Coating Resins Market Size, Share & Industry Analysis, By Resins (Acrylic, Alkyd, Polyurethane, Epoxy, Polyester, and Others), By Formulating Technology (Water-based, Solvent-based, Powder, and Others), By End-use Industry (Architectural Coatings, General Industrial Coatings, Powder Coatings, Wood Coatings, Automotive OEM Coatings, Automotive Refinish Coatings, Protective Coatings, Packaging Coatings), and Regional Forecast, 2026-2034

Coating Resins Market Size and Industry Overview

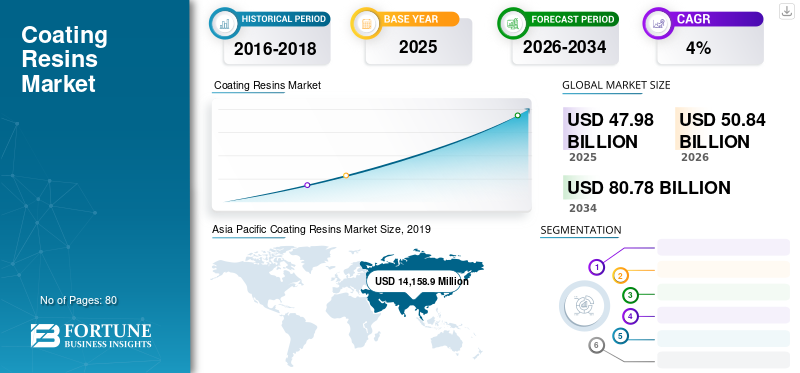

The global coating resins market size was valued at USD 47.98 billion in 2025. The market is projected to grow from USD 50.84 billion in 2026 to USD 80.78 billion by 2034, exhibiting a CAGR of 5.96% during the forecast period. Asia Pacific dominated the coating resins market with a market share of 42.01% in 2025.

Coating Resins are polymer compounds that are used in the manufacturing of coatings as primary components. These advanced materials serve as protective layers and are exclusively used for corrosion, toughness, weather, and stain resistance.

Due to the rising end-use industries and technological developments, the market is experiencing a high growth rate. Also, the economic growth in developing countries and strict environmental regulations are set to drive the market. The growing automotive manufacturing is projected to drive the market significantly during the forecast period. Additionally, the high economic growth in developing countries, rising investment in infrastructure, strict environmental legislation, surging buying power, and increasing demand for green and environmentally friendly coatings would propel growth.

Download Free sample to learn more about this report.

Coating Resins Market Key Takeaways

- 2025 Market Size: USD 47.98 Billion

- 2026 Market Size: USD 50.84 Billion

- 2034 Forecast Market Size: USD 80.78 Billion

- CAGR: 5.96% from 2026–2034

- Asia Pacific dominated the coating resins market with a 42.01% share in 2025.

- The acrylic segment held the largest share by resin type in 2025.

- The water-borne segment accounted for the leading share by formulating technology in 2025.

Asia Pacific

Asia Pacific led the global market with a 42.01% share and a market size of USD 14.16 billion in 2025.

Europe

Europe is expected to witness steady growth driven by infrastructure investments and increasing adoption of powder coatings.

North America

North America is projected to expand at a moderate pace due to rising industrial manufacturing and automotive demand.

U.S.

Growing construction activity and automotive sales continue to support coating resins demand.

Japan

Strong automotive production and industrial manufacturing activities contribute to market growth.

Read More

Coating Resins Market LATEST TRENDS

Download Free sample to learn more about this report.

Focus of Manufacturers on Developing Sustainable Products is a Current Trend

Sustainability continues to grow within the coatings industry. Producers of resin, pigments, additives, and final coating formulations have increased their focus on developing greener processes that use lesser energy, as well as generate fewer waste and emissions. Formal initiatives were developed by the most successful organizations to promote awareness, foster creativity, and facilitate the ongoing development and enhancement of sustainable operations. Green manufacturing not only helps the environment but also has a significant and observable effect on productivity and profitability. The principles of green chemistry focus on efficacy and hazard avoidance as a way of creating sustainable processes. The usage of energy goes hand in hand with carbon dioxide emissions and so, decreasing the amount of energy is a major objective. Asia Pacific witnessed a coating resins market growth from USD 13,462.2 million in 2018 to USD 14.159 million in 2019.

Another primary target of many producers in the industry is to improve the overall resource usage. For several companies in the coating resins sector, reducing the usage of energy is a key priority for the development and introduction of greener manufacturing processes. Generating more value from fewer resources is important for both the resins manufacturers and coating providers. From a manufacturing perspective, that means using more energy-efficient raw materials and products for their operations. It would ensure an improved energy quality, thereby enhancing fuel mix for energy-intensive operations and refining the formulation to minimize the footprint of the product.

- In 2019, Royal DSM announced the launch of Decovery SP-2022 XP, a new bio-based self-matting resin that will take ultra-matt flooring finishes to new heights in terms of aesthetic and practical efficiency, ease of application, and sustainability.

DRIVING FACTORS

Increasing Use of Liquid and Bio-based Epoxy Resin to Propel Growth

Different resins in the epoxy family are widely used in electrodeposition (ED) coatings and industrial coatings, particularly in the transport, industrial maintenance, and marine sectors. In powder coatings, epoxy resins are also commonly used. The development of high solids and ultra-high solids formulations using liquid epoxy resin is gaining more popularity nowadays. For achieving 100% solid epoxy formulations used as concrete surfaces, tank linings, and other similar applications, liquid epoxy resin is utilized. It is often augmented with phenoxy and novolac resins to improve their performance and characteristics. The performance of waterborne epoxy resin technology has increased and hence it is enabling higher use. Only a limited share of technology was achieved because of the substantial use of coatings made of metal.

In recent years, increasing environmental and economic issues, as well as the uncertainty that accompanies limited petrochemical resources, have triggered a rapid surge in research and development activities to develop bio-based polymers. Manufacturers are trying to substitute polymers derived from naturally occurring feedstocks with petroleum-based materials to fulfil the industrial need for environmental-compatible processes and goods that promote sustainable growth. Additionally, developing safer methods of polymer production, including the use of safer building blocks and additives, are of great interest. Commercial epoxy resins are commonly synthesized from DGEBA, cycloaliphatic epoxies, or diglycidyl ethers of Novolac resins. Due to their low cost, environmentally friendly nature, and capacity to be easily epoxidized, renewable natural resources have made it possible to act as building blocks for polymers.

Rising Demand for Polyurethane Resins to Boost Growth

Polyurethane coatings, especially 1K, 2K, or occasionally 3K are widely used in the automotive OEMs, transportation, automotive refinish, wood, industrial finishes, decorative coatings, and severe-service marine and high-performance industrial segments. The usage of polyurethane resins has been growing over the past several years due to their beneficial performance properties and their ability to be used in lower VOC formulations. An important and flourishing sub-segment of polyurethanes in the U.S. is 2K polyurea. To comply with the increasingly stringent VOC requirements, polyurethane water-borne dispersions (PUDs) are being increasingly developed. They are used to formulate single-component coatings with improved abrasion resistance, compared to water-borne acrylics. They can also be combined with other water-borne resins to meet cost targets and performance needs.

All polyurethane coating resins contain moderate levels of volatile organic compounds (VOCs). There are also no volatile organic compounds (VOCs) in 100% urethane solids. In lower solid coatings, the reduction in thickness between dry film thickness (DFT) and wet film thickness (WFT) is due to the evaporation of solvents into the environment as the coatings recover. In enclosed spaces, these evaporating solvents (VOCs) can create toxic conditions and employee health hazards. This makes 100% solids desirable due to the shortage of VOCs. A further advantage with 100% solids is fast drying periods. Drying times are also so low that the coatings are sprayed by plural component systems, ensuring that these coatings are not combined before the gun is sprayed. In a couple of hours, they can be easily used by people.

RESTRAINING FACTORS

Increasing Number of Stringent Regulations on VOC May Hinder Growth

Alkyds are mostly used on a global basis in nearly every category of end-use coatings. But, the use of alkyd resins is gradually decreasing, particularly in North America and Europe, as VOC limits continue to decline. The demand has switched to other resin forms for water-based and higher-solids formulations. New water-based alkyd systems are being introduced in the market, partly because of the increasing interest in resins produced with a higher content of renewable resources. The first alkyds produced were solvent-based, but the excess of solvents found in these coatings proved detrimental to human health and the environment.

Alkyds are typically organic and solvent-dependent, using up to 50% of the solvents based on volatile organic carbon (VOC). Due to their ease of application and high gloss characteristics, these resins are commonly used for coatings. In particular, alkyds have seen relatively little conversion to water-based or lower VOC alternatives, largely due to their dry time, shine, adhesion, and differences in corrosion resistance efficiency. Due to their low cost, ease of use, and high flexibility, solvent-borne alkyds continue to remain popular.

Nevertheless, the amount of alkyd resin is expected to decrease by two percent per year, primarily due to the loss of share of coating technologies that can provide better efficiency at lower VOCs. Solvent-borne coatings face increasingly stringent controls on VOCs. Diminishing their VOC quality while retaining their low cost and high efficiency is a struggle. Solvent-based alkyd coatings, however, lead to the release of VOCs, which typically have harmful impacts on human health and the atmosphere.

With stricter VOC legislation, to comply with these regulations, the coatings industry is facing tremendous pressure to reduce the VOC content of solvent-based coatings. Solvent-based alkyds coatings have lost their market share to other competing technologies, such as water-borne, powder and UV-curable coatings, due to their high VOC content. It is important to lower their VOC levels in order to satisfy the stringent VOC criteria and to retain excellent efficiency for reclaiming the market share of these coatings.

Coating Resins Market SEGMENTATION Analysis

By Resins Analysis

Acrylic Segment to Hold a Significant Share of the Global Market

Based on resins, the coating resins market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and others. The acrylic segment held a major market share due to the growing use of ceramic in the biomedicine industry. Resins or binders hold all components of the coatings together. Coating resins consist of polymers that are chosen on the basis of the physical and chemical properties desired in the finished product. Acrylics produce a shiny, hard finish with good resistance to chemicals and weather. Naturally, solvent-borne coatings are the biggest field of applications for acrylic resins made by solution polymerization.

Alkyds are relatively low in cost and because of their versatility, they are considered a ‘general purpose’ coating. They are extensively used in many coating systems based on solvents. They are a type of polyester made from polyols, acids, and vegetable oils. Epoxies provide excellent water resistance, superior chemical resistance, and abrasion resistance. However, if exposed to ultraviolet light, they can lose their gloss. Polyurethanes combine high gloss and flexibility with resistance to chemical stains and show excellent water resistance.

By Formulating Technology Analysis

Water-borne Segment to Lead Because of its Low VOC Content

In terms of formulating technology, the market is segmented into water-based, solvent-based, powder, and others. The water-borne segment constituted the primary market share. During application, these resins reduce VOC emissions, are easier to clean, can lower the risk of fire, and result in reduced worker exposure to organic vapors. This technology also lowers the cost of the coating process. They are beneficial for coating manufacturers, providing them with cost-effective and favorable payback time for any investment required to adapt the line of application for the use of water-borne resins. Key properties of these resins can be brought to a level that satisfies the product demand, such as hardness and resistance to water and chemicals.

Solvents resins are used for transporting the coating solids to the painted part. They are also added to coatings to aid in their application by reducing viscosity so that the coating can be applied easily. Solvents are a significant source of environmental concern in coating applications because hazardous air pollutants (HAPs) and VOCs are released as curing occurs.

By End-use Industry Analysis

To know how our report can help streamline your business, Speak to Analyst

Architectural Coatings Segment to Dominate Fueled by Rising Infrastructure Spending

On the basis of the end-use industry, the coating resins market is classified into architectural coatings, general industrial coatings, powder coatings, wood coatings, automotive OEM coatings, automotive refinish coatings, protective coatings, packaging coatings, and others. The architectural coatings segment is expected to be driven by the rising infrastructure spending and the increasing demand for high-performance and durable coating materials for construction components. These coatings are used to protect metallic sections of tanks, radiators, fences, and metal furniture from corrosion & rust.

An anticipated rise in infrastructure construction activities and an expanding middle-class population are creating lucrative opportunities for the architectural industry. The increasing use of industrial coatings in general industries is rising due to its properties such as high levels of corrosion resistance, chemical resistance, UV degradation, or weather ability with a cost-saving reduction. High durability, chemical resistance, sustainability, and scratch resistance, including low VOC and water-borne systems, are some of the key drivers of the automotive coating industry, both in OEM and refinishing. The rising use of industrial coatings, automotive coatings, and others is anticipated to increase the demand for these products.

REGIONAL ANALYSIS

Asia Pacific

Asia Pacific Coating Resins Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The market size in Asia Pacific stood at USD 14,158.9 million in 2025. The region dominated the market in 2019 and is likely to retain its position during the forecast period. The demand in the region is strongly influenced by government subsidies, automotive production, construction activities, interest rates, and consumer spending, all of which are the important components of GDP.

Europe

In Europe, developments in the oil & gas sector and infrastructural investments are expected to aid growth. Also, the use of powder coatings is expected to surge as a result of technological advancements made in this sector over the last few years. It will also grow because of the increased awareness of their environmental credentials.

North America

The recovery of the manufacturing sector in North America is projected to expand at a moderate pace. The region is experiencing a high demand because of the growing industrial manufacturing. Increasing automotive sales, accident rates, and rising construction activities are also anticipated to fuel the market growth in this region.

Latin America

The major multinational resins firms have a strong presence in Latin America and they would continue to invest in the market through organic strategic acquisitions. The increasing car ownership due to the higher spending power and living standards, as well as the presence of poor quality roads and frequent traffic accidents, is likely to boost the demand for automotive refinish coatings in the region.

To know how our report can help streamline your business, Speak to Analyst

Middle East & Africa

In the Middle East & Africa, the demand for white goods is expected to rise due to the lower interest rates. It is further set to create several opportunities for industrial coatings, which, in turn, would fuel the market growth. Apart from that, numerous resins manufacturers are creating better awareness of the benefits of using the right resins products for different applications, such as automotive, architecture, packaging, and others. The product demand is set to accelerate because of several novel trends in industrial production, construction and infrastructure spending, energy prices, and consumer spending.

KEY INDUSTRY PLAYERS

Key Companies to Strengthen Their Market Shares by Adopting Strategic Business Plans

The market is fragmented in nature with the presence of various major players and some global and regional small-and medium-sized players worldwide. Many companies are competing on the basis of the offered product quality and the technology used for the manufacturing of coating resins. Major players are involved in mergers and acquisitions, developing infrastructure, expanding their manufacturing facilities, investing in research and development facilities, and are looking for opportunities to integrate vertically across the value chain.

BASF SE, ALLNEX NETHERLANDS B.V., Covestro AG, DIC CORPORATION, Dow Chemical, and Arkema are some of the key players in the global market. The competition is anticipated to intensify as the leading players are actively engaged in expanding their product ranges, as well as global and regional footprint.

LIST OF KEY PLAYERS PROFILED IN COATING RESISNS MARKET:

- BASF SE (Ludwigshafen, Germany)

- ALLNEX NETHERLANDS B.V. (Bergen Op Zoom, The Netherlands)

- Covestro AG (Leverkusen, Germany)

- Wacker Chemie AG (Munich, Germany)

- Dow (Michigan, U.S.)

- Sherwin-Williams (Ohio, U.S.)

- Evonik (Essen, Germany)

- Mitsubishi Chemical Corporation (Tokyo, Japan)

- TORAY INDUSTRIES, INC. (Tokyo, Japan)

- Solvay (Brussels, Belgium)

- Eastman Chemical Company (Tennessee, U.S.)

- DIC CORPORATION (Tokyo, Japan)

- Hexion (Ohio, U.S.)

- Perstorp (Malmö, Sweden)

- DSM (Heerlen, Netherlands)

- Arkema (Colombes, France)

- Other Key Players

KEY INDUSTRY DEVELOPMENTS:

- July 2020 – Engineered Polymer Solutions (EPS) launched the EPS 2400 series in North America. It is a new line of six waterborne acrylic resins used by wood coating formulators to build high-performance solutions for cabinetry, furniture, and flooring applications in industrial applications.

- February 2019 – Arkema inaugurated a new first-class polyester resin production facility in Navi Mumbai, Maharashtra. A dedicated laboratory to provide both application development and technical support is also included in this facility. It will help Arkema provide better service to customers across India, as well as the Gulf Region and neighboring countries in the fast-rising powder coating industry.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The coating resins market research report provides a detailed analysis of the market and focuses on crucial aspects such as leading companies, products, and applications. Also, it offers detailed insights into market trends and highlights vital industry developments. In addition to the factors mentioned above, it encompasses various factors that have contributed to the growth of the market over recent years. This report also includes historical data & forecasts revenue growth at global, regional, and country levels, and analyzes the latest dynamics and opportunities in the industry.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Million) and Volume (Kilo Tons) |

|

Segmentation |

Resins; Formulating Technology; and End-use Industry |

|

By Resins |

|

|

By Formulating Technology |

|

|

By End-use Industry |

|

|

By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 47.98 billion in 2025 and is projected to reach USD 80.78 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 14,158.9 million.

Registering a CAGR of 5.96%, the market will exhibit steady growth in the forecast period (2026-2034).

The architectural coatings segment is expected to be the leading segment in this market during the forecast period.

The growing construction industry is the key factor driving the market.

BASF SE, ALLNEX NETHERLANDS B.V., Covestro AG, DIC CORPORATION, and Arkema are the major players in the global market.

Asia Pacific dominated the market in terms of share in 2025.

The high demand for green coating resins is expected to drive the adoption of these products.

- 2021-2034

- 2025

- 2021-2024

- 80

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us