Chickpea Flour Market Size, Share & Industry Analysis, By Product Type (Dark Brown Chickpea Flour, Beige Chickpea Flour, Lentil Flour, and Others), By Application (Food & Beverages [Bakery & Confectionery, Beverages, Meat Alternatives, RTE Products, and Others], Animal Feeds, and Others), By Nature (Conventional and Organic), By Distribution Channel (Online and Offline), and Regional Forecast, 2026-2034

(Offer valid till 31st Jul 2026)

KEY MARKET INSIGHTS

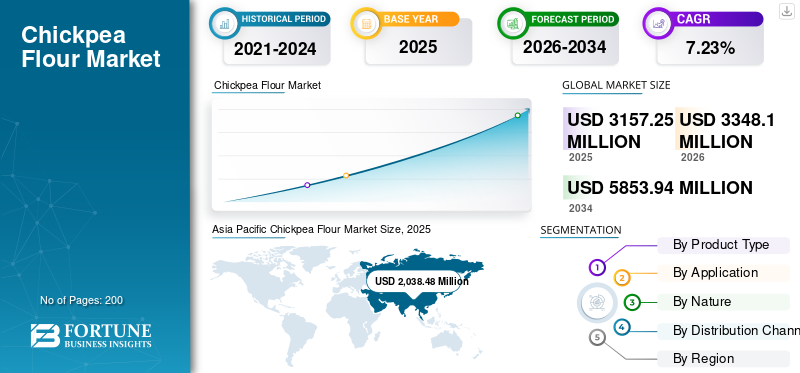

The global chickpea flour market size was valued at USD 3,157.25 million in 2025. The market is projected to grow from USD 3,348.10 million in 2026 to USD 5,853.94 million by 2034, exhibiting a CAGR of 7.23% during the forecast period. Asia Pacific dominated the global chickpea flour market with a market share of 64.6% in 2025.

Chickpea flour, milled from desi and kabuli chickpeas, is recognized for its high protein, fiber, and micronutrient content, making it a preferred substitute for wheat flour in gluten-free and clean-label formulations. The market expansion is supported by the rising demand for gluten-free, high-protein, clean-label, and plant-based ingredients across bakery, snacks, meat alternatives, and ready-to-eat (RTE) products. Increasing incorporation of chickpea flour in fortified foods, vegan formulations, and high-fiber products continues to boost global adoption. Sustainable crop sourcing and clean-label trends are gaining traction in the global market, encouraging new product lines across regions.

The global market is dominated by major players, including Ingredion Incorporated, Archer Daniels Midland Company (ADM), The Scoular Company, AGT Food and Ingredients, and Batory Foods. Manufacturers are leveraging production technologies, such as advanced roasting, micronization, and high-shear milling, to improve sensory performance and expand application potential across both food products and industrial categories.

Download Free sample to learn more about this report.

Chickpea Flour Market Trends

Rapid Expansion of Tapioca Pearls and Chickpea Flour-Based Beverages

The increasing commercialization of chickpea flour in vegan and meat alternative applications is indeed a key recent trend shaping growth in the global market, driven by its functional, nutritional, and clean-label attributes. The rising vegan and flexitarian diets are pushing the demand for plant-based proteins and chickpea flour use in protein-rich products, meat substitutes, and snacks has risen sharply in the last few years. Patented processing technologies (e.g., flavorless, high-functionality flour) specifically target egg and dairy replacement in vegan bakery, egg substitutes, and meat analogues, removing off-flavors and color while boosting protein functionality.

- For instance, in June 2023, Ardent Mills introduced two chickpea-based solutions, including Egg Replace and Ancient Grains Plus Baking Flour Blend, aimed at cost-effective, plant-based, high-protein bakery and snack applications. The use of chickpea flour in both products directly supports the broader trend toward pulse-based ingredients in vegan, egg-free, and “better-for-you” formulations in North American and global bakery markets.

MARKET DYNAMICS

Market Drivers

Expanding Applications in Bakery, Snacks, and Meat Alternatives to Drive Market Growth

The global chickpea flour market growth is accelerating due to its expanding use across bakery products, savory snacks, and plant-based meat alternatives. The ingredient’s functional versatility, such as its emulsifying, binding, and water-holding properties, supports its integration into mainstream and specialty food categories. This expansion is significantly enhancing commercial uptake and widening the consumer base. The U.S. brands have expanded chickpea-flour mixes in their gluten-free bakery portfolios, driving mainstream retail penetration.

- For instance, in July 2025, Mission Foods, an American manufacturer of tortillas and tortilla-related products, expanded its “Better for You” range with the launch of Mission Gluten-Free Chickpea Tortillas made from roasted chickpea flour, positioned as a high-fiber, vegan-friendly alternative to conventional wheat tortillas.

Market Restraints

Price Volatility and Raw Material Dependence to Impede Market Expansion

The global chickpea production is highly sensitive to climatic variations, monsoons, and regional agricultural policies. Yield fluctuations in major producers such as India and Australia create supply inconsistencies, affecting flour pricing. Additionally, high processing costs relative to wheat and soy-based flours restrain product adoption among price-sensitive food businesses.

- According to the Ministry of Agriculture and Farmers Welfare, chickpea production is anticipated to be 11.337 MMT (million metric tonnes), representing a drop of 198 KMT (thousand metric tonnes) compared to the second advance estimates published in 2025.

Market Opportunities

Expansion into Premium Pet Food and Aquafeed to Unlock New Growth Opportunities

Chickpea flour serves as a nutritious, non-allergenic protein and fiber source in premium dog and cat foods, enhancing digestibility, muscle development, and gut health benefits while supporting grain-free trends. Its inclusion in 11.5% of dry dog food recipes and growing use in kibble by brands such as Nestlé Purina reflect consumer preferences for natural, sustainable ingredients, with pulses such as chickpeas dominating pet nutrition due to lower allergy risks and versatility. This segment expands market reach in North America and Europe, where premium formulations prioritize clean-label profiles.

- For instance, in October 2025, The Pack, a pioneer in plant-based pet food and now a subsidiary of Prefera Pet Food, partnered with German biotech firm MicroHarvest to launch Gut Bites, the U.K.'s first microbial protein-based vegan dog treats. Key ingredients include milled broad beans, vegetable glycerine, chickpea flour, ground sweet potato, and fruits such as strawberry, apple, carrot, raspberry, and banana, and others.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product Type

Wide Applicability across Food Categories to Propel the Beige Chickpea Flour Segment’s Dominance

By product type, the market segments include dark brown chickpea flour, beige chickpea flour, lentil flour, and others.

The beige chickpea flour segment held a dominant market share in 2025 at USD 1,895.03 million, driven by its wide applicability in bakery, snacks, gluten-free, and plant-based alternatives mixes, and RTE foods. Its functional benefits, such as mild taste, fine texture, and formulation flexibility, support the highest CAGR of 7.53% over 2026 to 2034.

The lentil flour segment is expected to grow significantly with a CAGR of 7.13% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Rising Role in Bakery and Snack Innovation to Lead Food & Beverages Segment Growth

On the basis of application, the market is segmented into food & beverages, animal feed, and others.

The food & beverages segment dominated the global chickpea flour market share with USD 3,098.63 million in 2025, driven by continuous growth in bakery, clean-label foods, meat alternatives, and snack innovations. The segment is poised to grow at a CAGR of 7.18% over the forecast period, reflecting the steady mainstream integration of the flour in gluten-free and plant-based product categories.

The animal feed segment is expected to grow significantly at a CAGR of 10.06% during the forecast period.

By Nature

Affordability and Extensive Industrial Use to Fuel Conventional Segment’s Leadership

On the basis of nature, the market is segmented into conventional and organic.

The conventional segment dominated in 2025 with a valuation of USD 2,364.86 million, driven by large-scale production, price competitiveness, and extensive industrial use. The segment is set to surge at a CAGR of 7.04% over the analysis period, driven by the rising global market demand across foodservice, retail, and B2B ingredients sectors.

The organic segment is anticipated to grow at a CAGR of 7.80% during the forecast period.

By Distribution Channel

Wholesale and Foodservice Pull Fuels Offline Segment Market Leadership

On the basis of distribution channel, the market is segmented into online and offline.

The offline segment dominated with a value of USD 2,475.45 million in 2025, driven by supermarket chains, specialty stores, and wholesale distribution. The segment is likely to grow at a CAGR of 7.10% over the analysis period, supported by the rising availability of gluten-free and plant-based flours in mainstream retail. Wholesale and B2B distributors play a critical role in moving chickpea flour in bulk to industrial food users such as bakeries, snack manufacturers, and HoReCa operators. These buyers still rely heavily on established offline networks for ingredient procurement. This offline B2B ecosystem underpins the continued dominance of the offline channel in overall product distribution, despite rapid growth in online and e-commerce.

The online segment is anticipated to grow at a CAGR of 7.72% during the forecast period.

Chickpea Flour Market Regional Outlook

Regionally, the report covers the market analysis across North America, Europe, Asia Pacific, South America, and the Middle East and Africa.

Asia Pacific

Asia Pacific Chickpea Flour Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific leads the market with strong production clusters in India, Pakistan, Myanmar, and Australia. The region grows from USD 2,160.35 million in 2026 to USD 3,758.13 million in 2034 at a 7.17% CAGR over the forecast period. The regional growth is driven by abundant chickpea cultivation, expanding milling capacity, and rising clean-label food consumption.

India

India leads as the top producer, contributing 64.59% of the regional share in 2025, supported by countries such as Australia, Pakistan, and Myanmar. This regional strength stems from favorable cultivation conditions and established supply chains.

Europe

Europe expands from USD 346.44 million in 2026 to USD 629.15 million in 2034 at a 7.74% CAGR over the analysis period. The demand for chickpea flour is supported by bakery innovation, specialty diets, and strict clean-label standards. The growing awareness of lifestyle‑related diseases and the demand for weight‑management and satiety‑enhancing foods support the adoption of pulse flours, including chickpea flour, across mainstream retail in Western Europe.

North America

North America is anticipated to depict the highest CAGR of 8.25% over the forecast period, growing from USD 282.63 million in 2026 to USD 532.77 million in 2034. The regional expansion is driven by gluten-free diets, vegan formulations, and alternative protein products. Moreover, the rising incidence of celiac disease, wheat intolerance, and broader “free‑from” preferences support sustained demand for gluten‑free flours, including chickpea flour, within the broader gluten‑free flour market that itself is growing at double‑digit rates in North America.

U.S.

The rising demand for plant-based, gluten-free, and protein-rich foods fuels U.S. market growth, driven by health-conscious consumers adopting vegetarian, vegan, and allergen-free diets. Moreover, expanded distribution through supermarkets, e-commerce, and foodservice enhances accessibility, alongside its use in bakery, snacks, and clean-label products.

South America

South America is anticipated to grow at a CAGR of 6.41% over the forecast period, expanding from USD 134.62 million in 2026 to USD 221.31 million in 2034. The regional growth is tied to increasing RTE snacks consumption and rising plant-based diets. In Brazil and Argentina, the growing interest in plant-based and healthy foods drives consumption, supported by agricultural advancements and trade dynamics enhancing chickpea availability. The food service sector's integration of chickpea flour into diverse menus further accelerates growth amid rising vegan and vegetarian trends.

Middle East & Africa

The Middle East and Africa market is poised to expand from USD 424.07 million in 2026 to USD 712.57 million in 2034 at a 6.70% CAGR over the forecast period. The regional expansion is supported by growing bakery applications and emerging health-conscious consumer segments.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Emphasize Functional Ingredient Innovation to Strengthen Market Positions

The global market is moderately fragmented, comprising global ingredient manufacturers and regional mills. The competition is shaped by production capacity, sourcing integration, milling efficiency, product consistency, and the ability to meet clean-label requirements. Companies are also focusing on functional ingredient innovation, developing flours with superior nutritional profiles and application-specific properties for baking, snacks, and plant-based foods. In addition, strategic initiatives aimed at geographical expansion in emerging markets allows firms to leverage local chickpea supply while meeting regional demand.

Key Players in the Chickpea Flour Market

|

Rank |

Company Name |

|

1 |

Ingredion Incorporated |

|

2 |

Archer Daniels Midland Company (ADM) |

|

3 |

The Scoular Company |

|

4 |

AGT Food and Ingredients |

|

5 |

Batory Foods |

List of Key Chickpea Flour Companies Profiled

- Ingredion Incorporated (S.)

- Archer Daniels Midland (U.S.)

- AGT Food and Ingredients (Canada)

- The Scoular Company (U.S.)

- Batory Foods (U.S.)

- Anchor Ingredients (U.S.)

- Nutriati Inc. (U.S.)

- Bob’s Red Mill (U.S.)

- Ardent Mills (U.S.)

- King Arthur Baking Company (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2024: PepsiCo completed its USD 1.2 billion acquisition of Mexican‑American better‑for‑you brand Siete Foods, adding grain‑free products such as chickpea flour tortillas to its snacking and meal portfolio.

- October 2024: Nestlé’s “culinary innovations focused on protein” initiative included a notable India launch where chickpea flour (besan) is used as the base for new high‑protein MAGGI noodles, alongside other regional protein-focused launches such as Vital Pursuit frozen meals in the U.S. and affordable plant-based solutions in Latin America and Africa.

- September 2024: Grain Processing Corporation (GPC) acquired a specialty flour manufacturing and warehouse facility in Oskaloosa, Iowa, expanding its plant-based ingredient and milling footprint. The asset is a 64,000 sq ft flour production and seed-cleaning facility situated on 35 acres in Oskaloosa, Iowa.

- March 2024: Supplant Foods, an India-based food company, secured a patent for a proprietary chickpea processing method that enhances protein functionality in chickpea flour using precision techniques, allowing it to mimic egg proteins in baked goods. The process “tunes” the chickpea flour so that its proteins exhibit improved foaming, emulsifying, and gelling behavior closer to egg and dairy proteins while remaining cost-competitive for emerging markets such as India and China.

- May 2022: Tate & Lyle acquired substantially all of the assets of Nutriati, a U.S.-based ingredient technology company, focused on chickpea protein and flour, strengthening its position in plant-based proteins.

REPORT COVERAGE

The global industry report analyzes the market in depth and highlights crucial aspects such as global market trends, market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the report also provides insights into the global market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.23% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Product Type

|

|

By Application · Food & Beverages o Bakery & Confectionery o Beverages o Meat Alternatives o RTE Products o Others · Animal Feed · Others |

|

|

By Nature

|

|

|

By Distribution Channel · Online · Offline |

|

|

By Region · North America (By Product Type, Application, Nature, Distribution Channel, and Country) • U.S. (By Distribution Channel) • Canada (By Distribution Channel) • Mexico (By Distribution Channel) · Europe (By Product Type, Application, Nature, Distribution Channel, and Country) • Germany (By Distribution Channel) • Spain (By Distribution Channel) • Italy (By Distribution Channel) • France (By Distribution Channel) • U.K. (By Distribution Channel) • Rest of Europe (By Distribution Channel) · Asia Pacific (By Product Type, Application, Nature, Distribution Channel, and Country) • China (By Distribution Channel) • Japan (By Distribution Channel) • India (By Distribution Channel) • Australia (By Distribution Channel) • Rest of Asia Pacific (By Distribution Channel) · South America (By Product Type, Application, Nature, Distribution Channel, and Country) • Brazil (By Distribution Channel) • Argentina (By Distribution Channel) • Rest of South America (By Distribution Channel) · Middle East & Africa (By Product Type, Application, Nature, Distribution Channel, and Country) • South Africa (By Distribution Channel) • UAE (By Distribution Channel) • Rest of the Middle East & Africa (By Distribution Channel) |

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 3,157.25 million in 2025 and is anticipated to reach USD 5,853.94 million by 2034.

The global market will exhibit steady growth at a CAGR of 7.23% over the forecast period.

By product type, the beige chickpea flour segment led the market in 2025.

Asia Pacific holds the largest market share.

Expanding applications in bakery, snacks, and meat alternatives is a key factor driving the market growth.

Ingredion Incorporated, Archer Daniels Midland Company (ADM), The Scoular Company, AGT Food and Ingredients, and Batory Foods are the leading companies in the market.

The rapid expansion of tapioca pearls and chickpea flour-based beverages is a key industry trend.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 31st Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us