Commercial Aircraft Diagnostic & Maintenance Systems Aftermarket Size, Share & Industry Analysis, By component (Centralized Fault & Data Management, Data Management Unit, Central Maintenance System, Crew & Maintenance Interfaces, Data Loading & Security, Data Connectivity & Transfer, and Advanced & Future Technologies, By Offerings (MRO Services and Refurbished Parts), By Aircraft Family (A220, A320, A330, A350, A380, ATR 42/72, B737, B747, B767, B777, B787, Bombardier CRJ, COMAC C919, De Havilland Dash 8, Embraer E-Jets, and Sukhoi Superjet), and Regional Forecast, 2025-2045

KEY MARKET INSIGHTS

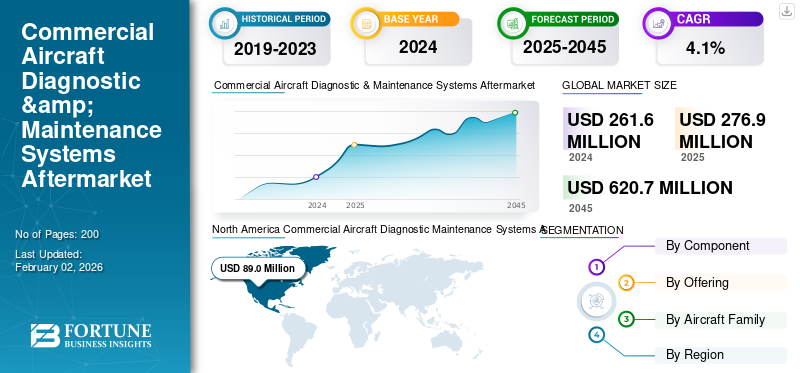

The global commercial aircraft diagnostic & maintenance systems aftermarket size was valued at USD 261.6 million in 2024. The aftermarket is projected to grow from USD 276.9 million in 2025 to USD 620.7 million by 2045, exhibiting a CAGR of 4.1% during the forecast period. North America dominated the global commercial aircraft diagnostic & maintenance systems aftermarket with a market share of 34.09% in 2024.

Commercial aircraft diagnostic & maintenance systems are critical to ensuring operational reliability, safety, and efficiency of modern fleets. These systems include health monitoring tools, sensors, onboard diagnostics, fault detection software, and ground-based maintenance operations and technologies. With rising fleet utilization, aging aircraft, and increasing regulatory focus on predictive maintenance, MRO and refurbished parts for diagnostic systems have gained strong momentum. Airlines and MRO providers are growingly integrating AI, IoT, and digital twin solutions to reduce AOG (Aircraft on Ground) incidents and extend component life.

Furthermore, the aftermarket encompasses several major players with Collins Aerospace, Honeywell Aerospace, Thales Group, and Safran Electronics & Defense at the forefront. Broad portfolio with innovative product launch, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Predictive Maintenance Boosts Aftermarket Adoption

Airlines are increasingly prioritizing predictive maintenance solutions to reduce aircraft downtime and prevent costly AOG (Aircraft on Ground) events. Advanced diagnostic systems integrated with AI and IoT enable real-time monitoring of avionics, engines and control systems, driving efficiency and safety. This trend is particularly strong in large fleets where operational efficiency and reliability is critical. For example, in March 2025, Emirates partnered with Honeywell to deploy predictive health monitoring systems across its Boeing 777 fleet, enabling data-driven diagnostics to reduce unplanned maintenance events. Such investments highlight how predictive capabilities are fueling maintenance repair and overhaul demand and adoption of refurbished diagnostic components.

MARKET RESTRAINTS

High Integration Costs Limits Product Adoption Across Smaller Airlines

While predictive diagnostic systems improve efficiency, their adoption faces restraints due to high implementation and integration costs. Smaller and regional airlines struggle with the financial burden of installing advanced health monitoring systems and upgrading legacy aircraft platforms. Additionally, the complexity of integrating AI-driven platforms with older fleets limits adoption. For instance, in December 2024, IATA highlighted that nearly 40% of regional airlines in Latin America are delaying the transition to advanced diagnostic systems due to cost concerns and compatibility issues. This underscores how financial and technological barrier restrict growth despite the clear benefits of predictive diagnostics.

MARKET OPPORTUNITIES

AI-Driven Digital Twins Create New Revenue Streams for Aftermarket

Digital twin technology is emerging as a major opportunity in diagnostic and maintenance systems, allowing airlines and MROs to simulate real time aircraft health and predict component wear. By combining AI with IoT data, airlines can significantly cut costs and extend component life cycles. In February 2025, Lufthansa Technik launched a digital twin platform for Airbus A350 operators, integrating real-time engine and avionics diagnostics into predictive maintenance planning. This shift not only enhances operational reliability but also creates opportunities for OEMs and MRO providers to offer subscription-based monitoring services, opening new revenue streams in the commercial aircraft diagnostic & maintenance systems aftermarket.

COMMERCIAL AIRCRAFT DIAGNOSTIC MAINTENANCE SYSTEMS AFTERMARKET TRENDS

Integration of Cloud-Based Diagnostic Platforms is Reshaping the Aftermarket

A key trend shaping the aftermarket is the shift toward cloud-based diagnostic and predictive maintenance platforms. These enable remote monitoring, real-time fault detection, and global access to aircraft health data, significantly reducing turnaround times. Airlines and MRO providers are increasingly investing in cloud-enabled systems to streamline maintenance workflows. In January 2025, Boeing announced an expansion of its AnalytX platform to integrate cloud-based predictive diagnostics across global operators of the 737 MAX and 787 fleets. This trend underscores the growing role of digital ecosystems in enhancing fleet availability, making cloud-based diagnostics a cornerstone of future MRO services.

MARKET CHALLENGES

Cybersecurity Risks in Connected Diagnostic Systems Challenge Aftermarket Stability

The increasing digitalization of diagnostic and maintenance systems exposes airlines and MROs to cybersecurity risks. Connected platforms and cloud-based solutions, while improving efficiency, also create vulnerabilities to hacking and data breaches. Regulatory bodies such as EASA and FAA are tightening compliance frameworks to ensure data security in connected aircraft systems. In November 2024, the FAA issued an advisory highlighting cybersecurity risks in predictive maintenance platforms following reported breaches in third-party diagnostic software used by regional airlines in North America. Such risks could undermine airline confidence, slow adoption, and increase compliance costs, posing a major threat to aftermarket growth.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component

High Demand for data management Contributed to Centralized Fault & Data Management Segmental Growth

On the basis of component, the aftermarket is classified into Centralized Fault & Data Management, Crew & Maintenance Interfaces, Data Loading & Security, Data Connectivity & Transfer, and Advanced & Future Technologies.

Among these, Centralized Fault & Data Management dominates, as airlines increasingly depend on real-time monitoring and predictive fault isolation to minimize unplanned downtime. This segment drives significant commercial aircraft diagnostic & maintenance systems aftermarket, with operators refurbishing modules to extend lifecycles and reduce costs.

Crew & Maintenance Interfaces are also gaining higher traction, particularly through intuitive dashboards and upgraded display systems for legacy fleets. Data Loading & Security is being reinforced by stricter cybersecurity regulations, while Data Connectivity & Transfer is expanding rapidly due to connected aircraft initiatives. Advanced technologies such as AI, digital twins, and block chain are emerging and remain in early adoption. In March 2025, Airbus integrated fault data management into its Sky wise platform, reinforcing the leading role of centralized systems in predictive maintenance.

To know how our report can help streamline your business, Speak to Analyst

By Offerings

Increasing Focus on Preventive Maintenance and Inspection Fuels Growth of MRO Segment

In terms of offerings, the aftermarket is categorized into MRO services and refurbished parts.

The MRO services segment captured the largest share of the aftermarket in 2024. In 2025, the segment is anticipated to dominate the market. MRO services account for the majority of cabin pressurization maintenance and repairs, including preventative inspections, leak checking, sensor calibration work, and changing any faulty parts. Airlines are reliant on certified MRO providers to ensure FAA and EASA regulatory requirements and safety standards are met. The expansion of predictive maintenance tools and digital diagnosis are also reinforcing the segment growth.

MRO services dominate, supported by the need for regular inspections, repair, and overhaul to ensure compliance with aviation industry safety standards. Airlines increasingly rely on third-party MRO providers and OEM-authorized centers for advanced diagnostic support, particularly for aging narrow-body fleets.

Refurbished parts, however, are witnessing strong growth due to their cost effectiveness and sustainability benefits. There is a growing demand for flight data modules and maintenance interface components that can be refurbished and recertified for extended service life. In January 2025, Lufthansa Technik announced it would expand its component refurbishment services for avionics systems, highlighting the rising adoption of refurbished diagnostic parts.

By Aircraft Family

Widespread Usage of Standard Diagnostic & Maintenance Systems MRO & Refurbished Parts Supplemented Segment Growth

Based on aircraft family, the aftermarket is segmented into Airbus A220, Airbus A320 Family (ceo/neo), Airbus A330 (ceo/neo), Airbus A350, Airbus A380, ATR 42/72, Boeing 737 Family (Classic/NG/MAX), Boeing 747, Boeing 767, Boeing 777, Boeing 787, Bombardier CRJ Series, COMAC C919, De Havilland Dash 8 (Q-Series), Embraer E-Jets (E1/E2), and Sukhoi Superjet 100.

The Airbus A320 Family (ceo/neo) segment held the dominating position in 2024. This is primarily due to its massive global installed base, high operational commonality, and advanced diagnostic capabilities. With over 12,000 aircraft delivered and more than 11,000 in service, the A320 family is the most-utilized and best-selling single-aisle aircraft in the world. This sheer volume creates a massive, enduring demand for Maintenance, Repair, and Overhaul (MRO) services, spare parts, and diagnostic tools, solidifying its aftermarket dominance.

The COMAC C919 segment is poised for rapid growth with the highest CAGR of 18.3% during the forecast period due to its exploding fleet size in China and its role as a cost-effective alternative for global budget airlines (Asia, Africa). Additionally, the strategic push for domestic tech indigenization creating a large, supportive ecosystem for its specific systems, driving demand for dedicated MRO (Maintenance, Repair, Overhaul) and diagnostics as utilization increases.

Commercial Aircraft Diagnostic & Maintenance Systems Aftermarket Regional Outlook

By geography, the aftermarket is categorized into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America Commercial Aircraft Diagnostic Maintenance Systems Aftermarket Size, 2024 (USD Million) To get more information on the regional analysis of this market, Download Free sample

The North America held the dominant share in 2023 valuing at USD 71.3 Million and also took the leading share in 2024 with USD 72.7 Million. North America dominates the market, supported by the large fleets of major carriers such as Delta, American Airlines, and United, coupled with strong MRO capabilities. The region’s leadership is further driven by high adoption of predictive maintenance, data-driven fault detection, and FAA regulatory compliance. The U.S. also hosts several OEMs and avionics suppliers that are key players in the diagnostic systems space.

- In July 2024, Boeing partnered with Collins Aerospace to enhance aircraft health monitoring capabilities for U.S. airlines, strengthening the diagnostic ecosystem in the region.

Europe and Asia Pacific

Europe and Asia Pacific collectively are growing rapidly. Europe benefits from strong airline operators such as Lufthansa, Air France-KLM, and Ryanair, alongside MRO leaders such as Lufthansa Technik and ST Engineering. Asia Pacific is witnessing rapid fleet expansion, especially from low-cost carriers in China and India, which boosts demand for diagnostic system MRO. Additionally, the region is emphasizing digital integration to improve aircraft availability. In October 2024, Singapore Airlines Engineering Company (SIAEC) signed a collaboration agreement with Honeywell to deploy advanced predictive maintenance solutions across its fleet.

Latin America and Middle East & Africa

Over the forecast period, Latin America & Africa and Middle East regions would witness a moderate growth in this marketspace. Latin America aftermarket in 2025 is set to record USD 20.6 Million as its valuation. Latin America and Middle East & Africa are emerging markets where fleet modernization and regional airline growth drive adoption of diagnostic and maintenance solutions. In Latin America, carriers such as LATAM Airlines and Azul are investing in refurbished parts to control operational costs. In Middle East & Africa, Gulf carriers such as Emirates and Qatar Airways lead adoption of high-tech diagnostic systems, while smaller regional carriers rely more on refurbished components. In September 2024, Emirates signed a deal with Lufthansa Technik to expand avionics and diagnostic MRO services for its Airbus A380 fleet, signaling strong MRO demand in the region.

COMPETITIVE LANDSCAPE

Key Industry Players

Wide Range of Product Offerings coupled with Strong Distribution Network of Key Companies Supported their Leading Position

The aftermarket is moderately consolidated, with a mix of OEMs, Tier-1 avionics suppliers, and independent MRO providers competing for contracts. Key players include Honeywell Aerospace, Collins Aerospace, Lufthansa Technik, Safran, Thales, GE Aviation, ST Engineering, and Boeing Global Services, all of which focus on integrating predictive maintenance and centralized data management into MRO workflows. OEMs are leveraging proprietary health-monitoring systems to maintain aftermarket dominance, while independent MROs emphasize refurbished components to deliver cost-efficient solutions.

Strategic partnerships and digital transformation initiatives are shaping competition, with companies investing in AI-driven fault detection, real-time data transfer, and secure cloud platforms. In June 2024, Honeywell launched its Connected Maintenance platform with AI-driven diagnostics, strengthening its foothold in predictive MRO. Competitive intensity is expected to rise as fleet operators demand higher reliability, lower downtime, and sustainable maintenance practices.

LIST OF KEY COMMERCIAL AIRCRAFT DIAGNOSTIC & MAINTENANCE SYSTEMS COMPANIES PROFILED

- Collins Aerospace (U.S.)

- Honeywell Aerospace (U.S.)

- Thales Group (France)

- Safran Electronics & Defense (France)

- Liebherr-Aerospace (Germany/France)

- Moog Inc. (U.S.)

- Parker Aerospace (U.S.)

- Spirit AeroSystems (U.S.)

- ST Engineering Aerospace (Singapore)

- Lufthansa Technik (Germany)

KEY INDUSTRY DEVELOPMENTS

- May 2025: Magnetic Engines entered into an agreement with Lufthansa’s Group Engine Management to perform MRO (engine repairs) for CFM56‑5B engines, enhancing availability of repaired components through diagnostic assessment and refurbished parts deployment.

- May 2025: FL Technics received EASA approval to conduct base maintenance on Boeing 737 MAX (8 & 9) aircraft with CFM Leap‑1B engines—adding to its diagnostic and repair capabilities for modern, digitally monitored aircraft systems.

- May 2025: Global MRO provider Safran Aircraft Engines completed its acquisition of Component Repair Technologies (CRT), bolstering engine-part repair and diagnostic capacity in the Americas and securing refurbished engine parts for MRO support.

- April 2025: MRO Japan partnered with Quest Global Services to deploy AI-based solutions aimed at improving aircraft maintenance operational efficiencies and reducing manual workload in diagnostic and repair tasks.

- March 2025: Indamer Technics in India opted for Ramco Systems’ aviation software to optimize maintenance workflows, reduce turnaround times, and gain real-time insights into diagnostic and parts management.

- March 2025: Cathay Pacific chose Trax to digitalize its engineering department, implementing modules such as eMRO, AeroDox, VisualCheck, Line Control, TaskControl, and eContent Control for advanced diagnostics and maintenance operations.

- February 2025: TIM Aerospace DWC MRO (a new widebody MRO in Dubai) selected IFS’s EmpowerMX software to manage maintenance operations digitally—enhancing diagnostic and workflow systems.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2045 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2045 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 4.1% from 2025-2045 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Component, Offering, Aircraft Family and Region |

|

By Component |

· Centralized Fault & Data Management o Central Fault Computer (CFC) o Data Management Unit (DMU) o Integrated CMS (Central Maintenance System) o Advanced CMS · Crew & Maintenance Interfaces o MCDU Interface o Touchscreen MCDU o Holographic MCDU · Data Loading & Security o Legacy Data Loader o Cyber-Secure Loader · Data Connectivity & Transfer o Secure Data Server o Wireless Data Transfer o Satellite Data Link o EFB Integration o Cloud Diagnostics · Advanced & Future Technologies o AI Health Management o Quantum Data Storage |

|

By Offering |

· MRO Services · Refurbished Parts o PMA o USM |

|

By Aircraft Family |

· Airbus A220 · Airbus A320 Family (ceo/neo) · Airbus A330 (ceo/neo) · Airbus A350 · Airbus A380 · ATR 42/72 · Boeing 737 Family (Classic/NG/MAX) · Boeing 747 · Boeing 767 · Boeing 777 · Boeing 787 · Bombardier CRJ Series · COMAC C919 · De Havilland Dash 8 (Q-Series) · Embraer E-Jets (E1/E2) · Sukhoi Superjet 100 |

|

By Geography |

· North America (By Component, Offering, Aircraft Family, and Country) o U.S. o Canada · Europe (By Component, Offering, Aircraft Family, and Country) o Germany o U.K. o Germany o France o Russia o Rest of Europe · Asia Pacific (By Component, Offering, Aircraft Family, and Country) o China o India o Japan o Australia o Rest of Asia Pacific · Latin America & Africa (By Component, Offering, Aircraft Family, and Country) o Brazil o Mexico o Rest of Latin America · Middle East (By Component, Offering, Aircraft Family, and Country) o UAE o Saudi Arabia o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global aftermarket value stood at USD 261.6 Million in 2024 and is projected to reach USD 620.7 Million by 2045.

In 2024, the aftermarket value stood at USD 87.3 Million.

The aftermarket is expected to exhibit a CAGR of 4.1% during the forecast period of 2025-2045.

The MRO services segment led the aftermarket by offering.

AI-Driven Digital Twins Create New Revenue Streams Driving MRO Demand.

Collins Aerospace (U.S.), Honeywell Aerospace (U.S.), and Thales Group (France) are some of the prominent players in the market.

North America dominated the aftermarket in 2024.

- 2019-2045

- 2024

- 2019-2023

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us