Chromatography Instruments Market Size, Share & Industry Analysis, By Type (Liquid Chromatography {High-Performance Liquid Chromatography, Ultra High-Performance Liquid Chromatography, and Others}, Gas Chromatography, Thin-Layer Chromatography, Biochromatography / FPLC Systems, Ion Chromatography, and Others), By Component (Autosampler, Detectors, Pumps, Fraction Collector, and Others), By End User (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, CROs & CDMOs, and Others), and Regional Forecast, 2026-2034

Chromatography Instrumentation Market Future Outlook

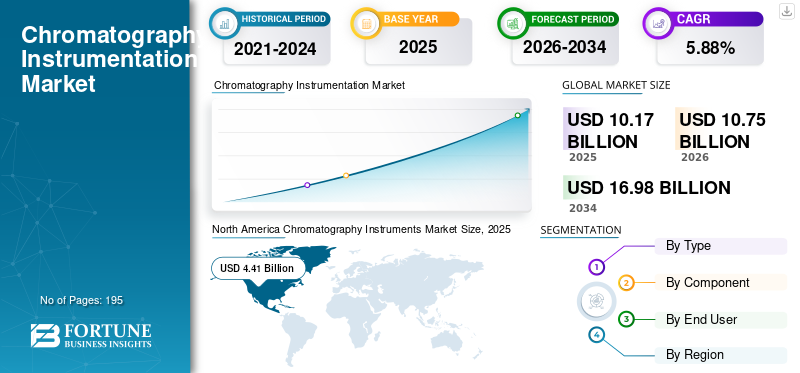

The global chromatography instruments market size was valued at USD 10.17 billion in 2025. The market is projected to grow from USD 10.75 billion in 2026 to USD 16.98 billion by 2034, exhibiting a CAGR of 5.88% during the forecast period. North America dominated the global market with a share of 43.36% in 2025.

The chromatography instruments are laboratory systems that are used for separation, identification, and measurement of the components in a mixture such as drugs, proteins, and others. These instruments work by passing a sample through a stationary phase using a mobile phase, so different compounds move at different speeds and get separated. This industry is primarily driven by increasing demand for chromatography instruments in drug discovery & development procedures.

The market encompasses various key industry players, such as Thermo Fisher Scientific Inc. Agilent Technologies, Inc., and others. These companies focus on innovative product development to maintain their market presence.

Download Free sample to learn more about this report.

CHROMATOGRAPHY INSTRUMENTS MARKET Key Takeaways

- 2025 Market Size: USD 10.17 Billion

- 2026 Market Size: USD 10.75 Billion

- 2034 Forecast Market Size: USD 16.98 Billion

- CAGR: 5.88% from 2026–2034

- North America dominated the chromatography instruments market with a 43.36% share, generating USD 4.41 billion in 2025.

- The detectors segment is projected to hold a 37.1% market share in 2026.

- The pharmaceutical and biotechnology companies segment is expected to account for 53.6% of the market in 2026.

North America

North America generated USD 4.41 billion in 2025 and is projected to maintain its leadership position.

Europe

Europe is expected to reach USD 2.79 billion in 2026, supported by increasing R&D activities.

Asia Pacific

Asia Pacific is projected to attain USD 2.12 billion in 2026, driven by the expansion of CROs, CDMOs, and manufacturing facilities.

U.S.

The chromatography instruments market is projected to reach USD 4.43 billion in 2026.

Japan

The chromatography instruments market is estimated to reach USD 0.39 billion in 2026.

Read More

CHROMATOGRAPHY INSTRUMENTS MARKET TRENDS

Faster Shift toward UHPLC is a Prominent Trend Observed in Market

In recent years, the market is seeing a faster shift from conventional HPLC to UHPLC. This is due to laboratories prioritizing higher throughput, sharper resolution, and shorter run times to cope with rising sample volumes in pharmaceutical quality control, bioprocess analytics, and bioanalysis. Furthermore, UHPLC adoption is also being accelerated by automation-ready architectures such as valve switching, online cleanup, and smarter scheduling that reduce manual steps and improve repeatability in regulated workflows. These factors are supporting the overall global chromatography instruments market growth.

- For instance, in March 2024, Shimadzu Corporation announced the launch of the Nexera FV UHPLC for online analysis.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Pharma/Biopharma R&D and QC Volumes is Propelling Market Growth

Rising pharma/biopharma R&D and QC volumes is a core market driver as every new drug program increases demand for validated separation methods to confirm identity, purity, impurities, stability, and batch consistency across development and commercialization. As pipelines expand, labs run more release testing, comparability, and method transfer, which pushes higher utilization and replacement cycles for LC/GC/IC systems. Moreover, this demand is amplified by the need to reduce turnaround times, in turn driving adoption of higher-throughput UHPLC and more automation in routine QC environments. All these factors cumulatively drive the overall market growth.

- For instance, various companies including Thermo Fisher Scientific Inc. Agilent Technologies, Inc., Waters Corporation, and others have witnessed a strong revenue growth in their products.

MARKET RESTRAINTS

High Cost of Advanced Instruments to Limit Market Growth

High cost of advanced instruments is a key restraint in the chromatography instruments market. LC/GC/IC platforms along with high-end detectors and automation modules require large, upfront budgets that many labs can’t approve quickly. This is especially limiting for academia and government-funded institutes, where instrument procurement depends on grant timing and can fluctuate sharply year to year. This results in limiting the market growth to certain extent.

- For instance, according to an article published in by Excedr in March 2025, the cost of a basic HPLC system starts around USD 10,000.

MARKET OPPORTUNITIES

Cloud-connected Chromatography and Remote Monitoring for Multi-Site Standardization to Offer Market Growth Opportunities

Cloud-connected chromatography and remote monitoring is a major growth opportunity in this market. The pharmaceutical and biopharmaceutical laboratories are increasingly using multi-site operations and need standardized methods, centralized visibility, and consistent compliance across locations. Additionally, remote monitoring enables higher instrument uptime by helping teams spot failures early, prioritize maintenance, and reduce unplanned downtime, directly improving lab productivity and cost control. Moreover, cloud-based analytics also supports audit readiness and data integrity, which is critical in regulated environments where manual data collation can delay batch release and investigations. All these factors would drive the market growth in the coming years.

- For instance, in November 2024, Waters Corporations announced waters connect Data Intelligence, a cloud-based application that leverages Empower CDS data to deliver remote data access, analytics, and audit-readiness dashboards for regulated labs.

MARKET CHALLENGES

Shortage of Skilled Personnel Pose a Critical Challenge to Market Growth

The shortage of skilled chromatography analysts is a major market challenge as advanced LC/GC/IC systems require operators who can develop methods, troubleshoot peak issues, maintain instruments, and ensure data integrity. In addition, limited expertise also reduces adoption speed for higher-end platforms such as UHPLC automation, multi-detector setups as teams hesitate to migrate validated methods without confident internal capability. All the factors cumulatively affect the market growth.

- For instance, according to an article published in August 2025, analytical labs are still struggling with retention and that fewer technicians are specializing in separation science.

Segmentation Analysis

By Type

Rising Usage of Liquid Chromatography to Propel Segmental Growth

Based on type, the market is divided into liquid chromatography, gas chromatography, thin layer chromatography, biochromatography / FPLC systems, ion chromatography, and others.

The liquid chromatography segment is likely to capture the largest global chromatography instruments market share. It is the most versatile platform, able to analyze a wide range of non-volatile, polar, and thermally labile compounds that are common in life science samples. Additionally, LC is deeply embedded in pharma/biopharma R&D and QC, where it is used for purity/impurity profiling, stability studies, potency assays, and method validation driving high installed base and repeat purchases.

- For instance, in October 2024, Agilent Technologies announced the launch of the Agilent Infinity III LC Series (next-generation HPLC systems), highlighting continued major investment and product refresh cycles in liquid chromatography platforms.

The biochromatography / FPLC systems segment is anticipated to rise with a CAGR of 10.27% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Importance of Detectors in Every Application Boosted Segmental Growth

On the basis of component, the market is divided into autosampler, detectors, pumps, fraction collector, and others.

The detectors segment dominated the global market in 2025. Detectors are the primary value-driving module that determines sensitivity, selectivity, and quantitation performance. Unlike pumps or autosamplers, detectors are frequently upgraded or added as labs expand methods, in turn driving the demand. The companies are also focusing on launching new products to gain market share. Furthermore, the segment is set to hold 37.1% share in 2026.

- For instance, in June 2025, Thermo Fisher Scientific introduced the next-generation Thermo Scientific Vanquish Charged Aerosol Detector (CAD) P Series.

The fraction collector segment is anticipated to rise with a CAGR of 10.23% over the forecast period.

By End User

Higher Demand from Academic & Research Institutes Supported their Leading Position

Based on end user, the market is segmented pharmaceutical and biotechnology companies, academic & research institutes, CROs & CDMOs, and others.

The pharmaceutical and biotechnology companies segment captured the leading share in the 2025 global market. They run the highest volumes of regulated analytical testing across the drug lifecycle including discovery, development, validation, commercial QC and batch release. Furthermore, the segment is set to hold 53.6% share in 2026.

In addition, CROs & CDMOs segment is projected to grow at a CAGR of 8.47% during the study period.

Chromatography Instruments Market Regional Outlook

By geography, the market is divided into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Chromatography Instruments Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America market size was USD 4.18 billion in 2024 and captured the dominating position. The region also maintained its dominance in 2025, with USD 4.41 billion. Increasing investments in drug development, strong presence of industry leaders, and active involvement of research community are some of the factors driving the North American market.

U.S. Chromatography Instruments Market

The U.S. market dominated the North American market and is set to attain a value of around USD 4.43 billion in 2026, accounting for roughly 41.3% of global market.

Europe

Europe’s market size is projected to witness a CAGR of 5.66% in the coming years. The region is anticipated to become the second highest among all regions. The region would reach a market size of USD 2.79 billion by 2026. Europe benefits from factors such as increasing research & development, strategic initiatives by operating players, which drives the market growth.

U.K. Chromatography Instruments Market

The U.K. market in 2026 is estimated at around USD 0.62 billion, representing roughly 5.8% of global revenues.

Germany Chromatography Instruments Market

The Germany’s market size is projected to reach approximately USD 0.57 billion in 2026, equivalent to around 5.3% of global sales.

Asia Pacific

Asia Pacific’s market size is projected to be valued at USD 2.12 billion in 2026 and secure the position of the third-largest region in the global industry. The regional market growth is driven by increasing number of CROs & CDMOs in Asian region, and expansion of manufacturing capacities by operating players.

Japan Chromatography Instruments Market

The Japan’s market in 2026 is estimated at around USD 0.39 billion, accounting for roughly 3.6% of global revenues.

China Chromatography Instruments Market

China’s market is projected to reach revenues of around USD 0.64 billion in 2026, representing roughly 5.9% of global sales.

India Chromatography Instruments Market

The Indian market in 2026 is estimated at around USD 0.38 billion, accounting for roughly 3.5% of global revenues.

Latin America and Middle East & Africa

The Latin America and the Middle East and Africa regions are anticipated to witness a slower growth rate in the coming years. The Latin America’s market size is set to reach a valuation of USD 0.62 billion in 2026. The improvements in laboratory capabilities and research funding are anticipated to drive the market growth.

GCC Chromatography Instruments Market

The GCC market in 2026 is estimated to be valued at around USD 0.23 billion, accounting for roughly 2.2% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Emphasis on Technological Advancements by Leading Players to Strengthen Market Share

The global chromatography instruments market is moderately consolidated. It comprises of a small number of large, diversified analytical-instrument manufacturers leading in LC and GC platforms. Prominent players including Thermo Fisher Scientific Inc., Agilent technologies, Inc., Waters Corporation, and others are anticipated to account for the major share of the global market. Factors such as strong global presence, wide distribution network, and broad portfolio with advanced products have supported the dominance of these companies.

- For instance, in April 2025, Waters Corporation announced the expansion of its Alliance iS Bio HPLC product line with integrated photodiode array (PDA) detection.

Other key companies in the market include PerkinElmer, Bio-Rad Laboratories, Inc., and others. Product enhancements, collaborations & partnerships are some of the strategies undertaken by these players to gain market share.

LIST OF KEY CHROMATOGRAPHY INSTRUMENTS COMPANIES PROFILED IN REPORT

- Thermo Fisher Scientific Inc. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Waters Corporation (U.S.)

- Shimadzu Corporation (Japan)

- PerkinElmer (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Metrohm AG (Switzerland)

- Hitachi, Ltd. (Japan)

- Gilson Incorporated (U.S.)

- SCION Instruments (The Netherlands)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Shimadzu Corporation announced release of i-Series integrated HPLC models (LC-2070/LC-2080) featuring automatic instrument-status diagnosis to improve reliability and operational efficiency.

- May 2025: Waters Corporation announced Empower software updates to support biologics data acquisition, including integration of Wyatt MALS and RI detectors for QC and compliance workflows.

- May 2025: Gilson Incorporated released a redesigned VERITY 1741 UV-VIS Detector for semi-preparative & preparative HPLC purification applications.

- May 2025: Agilent Technologies, Inc. launched InfinityLab Pro iQ Series (LC–mass detection), positioned for pharma/biopharma analytical needs

- April 2025: Biotage launched Isolera LS 150, an automated flash chromatography system aimed at purification scale-up and production workflows.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.88% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, Component, End User, and Region |

|

By Type |

· Liquid Chromatography o High-Performance Liquid Chromatography o Ultra High-Performance Liquid Chromatography o Others · Gas Chromatography · Thin-Layer Chromatography · Biochromatography / FPLC Systems · Ion Chromatography · Others |

|

By Component |

· Autosampler · Detectors · Pumps · Fraction Collector · Others |

|

By End User |

· Pharmaceutical & Biotechnology Companies · Academic & Research Institutes · CROs & CDMOs · Others |

|

By Region |

· North America (By Type, Component, End User, and Country) o U.S. o Canada · Europe (By Type, Component, End User, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Type, Component, End User, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Type, Component, End User, and Country/Sub-region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Type, Component, End User, and Country/Sub-region) o GCC o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 10.17 billion in 2025 and is projected to reach USD 16.98 billion by 2034.

In 2025, the market value stood at USD 4.41 billion.

The market is expected to exhibit a CAGR of 5.88% during the forecast period of 2026-2034.

By type, the liquid chromatography segment is expected to lead the market.

Technological advancements in products is primarily driving market expansion.

Thermo Fisher Scientific Inc., Agilent Technologies, Inc., Waters Corporation, and Shimadzu Corporation are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 195

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us