Coal Mining Market Size, Share & Industry Analysis, By Mining Method (Surface Mining and Underground Mining) By Grade (Low-Grade Coal (Lignite), Medium-Grade Coal (Sub-bituminous), High-Grade Coal (Bituminous), and Ultra-High-Grade Coal (Anthracite)), By End User (Power Generation, Steel Manufacturing, Cement Production, Chemical & Synthetic Fuels, Paper & Pulp, and Others) and Regional Forecast, 2026-2034

Coal Mining Market Size and Future Outlook

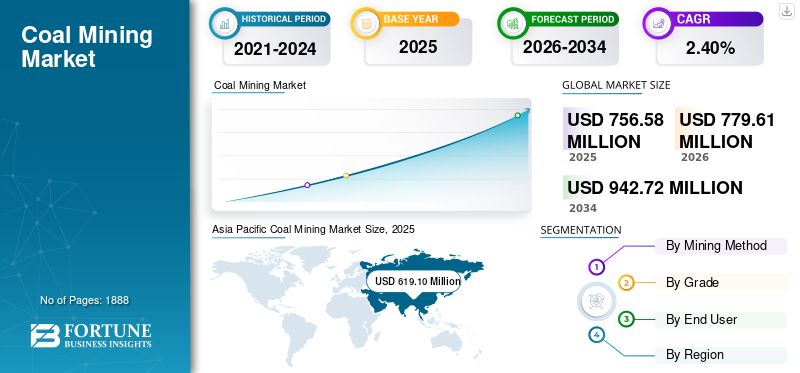

The global coal mining market size was valued at USD 756.58 million in 2025. The market is projected to grow from USD 779.61 million in 2026 to USD 942.72 million by 2034, exhibiting a CAGR of 2.40% during the forecast period. Asia Pacific dominated the global coal mining market with a market share of 81.82% in 2025.

Coal mining is the process of extracting coal from the Earth for use as a fuel and industrial raw material. It involves both surface mining and underground mining methods, depending on the depth and geological conditions of coal seams. The extracted coal is primarily used across various sectors, including power generation, steel manufacturing, and cement production. Rising electricity demand, particularly in emerging economies, continues to support coal use for baseload power generation, with global coal consumption reaching an estimated 8.8 billion tons in 2024, the highest level on record. Industrial demand for metallurgical coal in steel manufacturing further sustains mining activity. Coal’s cost competitiveness in energy-intensive and developing regions supports continued reliance on the fuel. Additionally, the large installed base of coal-fired power plants and energy security considerations reinforce short- to medium-term demand for coal mining.

Furthermore, many key industry players in the Coal Mining industry, such as Coal India Limited, China National Energy Group, China Shenhua Energy, Peabody Energy, and SUEK, are operating in the market and focusing on developing high-quality, standards-compliant coal mining solutions.

Download Free sample to learn more about this report.

COAL MINING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 756.58 million

- 2026 Market Size: USD 779.61 million

- 2034 Forecast Market Size: USD 942.72 million

- CAGR: 2.40% from 2026–2034

- Asia Pacific dominated the coal mining market with an 81.82% share in 2025.

- Surface mining accounted for the largest mining method segment with a 58.84% share in 2025.

- High-grade coal (bituminous) led the grade segment with a 55.44% share in 2025.

North America

North America accounted for USD 42.62 million in 2025, with market growth constrained by coal plant retirements and increasing adoption of natural gas and renewable energy.

Europe

Europe reached USD 61.91 million in 2025 and is projected to grow at a CAGR of 1.50%, reflecting the impact of decarbonization initiatives and coal phase-out policies.

Asia Pacific

Asia Pacific remained the leading regional market, supported by strong coal production and consumption across China, India, Indonesia, and Australia.

U.S.

The market was valued at USD 39.05 million in 2025, representing approximately 5.16% of global coal mining revenues, supported by industrial demand for metallurgical coal.

Japan

The coal mining market reached USD 38.24 million in 2025, accounting for roughly 5.05% of global coal mining revenues.

Read More

COAL MINING MARKET TRENDS

Plateauing and Structural Shift in Coal Demand Trend Observed in the Market

A defining trend in the global coal mining landscape is a plateau in coal demand, with growth slowing and consumption stabilizing at high levels before an eventual decline. Analysts project that demand will remain broadly flat through 2025–2026, with minor fluctuations across regions as emerging markets drive industrial and power needs while advanced economies phase down coal use. Coal’s share in global electricity generation is declining as renewables and gas gain traction, even though coal remains critical for energy security and reliability in many markets. This trend reflects structural changes in energy systems, with coal becoming less dominant relative to cleaner energy technologies.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Electricity Demand Growth and Coal Consumption Are Accelerating Market Growth

A major driver of the coal mining market growth is rising electricity demand, especially in developing economies where coal remains a key baseload fuel source. In 2024, global coal demand hit a record high of around 8.8 billion tons, driven largely by power generation needs in countries such as China and India, even as renewable capacity expanded. This reflects the continuing reliance on coal to meet peak and base-load electricity requirements, where grid reliability and capacity constraints remain challenges. Strong electricity demand growth, coupled with limited grid flexibility in some markets, reinforces coal power plant utilization and underpins coal mining volumes. Despite accelerating renewable deployment, coal’s role in meeting rising power demand persists in many regions due to existing infrastructure and incremental electricity growth tied to economic activity.

MARKET RESTRAINTS

Policy-Driven Phase-Outs and Environmental Regulation to Restrict Market Growth

Government policies aimed at reducing carbon emissions and phasing out coal-fired power plants act as a significant restraint on the coal mining market. Many advanced economies, including those in Europe and parts of North America, have committed to retiring coal capacity and implementing stricter environmental regulations to meet climate targets. For example, the U.K. closed its last coal-fired power plant in late 2024, marking a symbolic milestone in the decline of coal in that region. Similarly, coal demand in the European Union and the U.S. has decreased markedly in recent years due to regulatory pressure and incentives for cleaner energy. These policy-driven restraints reduce domestic coal demand and limit export opportunities for coal producers, constraining overall market growth despite ongoing demand in emerging markets.

MARKET OPPORTUNITIES

Industrial and Non-Power Coal Uses to Offer Market Growth Opportunities

An important opportunity for the coal mining sector lies in non-power industrial applications, such as steel manufacturing, chemicals, and high-temperature industrial processes. While coal’s role in electricity generation is gradually declining in some regions, demand for metallurgical coal used in blast furnaces and other industrial feedstocks remains resilient. For example, in 2024, non-power steam coal and lignite accounted for around 23% of total coal consumption, with growth concentrated in emerging economies. Expanding industrial activity in regions such as Southeast Asia and South Asia can sustain demand for coal in sectors, including steelmaking and chemical production, partly offsetting declines in power-sector consumption. Diversifying demand sources beyond power generation presents a strategic opportunity for coal producers to extend market relevance in the near- to mid-term.

MARKET CHALLENGES

Renewable Energy Penetration and Fossil Fuel Displacement to Pose a Critical Challenge to Market Growth

A key challenge for the coal mining market is the rapid penetration of renewable energy sources, which are increasingly displacing coal in electricity generation. In the first half of 2025, global renewable generation (primarily wind and solar) surpassed coal for the first time, reflecting surging solar output and expanding wind capacity. As renewables capture a larger share of electricity demand growth, coal plants are operating less frequently, particularly in advanced economies. This trend undermines long-term demand for thermal coal and pressures coal producers to adapt to shifting energy mixes. The structural shift toward low-carbon energy technologies poses a fundamental challenge for the coal mining industry’s growth prospects, particularly in markets with aggressive decarbonization policies.

SEGMENTATION ANALYSIS

By Mining Method

Surface Mining Segment Dominated Due to Its Low Cost Structure

Based on the mining method, the market is divided into surface mining and underground mining.

The surface mining segment accounted for the largest share of the coal mining market at 58.84% in 2025. This growth is driven by its lower cost structure, higher productivity, and suitability for large, shallow coal reserves. This method dominates in regions such as North America, Latin America, Australia, and parts of the Asia Pacific, where extensive open-pit operations (e.g., Powder River Basin in the U.S. and major coal basins in Indonesia and Colombia) enable high-volume extraction. Surface mining benefits from economies of scale, mechanization, and lower labor intensity, making it the preferred approach for thermal coal used in power generation. Its market share is further supported by faster development timelines and comparatively lower safety risks versus underground mining, although environmental and land-use concerns increasingly influence project approvals.

The underground mining segment is anticipated to rise with a CAGR of 2.82% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Grade

Excessive Demand for Good Quality & Economical Coal Boosted High-Grade Coal (Bituminous) Segment Growth

Based on grade, the market is segmented into low-grade coal (lignite), medium-grade coal (sub-bituminous), high-grade coal (bituminous), and ultra-high-grade coal (anthracite).

High-grade coal (bituminous) accounted for the largest coal mining market share at 55.44% in 2025, as it is extensively used in both power generation and steel manufacturing, particularly as metallurgical coal. Strong industrial demand, especially from steel production in the Asia Pacific, supports its leading market position. While thermal bituminous coal faces pressure from clean energy transitions, metallurgical coal demand continues to anchor its share in the global coal mix.

The ultra-high-grade coal (anthracite) segment is projected to grow at a CAGR of 3.54% over the forecast period.

- By End User

The Existence of Coal-based Power Generation from Earlier Times Puts Power Generation in a Leading Position

Based on end user, the market is segmented into power generation, steel manufacturing, cement production, chemical & synthetic fuels, paper & pulp, and others.

The power generation segment is one of the largest contributors to the coal mining market, accounting for 65.51% in 2025, as coal remains a key baseload fuel in many emerging economies where electricity demand continues to rise, and grid reliability is critical. A large number of installed coal-fired power plants in countries such as China, India, and several Southeast Asian nations sustains this dominant share. Although renewables are expanding rapidly, coal power plants continue to operate to meet peak demand and support energy security, particularly where alternative fuels are constrained by cost or infrastructure limitations.

In addition, steel manufacturing segment is projected to grow at a CAGR of 3.33% during the study period.

Coal Mining Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Coal Mining Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held a notable share in 2024, valued at USD 603.58 million, and also maintained the second-largest share in 2025, at USD 619.10 million. The market is driven by the presence of leading coal-producing nations, including China, India, Indonesia, and Australia. China alone accounts for more than 50% of global coal production, with output exceeding 4.7 billion tons in 2024, underscoring coal’s central role in electricity generation and industrial activity. India follows with over 1 billion tons, while Indonesia and Australia contribute hundreds of millions of tons annually, much of it for export. Although renewables are growing rapidly in the region, coal remains the foundation of grid power in China and India, and Southeast Asia continues to add coal plants to meet rising electricity demand. Asia Pacific’s dominant share is sustained by economic growth, industrial expansion, and energy infrastructure that still relies heavily on coal.

Australia Coal Mining Market

The Japan coal mining market in 2025 reached a valuation of USD 38.24 million, accounting for roughly 5.05% of global coal mining revenues.

China Coal Mining Market

China’s coal mining market is projected to be one of the largest worldwide, with 2025 revenues valued at USD 403.53 million, representing roughly 53.34% of global coal mining sales.

India Coal Mining Market

The Indian market in 2025 was valued at USD 94.78 million, accounting for roughly 12.53% of global Coal Mining revenues.

North America

North America held a notable share in 2025, accounting for USD 42.62 million. The region’s coal market has been growing slowly as utilities retire coal-fired plants in favor of natural gas and renewables. For example, U.S. coal production fell from about 996 million tons in 2008 to ~464 million tons in 2024, reflecting a long-term shift away from thermal coal for electricity. Industrial uses such as steelmaking and cement continue to support demand for metallurgical and sub-bituminous coal, but their scale is insufficient to offset losses in power generation. Canada’s smaller output is concentrated in metallurgical grades for export. North America’s share is declining, pressured by environmental regulations, plant retirements, and competition from cheaper, cleaner fuels.

U.S. Coal Mining Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was valued at USD 39.05 million in 2025, accounting for roughly 5.16% of global Coal Mining sales.

EUROPE

Europe is projected to record a growth rate of 1.50% over the coming years. The region reached a valuation of USD 61.91 million in 2025. Europe’s coal mining market is driven by aggressive decarbonization policies and the planned phase-out of coal-fired power plants across many EU countries. Germany, once a major coal producer, plans to end coal use for electricity by 2030, and nations such as France and the U.K. have already closed most of their coal plants. European coal production has fallen from over 900 million tons in the early 1990s to under 100 million tons in recent years in the EU alone. Despite this decline, some Eastern European and Balkan countries still mine coal for domestic electricity and heating. Russia remains Europe’s largest producer, though its export focus and geopolitical tensions have altered trade flows. Overall, coal’s market share in Europe continues to shrink as renewables and natural gas replace coal.

Russia Coal Mining Market

The Russia coal mining market in 2025 was valued at USD 30.11 million, representing roughly 3.98% of global Coal Mining revenues.

Germany Coal Mining Market

Germany’s coal mining market recorded a valuation of USD 10.68 million in 2025, equivalent to around 1.41% of global Coal Mining sales.

Rest of the World

The rest of the world region is expected to witness moderate growth in this market space during the forecast period. It reached a valuation of USD 32.95 million in 2025. Colombia is a key contributor in Latin America, producing over 50 million tons annually, mainly for export to North America and Europe. South Africa dominates coal mining in Africa with about 235 million tons per year, supplying domestic power generation and export markets (particularly metallurgical coal). Smaller producers in the Middle East, North Africa, and other parts of Latin America add incremental volumes. While coal’s share in the rest of the world is much smaller than in the Asia Pacific, it remains significant locally due to ongoing demand for electricity and industrial fuel, as well as export linkages. The rest of the world’s coal mining market is less uniform, combining both growing export sectors and domestic energy needs.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Higher-Quality cable management solutions by Key Players to Propel Market Growth.

Leading players in the coal mining market include Coal India Limited, China National Energy Group, China Shenhua Energy, Peabody Energy, and SUEK. These companies have been focusing on industry standards, reliable coal supply to support national energy security, and core industries such as power generation and steel manufacturing. These companies operate extensive mining portfolios and prioritize production stability and capacity utilization, even amid volatile demand and pricing environments. Coal India Limited (CIL), one of the world’s largest coal producers and a key representative of major coal mining players, demonstrates the industry's efforts to enhance operational efficiency, ensure energy security, and pursue sustainability while meeting national demand. In FY 2024–25, CIL sustained high output, producing 781 million tons of coal, reflecting resilience and scale in supply operations, which accounted for most of India’s domestic coal output amidst rising energy requirements.

LIST OF KEY COAL MINING COMPANIES PROFILED

- Coal India Limited (India)

- China National Energy Group (China)

- China Shenhua Energy (China)

- Shaanxi Coal and Chemical Industry Group (China)

- Yankuang Energy Group (China)

- SUEK (Siberian Coal Energy Company) (Russia)

- Peabody Energy (U.S.)

- Arch Resources (U.S.)

- PT AlamTri Resources (Adaro Energy) (Indonesia)

- Exxaro Resources (South Africa)

- Whitehaven Coal (Australia)

- Yancoal Australia (Australia)

- Core Natural Resources (U.S.)

- Alpha Metallurgical Resources (U.S.)

- Bogatyr Coal (Kazakhstan)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Coal India Ltd announced the reopening of 32 previously closed mines and the launch of up to five new opencast operations to meet rising domestic energy demand. These revitalized mines aim to boost output and reduce reliance on imports. Coal India continues to partner with private firms to achieve efficiency gains and scale production.

- June 2025: Central Coalfields Ltd (CCL), a Coal India subsidiary, announced plans to bring two new coal mines into production within the fiscal year. The Kotre Basantpur and Chandragupt projects are expected to add 10–12 million tons annually, boosting capacity. This expansion aligns with targets to improve overall output.

- May 2025: Glencore reorganized all its coal assets into a single Australian-based unit, combining its domestic and international coal holdings. The consolidation aimed to improve operational efficiency, reduce costs, and streamline management across multiple coal mines. This move reflects a strategic focus on maintaining a profitable coal portfolio while addressing investor concerns about coal exposure.

- February 2025: Gujarat Mineral Development Corporation (GMDC) achieved key clearances for its Baitarni-West coal mine in Odisha, targeting 15 million tons per annum production. The project included the appointment of a mining development operator and environmental approvals. This positions GMDC to expand its coal portfolio beyond lignite mining into higher-grade coal production.

- January 2025: The Adani Group commenced operations at the Gare-Palama Sector II coal block in Chhattisgarh, ramping up domestic coal production. This development supports power generation for Maharashtra and reduces dependence on imported coal. The project also includes investments in modern mining equipment and safety measures.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 2.40% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Mining Method, Grade, End User, and Region |

|

By Mining Method |

· Surface Mining · Underground Mining |

|

By Grade |

· Low-Grade Coal (Lignite) · Medium-Grade Coal (Sub-bituminous) · High-Grade Coal (Bituminous) · Ultra-High-Grade Coal (Anthracite) |

|

By End User |

· Power Generation · Steel Manufacturing · Cement Production · Chemical & Synthetic Fuels · Paper & Pulp · Others |

|

By Region |

· North America (By Mining Method, By Grade, By End User, and Country) o U.S. (By End User) o Canada (By End User) · Europe (By Mining Method, By Grade, By End User, and Country/Sub-region) o Poland (By End User) o Germany (By End User) o Russia (By End User) o Rest of Europe (By End User) · Asia Pacific (By Mining Method, By Grade, By End User, and Country/Sub-region) o China (By End User) o India (By End User) o Australia (By End User) o Southeast Asia (By End User) o Rest of Asia Pacific · Rest of the World (By Mining Method, By Grade, By End User) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 756.58 million in 2025 and is projected to reach USD 942.72 million by 2034.

In 2025, the Asia Pacific market value stood at USD 619.10 million.

The market is expected to grow at a CAGR of 2.40% over the forecast period of 2026-2034.

By mining method, the surface mining led the market in 2025.

Electricity demand growth and coal consumption are the key factors driving the market.

Coal India Limited, China National Energy Group, China Shenhua Energy, Peabody Energy, and SUEK Company are the major players in the global market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 1888

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us