Coffee Concentrate Market Size, Share & Industry Analysis, By Type (Caffeinated and Decaffeinated), By Distribution Channel (HoReCa and Retail [Supermarkets/Hypermarkets, Specialty Stores, Convenience Stores, and Online Retail]), By Form (Liquid Concentrate, Frozen Concentrate, and Powdered Concentrate), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

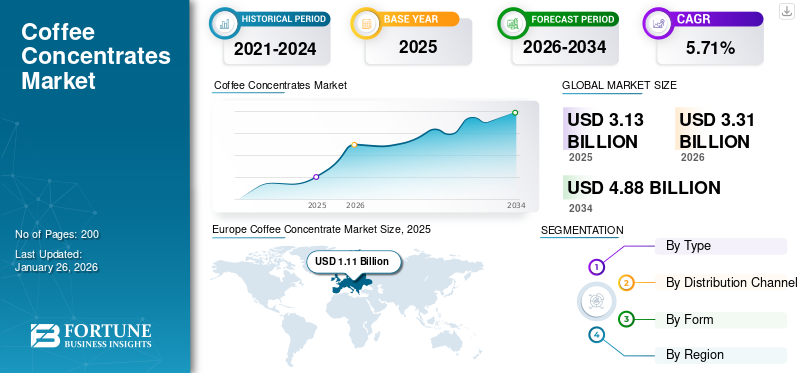

The global coffee concentrate market size was valued at USD 3.13 billion in 2025 and is projected to grow from USD 3.31 billion in 2026 to USD 4.88

billion by 2034, exhibiting a CAGR of 5.71% during the forecast period. Europe dominated the global coffee concentrate market with a market share of 35.46% in 2025.

Coffee concentrate is a highly concentrated liquid soluble brewing coffee which is produced by the cold brew manufacturing process of Arabica and Robusta coffee beans, and is used to make several coffee drinks. Based on variety, caffeine content, and product type, the global market is segmented into different categories targeting diverse consumer preferences for taste intensity and energy levels. The rising global coffee culture, growth of specialty cafés, rapid expansion of ready-to-drink coffee, and rise in demand for premium and craft beverages are driving the global market growth. The global market is witnessing steady growth, driven by the increasing demand for convenient coffee products among busy consumers and foodservice operators. Furthermore, the market is witnessing strong growth driven by the rising demand for quick and ready‑to‑drink beverages with high‑quality coffee and versatile options (pumpkin cold brew coffee concentrate and other versatile coffee concentrates) gaining popularity among consumers all over the globe.

Major players dominated the market including Nestlé S.A., JAB Holding Company, Starbucks Corporation, Keurig Dr Pepper Inc., and JDE Peet’s N.V. These companies lead the value chain with extensive café footprints, premium brand equity, proprietary extraction technologies, and strong retail distribution networks.

Download Free sample to learn more about this report.

Coffee Concentrate Market KEY TAKEAWAYS

- 2025 Market Size: USD 3.13 billion

- 2026 Market Size: USD 3.31 billion

- 2034 Forecast Market Size: USD 4.88 billion

- CAGR: 5.71% from 2026–2034

- Europe dominated the coffee concentrate market with a 35.46% share in 2025.

- The caffeinated segment is projected to account for the largest market share of 80.97% in 2026.

- The liquid concentrate segment is expected to lead the market with a 69.49% share in 2026.

Asia Pacific

Projected to reach USD 0.55 billion in 2026, driven by rising café culture.

North America

Projected to reach USD 0.95 billion in 2026, supported by premium coffee demand.

Europe

Projected to reach USD 1.17 billion in 2026, driven by strong soluble coffee consumption.

U.S.

Projected to reach USD 0.80 billion in 2026, fueled by premium coffee trends.

Japan

Projected to reach USD 0.04 billion in 2026, supported by specialty coffee adoption.

Read More

MARKET DYNAMICS

Market Drivers

Higher Convenience and Economical Nature of Liquid Soluble Coffee Products are Driving Market Growth

The liquid soluble coffee products are highly economical and convenient to use. Furthermore, the rising new product launches and new startups in the market have shown an increasing penetration in global markets with availability at several retail channels, including hypermarkets/supermarkets, convenience stores, specialty stores, and online retail. For instance, in August 2023, Tim Hortons announced the launch of its all-new coffee concentrate products in four new flavors, including medium blend black, birthday cake, cinnamon swirl, and mocha cereal, in all 50 states in the U.S. retail market.

Market Restraints

Higher Availability and Demand of Substitute Products to Restrain Market Growth

The demand for instant powdered coffee options is high in the market, with higher penetration owing to extensive product portfolios of major players, including Nestle, Kraft, and others. Instant powder coffee is available in several retail channels and also in tier-three cities in global markets and has a significant demand in emerging coffee markets, such as India, China, and others. In addition, the rising demand among consumers for coffee and increasing per capita coffee consumption in emerging markets have been driving the demand for instant powdered coffee in the market. Thus, the higher availability of substitute products in the market restrains the coffee concentrate market growth.

Market Opportunities

Omnichannel Retail Expansion and D2C Coffee Subscription Models to Shape the Industry

Omnichannel and e-commerce expansions create significant growth opportunities in the global market by enhancing accessibility, personalization, and sales through integrated digital-physical channels. Brands leverage data analytics for personalized recommendations, click-and-collect, and social platform shopping, while direct-to-consumer (D2C) models enhance margins via quality control and targeted marketing.

- For instance, in January 2025, NESCAFÉ expanded its portfolio with the launch of NESCAFÉ Espresso Concentrate, a first-ever liquid coffee concentrate designed for customizable, café-style iced espresso beverages at home. This innovation targets young consumers, particularly Gen Z and millennials, who favor cold, convenient, and customizable coffee experiences.

Coffee Concentrate Market Trends

Health-Driven Formulations and Sustainable Packaging to Create New Growth Prospects

Low-acid, organic, fair-trade, and sustainably sourced coffee concentrates industry are gaining traction as consumers prioritize digestive wellness and ethical sourcing. Recyclable glass bottles, aluminum cans, and Post-Consumer Recycled (PCR) plastics help brands meet sustainability mandates.

- For instance, in March 2024, Califia Farms transitioned its plant-based cold brew concentrate and other bottled products in the U.S. and Canada to lightweight, fully recyclable PET bottles made from 100% recycled plastic (rPET). This switch to 100% rPET bottles is part of a broader sustainability initiative aiming to reduce reliance on virgin plastic, lower greenhouse gas emissions by at least 19%, and cut company's energy consumption in half.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Caffeinated Coffee to Maintain Segment Leadership Due to Strong Consumer Dependence and Café Culture

The caffeinated segment is projected to dominate the market with a share of 80.97% in 2026 in the global market. The rising caffeine consumption among individuals in the global market is fueling the global coffee concentrates demand made from either Arabica or Robusta. Liquid soluble coffees have a higher caffeine content, thus catering to the rising demand among individuals for caffeine. It is projected to grow at a CAGR of 6.03% (2026–2034), supported by rising café chains, premium Arabica varieties, and growing demand for cold-brew concentrate in home-use applications.

The decaffeinated segment is expected to grow in the forecast period with a CAGR of 3.59% in 2026.

To know how our report can help streamline your business, Speak to Analyst

By Distribution Channel

Rising Advancement of Online Retail Channel to Fuel Retail Segment Growth

By distribution channel, the market is divided into HoReCa and retail. Retail, which has a dominant share of the market, is further segmented into supermarkets/hypermarkets, specialty stores, convenience stores, and online retail.

The retail segment is projected to account for 6.34% of the market share in 2026, expanding at a CAGR of 5.51%. The supermarkets/hypermarkets have the highest share in the market owing to the higher availability of different product variants. However, online retail is said to have the highest CAGR owing to the rapid growth in technology and convenience of doorstep delivery offered by the leading online grocery and e-commerce companies.

The HoReCa segment is anticipated to grow at a CAGR of 6.58% during the forecast period.

By Form

Liquid Concentrate’s Leadership is Driven by Its Ease of Use and Premium Taste Profiles

The market is segmented into liquid concentrate, frozen concentrate, and powdered concentrate.

The liquid concentrate segment is expected to lead the market with a share of 69.49% in 2026 due to its superior flavor extraction, ease of dilution, and wide adoption in cafés and RTD production. Liquid concentrate market is expected to grow at a CAGR of 5.78% from 2026–2034.

The frozen concentrate segment is anticipated to grow at a CAGR of 5.96% during the forecast period.

Coffee Concentrate Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and Middle East & Africa.

Europe

Europe Coffee Concentrate Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The European region has a dominant share in the market for coffee owing to the higher consumption of soluble coffee at home in countries, including the U.K., Germany, France, Italy, and others. Europe is a mature coffee market with strong specialty café networks and high consumption of premium Arabica and cold-brew beverages. Sustainability mandates and demand for organic concentrates support value growth at a CAGR of 5.93%. Nordic countries and Germany are leading consumption bases. The UK market is projected to reach USD 0.09 billion by 2026, while the Germany market is projected to reach USD 0.18 billion by 2026. The Europe market was valued at USD 1.11 billion in 2025, capturing 35.19% of global revenue, and is estimated to reach USD 1.17 billion in 2026.

North America

North America remains a high-value market owing to its strong cold-brew culture, dominance of premium RTD brands, and widespread adoption of concentrates in foodservice. Value of growth rate is expected to be 4.11%, driven by premium artisanal brands, subscription coffee services, and rising home-mix usage. The U.S. coffee concentrates market experiences robust growth driven by evolving consumer preferences for convenience and premium coffee experiences. Key factors include the surge in cold brew and ready-to-drink (RTD) formats, alongside operational efficiencies in foodservice. Moreover, consumers increasingly seek high-end, flavored, and specialty concentrates, driving premium product adoption in retail and cafés. The U.S. market is projected to reach USD 0.8 billion by 2026. North America accounted for USD 0.91 billion in 2025, representing 29.56% of the global market share, and is projected to reach USD 0.95 billion in 2026.

Asia Pacific

Asia Pacific accounted for the prominent share, reaching USD 873.18 million by 2034, with a CAGR of 6.84%. Growth is fueled by increasing café penetration, premium coffee culture among millennials, and rapid adoption of cold-brew concentrates in China, South Korea, Japan, and Australia. The Japan market is projected to reach USD 0.04 billion by 2026, the China market is projected to reach USD 0.08 billion by 2026, and the India market is projected to reach USD 0.27 billion by 2026. In 2025, Asia Pacific held 16.23% of the global market, reaching a valuation of USD 0.51 billion, and is projected to grow to USD 0.55 billion in 2026.

Latin America

South America shows robust growth driven by strong domestic coffee culture and rising consumption of cold-brew formats. The region is projected to achieve a CAGR of 6.54%, supported by urban café expansion and the emergence of craft coffee concentrate production brands in Brazil and Colombia. The Latin America region captured 13.81% of the global market in 2025, generating USD 0.44 billion in revenue, and is projected to reach USD 0.46 billion in 2026.

Middle East & Africa

MEA markets benefit from strong out-of-home consumption and rising specialty café penetration in the GCC. Coffee concentrate adoption is increasing in QSR chains and modern retail. MEA is projected to grow at a CAGR of 6.63%, supported by rising population and growing premium beverage demand. Middle East & Africa contributed approximately USD 0.17 billion to the global market in 2025, accounting for 5.22% share, and is expected to reach USD 0.18 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Advancements in Coffee Extraction By Key Market Players to Support Their Market Positions

The prominent players operating in the global market leverage proprietary cold-brew extraction technologies, sustainable sourcing models, and strong retail partnerships to strengthen their market presence. Innovation focuses on low-acid concentrates, functional coffee blends, flavored concentrates, single-origin variants, and sustainable packaging. Limited-edition flavors, e-commerce exclusives, and café-branded retail concentrates have become key strategies to attract younger consumers.

Key Players in the Market

|

Rank |

Company Name |

|

1 |

Nestlé S.A. |

|

2 |

Starbucks Corporation |

|

3 |

Keurig Dr Pepper Inc. |

|

4 |

JDE Peet’s N.V. |

|

5 |

Nestlé S.A. |

List of Key Coffee Concentrate Manufacturers Profiled

- Javy Coffee Company (U.S.)

- The J.M. Smucker Company (U.S.)

- Starbucks Corporation (U.S.)

- Blue Bottle Coffee, Inc. (U.S.)

- Kohana Coffee (U.S.)

- Nestlé S.A. (Switzerland)

- Climpson & Sons (U.K.)

- Monin (France)

- Grady’s Cold Brew (U.S.)

- Wandering Bear Coffee (U.S.)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Nestlé launched the first Nescafé Espresso Concentrate production line in Asia at its Sri Muda factory in Shah Alam, Malaysia. This new line addresses the growing demand for cold coffee across Asia and targets both domestic and export markets, including Singapore, Oceania, the Middle East, and North Africa (MENA), with potential expansion to Europe.

- July 2025: Red Diamond Coffee & Tea introduced its Fitz cold brew coffee concentrate in response to the rapidly rising consumer demand for cold brew coffee in foodservice and hospitality settings. The Fitz Cold Brew Coffee Concentrate enables operators to easily prepare premium cold brew by mixing a 16-oz bottle of concentrate with 112 oz of water to yield a gallon of ready-to-serve cold brew, eliminating the need for specialized equipment or lengthy brewing processes.

- May 2025: Moccona, a brand of freeze-dried instant coffee, launched a new single-serve liquid coffee concentrate product in Australia called Liquid Espresso Coffee Sachets. The product comes in an eight-pack format and is available in three flavors: Medium Roast, Dark Roast, and Caramel.

- November 2024: BKON launched its first ready-to-purchase product called Genesis Coldstretto, a cold espresso coffee concentrate. This shelf-stable and ready-to-use extraction delivers the authentic flavor of espresso in cold beverages without needing an espresso machine or trained barista.

- September 2024: Peet's Coffee launched Ultra Coffee Concentrate, as its first espresso-style concentrate for at-home use, made from the signature Espresso Forte blend using a gentle extraction process with only coffee and water.

- August 2023: Onyx Coffee Lab launched Extractions, a premium shelf-stable coffee concentrate, to deliver full-flavor specialty coffee profiles with convenience for home, cafe, or bar use.

REPORT COVERAGE

The global coffee concentrate market industry report analyzes the market in depth and highlights crucial aspects such as global market trends, market dynamics, prominent companies, investment in research reports and development, and end-use. Besides this, the report also provides insights into the global market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.71% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Distribution Channel · HoReCa · Retail o Supermarkets/Hypermarkets o Specialty Stores o Convenience/Grocery Stores o E-commerce |

|

|

By Form · Liquid Concentrate · Frozen Concentrate · Powdered Concentrate |

|

|

By Region · North America (By Type, Distribution Channel, Form, and Country) • U.S. (By Distribution Channel) • Canada (By Distribution Channel) • Mexico (By Distribution Channel) · Europe (By Type, Distribution Channel, Form, and Country) • Germany (By Distribution Channel) • Spain (By Distribution Channel) • Italy (By Distribution Channel) • France (By Distribution Channel) • Russia (By Distribution Channel) • U.K. (By Distribution Channel) • Rest of Europe (By Distribution Channel) · Asia Pacific (By Type, Distribution Channel, Form, and Country) • China (By Distribution Channel) • Japan (By Distribution Channel) • India (By Distribution Channel) • Australia (By Distribution Channel) • Rest of Asia Pacific (By Distribution Channel) · South America (By Type, Distribution Channel, Form, and Country) • Brazil (By Distribution Channel) • Argentina (By Distribution Channel) • Rest of South America (By Distribution Channel) · Middle East & Africa (By Type, Distribution Channel, Form, and Country) • South Africa (By Distribution Channel) • Saudi Arabia (By Distribution Channel) • Rest of the MEA (By Distribution Channel) |

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 3.13 billion in 2025 and is anticipated to reach USD 4.88 billion by 2034.

At a CAGR of 5.71%, the global market will exhibit steady growth over the forecast period.

By type, the caffeinated segment leads the market.

Europe held the largest market share in 2025.

Higher convenience and products being economical are driving market growth.

Nestle S.A., JAB Holding Company, Starbucks Corporation, Keurig Dr Pepper Inc., and JDE Peet’s N.V. are the leading companies in the market.

Health-driven formulations and sustainable packaging are shaping the industry.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us