China remains the largest consumer in the region, while Japan and South Korea contribute through industrial and high-spec building applications.

China Cellular Glass Market

In 2025, the Chinese market captured USD 47.3 million driven by industrial insulation in chemicals, refining, and selected cryogenic/cold-chain systems, where moisture-tight, non-combustible performance is valued.

Latin America

Latin America is experiencing steady growth with 2026 projections estimated to reach USD 29.8 million. The demand is largely import-driven and linked to selective industrial projects, premium construction specifications, and infrastructure use cases where load-bearing insulation and moisture resistance add value.

The Middle East & Africa

The Middle East & Africa is gradually expanding, with sales recorded of around USD 45.1 million in 2025. GCC countries account for the majority of regional demand due to industrial and energy infrastructure projects where vapor-tight insulation is valued, while non-GCC demand is tied to selected construction and institutional procurement.

GCC Cellular Glass Market

GCC reached USD 26.8 million in 2025, accounting for approximately 4.3% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Adopting Specification-Led Selling, Circularity Positioning, and Fabrication Capability to Maintain Market Positions

Competition is shaped by process know-how (closed-cell performance consistency), certification and compliance capabilities, access to recycled-glass feedstock, and the ability to support project specifications in construction and industrial markets. Key competitive differentiators include fabrication services for shells and custom shapes, contractor support, and published product documentation for sustainability-oriented procurement.

Some of the key market players include Owens Corning, Wedge India, PINOSKLO, ZHEJIANG ZHENSHEN INSULATION TECHNOLOGY CORP.LTD., and Tianjin Huali Thermal Insulation Building Material Co., Ltd. Product portfolios, technical approvals, and regional distribution strength support these players' positioning in the global market.

LIST OF KEY CELLULAR GLASS COMPANIES PROFILED

- Owens Corning (U.S.)

- Wedge India (India)

- PINOSKLO (Ukraine)

- ZHEJIANG ZHENSHEN INSULATION TECHNOLOGY CORP.LTD. (China)

- Tianjin Huali Thermal Insulation Building Material Co., Ltd. (China)

- INSULTHERM (U.S.)

- POLYDROS, S.A. (Spain)

- Cellglas Group AB (Sweden)

- Metfel Engineering LLC (Turkey)

- Multi-Glass Insulation Ltd. (Canada)

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.5% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Product Type, Application, and Region |

|

By Product Type |

· Block & Shell · Foam Glass Gravel |

|

By Application |

· Industrial · Construction · Others |

|

By Geography |

· North America (By Product Type, Application, and Country) o U.S. (By Application) o Canada (By Application) · Europe (By Product Type, Application, and Country/Sub-region) o Germany (By Application) o France (By Application) o Italy (By Application) o U.K. (By Application) o Rest of Europe (By Application) · Asia Pacific (By Product Type, Application, and Country/Sub-region) o China (By Application) o Japan (By Application) o India (By Application) o South Korea (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Product Type, Application, and Country/Sub-region) o Brazil (By Application) o Mexico (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Product Type, Application, and Country/Sub-region) o GCC (By Application) o South Africa (By Application) o Rest of the Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights estimates that the global market size was USD 558.5 million in 2025 and is projected to reach USD 907.7 million by 2034.

The market is slated to record a CAGR of 5.5% during the forecast period.

The industrial application segment led the market in 2025.

Europe held the highest market share in 2025.

Owens Corning, Wedge India, PINOSKLO, ZHEJIANG ZHENSHEN INSULATION TECHNOLOGY CORP.LTD., and Tianjin Huali Thermal Insulation Building Material Co., Ltd are some of the prominent players in the market.

The rising need for non-combustible, vapor-tight insulation in construction and industrial systems, especially where fire safety and moisture resistance are mandatory drives growth.

Stricter building energy codes, increasing use in below-grade/foundation and flat-roof assemblies, and continued industrial/cryogenic (e.g., LNG) investments where long-life, corrosion-resistant insulation reduces lifecycle risk.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us