Clinical Workflow Solutions Market Size, Share & Industry Analysis, By Type (Data Integration Solutions {EMR Integration Solutions, Medical Image Integration Solutions, and Medical device & physiologic data integration}, Real-time Communication Solutions, Workflow Automation Solutions {Patient Flow Management and Nursing & Staff Scheduling Solutions}, Care Collaboration Solutions {Medication Administration Solutions, Perinatal Care Management Solutions}, and Enterprise Reporting & Analytics Solutions), By End User (Hospitals & ASCs, Long-Term Care Facilities), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

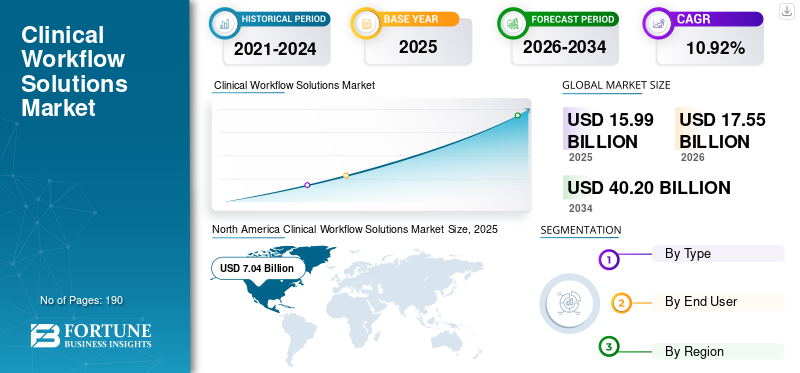

The global clinical workflow solutions market size was valued at USD 15.99 billion in 2025. The market is projected to grow from USD 17.55 billion in 2026 to USD 40.20 billion by 2034, exhibiting a CAGR of 10.92% during the forecast period. North America dominated the clinical workflow solutions market with a market share of 44.0% in 2025.

Clinical workflow solutions streamline clinical and operational processes across hospitals, ambulatory care, and other care settings. The core functions of these solutions include EHR-integrated automation, task orchestration, care-team communication, order and results management, clinical documentation workflows, and analytics for quality and throughput improvements. This marketspace is witnessing a strong growth owing to rising demand for EHR integration and demand for reduced clinician documentation burden along with other factors.

The market comprises various key industry players, such as Oracle, McKesson Corporation, and Koninklijke Philips N.V. These companies are focusing on innovative product offerings to maintain their market presence.

Download Free sample to learn more about this report.

Clinical Workflow Solutions Market Key Takeaways

- 2025 Market Size: USD 15.99 billion

- 2026 Market Size: USD 17.55 billion

- 2034 Forecast Market Size: USD 40.20 billion

- CAGR: 10.92% from 2026–2034

- North America dominated the clinical workflow solutions market with a 44.0% share in 2025.

- The enterprise reporting & analytics solutions segment accounted for the largest market share in 2025.

- The hospitals & ASCs segment is projected to hold a 76.5% market share in 2026.

North America

North America held a 44.0% share in 2025, valued at USD 7.04 billion.

Asia Pacific

Asia Pacific is projected to reach USD 3.89 billion by 2026, driven by expanding hospital networks and healthcare digitalization initiatives across China and India.

Europe

Europe is projected to reach USD 4.41 billion by 2026, supported by national eHealth initiatives and increasing adoption of digital healthcare solutions.

U.S.

The market projected to reach USD 7.07 billion by 2026.

Japan

The market projected to reach USD 0.94 billion by 2026.

Read More

CLINICAL WORKFLOW SOLUTIONS MARKET TRENDS

Increasing Cloud and SaaS Adoption is a Significant Trend Observed in Market

In recent years, the global market is witnessing an increasing adoption of cloud and SaaS based solutions. These solutions offer advantages such as faster deployments, easier upgrades, and the ability to scale workflows across multi-site systems, resulting in higher demand. Cloud delivery also supports remote/mobile-first care teams and enables more frequent feature releases. These factors are supporting the overall global clinical workflow solutions market growth.

- For instance, in August 2025, Oracle announced that its AI-driven EHR is now available for ambulatory providers in the U.S.

[EdMGtkDjdO]

MARKET DYNAMICS

MARKET DRIVERS

Increasing EHR Integration and Demand for Reduced Clinician Documentation Burden is Propelling Market Growth

Increasing EHR integration and the push to reduce clinician documentation burden is a major market driver. This can be owing to the increasing demand for workflow tools from healthcare providers that are integrated inside the EHR and remove extended worktimes caused by manual charting. As health systems standardize on large EHR platforms, they are increasingly preferring solutions that are natively embedded or tightly integrated. This demand is accelerating adoption of ambient documentation / AI scribe, smart note generation, and automated coding/order cues. These solutions deliver measurable benefits in productivity, clinician satisfaction, and documentation completeness. All these factors cumulatively drive the overall market growth.

- For instance, in January 2025, Nuance, which was acquired by Microsoft, announced that DAX Copilot embedded in Epic is now generally available.

MARKET RESTRAINTS

Data Privacy and Cybersecurity Risks to Hamper Market Growth

Data privacy and cybersecurity risks are a major market restraint for clinical workflow solutions. These platforms handle highly sensitive patient data, integrate deeply with EHRs/devices, and play an important role in care delivery. That makes them high-value targets for attackers and a single breach or ransomware event can trigger regulatory exposure, downtime, reputational damage, and loss of clinician trust, which slows purchasing decisions, extends security reviews, and pushes providers to limit integrations or delay rollouts. This results in limiting the market growth to a certain extent.

- For instance, in October 2025, a breach affecting 319,177 patients’ data was identified by VITAS Healthcare highlighting data security issues.

MARKET OPPORTUNITIES

AI/ML-enabled Clinical Decision Support and NLP-driven Documentation to Offer Market Growth Opportunities

AI/ML-enabled clinical decision support and NLP-driven documentation offers a strong market growth opportunity as it helps clinicians make faster, more consistent decisions, risk prediction, next-best action, guideline nudges while cutting documentation time through automated note generation and structured data capture. As health systems consolidate onto major EHRs, the biggest opportunity is for vendors that can deliver EHR-embedded AI with strong governance, auditability, and low hallucination risk. All these factors would drive the market growth in the coming years.

- For instance, in February 2024, Abridge launched Abridge Inside, a generative-AI documentation offering embedded inside standard Epic workflows.

MARKET CHALLENGES

Fragmented Vendor Landscape Pose a Critical Challenge to Market Growth

In this marketspace, buyers face complex vendor evaluation and consolidation trade-offs, in turn facing a challenge in market growth. Hospitals often require a significant number of different types of solutions. This creates multiple logins, inconsistent user experiences, duplicate workflows, and data silos, which reduces clinician adoption and slows ROI. In addition, procurement becomes harder too as systems struggle with vendor overlap and unclear ownership across IT/clinical/operations, leading to slower market growth.

- For instance, according to an article published in HealthcareITNews in November 2024, healthcare faces fragmentation from an abundance of systems and vendors with limited alignment.

Segmentation Analysis

By Type

High Demand for Software to Propel Segmental Growth

Based on the type, the market is divided into data integration solutions {emr integration solutions, medical image integration solutions, and medical device & physiologic data integration}, real-time communication solutions {nurse call alert systems and unified communication solutions}, workflow automation solutions {patient flow management solutions and nursing & staff scheduling solutions}, care collaboration solutions {medication administration solutions, perinatal care management solutions, rounding solutions, and others}, and enterprise reporting & analytics solutions.

The enterprise reporting & analytics solutions segment is expected to hold the largest global clinical workflow solutions market share. The dominance of the segment is primarily attributed to the high attach rates as deployed enterprise-wide across facilities, generation of recurring revenue through subscriptions and services, and increasing embedding inside core clinical platforms. Moreover, new product launches by operating players are also aimed at propelling the segmental revenue generation.

- For instance, in October 2024, Oracle announced updates to Oracle Health Data Intelligence designed to help organizations improve care quality and decision-making and highlighting cloud/AI-enabled analytics across networks.

The data integration solutions segment is anticipated to rise with a CAGR of 8.71% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

High Adoption by Hospitals Supported their Leading Position

Based on end user, the market is segmented hospitals & ASCs, long-term care facilities, and others.

The hospitals & ASCs segment captured the dominating position in the global market. This setting runs the most complex, high-acuity workflows, which creates the strongest demand for workflow software. In addition, hospitals and ASCs feel the most pressure on throughput, length of stay, staffing efficiency, and quality reporting, which directly increases demand for patient flow tools. Furthermore, the segment is set to hold 76.5% share in 2026.

In addition, long-term care facilities are projected to grow at a CAGR of 13.20% during the study period.

Clinical Workflow Solutions Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Clinical Workflow Solutions Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America captured the dominating position in 2024, with a revenue generation of USD 6.43 billion, and also maintained its dominance in 2025, with USD 7.04 billion. Key factors supporting regional dominance include high EHR penetration and early adoption of clinical workflow tools, strong vendor presence, and rising investment in AI-driven features. The U.S. has a well-established infrastructure for integration of clinical workflow solutions which supports the country’s market growth.

U.S Clinical Workflow Solutions Market

The U.S. market led the North American market and can be analytically approximated at around USD 7.07 billion in 2026, accounting for roughly 40.3% of the global market.

Europe

Europe is projected to witness a CAGR of 9.40% in the coming years, becoming the second highest among all regions. The region would reach a valuation of USD 4.41 billion by 2026. Growing adoption driven by national eHealth initiatives and regulatory emphasis on quality coupled with emphasis on data protection and local deployment models are boosting the European market growth.

U.K. Clinical Workflow Solutions Market

The U.K. clinical workflow solutions market in 2026 is estimated at around USD 0.68 billion, representing roughly 3.9% of global revenues.

Germany Clinical Workflow Solutions Market

Germany’s clinical workflow solutions market is projected to reach approximately USD 1.14 billion in 2026, equivalent to around 6.5% of global sales.

Asia Pacific

The Asia Pacific regional market is projected to be valued at USD 3.89 billion in 2026 and secure the position of the third-largest region in the global clinical workflow solutions industry. Expanding hospital networks, digitalization drives in China and India, and increasing private provider spending have majorly driven the regional market growth.

Japan Clinical Workflow Solutions Market

The Japan clinical workflow solutions market in 2026 is estimated at around USD 0.94 billion, accounting for roughly 5.4% of global revenues.

Increasing digitalization in healthcare organizations in Japan has driven the market growth.

China Clinical Workflow Solutions Market

China’s clinical workflow solutions market is projected to be one of the significant markets across the world, with 2026 revenues estimated at around USD 1.31 billion, representing roughly 7.5% of global sales.

India Clinical Workflow Solutions Market

The India clinical workflow solutions market in 2026 is estimated at around USD 0.32 billion, accounting for roughly 1.8% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are likely to grow at a slower rate in this market space over the study period. The Latin America market is set to reach a valuation of USD 0.77 billion in 2026. Selective adoption with larger projects at major hubs and gradual rollout in healthcare modernization programs is driving the regional market growth.

Saudi Arabia Clinical Workflow Solutions Market

The Saudi Arabia clinical workflow solutions market is projected to reach around USD 0.40 billion in 2026, representing roughly 2.3% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Growing Digital Transformation Initiatives by Leading Firms to Strengthen Market Position

The competitive structure of the global market for clinical workflow solutions is moderately consolidated. Key companies including Oracle, McKesson Corporation, and Koninklijke Philips N.V. hold dominant positions in the market. Continuous investments in cloud based platforms, new product launches, and advancements in current product offerings support their leadership.

Other key players in the clinical workflow solutions market include Epic Systems Corporation, Ascom, Stryker, and others. During the forecast period, these entities will expand their global footprint through various initiatives, including digital transformation support, healthcare-focused consulting, and service portfolio expansion.

LIST OF KEY CLINICAL WORKFLOW SOLUTIONS COMPANIES PROFILED

- NXGN Management, LLC. (U.S.)

- Epic Systems Corporation (U.S.)

- Oracle (U.S.)

- McKesson Corporation (U.S.)

- Ascom (Switzerland)

- Stryker (U.S.)

- Koninklijke Philips N.V. (The Netherlands)

- TigerConnect (U.S.)

- General Electric Company (GE Healthcare) (U.S.)

- TeleTracking Technologies, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Ascom in collaboration with B. Braun and Dräger introduced Silent ICU, focused on smart digital alarm management and workflow efficiency in critical care.

- August 2025: Oracle announced advancements to its Electronic Data Capture (EDC) solution, Oracle Clinical One Data Collection with an aim to streamline clinical trials.

- May 2025: Epic Systems Corporation launched new tools aimed at bringing generative AI into clinical workflows and improving EHR usability

- May 2025: Stryker announced the release of Vocera Edge server 4.15.1, with new features.

- March 2025: NextGen Healthcare announced AI-driven enhancements to streamline patient-provider workflows

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2019-2024 |

|

Growth Rate |

CAGR of 10.92% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, End User, and Region |

|

By Type |

· Data Integration Solutions o EMR Integration Solutions o Medical Image Integration Solutions o Medical device & physiologic data integration · Real-time Communication Solutions o Nurse Call Alert Systems o Unified Communication Solutions · Workflow Automation Solutions o Patient Flow Management Solutions o Nursing & Staff Scheduling Solutions · Care Collaboration Solutions o Medication Administration Solutions o Perinatal Care Management Solutions o Rounding Solutions o Others · Enterprise Reporting & Analytics Solutions |

|

By End User |

· Hospitals & ASCs · Long-Term Care Facilities · Others |

|

By Region |

· North America (By Type, End User, and Country) o U.S. o Canada · Europe (By Type, End User, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Type, End User, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Type, End User, and Country/Sub-region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Type, End User, and Country/Sub-region) o GCC o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 15.99 billion in 2025 and is projected to reach USD 40.20 billion by 2034.

In 2025, the market value stood at USD 7.04 billion.

The market is expected to exhibit a CAGR of 10.92% during the forecast period of 2026-2034.

By type, the enterprise reporting & analytics solutions segment is expected to lead the market.

EHR integration and demand for reduced clinician documentation burden is driving market expansion.

Oracle, McKesson Corporation, and Koninklijke Philips N.V. are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us