Climate Risk Analytics Market Size, Share & Industry Analysis, By Component (Software, Data & Analytics Services, and Professional & Consulting Services), By Risk Type (Physical Risk {Acute and Chronic}, Transition Risk {Policy & regulatory, and Technology transition}, & Liability Risk), By Deployment Mode (Cloud Based & On-Premise), By Organization Size (Small, Medium & Large Enterprises), By End-User (Banking, Financial Services & Insurance, Energy & Utilities, Government & Public Sector, Agriculture, Manufacturing, Transportation & Logistics, and Others) and Regional Forecast, 2026-2034

Climate Risk Analytics Market Size and Future Outlook

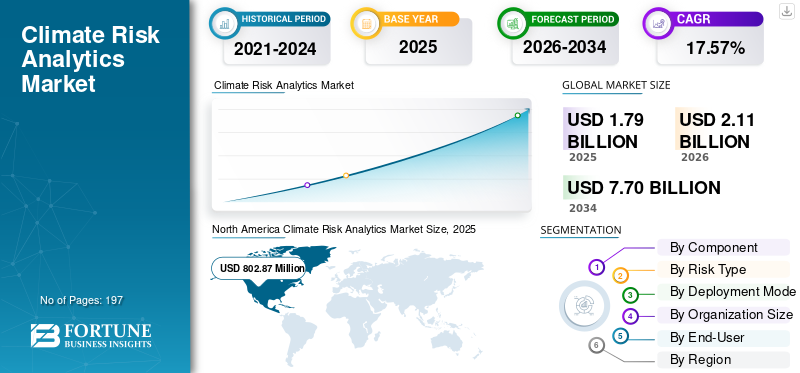

The climate risk analytics market size was valued at USD 1,799.5 million in 2025. The market is projected to grow from USD 2,110.7 million in 2026 to USD 7,706.4 million by 2034, exhibiting a CAGR of 17.57% during the forecast period. North America dominated the climate risk analytics market with a market share of 44.61% in 2025.

Climate risk analytics refers to the use of advanced data models, software platforms, and analytical tools used to identify, assess, and quantify the potential impacts of climate-related risks on assets, operations, and financial performance. These solutions play a critical role in supporting decision-making across financial institutions, governments, and corporations by enabling accurate evaluation of both physical risks, such as extreme weather events and long-term climate changes, and transition risks arising from evolving regulatory, technological, and market dynamics. Climate risk analytics tools are widely used across sectors including banking, energy, infrastructure, and manufacturing to enhance resilience, ensure regulatory compliance, and support long-term strategic planning.

The demand for climate risk analytics is increasing steadily, driven by structural shifts in global regulatory frameworks and growing awareness of climate-related financial exposure. One of the major market drivers is the rising implementation of disclosure standards such as TCFD, ISSB, and regional regulations such as the EU’s CSRD, which require organizations to assess and report climate risks in a structured manner. Additionally, increasing investments in sustainable finance and the integration of ESG considerations into investment strategies are accelerating the adoption of advanced risk analytics tools. The growing frequency and severity of climate events, along with heightened focus on infrastructure resilience and supply chain stability, are further contributing to market growth.

The market is moderately fragmented, comprising a mix of established financial data providers, technology firms, and specialized climate analytics companies. Key players such as MSCI Inc., Moody’s Corporation, S&P Global, Verisk Analytics Inc., and Jupiter Intelligence hold a strong presence, particularly in developed markets with mature financial and regulatory ecosystems. These companies are focusing on technological advancements such as integration of artificial intelligence, high-resolution climate modeling, and real-time data platforms to enhance the accuracy and usability of risk insights. Strategic initiatives including product innovation, partnerships with financial institutions, and expansion into emerging markets are shaping the competitive landscape and supporting the long-term evolution of the market.

Download Free sample to learn more about this report.

CLIMATE RISK ANALYTICS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1,799.5 million

- 2026 Market Size: USD 2,110.7 million

- 2034 Forecast Market Size: USD 7,706.4 million

- CAGR: 17.57% from 2026–2034

- North America dominated the climate risk analytics market with a 44.61% share in 2025.

- The software/platforms segment accounted for a 73.41% market share in 2025.

- The physical risk segment held a 49.73% market share in 2025.

North America

North America generated USD 802.87 million in 2025 and is projected to reach USD 942.17 million in 2026, supported by strong climate disclosure regulations.

Europe

Europe accounted for USD 506.50 million in 2025 and is expected to reach USD 589.48 million in 2026, driven by CSRD compliance and sustainable finance initiatives.

Asia Pacific

Asia Pacific recorded USD 345.64 million in 2025 and is forecast to reach USD 415.18 million in 2026, supported by ESG adoption and climate resilience investments.

U.S.

The market reached USD 699.22 million in 2025, representing nearly 87% of the North American market.

Japan

The market is expanding with rising ESG adoption, climate risk management initiatives, and investments in sustainable infrastructure across the country.

Read More

Climate Risk Analytics Market Trends

Rising Regulatory Pressure and Climate Disclosure Requirements are Major Market Trend

The increasing implementation of climate-related disclosure regulations and reporting frameworks is a major trend driving the growth of the market. Governments and regulatory bodies across the globe are mandating organizations to assess, quantify, and disclose their exposure to climate-related risks, particularly in the financial sector. Frameworks such as the Task Force on Climate-related Financial Disclosures (TCFD), the International Sustainability Standards Board (ISSB), and region-specific regulations such as the European Union’s Corporate Sustainability Reporting Directive (CSRD) are compelling companies to adopt structured and data-driven approaches to climate risk assessment. As a result, organizations are increasingly relying on advanced climate risk analytics platforms to ensure compliance, enhance transparency, and support informed decision-making.

Furthermore, financial institutions including banks, asset managers, and insurers are integrating climate risk into their core risk management and investment strategies. This shift is driving demand for sophisticated tools capable of scenario analysis, stress testing, and portfolio-level risk evaluation under different climate pathways. Climate risk analytics solutions enable organizations to align with regulatory expectations while also identifying potential financial impacts associated with physical and transition risks. For instance, in 2026, major financial regulators including the European Central Bank (ECB), Bank of England (PRA), Federal Reserve, European Banking Authority (EBA), Monetary Authority of Singapore (MAS), and Australian Prudential Regulation Authority (APRA) expanded climate stress testing requirements for banks and insurance companies, prompting widespread adoption of climate risk analytics platforms to support regulatory reporting and risk modeling.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of Cloud-Based Platforms is Propelling Market Growth

The rapid expansion of cloud-based platforms is significantly enhancing the accessibility, scalability, and deployment efficiency of climate risk analytics solutions, thus driving climate risk analytics market growth. Organizations are increasingly shifting from traditional on-premise systems to cloud-based environments to manage large volumes of climate, financial, and geospatial data more effectively. Cloud platforms enable real-time data processing, seamless integration of multiple data sources, and advanced analytics capabilities, allowing users to perform complex climate scenario modeling and risk assessments with greater speed and accuracy.

Additionally, the Software-as-a-Service (SaaS) model is gaining strong traction across both large enterprises and small & medium enterprises (SMEs), as it reduces upfront infrastructure costs and simplifies implementation. Cloud-based solutions also allow continuous updates aligned with evolving regulatory frameworks such as TCFD, ISSB, and CSRD, ensuring that organizations remain compliant without significant system overhauls. Moreover, the flexibility of cloud platforms supports collaboration across departments and geographies, enabling organizations to integrate climate risk insights into enterprise-wide decision-making processes.

MARKET RESTRAINTS

Data Complexity and Lack of Standardization are Restraining Market Growth

The complexity of climate data and the lack of standardized methodologies for risk assessment are key restraints for the market. Climate risk analysis requires the integration of large volumes of heterogeneous data, including historical climate data, forward-looking projections, geospatial datasets, and financial information. Managing and processing such complex datasets can be challenging for organizations, particularly those with limited technical capabilities.

Moreover, the absence of universally accepted standards for climate risk modeling and scenario analysis creates inconsistencies in results and reporting. Different models, assumptions, and data sources can lead to varying outcomes, making it difficult for organizations to compare results and make informed decisions. This lack of standardization can hinder adoption, especially among smaller enterprises and organizations in developing regions. For instance, in 2025, organizations such as MSCI Inc., Moody’s Corporation, and S&P Global highlighted challenges related to inconsistencies in climate scenario modeling and emphasized the need for standardized frameworks to improve comparability and reliability of risk assessments.

MARKET OPPORTUNITIES

Growing Integration of Climate Risk Analytics into Investment and Asset Management is Creating Market Opportunities

The increasing integration of climate risk considerations into investment strategies and asset management practices is creating significant growth opportunities for the market. Investors and asset managers are placing greater emphasis on understanding how climate-related risks can impact asset valuations, portfolio performance, and long-term returns. This has led to rising demand for advanced analytics platforms that provide granular, asset-level insights and scenario-based forecasting capabilities.

Additionally, the rapid growth of sustainable finance and ESG investing is further driving the adoption of climate risk analytics solutions. Organizations are leveraging these tools to align their portfolios with climate goals, recognize high-risk exposures, and optimize capital allocation. The use of geospatial analytics and artificial intelligence is also enhancing the ability to model complex climate scenarios and improve decision-making processes.

For instance, in 2026, leading asset management firms such as BlackRock, State Street Global Advisors, and Amundi expanded the use of climate risk analytics platforms to evaluate portfolio exposure under different climate scenarios, enabling more informed investment decisions and improved risk mitigation strategies.

MARKET CHALLENGES

Limited Data Availability in Emerging Markets and Modeling Uncertainty are Challenging Market Expansion

Limited availability of high-quality climate data in emerging markets and inherent uncertainties in climate modeling present significant challenges for the market. Many regions lack comprehensive historical datasets and localized climate projections, which are essential for accurate risk assessment. This limitation can reduce the effectiveness of analytics tools and hinder adoption in developing economies. Furthermore, climate models rely on long-term assumptions and scenario-based projections, which inherently involve uncertainty. Variations in emission pathways, policy developments, and technological advancements can significantly impact model outcomes, making it difficult for organizations to rely on a single set of projections. This uncertainty can create hesitation among end-users and complicate decision-making processes.

For instance, in 2025, institutions such as the World Bank, Network for Greening the Financial System (NGFS), and United Nations Environment Programme Finance Initiative (UNEP FI) highlighted challenges in applying global climate models to local contexts, emphasizing the need for improved data granularity and more reliable regional projections.

Segmentation Analysis

By Component

Software / Platforms Segment is Leading Driven by Increasing Demand for Scalable Risk Assessment Solutions

Based on component, the market is segmented into software/platforms, data & analytics services, and professional & consulting services.

The software/platforms segment dominated the market accounting for a 73.41% share in 2025, driven by the increasing adoption of scalable, cloud-based solutions for climate risk assessment, scenario analysis, and regulatory reporting. These platforms enable organizations to integrate large volumes of climate and financial data, perform advanced modeling, and generate actionable insights, making them essential tools for financial institutions, corporates, and government agencies. Additionally, the growing need for automation, real-time analytics, and integration with enterprise systems is further fast-tracking the adoption of software/platform solutions.

The data & analytics services segment is expected to grow at a CAGR of 15.76% during the forecast period, supported by the rising demand for high-quality datasets, climate modeling, and customized analytics solutions. Organizations are increasingly relying on third-party providers for climate data acquisition, processing, and interpretation. The professional & consulting services segment also holds a considerable share, driven by the need for regulatory compliance, strategy development, and implementation support, particularly among organizations in the early stages of climate risk integration.

By Risk Type

Physical Risk Segment Dominates Due to Increasing Climate Event Frequency

Based on risk type, the market is segmented into physical risk, transition risk, and liability risk.

The physical risk segment dominated the market accounting for the 49.73% share in 2025, driven by the increasing frequency and severity of climate-related events such as floods, storms, wildfires, and heatwaves. Organizations across sectors are prioritizing the assessment of asset-level exposure to physical risks to mitigate financial losses and improve resilience. Climate risk analytics solutions enable detailed geospatial analysis and forward-looking projections, supporting the strong adoption of physical risk assessment tools.

The liability risk segment is expected to grow at a CAGR of 19.53% during the forecast period, driven by increasing legal, regulatory, and reputational pressures associated with climate change. As stakeholders, including investors, regulators, and the public, demand greater accountability and transparency, organizations are facing a rising risk of litigation related to inadequate climate disclosures, environmental damages, and failure to meet sustainability commitments. This has significantly increased the need for advanced analytics tools that can assess potential legal exposures and support accurate reporting.

By Deployment Mode

Cloud-Based Segment is Leading Supported by Scalability and Real-Time Analytics Capabilities

Based on deployment mode, the market is segmented into cloud-based and on-premise solutions.

The cloud-based segment dominated the market accounting for the 74.96% share in 2025, driven by its scalability, flexibility, and ability to process large volumes of climate and financial data in real time. Cloud platforms enable seamless integration with multiple data sources, support advanced analytics, and facilitate collaboration across organizations. The increasing adoption of Software-as-a-Service (SaaS) models and the need for cost-effective deployment are further contributing to the growth of this segment growth.

The on-premise segment holds a comparatively smaller share, primarily driven by organizations with stringent data security and regulatory requirements. However, its growth is relatively moderate compared to cloud-based solutions, as enterprises increasingly shift toward digital and cloud-first strategies.

By Organization Size

Large Enterprises Segment Dominated Due to Regulatory Compliance and Advanced Risk Management Needs

Based on organization size, the market is segmented into large enterprises and small & medium enterprises (SMEs).

The large enterprises segment dominated the market, accounting for a 78.53% share in 2025, driven by stringent regulatory requirements, higher exposure to climate-related risks, and the availability of resources to invest in advanced analytics solutions. Large organizations, particularly in the financial services, energy, and infrastructure sectors, are actively adopting climate risk analytics tools to support compliance, risk management, and strategic decision-making.

The SMEs segment is expected to grow at a 17.05% CAGR during the forecast period, supported by increasing awareness of climate risks and the availability of cost-effective, cloud-based analytics solutions. As regulatory frameworks expand and sustainability becomes a key business priority, SMEs are gradually integrating climate risk analytics into their operations, contributing to the segment’s growth.

By End-User

To know how our report can help streamline your business, Speak to Analyst

BFSI Segment Leads Driven by Increasing Climate Risk Integration in Financial Decision-Making

Based on end-user, the market is segmented into BFSI, energy & utilities, government & public sector, real estate & infrastructure, agriculture & forestry, manufacturing, transportation & logistics, and others.

The BFSI segment held the highest climate risk analytics market share of 36.73% in 2025, driven by increasing regulatory pressure, climate stress testing requirements, and the need to assess portfolio-level risk exposure. Financial institutions are extensively using climate risk analytics platforms to evaluate credit risk, investment risk, and long-term financial impacts under various climate scenarios.

The government & public sector segment is expected to be the fastest growing segment during the forecast period, driven by increasing focus on climate policy implementation, infrastructure resilience, and long-term environmental planning. Governments and public authorities are playing a central role in assessing and mitigating climate-related risks across national and regional infrastructure, including transportation networks, energy systems, and urban developments. The growing adoption of climate risk analytics tools is enabling policymakers to conduct scenario analysis, evaluate vulnerability to physical risks, and design effective adaptation and mitigation strategies.

Climate Risk Analytics Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Climate Risk Analytics Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The North America region dominated the global market, accounting for approximately USD 802.87 million in 2025 and will reach USD 942.17 million in 2026. The market in North America is growing due to strong regulatory frameworks, increasing climate disclosure requirements, and widespread adoption of advanced analytics solutions. The region is witnessing rising demand for climate scenario analysis, stress testing, and portfolio-level risk assessment tools across financial institutions and corporates.

U.S. Climate Risk Analytics Market

The U.S. market accounted for approximately USD 699.22 million in 2025, representing nearly 87% share of the North America market. The market is growing due to increasing regulatory pressure, adoption of climate stress testing, and strong presence of financial institutions integrating climate risk into decision-making processes.

Europe

The Europe region accounted for USD 506.50 million in 2025 and will reach USD 589.48 million in 2026. The market in Europe is growing due to stringent regulatory frameworks such as the Corporate Sustainability Reporting Directive (CSRD), increasing investments in sustainable finance, and strong focus on climate transparency. The European Union’s emphasis on climate disclosures and risk management is encouraging the adoption of advanced analytics platforms.

U.K. Climate Risk Analytics Market

The U.K. market in 2025 reached USD 86.83 million. The market holds a notable share within Europe, driven by strong regulatory oversight and increasing adoption of climate stress testing frameworks led by institutions such as the Bank of England.

Germany Climate Risk Analytics Market

The German market in 2025 was valued at USD 112.06 million. The market is driven by strong industrial infrastructure, expansion of renewable energy projects, and increasing investments in grid modernization.

Asia Pacific

The Asia Pacific region accounted for USD 345.64 million in 2025 and will reach USD 415.18 million in 2026. The Asia Pacific market is growing due to rapid economic development, increasing exposure to climate-related risks, and rising adoption of ESG frameworks across countries such as China, India, Japan, and Southeast Asia. Government initiatives focused on climate resilience, sustainable infrastructure, and green finance are further supporting market growth.

China Climate Risk Analytics Market

China accounted for USD 113.66 million in 2025, representing around 32.88% share of the Asia Pacific market. This growth is driven by strong government focus on carbon neutrality and expansion of green finance initiatives.

India Climate Risk Analytics Market

India market reached USD 90.01 million in 2025 and will be valued at USD 110.83 million in 2026. The growth is supported by increasing climate vulnerability and infrastructure development.

Latin America & Middle East Africa

Latin America and the Middle East & Africa accounted for USD 76.39 million and USD 68.10 million in 2025, respectively. The market in Latin America is growing due to increasing awareness of climate risks, rising investments in sustainable infrastructure, and increasing regulatory frameworks. Countries such as Brazil and Mexico are increasingly adopting climate risk analytics solutions for policy planning and financial risk assessment.

The Middle East & Africa market is growing due to expanding infrastructure development, increasing focus on climate resilience, and rising investments in sustainability initiatives. Governments are adopting climate analytics tools to support long-term planning and mitigate environmental risks.

GCC Climate Risk Analytics Market

The GCC market in 2025 was at USD 29.53 million. The GCC region holds a significant share within Middle East & Africa region, driven by increasing investments in smart city projects, energy diversification, and sustainability initiatives across countries such as the UAE, Saudi Arabia, and Qatar.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Adoption of Advanced Climate Modeling, AI Integration, and Scalable Analytics Platforms by Key Players Drives Market Competition

Climate risk analytics market vendors are undertaking various strategic initiatives to support market growth by focusing on technological innovation, integration of advanced climate modeling capabilities, and expansion of scalable analytics platforms. Major players such as MSCI Inc., Moody’s Corporation, S&P Global Inc., Verisk Analytics Inc., Jupiter Intelligence, and XDI (Cross Dependency Initiative) are investing in high-resolution climate data, geospatial analytics, and AI-driven risk modeling solutions. These companies are continuously enhancing their platforms by incorporating features such as real-time risk assessment, scenario analysis, asset-level risk mapping, and integration with financial systems to support banks, insurers, asset managers, and government agencies.

In June 2024, MSCI Inc. expanded its climate risk analytics suite by enhancing its Climate Value-at-Risk (Climate VaR) model, enabling more granular asset-level analysis and improved scenario-based forecasting for institutional investors. This development highlights the growing focus on high-precision, data-driven analytics solutions in the market.

LIST OF KEY CLIMATE RISK ANALYTICS COMPANIES PROFILED

- MSCI Inc. (U.S.)

- Moody’s Corporation (U.S.)

- Verisk Analytics Inc. (U.S.)

- Jupiter Intelligence (U.S.)

- XDI (Cross Dependency Initiative) (Australia)

- Climate X (U.K.)

- Cervest Ltd. (U.K.)

- Swiss Re Group (Switzerland)

- io (U.S.)

- Woodwell Climate Research Center (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: MSCI Inc. enhanced its Climate Value-at-Risk (Climate VaR) framework by incorporating improved climate scenario datasets and expanded asset-level coverage across emerging markets. The update enables investors to better assess portfolio exposure to both acute and chronic physical risks, as well as transition risks under evolving policy environments. This development reflects the increasing demand for more localized and forward-looking climate risk insights in global investment strategies.

- February 2026: Moody’s Corporation expanded its climate risk analytics platform by integrating advanced geospatial data and AI-driven modeling capabilities into its credit assessment tools. The enhancement allows financial institutions to evaluate borrower-level climate exposure more accurately, particularly in sectors such as real estate, infrastructure, and energy. This initiative highlights Moody’s focus on embedding climate intelligence into core financial decision-making processes.

- January 2026: S&P Global introduced upgraded climate scenario analysis tools, designed to support regulatory reporting and portfolio stress testing under multiple climate pathways. The platform enhancements enable users to align their risk assessments with evolving global standards such as ISSB and regional disclosure frameworks. This development underscores the growing importance of standardized and transparent climate risk reporting across financial markets.

- November 2025: Jupiter Intelligence expanded its climate analytics platform by launching enhanced asset-level risk modeling solutions for infrastructure and real estate sectors. The update incorporates high-resolution climate projections and real-time data inputs, enabling organizations to assess vulnerabilities more accurately and develop effective resilience strategies. This reflects the increasing demand for granular and actionable climate risk insights.

- September 2025: Climate X strengthened its digital twin climate risk platform by improving its geospatial simulation capabilities and expanding coverage across additional global regions. The platform enhancements enable more precise modeling of climate impacts on physical assets, supporting financial institutions and corporates in making data-driven investment and risk management decisions.

REPORT COVERAGE

The climate risk analytics market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 17.57% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Component, By Risk Type, By Deployment Mode, By Organization Size, By End-User, and Region |

| By Component |

|

| By Risk Type |

|

| By Organization Size |

|

| By Deployment Mode |

|

| By End-User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the market value stood at USD 1,799.5 million in 2025 and is projected to reach USD 7,706.4 million by 2034.

The market is expected to exhibit a CAGR of 17.57% during the forecast period (2026-2034).

The Banking, Financial Services & Insurance (BFSI) segment led the market in terms of end-user.

Increasing regulatory mandates and climate disclosure requirements are driving market growth.

MSCI Inc., Moodys Corporation, and Jupiter Intelligence are leading companies in the market.

North America held the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 197

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us