Cold Chain Logistics Market Size, Share & Industry Analysis, By Type (Refrigerated Warehouses, Refrigerated Transportation), By Application (Fruits & Vegetables, Fish, Meat, and Seafood, Dairy & Frozen Desserts, Bakery & confectionery, Processed Food, Pharmaceuticals, Others) and Regional Forecasts, 2026-2034

Cold Chain Logistics Market Size

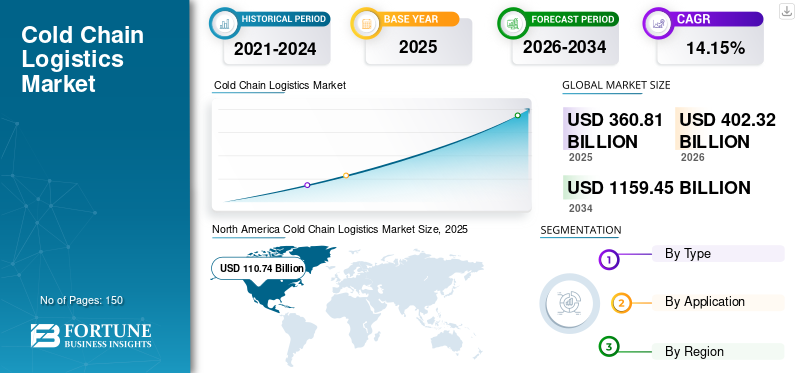

The global cold chain logistics market was valued at USD 360.81 billion in 2025 and is projected to grow from USD 402.32 billion in 2026 to USD 1,159.45 billion by 2034, exhibiting a CAGR of 14.15% during the forecast period. North America dominated the global market with a share of 30.69% in 2025.

The cold chain logistics market encompasses the transportation and storage of temperature-sensitive products, including perishable food items, pharmaceuticals, and chemicals, under controlled conditions to maintain their integrity and quality. With increasing globalization and demand for fresh and frozen products worldwide, the cold chain logistics industry is experiencing significant growth. Factors, such as advancements in refrigeration technology, stringent regulatory requirements, and the expansion of the pharmaceutical and healthcare sectors are driving market expansion.

Additionally, the rise of e-commerce and online grocery delivery services is further fueling demand for efficient cold chain logistics solutions. Overall, the market is characterized by innovation, stringent quality standards, and a focus on ensuring product safety and integrity throughout the supply chain.

The COVID-19 pandemic had a profound impact on the cold chain logistics market. With the global distribution of vaccines and pharmaceuticals, the demand for temperature-controlled storage and transportation surged. Additionally, disruptions in supply chains and logistics networks posed challenges, highlighting the importance of robust cold chain infrastructure. The pandemic accelerated digitalization and adoption of innovative technologies in cold chain logistics to ensure the safe and efficient distribution of temperature-sensitive goods amidst unprecedented challenges.

Download Free sample to learn more about this report.

Cold Chain Logistics Market Key Takeaways

- 2025 Market Size: USD 360.81 billion

- 2026 Market Size: USD 402.32 billion

- 2034 Forecast Market Size: USD 1,159.45 billion

- CAGR: 14.15% from 2026–2034

- North America dominated the global market with a 30.69% share in 2025.

- The refrigerated warehouse segment held the largest market share in 2025.

- The dairy & frozen desserts segment accounted for the major market share in 2025.

North America

North America held a 30.69% share in 2025, valued at USD 110.74 billion.

Asia Pacific

Asia Pacific accounted for 34.80% share in 2025, valued at USD 125.55 billion.

Europe

Europe held a 25.06% share in 2025, valued at USD 90.44 billion.

U.S.

The market projected to reach USD 79.52 billion by 2026.

Japan

The market projected to reach USD 24.53 billion by 2026.

Read More

Cold Chain Logistics Market Trends

Increasing Consumer Demand for Perishable Goods Drive Growth of Cold Chain Logistics Market

The increasing trend of buying perishable goods through the online platform has led to new opportunities and challenges. These include the requirement for automated warehouses to manage inventories, and innovative solutions to offer last-mile delivery. That also creates demand for advanced temperature monitoring devices to maintain quality and prolong the shelf life of perishable food products. Consumers are nowadays more conscious about wellness and health, and the effect that food nutrients, particularly protein, have on overall mental and physical development. This has caused a change in the consumption pattern of perishable goods, such as fruits and vegetables, dairy products, meat, eggs, fish, and seafood.

Download Free sample to learn more about this report.

Cold Chain Logistics Market Growth Factors

Increasing Demand for Temperature-Sensitive Pharmaceuticals and Biologics to Propel Market Growth

With the COVID-19 pandemic highlighting the critical importance of maintaining the integrity and efficacy of vaccines and other medical products, the need for robust cold-chain logistics solutions has become more pronounced than ever. According to data from the International Federation of Pharmaceutical Manufacturers & Associations (IFPMA), global pharmaceutical sales are projected to reach USD 1.5 trillion by 2024, with a significant portion of these sales comprising temperature-sensitive products. The development and distribution of vaccines and biologics, including mRNA vaccines and gene therapies, require stringent temperature control throughout the supply chain to ensure their effectiveness and safety.

As governments around the world continue to roll out vaccination campaigns and invest in healthcare infrastructure, the demand for cold chain logistics services is expected to grow exponentially. The pharmaceutical industry is witnessing a shift toward personalized medicine and biological therapies, which often have strict temperature requirements for storage and transportation. Biologics, such as monoclonal antibodies, cell therapies, and gene therapies, are increasingly being used to treat various diseases, driving the demand for specialized cold-chain logistics solutions.

Regulatory authorities, including the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA), have implemented stringent guidelines for the handling and distribution of temperature-sensitive pharmaceuticals. Compliance with these regulations necessitates investments in state-of-the-art cold chain infrastructure and temperature-monitoring technologies.

Additionally, the rise of e-commerce and direct-to-consumer healthcare services is contributing to the growth of the cold chain logistics market. With the increasing popularity of online pharmacies and doorstep delivery of prescription medications, there is a growing need for reliable cold-chain logistics solutions to ensure the safe and timely delivery of temperature-sensitive medical products to consumers. As the pharmaceutical industry continues to innovate and develop new therapies, the need for advanced cold chain logistics solutions will remain a critical factor driving market expansion.

RESTRAINING FACTORS

Environmental Concerns Regarding Greenhouse Gas Emissions Restrain Market Growth

Cold chain industry development places a substantial burden on the environment since refrigeration is a source of greenhouse gases and is energy-intensive. The snowballing number of refrigerated road transportation is extremely gaining massive demand across the world. Keeping products cold to prolong shelf life and maintain the quality of the products throughout the transportation phase of the cold chain (like trains, ships, and trucks) is important. Refrigerated transportation accounts for about 7% of total world hydrofluorocarbons (HFCs) consumption.

Likewise, diesel-powered reefer trucks, trailers, and containers consume around 21% more power than non-refrigerated diesel-powered trucks. This has noteworthy implications on climate change, as the development of cold chain infrastructure becomes almost ubiquitous in developing nations. Therefore, environmental concerns regarding greenhouse gas emissions are anticipated to hinder the cold chain logistics market growth.

Cold Chain Logistics Market Segmentation Analysis

By Type Analysis

Refrigerated Warehouse Held Largest Share of Market due to Increased Demand for Automated Warehouses to Manage Inventories

Based on type, the market is segmented into refrigerated warehouses and refrigerated transportation. In 2026, Refrigerated Warehouses dominated the segment with a market share of 53.91%. Changing the dietary patterns and lifestyles of consumers is propelling the demand for frozen food products. This is anticipated to boost the demand for refrigerated warehouses.

Furthermore, the refrigerated transportation segment is projected to grow at the fastest CAGR over the forecast period due to the increasing use of safe refrigerated transportation of temperature-sensitive goods and products. Transportation modes used are refrigerated cargo, refrigerated railcars, refrigerated trucks, and air cargo.

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Growth of Pharmaceuticals Segment Due to its Importance in Maintaining Efficacy and Safety of Pharmaceuticals

Based on the application, this market is segmented into fruits & vegetables, fish, meat, and seafood, dairy & frozen desserts, bakery & confectionery, processed food, pharmaceuticals, and others. In 2026, Dairy & Frozen Desserts dominated the segment with a market share of 21.99%. This is attributable to the increasing demand for animal protein products such as cheese, milk, and meat.

A cold chain is used for transporting frozen bakery products like bread and cakes, and frozen meat like fish, poultry, beef, seafood, and pork. Changing dietary habits of consumers and growing levels of disposable income are boosting the product demand from the bakery and confectionary segments.

REGIONAL INSIGHTS

North America Cold Chain Logistics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America contributed approximately USD 110.74 Billion to the global market in 2025, accounting for 30.69% share, and is expected to reach USD 118.02 Billion in 2026. The region’s growth is supported by advanced cold chain infrastructure, strong demand for temperature-sensitive food and pharmaceutical products, and the widespread adoption of modern logistics technologies. The growing penetration of connected devices, expanding refrigerated warehousing capacity, and a large consumer base continue to drive market expansion. The U.S. market is projected to reach USD 79.52 Billion in 2026.

Asia Pacific

The Asia Pacific region captured 34.80% of the global market in 2025, generating USD 125.55 Billion in revenue, and is projected to reach USD 144.31 Billion in 2026. The region is witnessing strong growth due to increasing government investments in cold chain infrastructure, rising consumption of meat, dairy, and processed food products, and expanding pharmaceutical manufacturing activities. Growing foreign direct investments and improvements in logistics networks are further supporting market development. The China market is projected to reach USD 64.08 Billion in 2026, while India and Japan are expected to reach USD 22.53 Billion and USD 24.53 Billion, respectively.

Europe

In 2025, the Europe market stood at USD 90.44 Billion, representing 25.06% of global demand, and is projected to grow to USD 101.22 Billion in 2026. Growth in the region is driven by increasing demand for high-quality food preservation, expansion of pharmaceutical cold chain services, and stringent regulations regarding food safety and product quality. The development of advanced refrigerated transportation and storage facilities continues to support market growth. The U.K. and Germany markets are projected to reach USD 28.19 Billion and USD 31.33 Billion in 2026, respectively.

Rest of the World

In 2025, Rest of the World represented USD 34.09 Billion, accounting for 9.45% of the worldwide market, and is projected to grow to USD 38.77 Billion in 2026. Demand across these regions is increasing due to rising disposable incomes, rapid urbanization, and growing consumption of perishable, frozen, and ready-to-cook food products. Expanding pharmaceutical distribution networks and investments in cold storage infrastructure are also contributing to market growth. Developing economies continue to present significant opportunities as adoption of cold chain logistics services increases across food and healthcare industries.

List of Key Companies in Cold Chain Logistics Market

Key Market Players Are Constantly Upgrading Their Technologies to Stay Ahead of Competition

This market is highly competitive and fragmented, with key players such as the U.S. Cold Storage, AmeriCold Logistics LLC, LINEAGE LOGISTICS HOLDING, LLC, VersaCold Logistics Services, and NICHIREI LOGISTICS GROUP INC. (NICHIREI CORPORATION). These players are increasing their multi-compartment reefer vehicle fleets to offer added services to their end-users. Moreover, key companies are upgrading their technologies to ensure safety, integrity, and efficiency.

LIST OF KEY COMPANIES PROFILED:

- U.S. Cold Storage (New Jersey, U.S.)

- AmeriCold Logistics LLC (Georgia, U.S.)

- LINEAGE LOGISTICS HOLDING, LLC (Michigan, U.S.)

- VersaCold Logistics Services (Ontario, Canada)

- NICHIREI LOGISTICS GROUP INC. (NICHIREI CORPORATION) (Tokyo, Japan)

- CONGEBEC LOGISTICS INC. (Quebec, Canada)

- Burris Logistics (Delaware, U.S.)

- CONESTOGA COLD STORAGE (Ontario, Canada)

- Kloosterboer (Netherlands)

- COLD BOX EXPRESS, INC. (Alabama, U.S.)

KEY INDUSTRY DEVELOPMENTS:

- January 2024: Snowman Logistics expanded its operations at a newly leased multi-temperature-controlled warehouse in Guwahati, Assam. The total capacity of the warehouse is 5,152 pallets, and this facility features eight chambers and four loading bays that are equipped with the latest infrastructure. It is specifically designed to accommodate products from ambient temperatures to minus 25 degrees Celsius. The warehouse will primarily focus on providing storage, handling, and transportation services for ice cream, poultry, ready-to-eat food, dairy products, confectionery, bakery products, seafood, fruits, and vegetables.

- January 2024: GreenDome Holdings, through its subsidiary Elite Co., a prominent logistics investment vehicle owned by regional industry leaders, acquired LogX, the UAE's leading temperature-controlled logistics company. This multi-million dollar deal marks another significant milestone for GDH as it strengthens its position in the market and expands its service offerings.

- December 2023: AVG Logistics acquired over 50 cold chain vehicles to strengthen fleet operations, taking the company's total cold chain fleet strength to 275. This enhanced AVG's ability to service. Recently, a long-term contract was signed with India's largest MNC FMCG Company, both on the dry and frozen goods side.

- October 2023: Mitsui & Co., Ltd. signed an agreement to invest in PT. Pangan Lestari is one of the leading food distribution and cold-chain logistics companies in Indonesia. This contribution enhanced the quality of PL's business by leveraging its knowledge and expertise in food distribution and cold-chain logistics.

- May 2023: TAHUHU launched the first automated and smart cold chain logistics service in Hong Kong. The solution includes a seamless temperature-control loading dock, “muti-level no-man zone,” and top-of-the-line automation equipment, such as "goods-to-person" systems and “automated vertical cargo lift. The facility's ability to optimize storage space and increase productivity while maintaining the highest quality standards is a testament to its commitment to excellence. With its advanced automation and innovative systems, TAHUHU set a new standard for cold chain logistics in Hong Kong.

REPORT COVERAGE

The global cold chain logistics market report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading product applications. Besides this, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that have contributed to the market’s growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 14.15% (2026-2034) |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

By Application

By Geography

|

Frequently Asked Questions

Fortune Business Insights report forecasts that the global market size was USD 360.81 billion in 2025 and is projected to reach USD 1,159.45 billion by 2034.

In 2025, the North American market revenue stood at USD 110.74 billion.

The market is projected to grow at a CAGR of 14.15% and will exhibit exponential growth over the forecast period (2026-2034).

The refrigerated warehouse segment is expected to be the leading segment in this market during the forecast period.

Increasing need for temperature control to prevent food losses, and the rising demand for perishable goods among consumers across the world to propel the market growth.

LINEAGE LOGISTICS HOLDING, LLC is the leading player in the global market.

North America dominated the market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us