Cerebral Palsy Treatment Market Size, Share & Industry Analysis, By Disease Type (Spastic Cerebral Palsy, Dyskinetic Cerebral Palsy, Ataxic Cerebral Palsy, and Others), By Treatment (Botulinum Toxin, Anticonvulsants, Anticholinergics, Muscle Relaxants, and Others), By Age Group (Pediatrics (0–12 years), Adolescents (13–17 years), and Adults (18+ years)), By Route of Administration (Oral, Injectable, and Intrathecal), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies & Drug Stores, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

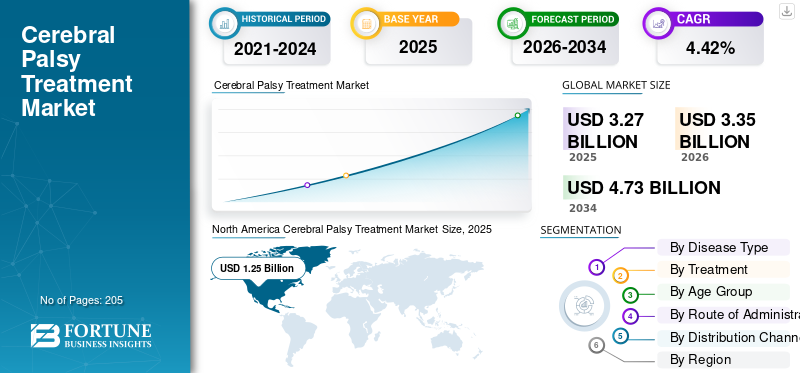

The global cerebral palsy treatment market size was valued at USD 3.27 billion in 2025. The market is projected to grow from USD 3.35 billion in 2026 to USD 4.73 billion by 2034, exhibiting a CAGR of 4.42% during the forecast period. North America dominated the global market with a share of 38.23% in 2025.

Cerebral Palsy (CP) is a group of neurological disorders that affect a person’s movement, muscle tone, posture, and coordination. It is caused by damage or abnormal development of the brain, most often occurring before birth, but it can also happen during birth or early infancy. This market is driven by the need to develop effective treatments, the increasing prevalence of the condition, and growing awareness among the population.

The market encompasses key players such as Neurocrine Biosciences, Inc., REVANCE, Pfizer Inc., and Ipsen Pharma. This companies are emphasizing on innovative product development to maintain their market presence.

Download Free sample to learn more about this report.

CEREBRAL PALSY TREATMENT MARKET TRENDS

Increasing Use of Botulinum Toxin (BoNT-A) in Pediatric Spasticity Cerebral Palsy is a Key Market Trend

BoNT-A remains the most valuable therapy in CP pharmacotherapy, and recent work is increasingly focused on real-world effectiveness, goal attainment, and improved patient selection, especially in severe CP (GMFCS IV–V) and ambulant children. This supports broader adoption, repeat dosing adherence, and more structured spasticity clinics. This trend is accelerating the adoption of injection guidance tools, which can improve precision and patient outcomes, in turn supporting higher procedure throughput and stronger real-world value propositions. These factors are supporting the overall global cerebral palsy treatment market growth.

- For instance, according to a study published in June 2025 in Developmental Medicine & Child Neurology, abobotulinumtoxinA in pediatric lower-limb spasticity, with most patients having CP, is being evaluated.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Prevalence of Cerebral Palsy is Driving Market Growth

The global cerebral palsy treatment market is primarily being driven by the rising overall burden of cerebral palsy, especially in Low and Middle-Income Countries (LMICs), where population growth and improving survival increase the number of children living with long-term neurodisability. Around the world, the absolute number of individuals needing lifelong symptom management for spasticity, epilepsy, and drooling is increasing as more infants survive prematurity and neonatal complications. This expands the treated population base for anticonvulsants and supports broader uptake of botulinum toxin as specialist capacity grows. All these factors cumulatively drive the overall market growth.

- For instance, according to a study published in August 2025 in The Lancet, the prevalence of CP is approximately 1.6 per 1,000 in high-income countries, but can be as high as 4 per 1,000 in LMICs.

MARKET RESTRAINTS

High Cost of Advanced Spasticity Therapies to Hamper Market Growth

The high cost of advanced spasticity therapies, especially botulinum toxin injections and Intrathecal Baclofen (ITB) based regimens, is a major market restraint in the cerebral palsy treatment market. It limits affordability and reimbursement approvals, particularly outside high-income settings. Additionally, the ongoing follow-up burden for severe spasticity management, such as repeat injections, monitoring, and multidisciplinary care, which raises the total cost of care and payer scrutiny, also limits the market growth. This results in limiting the market growth to a certain extent.

- For instance, according to an article published by the Cerebral Palsy Guide in November 2025, the lifetime cost to treat and care for a patient with cerebral palsy is approximately USD 1.6 million in 2026.

MARKET OPPORTUNITIES

Expansion of Intrathecal Baclofen (ITB) Therapy to Offer Market Growth Opportunities

Expansion of Intrathecal Baclofen (ITB) therapy presents a significant market opportunity. This therapy is promising, particularly for cerebral palsy patients with severe generalized spasticity who do not achieve adequate control with oral agents or focal botulinum toxin. In recent years, this therapy gained attention for its ability to deliver baclofen directly to the spinal fluid, improving efficacy while reducing systemic side effects compared to high-dose oral therapy. The opportunity is strengthened by growing efforts to standardize patient selection, define measurable outcomes (such as spasticity scales and the GMFM), and establish clearer referral pathways through multidisciplinary spasticity clinics. All these factors would drive the market growth in the coming years.

- For instance, according to an article published in April 2024, improvements in spasticity severity and motor function metrics were observed during an evaluation study of intrathecal baclofen.

MARKET CHALLENGES

Fragmented Care Pathways and Uneven Referral Patterns Pose a Significant Challenge to Market Growth

Fragmented care pathways and uneven referral patterns are a persistent challenge in the cerebral palsy treatment market. The management of cerebral palsy spans neurology, rehabilitation, orthopedics, and allied health, and patients often move between providers without a single coordinated treatment owner. This fragmentation delays therapy escalation and creates variability. It also increases the risk during transitions of care, thereby reducing the continuity of long-term drug management and the frequency of repeat procedures. All the factors cumulatively affect the market growth.

Segmentation Analysis

By Disease Type

High Number of Patients to Propel Spastic Cerebral Palsy Segmental Growth

Based on the disease type, the market is divided into spastic cerebral palsy, dyskinetic cerebral palsy, ataxic cerebral palsy, and others.

The spastic cerebral palsy segment captured the largest global cerebral palsy treatment market share. This is the most prevalent and consistently treated motor impairment in cerebral palsy, in turn dominating the global market. Additionally, spastic CP is recognized as the most common CP subtype, creating the largest treatable pool for drug interventions.

- For instance, according to a study published in the National Center for Biotechnology Information (NCBI) in July 2021, spasticity is present in more than 80% of the population with cerebral palsy (CP).

The dyskinetic cerebral palsy segment is anticipated to rise with a CAGR of 5.80% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Treatment

High Usage for Epilepsy Management to Boost Anticonvulsants Segmental Growth

On the basis of treatment, the market is divided into botulinum toxin, anticonvulsants, anticholinergics, muscle relaxants, and others.

The anticonvulsants segment dominated the global market in 2025. Epilepsy is one of the most common and clinically impactful comorbidities in cerebral palsy, creating a large, continuously treated patient pool. Additionally, anti-seizure medicines are typically taken daily for years, driving steady, high-volume prescription demand and recurring revenues. Furthermore, the segment is set to hold a 41.4% share in 2026.

- For instance, according to a study in November 2024 in Medicina, out of 88,138 CP patients in the U.S. National Inpatient Sample, 44,901 had epilepsy.

The botulinum toxin segment is anticipated to grow with a CAGR of 5.46% over the forecast period.

By Age Group

Large Pediatric Patient Population to Boost Pediatrics Segmental Growth

On the basis of age group, the market is divided into pediatrics (0–12 years), adolescents (13–17 years), and adults (18+ years).

The pediatrics (0–12 years) segment captured the largest share. Cerebral palsy is typically identified in early childhood, and pharmacotherapy is initiated early to manage spasticity, seizures, and drooling. Pediatric patients account for the largest active treatment pool, as families and clinicians prioritize early intervention to improve mobility, function, and participation, which increases the utilization of anticonvulsants and spasticity therapies, including botulinum toxin cycles. Furthermore, the segment is set to hold a 49.3% share in 2026.

- For instance, according to a study published in the National Center for Biotechnology Information (NCBI) in August 2022, the current overall CP birth prevalence is 1.6 per 1000 live births.

The adults (18+ years) segment is expected to rise with a CAGR of 5.97% over the forecast period.

By Route of Administration

Ease of Administration Supported the Oral Segmental Dominance

Based on the route of administration, the market is divided into oral, injectable, and intrathecal.

The oral segment is expected to account for the largest market share. Oral medicines are easier to initiate and maintain across care settings, requiring no procedure room, injector training, or sedation support. This makes oral therapies the most scalable and accessible option across all regions, particularly in emerging markets where specialist injection capacity is limited. In addition, oral drugs are dispensed largely through retail/community channels, enabling refill-driven continuity and stable volumes. Furthermore, the segment is set to hold a 54.3% share in 2026.

- For instance, epilepsy being an important symptom of cerebral palsy is managed through oral medications.

The injectable segment is likely to grow with a CAGR of 5.32% over the forecast period.

By Distribution Channel

High Patient Admissions in Hospitals to Support Hospital Pharmacies Segment Growth

Based on distribution channel, the market is segmented into hospital pharmacies, retail pharmacies & drug stores, and others.

In 2025, the hospital pharmacies segment held the leading position in the global market. CP management is heavily driven by injectable botulinum toxin for spasticity and, in severe cases, intrathecal baclofen therapy, both of which are typically delivered through hospital-based neurology/rehab pathways. Additionally, hospitals also handle complex pediatric cases where dosing, monitoring, and multidisciplinary coordination are essential. Furthermore, the hospital pharmacy segment is set to hold a 50.4% share in 2026.

In addition, retail pharmacies & drug stores are projected to grow at a CAGR of 5.34% during the forecast period.

Cerebral Palsy Treatment Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Cerebral Palsy Treatment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America cerebral palsy treatment market size was USD 1.22 billion in 2024 and dominated the global market. The region also maintained its dominance in 2025, with USD 1.25 billion. The regional market growth can be attributed to high prevalence of cerebral palsy, and rapidly expanding clinical pipeline of innovative drugs in the region.

U.S. Cerebral Palsy Treatment Market

The U.S. market held the leading share of the North American market and is expected to reach USD 1.18 billion as its valuation in 2026, accounting for roughly 35.3% of global market.

Europe

Europe cerebral palsy treatment market is anticipated to grow at a CAGR of 3.91% in the coming years. The region is anticipated to become the second highest among all regions. European market is majorly driven by rising investments in drug development, and advancing treatment facilities coupled with rising burden of cerebral palsy among the population.

U.K Cerebral Palsy Treatment Market

The U.K. cerebral palsy treatment market in 2026 is estimated at around USD 0.22 billion, representing roughly 6.5% of global revenues.

Germany Cerebral Palsy Treatment Market

Germany cerebral palsy treatment market size is projected to reach approximately USD 0.20 billion in 2026, equivalent to around 6.0% of global sales.

Asia Pacific

Asia Pacific cerebral palsy treatment market size is set to be valued at USD 0.79 billion in 2026 and secure the position of the third-largest region in the global industry. This is driven by increasing awareness about the disease, rising investment in clinical research, and others.

Japan Cerebral Palsy Treatment Market

The Japan cerebral palsy treatment market in 2026 is estimated at around USD 0.15 billion, accounting for roughly 4.4% of global revenues.

China Cerebral Palsy Treatment Market

China’s cerebral palsy treatment market is projected to reach revenues of around USD 0.24 billion in 2026, representing roughly 7.2% of global sales.

India Cerebral Palsy Treatment Market

The India cerebral palsy treatment market in 2026 is estimated at around USD 0.13 billion, accounting for roughly 3.7% of global revenues.

Latin America and Middle East & Africa

The Latin America and the Middle East & Africa regions are likely to witness a growing adoption of cerebral palsy medications throughout the forecast period. The Latin America cerebral palsy treatment market size is expected to reach a valuation of USD 0.19 billion in 2026. These regional growth is majorly driven through increasing number of patients along with availability of generic medications driving the affordability of treatment.

Among the Middle East & Africa region, the GCC market in 2026 is estimated at around USD 0.05 billion, accounting for roughly 1.6% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Research and Development Activities by Prominent Companies to Strengthen Market Share

The global cerebral palsy treatment market is semi-fragmented in structure. It is highly consolidated in premium, procedure-linked injectables, such as botulinum toxins, while remaining fragmented in oral therapies such as anticonvulsants, muscle relaxants, and anticholinergics. Some of the key players include Ipsen Pharma, Abbvie Inc., Revance, Pfizer Inc. and others.

Other key players in the market include Neurocrine Biosciences, Inc., HOPE BIOSCIENCES, Kidswell Bio, and others. These companies are actively involved in the development of innovative drugs for the treatment of the disease.

- For instance, in April 2022, Neurocrine Biosciences, Inc. initiated a phase 3 clinical trial for the evaluation of the efficacy of Valbenazine for the treatment of dyskinetic cerebral palsy.

LIST OF KEY CEREBRAL PALSY TREATMENT COMPANIES PROFILED

- Neurocrine Biosciences, Inc. (U.S.)

- REVANCE (U.S.)

- Abbvie Inc. (U.S.)

- HOPE BIOSCIENCES (U.S.)

- Kidswell Bio (Japan)

- Ipsen Biopharmaceuticals, Inc. (U.S.)

- DSM Pharmaceuticals, Inc. (U.S.)

- Pfizer Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Neurocrine Biosciences, Inc. reported that its Phase 3 KINECT-DCP study of valbenazine in dyskinetic cerebral palsy did not meet primary/key secondary endpoints.

- November 2025: Kidswell Bio’s subsidiary S-Quatre announced alignment at a U.S. FDA pre-IND meeting for a planned company-sponsored CP trial of allogeneic SQ-SHED.

- November 2025: Kidswell Bio disclosed interim results via Nagoya University from a study using autologous SHED in children with CP, reporting safety/tolerability and suggesting potential motor function improvements.

- August 2024: Granules India announced U.S. FDA ANDA approval for glycopyrrolate oral solution 1 mg/5 mL, referencing equivalence to Cuvposa and noting its pediatric drooling indication.

- January 2024: Neurotech announced Human Research Ethics Committee (HREC) approval to commence a Phase I/II trial of NTI164 in pediatric spastic diplegia CP.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.42% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Disease Type, Treatment, Age Group, Route of Administration, Distribution Channel, and Region |

|

By Disease Type |

· Spastic Cerebral Palsy · Dyskinetic Cerebral Palsy · Ataxic Cerebral Palsy · Others |

|

By Treatment |

· Botulinum Toxin · Anticonvulsants · Anticholinergics · Muscle Relaxants · Others |

|

By Age Group |

· Pediatrics (0–12 years) · Adolescents (13–17 years) · Adults (18+ years) |

|

By Route of Administration |

· Oral · Injectable · Intrathecal |

|

By Distribution Channel |

· Hospital Pharmacies · Retail Pharmacies & Drug Stores · Others |

|

By Region |

· North America (By Disease Type, Treatment, Age Group, Route of Administration, Distribution Channel, and Country) o U.S. o Canada · Europe (By Disease Type, Treatment, Age Group, Route of Administration, Distribution Channel, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Disease Type, Treatment, Age Group, Route of Administration, Distribution Channel, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Disease Type, Treatment, Age Group, Route of Administration, Distribution Channel, and Country/Sub-region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Disease Type, Treatment, Age Group, Route of Administration, Distribution Channel, and Country/Sub-region) o GCC o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 3.27 billion in 2025 and is projected to reach USD 4.73 billion by 2034.

In 2025, the North America market value stood at USD 1.25 billion.

The market is expected to exhibit a CAGR of 4.42% during the forecast period of 2026-2034.

By disease type, the spastic cerebral palsy segment dominated the market.

Increasing prevalence of cerebral palsy is the key factor driving the market.

Neurocrine Biosciences, Inc., Revance, Pfizer Inc., and Ipsen Pharma are some of the major players in the global market.

North America dominated the market in 2025 in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us