Clustering Software Market Size, Share & Industry Analysis, By Deployment (On-premises and Cloud-based), By Enterprise Type (Large Enterprises and Small & Medium Enterprises (SMEs)), By Operating System (Windows, Linux/ Unix, and Others), By Type (Self-service clustering, Managed clustering, and Hybrid clustering), By Industry (BFSI, IT and Telecommunication, Healthcare, Retail & E-commerce, Manufacturing, and Others), and Regional Forecast, 2026-2034

Clustering Software Market Size and Future Outlook

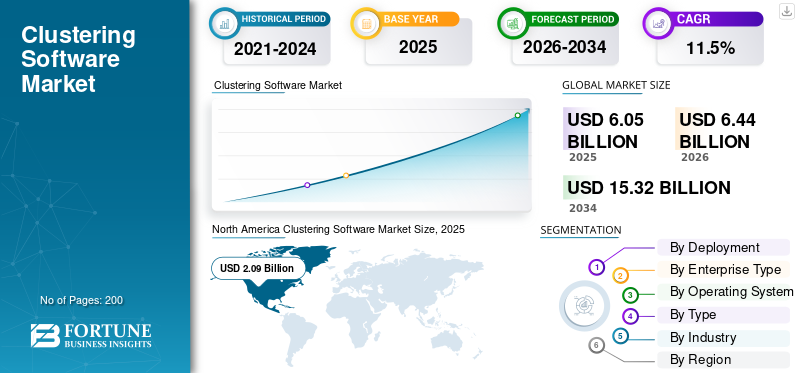

The global clustering software market size was valued at USD 6.05 billion in 2025. The market is projected to grow from USD 6.44 billion in 2026 to USD 15.32 billion by 2034, exhibiting a CAGR of 11.5% during the forecast period. North America dominated the global clustering software market with a market share of 34.55% in 2025.

The market for clustering software is experiencing tremendous growth as key companies increasingly focus on delivering continuous service availability, providing scalable computing power, and enhancing the ability to process and analyze large volumes of data. With the rise in popularity of hybrid cloud computing, as well as the growing use of container-based applications and artificial intelligence (AI), organisations have begun to rely heavily on clustering solutions to provide improved operational stability and reduce the risk of downtime in their systems.

Today’s modern clusters offer automated failover capabilities, intelligent workload distribution, and real-time monitoring. Therefore, many organisations can effectively support complex distributed IT environments with a much higher degree of reliability than previously possible.

This market growth is being increased by the ongoing digital transformation occurring across many industries, including banking and financial services, healthcare, telecommunications, manufacturing, and retail. The growth in online services, coupled with the dramatic increase in transactional data and the increasingly adopt use of edge computing devices, also adds to the current demand for clustering software solutions. The trend toward digital transformation in organisations’ IT infrastructure and their growing need to build resilient IT environments further support increased requirements for clustering software solutions.

Companies such as Oracle, SAP SE, and Alteryx stay competitive in the market by tightly integrating advanced clustering and machine learning capabilities into their broader analytics ecosystems. They focus on automating data preparation and modeling, enabling users to run clustering at scale with minimal complexity. These firms also strengthen their positions through vertical specific solutions.

Download Free sample to learn more about this report.

Clustering Software Market Key Takeaways

- 2025 Market Size: USD 6.05 billion

- 2026 Market Size: USD 6.44 billion

- 2034 Forecast Market Size: USD 15.32 billion

- CAGR: 11.5% from 2026–2034

- North America dominated the global clustering software market with a 34.55% share in 2025.

- The healthcare industry segment is expected to grow at a CAGR of 14.3% during the forecast period.

- The cloud-based segment is expected to grow at a CAGR of 16.0% during the forecast period.

North America

North America is projected to reach a market size of USD 2.22 billion by 2026.

Europe

Europe is expected to maintain steady growth and reach USD 1.84 billion by 2026.

Asia Pacific

Asia Pacific is anticipated to register the highest regional growth and achieve USD 1.62 billion by 2026.

U.S.

The clustering software market is projected to reach USD 1.97 billion by 2026.

Japan

Increasing adoption of cloud technologies and digital transformation initiatives is expected to support market growth.

Read More

IMPACT OF AI

Implementation of AI Capabilities to Fuel Growth of Market

AI has transformed clustering software by making it smarter, more flexible, and capable of handling complex data. Unlike traditional methods that rely on simple distance metrics and fixed parameters, AI-powered clustering can automatically learn meaningful features, capture nonlinear patterns, and dynamically adjust clusters.

This results in more accurate and semantically meaningful groupings, especially for high-dimensional or unstructured data such as images and text. AI also improves scalability, allowing real-time clustering of large datasets, reduces noise, and helps in detecting anomalies.

For instance, in December 2022, ISRA VISION launched Cloud Xperience, a cloud-based software platform for its SMASH inspection systems that leverages AI for automated clustering and classification of defects. The platform centralizes production data, enables real-time monitoring of KPIs, and allows process optimization across multiple sites.

CLUSTERING SOFTWARE MARKET TRENDS

Expansion into SMEs and Diverse Industries to be a Key Trend in Market

Historically, clustering software was primarily used by large corporations, which had the necessary infrastructure and budget to support its implementation. However, due to the proliferation of low-cost cloud-based deployment models, reduced technical and financial barriers to entry, and the introduction of simpler management tools, small & medium sized enterprises (SMEs) can now leverage distributed computing for analytics, data processing, and decision-making.

As a result of these changes, the use of clustering technology has expanded beyond the traditional tech industries. It is now being adopted in many other sectors, including healthcare, retail, manufacturing, finance, and logistics. This combination of SME's adoption and cross-industry growth is opening up new opportunities for market expansion and creating demand for the development of clustering technologies that can meet the needs of organizations of all shapes and sizes.

MARKET DYNAMICS

MARKET DRIVERS

Explosion of Data and Increasing Data Complexity to Propel Market Growth

The rapid increase in data growth/complexity has become a main factor driving many users to cluster software. These days, organizations produce and receive large amounts of data through various means, including databases, devices, users, and media. For instance,

- According to Rivery, in 2024, the global volume of data created, captured, copied, and consumed reached 149 zettabytes, and it is projected to grow further to 181 zettabytes by the end of 2025.

The traditional approach to utilizing numerous databases via a single server is unable to handle this increased level and type of Data. It therefore requires a new approach that supports the distribution of data between multiple servers and allows for parallel processing, as clustering software accomplishes.

In addition to simply dealing with an increased quantity of data, today's data often contains multiple high-dimensional features, large amounts of real-time data (timed streams of data), and non-traditional formats. As a result, these characteristics complicate the use of clustering software.

MARKET RESTRAINTS

Data Security and Regulatory Compliances Constraint Market Growth

Organizations considering the use of clustering software face several major obstacles, including security, privacy, and regulatory compliance issues. The vast majority of companies work with sensitive/confidential customer information, such as personal information, financial records, health care data, and/or proprietary business information, so security concerns for their cluster infrastructure should be paramount.

As clustering systems typically utilize distributed storage and/or processing across multiple nodes or cloud environments, the likelihood of a data breach, unauthorized access, or accidental exposure increases significantly if they are not properly managed.

Furthermore, organizations operating in regulated industries are required to protect and secure the personal information of their customers in accordance with regulatory requirements, including the GDPR, HIPAA, or other sector-specific regulations.

MARKET OPPORTUNITIES

Growing Adoption of AI and Machine Learning to Create Lucrative Growth Opportunities

The increasing use of Artificial Intelligence (AI) and Machine Learning (ML) across various sectors is driving a growing demand for cluster computing software. For instance,

- According to an IBM survey, 42% of enterprise-level companies are currently using machine learning, while another 40% plan to explore its adoption by 2025.

There are many different types of applications that companies are executing, utilizing AI or ML, such as predictive analytics, recommendation engines, Natural Language Processing (NLP), computer vision, and automation, to deliver products or services to their customers.

AI and machine learning require processing large, complex, and high-dimensional datasets that often exceed the capacity of traditional computers. Clustering software addresses this by enabling parallel processing across multiple nodes, providing the computing power needed to train models more efficiently, review generated data, and support iterative model development by distributing workloads across clusters within an organization.

Download Free sample to learn more about this report.

Clustering Software Market Segmentation Analysis

By Industry

BFSI Emerges as a Key Revenue Contributor in Market Growth

Based on industry, the market is classified into BFSI, IT and telecommunications, healthcare, retail & e-commerce, manufacturing, and others.

To know how our report can help streamline your business, Speak to Analyst

BFSI holds the majority share in the market primarily due to its critical need for uninterrupted operations, high-volume transaction processing, and stringent data-security requirements. Financial institutions rely heavily on real-time analytics, fraud detection, risk modeling, and core banking applications that must remain continuously available. Clustering software ensures high availability, load balancing, and rapid failover to prevent service disruptions. Additionally, regulatory pressures around data integrity and disaster recovery further drive BFSI organizations to invest in advanced clustering solutions.

The healthcare industry is expected to grow at a CAGR of 14.3% over the forecast period.

By Deployment

On-Premises Solutions Dominate Clustering Software Adoption Trends

In terms of deployment, the market is categorized into on-premises and cloud-based.

The on-premises captured the largest market share in 2025. In 2026, the segment is anticipated to dominate with a 55.2% share, as the majority of organizations utilize on-premises clustering software to maintain maximum control over their data, infrastructure, and security. This is especially true for organizations with critical or sensitive workloads that require a high degree of custom configuration, predictable performance, and a hands-on approach to managing failover.

The cloud-based is expected to grow at a CAGR of 16.0% over the forecast period.

By Enterprise Type

Large Enterprises Lead Adoption of High-Availability Clustering Software

In terms of enterprise type, the market is categorized into large enterprises and small & medium enterprises.

Large enterprises captured the largest share of the market in 2025. In 2026, the segment is expected to dominate with a 67.0% share, driven by the need for extensive IT infrastructure that supports high levels of availability, consistency of performance, and advanced scalability. These organizations operate in environments with numerous applications and large transaction volumes across multiple locations; therefore, they rely heavily on clustered technology to minimize service interruptions and ensure continuous access to services.

Small & medium enterprises are expected to grow at a CAGR of 14.3% over the forecast period.

By Operating System

Linux/Unix Remains Preferred Platform for Clustering Software

In terms of operating system, the market is categorized into windows, linux/unix, and others.

The linux/unix segment captured the largest share of the market in 2025. In 2026, the segment is expected to dominate with a 50.7% share, as it provides large numbers of users with strong stability, scalability, and performance capabilities that are ideal for high-availability solutions. A benefit of their open-source architecture is the abundance of options for customization and the ease of integrating with cluster tools.

Others (macOS, etc.) is expected to grow at a CAGR of 11.1% over the forecast period, driven by increasing adoption in creative industries, design, and technology sectors. MacOS offers stability, seamless integration with creative tools, and a user-friendly experience, making it a preferred choice.

By Type

Enterprises Favor Self-service Clustering for Agility and Scalability

In terms of type, the market is categorized into self-service clustering, managed clustering, and hybrid clustering.

The self-service clustering segment captured the largest share of the market in 2025. In 2026, the segment is expected to dominate with a 53.1% share, as more companies focus on making it easier for users to deploy and manage clusters with reduced dependence on IT resources. Self-service clustering solutions have been developed to provide an accelerated process for setting up clusters, automated processes for configuring, and easy-to-use interfaces to help users easily scale, maintain availability, and reduce the complexity associated with managing a cluster environment.

Managed clustering is expected to grow at a CAGR of 13.6% over the forecast period.

Clustering Software Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and Middle East & Africa.

NORTH AMERICA

North America holds the majority of the clustering software market share, supported by its advanced enterprise IT infrastructure, a strong base of large-scale data-intensive companies, and the significant presence of major cloud and software vendors. The region benefits from early adoption of high-availability architectures, AI-driven workload automation, and advanced distributed computing frameworks. North America is projected to reach USD 2.22 billion by 2026, with the U.S. alone contributing USD 1.97 billion, underscoring its continued leadership in mission-critical IT deployments and enterprise resilience strategies.

North America Clustering Software Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

EUROPE

Europe represents the second-largest share of the market and is expected to maintain steady clustering software market growth, reaching USD 1.84 billion by 2026. Growth in this region is driven by rapid modernization of enterprise data centers, strict data protection regulations that encourage secure on-premises clustering, and rising adoption of automation-based IT orchestration platforms. Key contributors include the U.K. (USD 0.32 billion), Germany (USD 0.28 billion), and France (USD 0.22 billion), reflecting strong increasing demand for high-availability systems and operational continuity solutions.

ASIA PACIFIC

Asia Pacific is anticipated to register the highest CAGR by 2026, achieving a market size of USD 1.62 billion. This acceleration is fueled by large-scale digital transformation, rapid cloud adoption, and growing enterprise dependence on scalable workload distribution technologies. Countries such as China (USD 0.55 billion) and India (USD 0.36 billion) lead the region due to the expansion of data center ecosystems, increasing 5G deployment, and government-driven investments in advanced computing capabilities.

MIDDLE EAST & AFRICA

The Middle East & Africa region is projected to grow steadily, reaching USD 0.40 billion by 2026. This growth is supported by improvements in enterprise IT infrastructure, national digital modernization initiatives, and a rising demand for clustering solutions within the government, transportation, and retail sectors. The GCC countries are expected to account for USD 0.05 billion, driven by strong investments in resilient IT operations and emerging cloud-native ecosystems.

SOUTH AMERICA

South America is expected to reach USD 0.23 billion by 2026, driven by increasing enterprise adoption of clustering software for workload optimization, logistics systems, high-availability e-commerce platforms, and digital urban services. The expansion of data center footprints and the greater adoption of cloud platforms in countries such as Brazil and Mexico continue to support regional market growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovative Ecosystems and Strategic Integration Drive Market Leadership

The clustering software market is led by major enterprise-focused companies that continuously innovate by integrating advanced high-availability frameworks, AI-driven workload management, and scalable distributed computing ecosystems. Key players, including IBM, Oracle, SAP, and Fujitsu, shape the market by providing robust and reliable clustering solutions that support mission-critical applications, real-time data processing, and large-scale enterprise operations across various industries.

These companies differentiate themselves through comprehensive platforms that combine automated failover, intelligent resource allocation, hybrid and multi-cloud compatibility, and real-time system monitoring. Their offerings emphasize high reliability, performance optimization, and seamless integration with enterprise IT infrastructures, ERP systems, and big data platforms. For example, IBM delivers solutions such as PowerHA and Spectrum for high availability, Oracle provides Real Application Clusters for scalable database operations, SAP integrates clustering capabilities within its enterprise software to ensure system continuity, and Fujitsu offers high-availability solutions for mission-critical enterprise applications. Collectively, these companies define the competitive landscape by driving continuous innovation and delivering scalable, resilient, and enterprise-grade clustering solutions.

LIST OF KEY CLUSTERING SOFTWARE COMPANIES PROFILED

- IBM Corporation (U.S.)

- Oracle (U.S.)

- SAP SE (Germany)

- Alteryx, Inc. (U.S.)

- Axigen (Romania)

- Symantec (U.S.)

- Fujitsu (Japan)

- NEC Corporation (Japan)

- Red Hat (U.S.)

- VMware (U.S.)

- Hewlett Packard Enterprise Development LP (U.S.)

- Amazon Web Services, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Penguin Solutions (Nasdaq: PENG) released ICE ClusterWare 13.0, a major update to its AI and HPC cluster-management software. The new version introduces anomaly detection with auto-remediation to maintain peak performance across large clusters, as well as network-isolated multi-tenancy, which enables organizations to share GPU clusters among different user groups securely.

- September 2025: DH2i’s DxEnterprise clustering software now supports SQL Server 2025, offering full high availability (HA) and automated failover for AI-driven workloads, including vector databases and Kubernetes-based Availability Groups (AGs). The update enables enterprises to run mission-critical AI applications across on-prem, cloud, hybrid, and container environments with seamless failover, enhanced scalability, and continuous uptime, helping modernize infrastructure while maintaining robust reliability.

- February 2024: Advanced Clustering released a new edition of ClusterVisor, its HPC cluster management software. The update includes a redesigned web UI, role-based access control, monitoring alerts, and an improved upgrade tool. Most notably, it now bundles LogVisor AI, which analyzes log files and converts important messages into actionable alerts, enabling administrators to maintain optimal performance and prevent failures.

- November 2023: DH2i showcased its DxEnterprise smart high availability clustering software at the PASS Data Community Summit. The platform provides automatic failover for SQL Server Availability Groups in Kubernetes, enabling seamless modernization with containers and zero downtime.

- October 2022: SIOS LifeKeeper for Linux was SAP-recertified, confirming its reliability as clustering software for SAP NetWeaver and SAP S/4HANA environments. The certification validates its ability to deliver high availability and disaster recovery through automated failover.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also includes a detailed competitive landscape, providing information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 11.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Deployment, Enterprise Type, Operating System, Type, Industry and Region |

| By Deployment |

|

| By Enterprise Type |

|

| By Operating System |

|

| By Type |

|

| By Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 6.05 billion in 2025 and is projected to reach USD 15.32 billion by 2034.

In 2025, the market value stood at USD 2.09 billion.

The market is expected to exhibit a CAGR of 11.5% during the forecast period of 2026-2034.

The BFSI led the market by Industry.

Explosion of data and increasing data complexity to propel the market growth

IBM, Oracle, SAP, and Fujitsu are some of the prominent players in the market.

North America dominated the market in 2025.

The healthcare segment is expected to grow with the highest CAGR.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us