Cobalt Metal Market Size, Share & Industry Analysis, By Application (Superalloys, Hard Metals, Magnets, and Others), By End-Use Industry (Aerospace, Industrial/Mining, Defense, Automotive, and Others), and Regional Forecast, 2025-2032

Cobalt Metal Market Size and Future Outlook

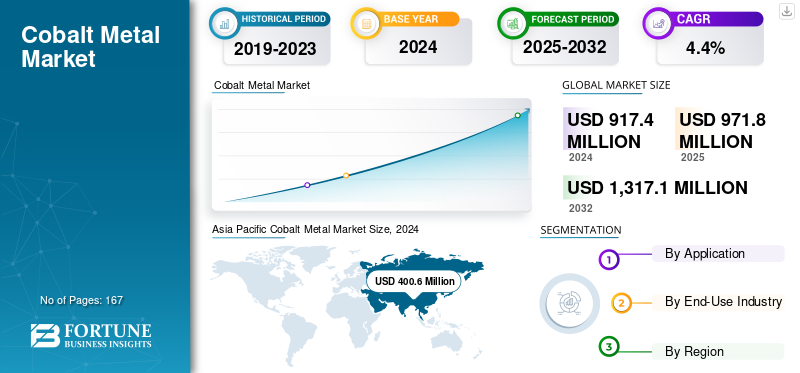

The global cobalt metal market size was valued at USD 917.4 million in 2024. The market is projected to grow from USD 971.8 million in 2025 to USD 1,317.1 million by 2032, exhibiting a CAGR of 4.4% during the forecast period. Asia Pacific dominated the global cobalt metal market with a market share of 43.66% in 2024.

Cobalt metal is a critical metallurgical material used primarily in high-performance alloys and engineered systems where strength, heat resistance, and reliability are essential. It serves as a core alloying element in superalloys for aerospace turbines, performance-critical industrial components, cemented carbides, and SmCo permanent magnets. Cobalt’s ability to deliver exceptional mechanical stability, high-temperature performance, and magnetic integrity have made them better than alternative metals. Alternative metals have lower efficiency and durability. Its unique role in enabling advanced aerospace, cutting tools, energy infrastructure, and defense technologies ensures sustained demand for this refined metal across global industrial supply chains.

The market is led by Glencore, CMOC Group, Jinchuan Group, Umicore, and Eurasian Resources Group (ERG). Their leadership is built on large-scale cobalt mining and refining capacities, strong integration into metallurgical and alloy-grade cobalt supply chains, and established relationships with key manufacturers in the aerospace, tooling, and magnet sectors. Continuous investments in refining upgrades, responsible sourcing, metal recovery, and supply-chain traceability further reinforce their competitive positions, enabling these players to influence the metal’s flows, pricing, and also influence long-term industry developments.

Download Free sample to learn more about this report.

COBALT METAL MARKET KEY TAKEAWAYS

- 2024 Market Size: USD 917.4 million

- 2025 Market Size: USD 971.8 million

- 2032 Forecast Market Size: USD 1,317.1 million

- CAGR: 4.4% from 2025–2032

- Asia Pacific dominated the cobalt metal market with a 43.66% share in 2024.

- The aerospace segment is projected to hold a 49.2% share in 2025.

- The superalloys segment accounted for the largest market share in 2024.

Asia Pacific

Asia Pacific reached USD 378.5M 2023 and USD 400.6M 2024, driven by EV growth, battery manufacturing, and strong electronics and alloy industries.

Europe

Europe is projected at USD 238.5M 2025, driven by gigafactory expansion, strict raw material policies, and rising battery demand.

North America

North America is projected at USD 208.5M 2025, driven by EV expansion, aerospace demand, and rising cobalt recycling and refining investments.

U.S.

U.S. is projected at USD 166.6M 2025, driven by EV adoption, grid storage growth, and industrial alloy demand.

Japan

Japan is included in Asia Pacific growth, driven by battery supply chains and advanced electronics manufacturing.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Usage of Superalloys in Aerospace & Defense Industry Fuels Market Demand

The expanding aerospace and defense industry remains a key force driving consumption. Cobalt’s high-temperature strength, corrosion resistance, and ability to maintain structural integrity make it indispensable for turbine blades, jet engines, and critical defense components.

- According to SIPRI, global military expenditure reached USD 2.44 trillion in 2023, marking a 6.8% rise from the previous year.

As governments modernize fleets and commercial aviation rebounds, manufacturers are intensifying procurement of cobalt-based alloys, directly reinforcing the metal’s strategic importance in the industrial value chain.

MARKET RESTRAINTS:

Supply Concentration and Regulatory Pressures Limit Market Expansion

Cobalt metal market growth faces headwinds from limited mining flexibility and rising environmental scrutiny. The majority of cobalt production originates as a by-product of copper and nickel mining, making output dependent on other commodity cycles. Regulatory tightening on mining practices and sustainability standards further complicates capacity expansion and project approvals.

- According to the U.S. Geological Survey (USGS), the Democratic Republic of the Congo (DRC) accounted for approximately 56% of global cobalt mine production in 2023, underscoring the market’s high geographic concentration and exposure to regional risks. This dependence on a single source heightens supply vulnerability, with political instability, logistical constraints, and regulatory shifts in the DRC posing potential challenges to long-term cobalt availability and pricing stability across global end-use industries.

MARKET OPPORTUNITIES:

Advancing Alloy Technologies Creates New Avenues for Market Demand

The growing focus on high-performance materials across the aerospace, energy, and industrial sectors is opening up new growth opportunities. Its exceptional heat resistance and mechanical strength make it vital in next-generation superalloys, additive manufacturing powders, and wear-resistant coatings. As industries seek lighter yet stronger materials, cobalt-based alloys are gaining ground in both design innovation and performance optimization.

- According to Airbus, global aircraft deliveries are expected to exceed 40,000 new planes by 2042, supported by rising air traffic and fleet modernization. Similarly, the International Energy Agency (IEA) notes an increasing demand for high-temperature alloys in turbine and power generation equipment.

This shift toward advanced metallurgy and material efficiency positions cobalt as a key enabler of industrial innovation, sustaining long-term growth potential beyond traditional applications.

MARKET CHALLENGES:

Uneven Refining Distribution Deters the Market Development

The market continues to face supply pressure due to uneven refining distribution and limited secondary recovery. While mined feedstock remains concentrated in select African countries, most cobalt refining capacity is located overseas, constraining supply flexibility for industrial and alloy applications. This imbalance heightens vulnerability to logistical and policy disruptions, particularly for manufacturers that rely on consistent metal quality.

- According to the Cobalt Institute, over 34,000 tonnes of cobalt were lost in global electronic waste in 2022, representing nearly one-sixth of the total mined supply that year. Such material leakage highlights the gap between primary output and recoverable resources, reinforcing long-term challenges in ensuring sustainable, traceable, and reliable cobalt metal availability.

COBALT METAL MARKET TRENDS:

Growing Focus on Recycling and Sustainable Sourcing Shapes Market Direction

An increasing emphasis on circular economy practices is reshaping the market. Producers and end-users are investing in closed-loop recycling systems and traceable sourcing to reduce their reliance on mined materials and align with global sustainability targets. This trend is particularly evident among alloy and aerospace manufacturers seeking to secure ethical and consistent cobalt supply while lowering carbon intensity across their production chains.

- According to the Cobalt Institute, recycled cobalt accounted for nearly 12% of the total supply in 2024, is expected to rise steadily as industrial recovery programs and scrap collection improve. The integration of recycling into mainstream sourcing strategies is gradually transforming cobalt from a high-risk critical metal into a more resilient and responsibly managed resource.

Download Free sample to learn more about this report.

Segmentation Analysis

By Application

Requirement for High-Performance Materials Sustains the Dominance of Superalloys

On the basis of application, the market is classified into superalloys, hard metals, magnets, and others.

The superalloys segment accounted for the most significant cobalt metal market share in 2024. Superalloys remain the leading application, supported by their essential role in components exposed to extreme temperature and mechanical stress. Cobalt’s ability to enhance strength, oxidation resistance, and durability makes it a critical alloying element in turbine engines, gas turbines, and other advanced industrial systems. The segment’s continued prominence reflects the expanding need for reliable, high-performance materials across aerospace, energy, and heavy-engineering sectors.

To know how our report can help streamline your business, Speak to Analyst

By End-Use Industry

Essential Role of Superalloys is Driving the Demand in the Aerospace End-Use Industry

In terms of end-use industry, the market is categorized into aerospace, industrial/mining, defense, automotive, and others.

The Aerospace segment accounted for the largest share in 2024. In 2025, the segment is anticipated to dominate with a 49.2% share. The aerospace industry remains the largest consumer, primarily due to cobalt metal’s essential role in high-performance superalloys. These superalloys are used in turbine engines and critical structural components. Cobalt’s superior thermal strength, corrosion resistance, and fatigue durability make it indispensable in aircraft manufacturing, ensuring reliability in extreme operating environments.

- According to Boeing’s 2024 Commercial Market Outlook, global aircraft demand is projected to record 43,975 new deliveries by 2043, reflecting strong replacement needs, expanding fleets, and sustained growth in air travel. This continued expansion highlights the aerospace sector’s pivotal role in driving demand for advanced materials, such as cobalt-based superalloys, used in engines and turbine components.

The automotive segment is expected to grow at a CAGR of 5.4% over the forecast period.

Cobalt Metal Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Cobalt Metal Market Size, 2024 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2023, valued at USD 378.5 million, and also took the leading share in 2024 with USD 400.6 million. Asia Pacific has the core demand and is the processing hub for cobalt metal, driven by large-scale battery manufacturing, strong growth in electric vehicles, and robust electronics and alloy industries. China, Japan, South Korea, and India are the key players in the battery-grade cobalt market, with integrated supply chains that span from precursors to cathode materials. Rising EV penetration and energy storage installations are reshaping cobalt consumption with batteries steadily crowding out legacy uses in hard metals and chemicals. In 2025, the China market is estimated to reach USD 139.9 million, supported by its dominant role in cobalt refining and active investments in recycling and closed-loop supply. Concentrated refining capacity and exposure to imported feedstock, however, continue to underline cobalt supply chain challenges and the need for diversification.

- According to the China Association of Automobile Manufacturers (CAAM), China produced 31.28 million vehicles in 2024, including over 10 million new-energy vehicles, underscoring its pivotal role as the world’s largest automotive manufacturing base and a major driver of demand.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe is expected to experience significant growth in the coming years. During the forecast period, the European region is projected to record a growth rate of 3.4% and reach a valuation of USD 238.5 million in 2025. Europe’s cobalt metal demand is shaped by the rapid expansion of lithium-ion gigafactories, high-performance automotive and industrial applications, and stringent environmental and traceability requirements. The region is building a more resilient supply chain under the EU Critical Raw Materials Act, which prioritizes secure sourcing, local processing, and higher recycling rates for critical minerals, including cobalt. Alongside battery plants in Germany, France, and the Nordic countries, aerospace alloys and specialized chemicals continue to support a diversified cobalt metal industry even as clean energy technologies heavily drive overall growth. Backed by these factors, the U.K. is anticipated to record a valuation of USD 34.6 million, Germany USD 77.4 million, and France USD 54.6 million in 2025, with further upside from recycling and secondary supply.

- The EU’s Critical Raw Materials Act formally recognizes cobalt as a strategic raw material and targets higher domestic extraction, processing, and recycling capacities to reduce import dependence and improve cobalt supply chain resilience.

North America

The market in North America is estimated to reach USD 208.5 million in 2025. North America’s demand is sustained by the acceleration of EV capacity, a large vehicle fleet transitioning toward electrification, and established consumption in superalloys, aerospace, and defense applications. Policy support through incentives and local content rules is encouraging regional investments in cathode materials, recycling, and refined cobalt production, supporting a more balanced cobalt production–consumption profile for the long term. While the region still relies on imported intermediate products, new projects aim to address cobalt supply chain challenges and mitigate exposure to highly concentrated overseas refining. In 2025, the U.S. market is estimated to reach USD 166.6 million, underpinned by rising demand from passenger EVs, grid-scale storage, and high-performance industrial alloys.

- Analysis from Argonne National Laboratory suggests that U.S. cobalt demand from batteries could multiply several-fold by 2035 under electrification scenarios, reinforcing the strategic importance of securing battery-grade cobalt supply for the regional EV transition.

Latin America

Latin America is expected to reach USD 32.5 million in 2025, driven by industrial expansion and gradual entry into the battery materials ecosystem. While consumption remains moderate, the region is relevant on the resource side due to emerging cobalt mining trends and growing interest in downstream processing. Over time, closer integration with North American supply chains may strengthen the regional demand in Latin America.

Middle East & Africa

The Middle East & Africa are expected to reach USD 67.3 million in 2025, with limited but rising demand linked to automotive industry growth, industrialization, and energy projects. Africa remains central to global cobalt production statistics, with the DRC supplying the majority of mined cobalt. Improving traceability and refining initiatives aim to reduce supply-chain volatility. Gradual increases in infrastructure and industrial activities are expected to support cobalt consumption by end-use sectors.

COMPETITIVE LANDSCAPE

Key Industry Players:

Concentration of Mining and Refining Leaders Shapes Product Supply Dynamics

The cobalt metal market is moderately consolidated, with a small group of mining and refining majors controlling majority high-purity cobalt supply globally. These companies anchor global availability through large upstream assets, vertically integrated refining networks, and long-term relationships with superalloy, hard-metal, and magnet manufacturers. Their focus remains on stable metal output, refining efficiency, and responsible sourcing rather than frequent capacity announcements.

Key players in the global cobalt metal market include Glencore, CMOC Group, Jinchuan Group, Eurasian Resources Group (ERG), and Umicore. Their large-scale mining portfolios, cobalt metal refining capabilities, and integration into critical metallurgical end-uses give them structural influence over global metal flows and pricing. Incremental upgrades in refining processes and traceability frameworks continue to strengthen supply reliability for high-performance applications across aerospace, industrial machinery, and advanced materials.

LIST OF KEY COBALT METAL COMPANIES PROFILED:

- Umicore (Belgium)

- Jinchuan Group Co., Ltd. (China)

- CMOC (China)

- Glencore (Switzerland)

- Huayou Cobalt Co., Ltd. (China)

- Eurasian Resources Group (Luxembourg)

- Freeport-McMoRan (U.S.)

- Vale Base Metals Limited (Canada)

- Sherritt International Corporation (Canada)

- Jervois (Australia)

KEY INDUSTRY DEVELOPMENTS:

REPORT COVERAGE

The global cobalt metal market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2019-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Period | 2019-2023 |

| Growth Rate | CAGR of 4.4% from 2025-2032 |

| Unit | Value (USD Million) and Volume (Tons) |

| Segmentation | By Application, End-Use Industry, and Region |

| By Application |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 917.4 million in 2024 and is projected to reach USD 1,317.1 million by 2032.

In 2024, the market value stood at USD 400.6 million.

The market is expected to exhibit a CAGR of 4.4% during the forecast period.

The superalloys segment led the market by application.

The key factors driving the market are the rising aerospace & defense production fuels the market demand.

Glencore, CMOC Group, Jinchuan Group, Eurasian Resources Group (ERG), and Umicore are some of the prominent players in the market.

Asia Pacific dominated the market in 2024.

Advancing alloy technologies are some of the factors that are expected to favor the product adoption.

- 2019-2032

- 2024

- 2019-2023

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us