City Bus Market Size, Share & Industry Analysis, By Type (Single-Decker and Double-Decker), By Size (Mini, Standard and Articulated), By Propulsion (ICE and Electric), By Passenger Capacity (Up to 30 Passengers, 31–80 Passengers, and Above 80 Passengers), By Ownership (Public-Owned and Private-Owned) and Regional Forecasts, 2026-2034

City Bus Market Size

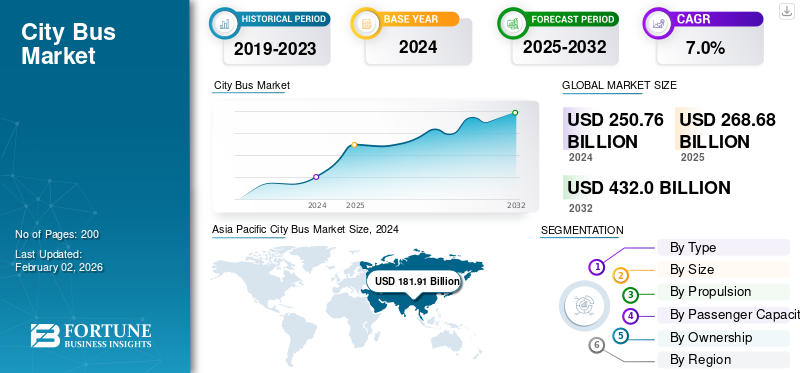

The global city bus market size was valued at USD 268.68 billion in 2025. The market is projected to grow from USD 288.91 billion in 2026 to USD 495.52 billion by 2034, exhibiting a CAGR of 6.98% during the forecast period. Asia Pacific dominated the city bus market with a market share of 72.34% in 2025.

City buses are purpose-built vehicles designed for the efficient transportation of passengers within urban and suburban areas, serving as a vital component of the broader transportation system. Unlike long-distance coaches, they prioritize frequent stops, easy boarding and alighting, and optimized seating and standing capacity to handle dense passenger flows. City buses come in various configurations: mini, standard, articulated, and double-decker, offering flexible options for route density and urban infrastructure. These vehicles are powered by a range of propulsion systems, including internal combustion engines (ICE), hybrid drivetrains, battery-electric systems, and emerging hydrogen fuel-cell technologies, reflecting the sector’s gradual shift toward sustainable and cost-effective mobility.

The primary appeal of city buses lies in their ability to provide affordable, safe, and cost-effective transportation solutions while reducing urban congestion and emissions. They form the backbone of public transit networks, linking residential areas with commercial, educational, and industrial hubs. As cities expand and populations grow, demand for reliable and environmentally friendly bus transport continues to rise. Electric and hybrid city buses offer quieter operation, lower operating costs, and cost-effective performance, along with zero or reduced tailpipe emissions, making them central to municipal climate and air-quality goals. Governments worldwide are promoting their adoption through subsidies, tax incentives, and substantial investments in public transportation infrastructure to support depot and on-route charging.

The global city bus industry is evolving rapidly, driven by electrification, digitalization, and shifting mobility patterns. Modern city buses are increasingly equipped with real-time passenger information systems, enabling commuters to access live updates on routes, arrival times, and service changes, thereby improving travel convenience and overall transit efficiency. The growing integration of Mobility as a Service (MaaS) platforms is further transforming public transport by connecting city buses with other mobility modes such as metro, ride-sharing, and micro-mobility solutions. Partnerships among us bus makers, battery suppliers, and charging infrastructure firms are reshaping traditional production and procurement models. At the same time, many cities are phasing out diesel fleets to comply with stricter emission norms, creating strong replacement demand for zero-emission buses (ZEBs). Growth is also supported by the expansion of Bus Rapid Transit (BRT) networks and smart city initiatives across Asia, Europe, and the Americas.

Leading manufacturers illustrate these trends. BYD and Yutong dominate the electric city bus market, supplying large fleets in China and exporting to Europe and Latin America. Volvo Buses and Mercedes-Benz have introduced fully electric models such as the Volvo 7900 Electric and eCitaro, designed for energy efficiency and passenger comfort. Tata Motors and Ashok Leyland are expanding their electric and CNG city bus lines under India’s FAME and PM-eBus Sewa programs. Alexander Dennis in the UK continues to develop battery and hydrogen double-decker buses for dense urban routes. These examples highlight how the city bus sector is transitioning from traditional diesel fleets to advanced, zero-emission, connected, and sustainable public transportation solutions, which are crucial to the future of urban mobility and next-generation transportation systems.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Urbanization and Government Push for Public Transport Electrification Accelerate the Market Growth

Rapid urbanization and increasing population densities are driving the demand for efficient and sustainable mass transit solutions, thereby fueling city bus market growth. Governments across regions are prioritizing the electrification of public transport to combat pollution and congestion. City buses form the backbone of urban mobility strategies, supported by incentive programs, clean transport missions, and zero-emission targets that encourage widespread deployment of electric and hybrid buses.

- For instance, in August 2024, India’s PM-eBus Sewa scheme approved 10,000 new electric city buses for 169 cities to promote cleaner and more affordable mobility.

MARKET RESTRAINTS

Uneven Access to Financing and Subsidy Programs Across Regions May Limit the Market Growth

The availability of financial incentives and subsidy frameworks varies greatly between developed and developing nations. Municipalities in low-income regions often lack funding to adopt zero-emission fleets, resulting in continued reliance on older diesel models. This disparity hinders global electrification and limits equitable progress toward sustainable public transportation infrastructure.

- For instance, a World Bank 2024 study highlighted that cities in Sub-Saharan Africa face investment gaps exceeding USD 5 billion annually for bus electrification projects.

MARKET OPPORTUNITIES

Growing Adoption of Hydrogen and Battery-Electric Technologies to Create Lucrative Opportunities

Technological advancements in hydrogen fuel-cell and battery-electric systems present new opportunities for long-range, efficient city bus operations. OEMs are investing in modular powertrains, faster charging solutions, and energy-efficient drivetrains to meet the rising demand for zero-emission buses in urban and intercity applications. This transition aligns with cities’ long-term sustainability and emission-reduction goals.

- For instance, in May 2024, Volvo Buses unveiled the BZR Electric platform, which is compatible with both battery-electric and fuel-cell configurations, thereby enhancing operational flexibility for fleet operators.

CITY BUS MARKET TRENDS

Transition Toward Zero-Emission and Connected Bus Fleets is one of the Significant Market Trends

The city bus market is undergoing a major transition toward zero-emission and digitally connected fleets. Telematics integration, predictive maintenance, and real-time route optimization are becoming standard features in the industry. This convergence of clean propulsion and smart connectivity enhances fleet efficiency and supports data-driven urban transport management.

- For instance, in July 2025, Go‑Ahead London deployed a major EV charge-management platform called BetterFleet across over 1,000 electric buses and 20 depots, scaling to 1,500 units at 30 depots by the end of 2025.

MARKET CHALLENGES

Integration of Large-Scale Electric Fleets into Existing Transit Systems is Challenging for the Market

Integrating electric and hybrid buses into legacy transit networks remains a key operational challenge. Upgrading grid capacity, building depot charging infrastructure, and synchronizing schedules to accommodate charging cycles demand significant investment and planning. Effective coordination between transit agencies, utilities, and OEMs is crucial for seamless implementation.

- For example, in June 2025, Transport for London announced that it had achieved a milestone of over 2,000 zero-emission buses on its network but flagged challenges coordinating charging infrastructure and route deployment for the remaining fleet.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Single-Decker Buses Dominate the Market for Urban and Intercity Operations

By type, the city bus is classified into single-decker and double-decker types.

In 2026, Single Decker Buses dominated the segment with a market share of 93.19%. Single-decker buses dominate the market due to their operational flexibility, cost efficiency, and suitability for high-frequency urban and intercity routes. They are easier to maintain and maneuver in congested environments, making them the preferred choice for most public transport operators.

- For instance, Volvo’s 7900 Electric and Yutong’s E12 single-decker models continue to be widely deployed across European and Asian cities, underscoring their dominance in municipal fleet tenders.

By Size

Standard-Size Buses Lead Due to Balanced Capacity and Range

Based on size, the market is divided into mini, standard, and articulated buses.

In 2026, standard-size city buses dominated the segment with a market share of 67.65%, striking an optimal balance between passenger capacity, route efficiency, and operational cost. They are extensively used in both urban and suburban services, offering versatility across city layouts and passenger volumes.

- For example, Solaris Urbino 12 Electric and BYD K9 standard-size buses remain top choices for city fleets in Europe and Asia due to their proven performance and range adaptability.

By Propulsion

To know how our report can help streamline your business, Speak to Analyst

In propulsion terms, the market includes internal combustion engine (ICE), hybrid, and electric buses.

In 2026, Electric buses dominated the segment with a market share of 62.50%. Electric buses dominate the market in terms of revenue due to their higher unit prices and growing adoption under zero-emission mandates. In contrast, ICE buses account for the largest city bus market share in volume as many developing regions continue to use diesel and CNG vehicles. The shift toward electrification is accelerating, driven by government funding and reductions in battery costs.

- For instance, BYD, Volvo, and Mercedes-Benz eCitaro electric models recorded significant global sales growth in 2024, supported by municipal fleet transitions across Europe, China, and India.

By Seating Capacity

31–80 Passenger Segment Dominates Urban Fleet Deployments

By seating capacity, the market is categorized into up to 30, 31–80, and above 80 passengers.

In 2026, 31–80 Passengers dominated the segment with a market share of 68.27%, as standard and articulated buses typically fall within this range, making them ideal for dense urban routes and BRT systems. This capacity range ensures optimal cost-per-kilometer and passenger turnover rates.

- For instance, Ashok Leyland’s Switch EiV 12 and BYD B12 models are designed to seat between 60–75 passengers, aligning with most global city route requirements.

By Ownership

Public-Owned Fleets Dominate Due to Government Electrification Programs

By ownership, the market is categorized into public-owned and private-owned.

Public-owned fleets dominate globally, driven by large-scale government procurements under national clean mobility and electrification missions. These fleets are usually deployed under long-term service contracts or public-private partnership models.

- For example, in 2024, Transport for London (TfL), Delhi Transport Corporation (DTC), and BVG Berlin collectively operated over 35,000 government-owned city buses, the majority of which are transitioning to zero-emission fleets under public sustainability programs.

City Bus Market Regional Outlook

By region, the city bus market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific City Bus Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific generated USD 194.36 Billion, contributing 72.34% to global market revenue, and is projected to grow to USD 209.26 Billion in 2026. The region dominates the global market owing to rapid urbanization, strong government support for public transportation electrification, and extensive domestic manufacturing capabilities. Countries such as China, India, Japan, and South Korea continue to lead the production and adoption of city buses, particularly electric models, supported by large-scale investments in sustainable mobility. The China market is projected to reach USD 167.77 Billion in 2026, while India and Japan are expected to reach USD 10.96 Billion and USD 6.31 Billion, respectively.

Europe

Europe maintained a strong presence in the market, reaching USD 20.16 Billion in 2025, accounting for 7.50% share, and is expected to reach USD 20.96 Billion in 2026. Growth in the region is supported by stringent environmental regulations, government incentives for zero-emission public transportation, and large-scale fleet electrification programs. Investments in advanced battery technologies and charging infrastructure continue to accelerate the adoption of electric city buses. The U.K. and Germany markets are projected to reach USD 2.43 Billion and USD 2.65 Billion in 2026, respectively.

North America

The North America region captured 2.59% of the global market in 2025, generating USD 6.97 Billion in revenue, and is projected to reach USD 7.47 Billion in 2026. The market is driven by ongoing fleet modernization programs, increasing adoption of low-emission transportation solutions, and supportive government initiatives promoting clean public transit. Major cities across the U.S. and Canada are expanding electric bus deployments to reduce emissions and improve urban mobility. The U.S. market is projected to reach USD 4.32 Billion in 2026.

Rest of the World

Rest of the World contributed 17.57% to the global market in 2025, with a valuation of USD 47.20 Billion, and is projected to reach USD 51.22 Billion in 2026. Growth across Latin America, the Middle East, and Africa is supported by investments in Bus Rapid Transit (BRT) networks, increasing urbanization, and the gradual adoption of electric buses. Governments in several countries are focusing on sustainable transportation initiatives and public transit expansion, creating opportunities for market growth while adoption remains at an earlier stage compared to Asia Pacific and Europe.

COMPETITIVE LANDSCAPE

Key Industry Players

Collaborations and Electrification Strategies Redefine Market Leadership

The global city bus market is moderately consolidated, with established OEMs and emerging electric bus specialists competing through technological innovation, partnerships, and sustainable mobility programs. Leading manufacturers are focusing on developing advanced electric and hydrogen-powered buses, expanding smart fleet management solutions, and strengthening aftersales and charging infrastructure support to secure long-term contracts with municipalities and transport operators.

Volvo Buses, BYD Company Ltd., Yutong Bus Co., Ltd., and Mercedes-Benz (Daimler Buses) are among the leading players driving global electrification. Volvo is expanding its electric bus platforms, such as the BZR Electric, offering modular battery and hydrogen options. BYD and Yutong dominate the electric segment, exporting large fleets to Europe, Latin America, and Southeast Asia. Daimler Buses continues to grow with its eCitaro line, combining zero-emission performance with high passenger comfort.

Other notable players include Tata Motors, Ashok Leyland, Alexander Dennis Limited (ADL), and Solaris Bus & Coach. Tata Motors and Ashok Leyland are scaling up local electric bus manufacturing under India’s FAME and PM-eBus Sewa programs. ADL leads in the U.K. double-decker electric segment, while Solaris is expanding across the EU with its Urbino Electric range. These manufacturers maintain competitiveness through R&D investments, localized production, and strong collaborations with battery and charging system providers.

- For instance, in March 2025, BYD announced its European showcase at Busworld Europe 2025, unveiling new solid-state battery-powered city buses and strengthening its exports-to-Europe footprint.

LIST OF KEY CITY BUS COMPANIES PROFILED

- Yutong Bus Co. Ltd. (China)

- BYD Co. Ltd. (China)

- Daimler Buses GmbH (Germany)

- AB Volvo (Sweden)

- Force Motors Ltd. (India)

- Tata Motors (India)

- Ashok Leyland (India)

- Scania AB (Sweden)

- IVECO S.p.A (Italy)

- NFI Group (Canada)

KEY INDUSTRY DEVELOPMENTS

- November 2025: According to Sustainable Bus news, battery-electric bus registrations in Europe (vehicles > 8 t) reached 5,315 units in H1 2025, an approximately 41% increase over the first half of 2024.

- March 2025: A report by Transport & Environment (T&E) found that 49% of all new city buses in the EU in 2024 were zero-emission models, indicating a strong uptake for battery-electric buses.

- February 2025: Volvo Buses announced its first electric bus order with Go‑Ahead in London, comprising 25 Volvo BZL Electric single-deck buses to be deployed in 2025.

- October 2024: UK operator Go‑Ahead Transport Group made a £500 million investment to purchase up to 1,200 zero-emission buses (electric) built by Wrightbus, supporting UK-made manufacturing and decarbonization of its fleet.

- March 2024: Wrightbus secured a contract from Arriva London to deliver 87 new zero-emission buses (11 single-deck and 76 double-deck Electroliner models) for London services.

REPORT COVERAGE

The global city bus market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends that are expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also includes a detailed competitive landscape providing information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.98% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, Propulsion, Drivetrain, Seating Capacity, and Region |

|

By Type |

|

|

By Size |

|

|

By Propulsion |

|

|

By Passenger Capacity |

|

|

By Ownership

|

|

|

By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 268.68 billion in 2025 and is projected to reach USD 495.52 billion by 2034.

In 2025, the market value stood at USD 194.36 billion.

The market is expected to exhibit a CAGR of 6.98% during the forecast period of 2026-2034.

The single-decker segment led the market in terms of city bus type.

Rising urbanization and government efforts to electrify public transport electrification are driving the growth of the city bus market.

Yutong Bus, BYD, Daimler Buses, and AB Volvo are some of the prominent players in the market.

Asia-Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us