Circular Packaging Market Size, Share & Industry Analysis, By Material (Paper & Paperboard, Plastic, Metal, Glass, and Others), By Packaging Type (Bottles & Jars, Boxes & Cartons, Bags & Pouches, Films & Wraps, Cans, Trays & Clamshells, and Others), By End-use Industry (Food & Beverages, Healthcare, Personal Care & Cosmetics, Household, E-commerce & Retail, Agriculture, Chemicals, and Others), and Regional Forecast, 2026–2034

(Offer valid till 15th Aug 2026)

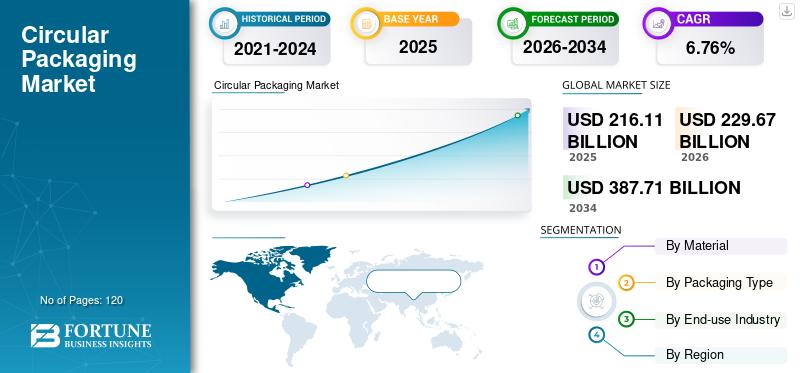

KEY MARKET INSIGHTS

The global circular packaging market size was valued at USD 216.11 billion in 2025. The market is projected to grow from USD 229.67 billion in 2026 to USD 387.71 billion by 2034, exhibiting a CAGR of 6.76% during the forecast period. North America dominated the global circular packaging market with a market share of 33.48% in 2025.

Circular packaging pertains to packaging systems designed to reduce plastic waste and resource consumption by being reusable, recyclable, or compostable. These solutions allow materials to remain in circulation for extended periods through reuse models or closed loop recycling systems, rather than being discarded after a single use.

Global companies are increasingly committing to ambitious sustainability objectives, which include 100% recyclable, compostable or reusable packaging, and increased utilization of post-consumer recycled (PCR) materials. Circular packaging aligns closely with ESG objectives, packaging strategies for carbon-reduction strategies, and brand reputation management, positioning it as a strategic priority rather than merely a compliance-driven effort. Rising consumer demand for packaging that can be easily recycled or reused continues to support market growth.

Key industry players, such as Amcor plc, Tetra Pak, and Smurfit Kappa, are focusing on developing innovative products to accelerate adoption.

Download Free sample to learn more about this report.

CIRCULAR PACKAGING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 216.11 billion

- 2026 Market Size: USD 229.67 billion

- 2034 Forecast Market Size: USD 387.71 billion

- CAGR: 6.76% from 2026–2034

- North America dominated the circular packaging market with a 33.48% share in 2025.

- Paper & paperboard held the largest material segment share in 2025.

- Bottles & jars dominated the packaging type segment in 2025.

North America

North America remained the leading regional market in 2025, supported by strong sustainability commitments from corporations, retailers, and e-commerce companies.

Europe

Europe accounted for USD 56.60 billion in 2025 and is projected to grow at a CAGR of 6.51%, driven by stringent circular economy regulations and EPR frameworks.

Asia Pacific

Asia Pacific reached USD 44.58 billion in 2025, supported by rapid urbanization, growing packaged goods consumption, and government waste reduction initiatives.

U.S.

The market was valued at approximately USD 56.55 billion in 2025, driven by retailer sustainability scorecards, ESG expectations, and state-level environmental regulations.

Japan

The market reached around USD 5.54 billion in 2025, benefiting from advanced waste sorting systems, material efficiency practices, and strong consumer participation in recycling programs.

Read More

CIRCULAR PACKAGING MARKET TRENDS

Integration of Digital and Smart Packaging for Circularity is a Prominent Trend Observed in the Market

The combination of digital and smart packaging technologies is becoming a vital enabler of circularity within the global packaging industry by enhancing traceability, recycling efficiency, and consumer engagement. Technologies such as QR codes, digital watermarks, RFID tags, and near-field communication (NFC) enable packaging to convey comprehensive information regarding material composition, recycling guidelines, and lifecycle impacts. This advancement enhances sorting precision at material recovery facilities, supporting design-for-recycling goals and resulting in increased material recovery rates and improved quality of recycled feedstock.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Environmental Regulations and Extended Producer Responsibility (EPR) to Drive Market Growth

Governments across Europe, North America, and certain regions of Asia are implementing stringent regulations aimed at minimizing packaging waste. These include prohibitions on single use plastics, requirements for recycled content, and Extended Producer Responsibility (EPR) initiatives. Such policies compel manufacturers and brand owners to reimagine packaging for recyclability, reuse, and material recovery, directly promoting the adoption of circular packaging solutions in sectors such as food and beverages, personal care, and retail. Henceforth, increasing demand for sustainable packaging solutions, growing stringency of environmental impact, regulations and the extension of producer responsibility (EPR) are key factors driving the global circular packaging market growth.

MARKET RESTRAINTS

High Cost of Circular Materials and Infrastructure Obstructs Market Growth

Circular packaging materials, including PCR plastics, mono-material flexible packaging, and bio-based alternatives, frequently incur higher expenses compared to virgin biodegradable materials. This is attributed to factors such as limited supply, processing complexities, and quality limitations. Furthermore, the capital-intensive nature of investments in recycling, sorting, and reverse logistics infrastructure continues to hinder adoption by small and mid-sized manufacturers. Thus, the high cost of circular raw materials and supporting infrastructure continues to hampers market growth.

MARKET OPPORTUNITIES

Innovation in Recyclable, Reusable, and Compostable Materials Offers Market Growth Opportunities

Advancements in materials science, including high-quality PCR resins, mono-material laminates, fiber-based alternatives, and compostable polymers, are expanding the new possibilities for the adoption of the product. These advancements allow brands to achieve sustainability goals while maintaining functionality, thereby unlocking considerable growth potential in both flexible and rigid packaging sectors. As digital tracking, smart labeling, and logistics technologies continue to evolve, reuse-oriented circular packaging models are increasingly becoming economically feasible, generating new revenue streams and opportunities for long-term customer engagement.

MARKET CHALLENGES

Scaling Circular Packaging Without Compromising Economics Poses a Critical Challenge to Market Growth

Although pilot projects and specialized applications are on the rise, the widespread implementation of the product in mass-market products continues to face difficulties due to cost constraints, the intricacies of supply chains, and the irregular supply of recycled materials. Striking a balance between achieving economies of scale and ensuring profitability presents a significant challenge for manufacturers and brand owners. Therefore, scaling circular packaging without compromising economics poses a critical challenge to market growth.

Segmentation Analysis

By Material

Recyclability, Regulation, and Consumer Trust to Drive Paper & Paperboard Segment Growth

Based on material, the market is divided into paper & paperboard, plastic, metal, glass, and others.

The paper & paperboard segment is expected to account for the largest share of the market. The segment leads the market primarily due to its excellent recyclability, established collection infrastructure, and robust regulatory acceptance. The high rates of recycling and compatibility with current waste management systems render paper & paperboard a low-risk, scalable option for brands moving toward circular packaging.

The plastic segment is expected to grow at a CAGR of 6.89% over the forecast period.

By Packaging Type

Bottles & Jars Segment Led the Market due to their Natural Compatibility

Based on packaging type, the market is segmented into boxes & cartons, bottles & jars, sleeves & slipcases, inserts & dividers, tubes, and others.

In 2025, the bottles & jars segment dominated the global market. The segment of bottles and jars leads the global market due to their natural compatibility with circularity, facilitated by reuse, recyclability, and closed-loop recovery systems. Rigid containers, including bottles and jars, are simpler to collect, sort, and reprocess than more complex flexible packaging options. Their uniform shapes and clear materials contribute to enhanced recycling efficiency and a consistent quality of recycled materials, thereby promoting large-scale circular models.

The boxes & cartons segment is projected to grow at a CAGR of 7.12% over the forecast period.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Food & Beverages Segment to Dominate owing to Substantial Packaging Consumption

Based on end-use industry, the market is segmented into food & beverages, healthcare, personal care & cosmetics, household, e-commerce & retail, agriculture, chemicals, and others.

The food & beverages segment is expected to hold a dominant market share over the forecast period. The food & beverages segment leads the global market owing to its substantial packaging consumption and everyday usage. Packaging is essential at each phase of production, distribution, and consumption, resulting in considerably greater material utilization compared to other end-use industries. This high volume intensity positions the sector as a key target for circular packaging initiatives, as even slight packaging design enhancements can yield significant environmental benefits. Prominent international brands have committed to ensuring that their packaging is entirely recyclable, reusable, or compostable, while also enhancing the incorporation of recycled materials and refill systems, thus driving the segment’s growth.

The healthcare segment is projected to grow at a CAGR of 7.31% over the forecast period.

Circular Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America held the dominant circular packaging market share in 2024, valued at USD 67.90 billion, and maintained its leading position in 2025, with a value of USD 72.35 billion. In the region, the adoption of the product is primarily driven by robust sustainability commitments from multinational corporations and growing pressure from major retailers and e-commerce platforms.

U.S Circular Packaging Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 56.55 billion in 2025, accounting for roughly 26.17% of global circular packaging sales. In the U.S., the market is influenced by sustainability scorecards from retailers, expectations for environmental, social, and governance (ESG) practices led by investors, and state-level legislation, rather than by cohesive federal regulations.

Europe

Europe is projected to record a growth rate of 6.51% in the coming years, the second-highest among all regions, and reached a valuation of USD 56.60 billion in 2025. Europe represents the most regulation-oriented market globally. Stringent policies, including mandatory targets for recycled content, plastic taxes, landfill limitations, and extensive Extended Producer Responsibility (EPR) frameworks, are driving the widespread adoption of these sustainable practices.

U.K Circular Packaging Market

The U.K. market in 2025 reached around USD 10.22 billion, representing approximately 5.56% of global circular packaging revenues.

Germany Circular Packaging Market

Germany’s market reached approximately USD 12.62 billion in 2025, equivalent to around 8.04% of global circular packaging sales.

Asia Pacific

Asia Pacific stood at USD 44.58 billion in 2025 and secure the position of the third-largest region in the market. In the region, India and China are both estimated to reach USD 11.77 billion and USD 15.90 billion, respectively, in 2025. In the Asia Pacific region, the expansion of circular packaging is driven by rapid urbanization, increasing consumption of packaged goods, and a growing emphasis from governments to reduce waste. Cost efficiency, scalability, and lightweight designs are crucial factors as brands pursue circular solutions that facilitate high-volume production while remaining cost-effective.

Japan Circular Packaging Market

The market in Japan reached around USD 5.54 billion, accounting for approximately 2.56% of global circular packaging revenues.

A deep-rooted culture of waste reduction, material efficiency, and precise packaging has influenced Japan's adoption of the product. The country's sophisticated sorting systems and consumer adherence facilitate effective circular models, especially for rigid and mono-material packaging types.

China Circular Packaging Market

China’s market is projected to be one of the largest worldwide, with revenues estimated at around USD 15.90 billion in 2025, representing roughly 7.36% of global circular packaging sales.

India Circular Packaging Market

In India, the market in 2025 stood at USD 11.77 billion, accounting for roughly 5.44% of global circular packaging revenues.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market is set to reach a valuation of USD 24.25 billion in 2025. Evolving waste management regulations and the significant impact of multinational companies active in the region drive the market in the region.

In the Middle East & Africa, South Africa is set to reach a value of USD 5.23 billion in 2025.

Saudi Arabia Circular Packaging Market

In Saudi Arabia, the market is projected to reach approximately USD 7.37 billion in 2025, accounting for roughly 3.41% of global circular packaging revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on New Product Launches to Advance Research Activities

The market is moderately consolidated, with a combination of global packaging giants and regional specialists competing on material innovation, recycling infrastructure, and closed-loop supply partnerships. Leading companies such as Amcor plc, Tetra Pak, Smurfit Kappa, Mondi, Sealed Air, and Ball Corporation are strengthening their positions through new product launches, lightweight and recyclable packaging designs, and investments in circular materials such as recycled plastics, paper-based alternatives, and aluminum. Competition is enhanced by collaborations with recyclers, brand owners, and sustainability organizations to improve collection and sorting, increase recycled content availability, and meet evolving regulatory and customer requirements. Overall, players that can combine scalable manufacturing with measurable circularity outcomes, such as higher recycled content, recyclability, and traceability that are expected to gain an edge during the forecast period.

- For instance, in July 2025, PepsiCo and Tetra Pak partnered with The Circulate Initiative to enhance the working conditions of informal waste workers in India. The Circulate Initiative’s Responsible Sourcing Initiative aims to expedite the adoption of responsible sourcing practices throughout the plastics recycling value chain.

Other notable players in the global market include Mondi, Sealed Air, and Ball Corporation. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY CIRCULAR PACKAGING COMPANIES PROFILED

- Amcor plc (Switzerland)

- Tetra Pak (Switzerland)

- Smurfit Kappa (Ireland)

- Mondi (U.K.)

- Sealed Air (U.S.)

- Ball Corporation (U.S.)

- DS Smith (U.K.)

- Stora Enso (Finland)

- Huhtamaki Oyj (Finland)

- International Paper Company (U.S.)

- Ranpak Holdings Corp. (U.S.)

- Greif, Inc. (U.S.)

- Gerresheimer AG (Germany)

- Ardagh Group S.A. (Luxembourg)

- Trivium Packaging (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Amcor announced its involvement in a three-year plastic recycling initiative led by the Danish Technological Institute aimed at implementing full-scale circular recycling of food packaging made from polyethylene (PE) and polypropylene (PP) rigid plastics sourced from household collections.

- September 2025: Coveris, a leading European manufacturer of paper and plastic packaging, has proudly collaborated on an innovative healthcare circularity initiative. The Full Circle project effectively recycles used medical plastic packaging into new, contact-sensitive packaging.

- May 2025: Mondi and ZARELO have collaborated to launch a recyclable paper-based packaging solution for fire starters utilized in fireplaces and barbecues. This smooth shift to lightweight paper-based packaging demonstrates a robust partnership founded on trust and expertise, further emphasizing both companies' commitment to innovative and circular packaging solutions.

- October 2024: Tetra Pak and Lactalis introduced a carton package that incorporates certified recycled polymers derived from used beverage cartons, representing a pioneering achievement for the beverage carton sector and a crucial advancement towards a circular economy. This material has received certification from ISCC PLUS, confirming its origin from the recycling of used beverage cartons in Spain. It is assigned to the package through a mass balance attribution method.

- June 2022: Stora Enso and Tetra Pak initiated a feasibility study to enhance the recycling of beverage cartons in the Benelux region. This collaborative effort aims to promote circular solutions for paper-based packaging by establishing a new recycling facility.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.76% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material, Packaging Type, End-use Industry, and Region |

|

By Material |

· Paper & Paperboard · Plastic · Metal · Glass · Others |

|

By Packaging Type |

· Bottles & Jars · Boxes & Cartons · Bags & Pouches · Films & Wraps · Cans · Trays & Clamshells · Others |

|

By End-use Industry |

· Food & Beverages · Healthcare · Personal Care & Cosmetics · Household · E-commerce & Retail · Agriculture · Chemicals · Others |

|

By Region |

· North America (By Material, Packaging Type, End-use Industry, and Country) o U.S. o Canada · Europe (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o Germany o U.K. o France o Italy o Spain o Russia o Poland o Romania o Rest of Europe · Asia Pacific (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o Brazil o Mexico o Argentina o Rest of Latin America · Middle East & Africa (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o Saudi Arabia o UAE o Oman o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 216.11 billion in 2025 and is projected to reach USD 387.71 billion by 2034.

In 2025, the market value stood at USD 72.35 billion.

The market is expected to exhibit a CAGR of 6.76% during the forecast period (2026-2034).

By material, the paper & paperboard segment is expected to lead the market.

Stringent environmental regulations and extended producer responsibility (EPR) are the key factors driving market expansion.

Amcor plc, Tetra Pak, Smurfit Kappa, Mondi, Sealed Air, and Ball Corporation are major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us