Commercial Aircraft Engine Controls Aftermarket, Size, Share, and Industry Analysis, By Component (FADEC Processor, Thrust Control Sensor, Fuel Metering Valve, Start Control Unit, Reverser Actuator, Hydraulic Control Unit, Thrust Lever Encoder, Fuel Flow Regulator, Thrust Reverser Actuator, Smart Thrust Resolver, Fuel Control Unit, Digital Start Controller, Reverser Control Valve, & Others), By Offering (MRO Services and Refurbished Parts), By Aircraft Family (A220, A320, A330, A350, A380, ATR 42/72, B737, B747, B767, B777, B787, & Others), and Regional Forecast 2025-2045

KEY MARKET INSIGHTS

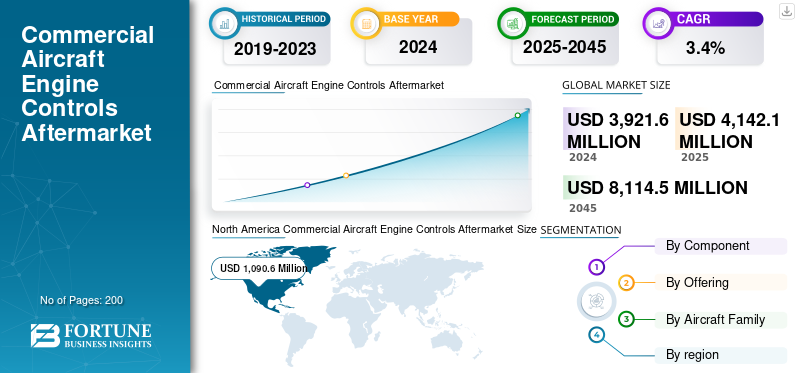

The commercial aircraft engine controls aftermarket size was valued at USD 3,921.6 million in 2024. The market is projected to grow from USD 4,142.1 million in 2025 to USD 8,114.5 million by 2045, exhibiting a CAGR of 3.4% during the forecast period. North America dominated the global commercial aircraft engine controls aftermarket with a market share of 27.81% in 2024.

Commercial aircraft engine controls aftermarket covers the mechanisms that regulate engine performance by managing thrust, fuel flow, turbine temperature, and overall efficiency. Modern aircraft rely on advanced Full Authority Digital Engine Control (FADEC) units to ensure precision and safety. The commercial aircraft engine controls aftermarkets market includes maintenance, repair, and overhaul (MRO) services that keep these systems airworthy, reliable, and compliant with aviation regulations, including inspection, software renewal, sensor calibration, and component replacement. In parallel, the refurbished parts market consists of reconditioning and certifying reused engine control components such as sensors, actuators, and processors to meet operational requirements. This segment offers operators cost-effective and more sustainable options for new parts.

Key players in the commercial aircraft engine controls aftermarket include GE Aerospace, Safran, Collins Aerospace, Honeywell, and Pratt & Whitney. These companies are fueling market growth through ongoing innovation, strategic collaborations, and expansion of aftermarket services networks. Advanced digital technologies, such as predictive maintenance, artificial intelligence-based health monitoring, and digital twins to improve engine control system reliability and minimize aircraft downtime.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Global Rising Need for MRO Services is Driving the Growth of the Market

The fast growth of commercial and military aircraft fleets globally, combined with the substantial cost of replacing new engine control units, is increasing demand for MRO services and overhauled parts. Operators and airlines are under continuous pressure to reduce operating expenses while maintaining safety and regulatory requirements, which is accelerating demand for refurbished FADEC units, sensors, and actuators.

Additionally, rising flight hours following post-pandemic recovery are leading to more frequent maintenance cycles, and OEMs and independent MRO providers are increasing their service networks to deliver quicker turnaround times. As a result, expansion of the fleet, cost economies, and compliance requirements are fueling market growth.

- For instance, in March 2023, GE Aerospace and Emirates entered a long-term agreement for engine control system MRO support and component refurbishment for Emirates. The agreement aims to improve parts availability, shorten supply chains, and reduce life-cycle costs for Emirates, a major operator of Boeing 777s and Airbus A380s.

Market Restraints

High Certification Cost and Supply Chain Challenges are hindering Market Growth

The MRO and refurbished parts market is growing; however, high certification costs and supply chain disturbance due to the Russia-Ukraine conflict and U.S. tariff war decelerate its growth. The major challenge is the lengthy process of certification and regulatory approval, making refurbishment costly and time-consuming, with smaller players having difficulties in competing.

Additionally, supply chain disruption, especially in procuring electronic components and raw materials for FADEC units and sensors, increases lead times. Airlines are also concerned about reconditioned parts since reliability and lifespan compared to new OEM parts remain. In addition, escalating labor and maintenance costs and the intricacy of contemporary digital engine control systems inject financial and operational burdens, holding back rapid market penetration.

- For instance, in September 2022, European MRO providers reported delays in delivering refurbished engine control components due to semiconductor shortages due to Russia-Ukraine conflict, highlighting supply chain vulnerabilities in the aftermarket sector.

Market Opportunities

Digitalization and Sustainability Create Strong Opportunities in the Market

The growth of digital technologies, such as predictive maintenance, AI-based diagnostics, and digital twins, enables MRO providers to detect faults earlier and minimize downtime. Airlines are increasingly seeking cost-effective and sustainable solutions, resulting in increasing demand for refurbished FADEC units, sensors, and actuators that increase part lifecycles and minimize waste. As regulators and airlines focus on reducing carbon emissions and circular economy solutions, the refurbished parts market is well-positioned to be a key growth driver.

In addition, the growth of OEM-supported and MRO sites is growing fast, with markets such as Asia Pacific and the Middle East & Africa investing heavily to serve expanding fleets in these regions.

- For instance, in June 2023, Collins Aerospace launched a digital predictive maintenance solution for engine control systems, enabling airlines to reduce unscheduled removals and optimize the use of refurbished parts, directly supporting cost savings and sustainability goals.

Commercial Aircraft Engine Controls Aftermarket Trends

Shifting Toward Digital MRO and Sustainable Refurbishment in Engine Control Systems

The integration of digital and predictive technologies with MRO services allows real-time monitoring and preventive maintenance of engine control systems. MRO providers and airlines are increasingly using AI, IoT sensors, and digital twins to streamline engine health checks and prolong service intervals.

Increasing acceptance of refurbished and green-certified parts is another key trend, fueled by airline cost constraints and the sustainability duties of airlines. OEMs and independent service providers are also developing regional MRO centers to minimize turnaround times and support fast-growing fleets in the Middle East and Asia Pacific. Moreover, increasing FADEC and advanced electronic system complexity is driving specialized technician training and strategic OEM-MRO partnerships, transforming the aftermarket landscape.

- For instance, in February 2024, Lufthansa Technik announced the expansion of its digital engine control component repair services, combining AI-based diagnostics with refurbished parts programs to deliver faster and more sustainable solutions to airline customers.

Download Free sample to learn more about this report.

Impact of Russia-Ukraine Conflict

The Russia & Ukraine conflict has had both major short-term and long-term effects on the commercial aircraft engine controls aftermarkets market. Russia sanctions have limited the availability of Western-produced aircraft parts, such as engine control systems, compelling Russian airlines to depend heavily on refurbished and utilize parts to maintain fleets running. Internationally, the conflict has interrupted supplies of semiconductors and raw materials essential for FADEC and electronic engine control components, resulting in increased lead times and prices of MRO services. Concurrently, increasing fuel and operating costs have compelled airlines globally to place greater emphasis on cost-saving refurbished parts and optimized maintenance cycles. This has indirectly heightened demand in some regions while limiting supply in others, creating dynamics.

Segmentation Analysis

By Component

FADEC Dominates the Segment Due to Its Primary Role in Modern Jet Engines

The component segment is divided by the FADEC Processor (dual-core module, dual-channel FADEC, and AI-integrated FADEC), thrust control sensor, fuel metering valve, start control unit, reverser actuator, hydraulic control unit, thrust lever encoder, fuel flow regulator, thrust reverser actuator, smart thrust resolver, fuel control unit, digital start controller, reverser control valve, fiber-optic thrust sensor, adaptive fuel controller, electric starter-generator, and composite reverser actuator.

The FADEC (Full Authority Digital Engine Control) processor segment holds the largest share in the commercial aircraft engine controls aftermarkets market. This is as it serves as the primary brain of modern jet engines, controlling thrust, fuel efficiency, emissions, and safety features. Modern fleets are nearly all FADEC-fitted, with more than 85% of commercial aircraft delivered after 2015 employing digital FADEC systems. Advanced FADEC configurations such as dual-core modules, dual-channel redundancy, and AI-based FADECs are critical for predictive maintenance, engine health monitoring, and meeting more stringent fuel efficiency and emissions regulations.

As worldwide fleets grow, the FADEC is the largest aftermarket demand segment, estimated at more than 26.82% of engine control MRO revenues in 2024, and the leading component segment.

For instance, in September 2023, Safran introduced its new FADEC 4 processor, offering 10X more computing power than the previous FADEC 3 systems to improve engine performance and efficiency on Airbus A320neo and Boeing 737 MAX aircraft.

To know how our report can help streamline your business, Speak to Analyst

By Offering

MRO Service Segment Dominates the Market due to the Need for High Frequency of Inspection

By offering, the market is fragmented into MRO Services and Refurbished Parts (USM and PMA) segments.

The MRO services segment dominates the commercial aircraft engine controls aftermarket market. This is due to airlines and operators needing to comply with strict regulatory mandates requiring regular inspection, calibration, repair, and replacement of FADEC processors, sensors, and actuators throughout an aircraft’s lifecycle. Unlike parts sales, which occur periodically, MRO services generate recurring demand tied to flight hours and maintenance cycles, making them a more consistent revenue stream. With global fleets expanding and aircraft utilization rising post-pandemic, the demand for timely MRO support is expected to grow further.

- For example, in July 2025, GE Aerospace increased its 2025 profit forecast, driven by soaring demand for aftermarket support services as airlines extend the lifespan of older aircraft and deliveries are delayed.

GE Aerospace commercial engine unit, which generates over 70% of its revenue from parts and services, reported its profit went up by 33% to be USD 2.23 billion and revenue by 30% to be USD 7.99 billion in Q2, highlighting MRO service demand is driving its financials.

By Aircraft Family

Boeing 737 Family (Classic/NG/MAX) Segment Dominates the Market due to its Widespread Use On Short-And Medium-Haul Routes

In terms of aircraft family, the market is segmented by Airbus A220 (ex-CSeries), Airbus A320 Family (ceo/neo), Airbus A330 (ceo/neo), Airbus A350, Airbus A380, ATR 42/72, Boeing 737 Family (Classic/NG/MAX), Boeing 747, Boeing 767, Boeing 777, Boeing 787, Bombardier CRJ Series, COMAC C919, De Havilland Dash 8 (Q-Series), Embraer E-Jets (E1/E2), and Sukhoi Superjet 100.

The Boeing 737 Family (Classic/NG/MAX) dominates the commercial aircraft engine controls aftermarkets market. As it represents the largest in-service commercial aircraft family globally, with over 8,000+ units in service worldwide. Its widespread use on short-and medium-haul routes makes it an ideal choice for many airlines and operators, leading to greater utilization rates and shorter maintenance cycles than its widebody counterparts. The combination of a large installed base, heavy flight usage, and stringent regulatory maintenance requirements continues to drive the strong demand for aftermarket MRO service and refurbished engine control parts within the Boeing 737 aftermarket.

- For instance, in January 2025, ST Engineering secured a five-year MRO contract to service the CFM LEAP-1B engines powering Korean Air’s Boeing 737 MAX fleet. The agreement includes quick-turn services and performance restoration visits at the Singapore facility, reinforcing its role as a Premier MRO provider within CFM’s open MRO ecosystem.

Commercial Aircraft Engine Controls Aftermarket Regional Outlook

By region, the market is studied across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

North America Commercial Aircraft Engine Controls Aftermarket Size, 2024 (USD Million) To get more information on the regional analysis of this market, Download Free sample

North America dominates the market due to its large installed base of Boeing and Airbus fleets, the robust OEM presence of companies such as GE Aerospace, Honeywell, and Collins, and modern MRO infrastructure. Europe is the second-largest market, propelled by the presence of key players such as Safran and Lufthansa Technik, and stringent regulatory standards that guarantee repeat demand for engine control maintenance.

Asia Pacific is the second-fastest growing region, driven by the speed of fleet growth in China, India, and Southeast Asia, where increasing low-cost carrier activity fuels MRO and used parts uptake.

The Middle East & Africa are anticipated to be the fastest-growing region, supported by strategically located MRO hubs in the UAE, Qatar, and Turkey, serving local and transit fleets. Latin America shows consistent growth, driven by fleet renewal and growing use of low-cost refurbished parts.

Overall, these dynamics reflect a mature Western aftermarket alongside strong growth potential in the Asia Pacific and the Middle East.

- For instance, in February 2025, Reuters, in its recent report, stated that Airbus, Collins Aerospace, Pratt & Whitney, and Rolls-Royce significantly increased parts sourcing from Indian suppliers such as Hical Technologies and JJG Aero to navigate Western supply disruptions. The Asia Pacific aerospace sector is thriving, with 2024 revenues expected to be 54% higher than 2019 levels, highlighting the region’s growing strategic importance in both manufacturing and MRO activities.

Competitive Landscape

Key Players Are Forging Long-Term Service Contracts to Boost Their Market Share

The commercial aircraft engine controls aftermarkets market is dominated by OEMs such as GE Aerospace, Pratt & Whitney, Safran, Collins Aerospace, and Honeywell. Their leadership is driven by control over proprietary software, global service networks, and long-term service contracts that help secure market share. Large independent MRO providers such as MTU Maintenance, Lufthansa Technik, ST Engineering, and StandardAero compete by offering faster turnaround times, flexible work scopes, and access to used serviceable materials, which are particularly attractive to operators managing mixed or aging fleets.

Niche repair shops and regional MROs focus on specialized component-level repairs, while parts suppliers such as Heico, Wencor, and TransDigm drive cost savings with PMA and refurbished components. Overall, OEMs maintain a competitive edge through lifecycle control and data ownership, while independent MROs and parts specialists’ firms' growth is driven by offering cost-effective, flexible, and sustainable aftermarket solutions.

LIST OF KEY Commercial Aircraft Engine Controls Aftermarkets PLAYERS Profiled

|

SR. No |

MRO Service & Refurbished Parts Company |

MRO Service Providers |

Refurbished Parts Suppliers |

|

|

1 |

Lufthansa Technik AG (Germany) |

Pratt & Whitney (RTX) (U.S.) |

Heico Aerospace (U.S.) |

|

|

2 |

MTU Aero Engines (Germany) |

GE Aerospace (U.S.) |

Wencor Group (U.S.) |

|

|

3 |

StandardAero (U.S.) |

Safran Aircraft Engines (Safran Nacelles) (France) |

TransDigm Group subsidiaries (U.S.) |

|

|

4 |

ST Engineering Aerospace (Singapore) |

Rolls-Royce plc. (U.K.) |

AAR Corp. (Parts Trading arm) (U.S.) |

|

|

5 |

SR Technics (Switzerland) |

Collins Aerospace (RTX) (U.S.) |

AvAir (U.S.) |

|

|

6 |

|

Honeywell Aerospace (U.S.) |

|

|

KEY INDUSTRY DEVELOPMENTS

- April 2025- Pratt & Whitney implemented 3D-printing technology to streamline repairs for its Geared Turbofan (GTF) engine components, slashing turnaround time by over 60%. The company projects to recover approximately USD 100 million worth of parts over the next five years and has expanded its MRO capacity through new agreements with MTU Aero Engines and Delta Tech Ops.

- March 2025- The Australian special report stated that the state of Queensland is rapidly positioning itself as a regional MRO hub. With over 300 aerospace firms already contributing to 31% of national MRO activity and nearly 18,400 aviation-related jobs, the region aims to capture more of the anticipated 4% annual fleet across the Asia Pacific market.

- August 2025- The Odisha state cabinet sanctioned the construction of an MRO facility at Biju Patnaik International Airport (BPIA), led by Air Works India. Backed by a USD 9.6 million incentive package and a USD 18 million investment, the facility, first of its kind in eastern India, is expected to play a pivotal role in supporting India’s projected growth in the aviation MRO sector.

- April 2022- Lufthansa Technik vastly expanded its AVIATAR health-monitoring portfolio for Boeing 737 NG fleets, enabling broader digital diagnostics and proactive shop visits.

- July 2024- GE Aerospace announced approx USD 1 billion investment over the next five years to expand and upgrade global MRO & component-repair facilities, boosting LEAP/CFM capacity and TAT.

REPORT COVERAGE

The research report delivers a detailed analysis of the market and emphasizes key aspects such as key players, offerings, objects, and end-users. Moreover, the report presents insights into commercial aircraft engine controls, aftermarket trends, competitive landscape, market dynamics, product pricing, regional analysis, market players, and competition landscape, while highlighting key drivers of industry growth. In addition to the factors stated above, the report encompasses several direct and indirect influences that have contributed to market sizing in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2045 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2045 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 3.4% from 2025 to 2045 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Component · FADEC Processor o Dual-Core Module o Dual-Channel FADEC o AI-Integrated FADEC · Thrust Control Sensor · Fuel Metering Valve · Start Control Unit · Reverser Actuator · Hydraulic Control Unit · Thrust Lever Encoder · Fuel Flow Regulator · Thrust Reverser Actuator · Smart Thrust Resolver · Fuel Control Unit · Digital Start Controller · Reverser Control Valve · Fiber-Optic Thrust Sensor · Adaptive Fuel Controller · Electric Starter-Generator · Composite Reverser Actuator |

|

By Offerings · MRO Services · Refurbished Parts o USM o PMA |

|

|

By Aircraft Family · Airbus A220 (ex-CSeries) · Airbus A320 Family (CEO/NEO) · Airbus A330 (CEO/NEO) · Airbus A350 · Airbus A380 · ATR 42/72 · Boeing 737 Family (Classic/NG/MAX) · Boeing 747 · Boeing 767 · Boeing 777 · Boeing 787 · Bombardier CRJ Series · COMAC C919 · De Havilland Dash 8 (Q-Series) · Embraer E-Jets (E1/E2) · Sukhoi Superjet 100 |

|

|

By Region · North America (By Component, By Offerings, By Aircraft Family, and By Country) o U.S. (By Component) o Canada (By Component) · Europe (By Component, By Offerings, By Aircraft Family, and By Country) o U.K. (By Component) o Germany (By Component) o France (By Component) o Russia (By Component) o Rest of Europe (By Component) · Asia Pacific (By Component, By Offerings, By Aircraft Family, and By Country) o China (By Component) o India (By Component) o Japan (By Component) o South Korea (By Component) o Rest of Asia-Pacific (By Component) · Middle East & Africa (By Component, By Offerings, By Aircraft Family, and By Country) o Saudi Arabia (By Component) o Israel (By Component) o Turkey (By Component) o Rest of the Middle East (By Component) · Latin America (By Component, By Offerings, By Aircraft Family, and By Country) o Brazil (By Component) o Rest of Latin America (By Component) |

Frequently Asked Questions

According to the Fortune Business Insights study, the global market was valued at USD 3,921.6 million in 2024 and is anticipated to be USD 8,114.5 million by 2045.

The market will likely grow at a CAGR of 3.4% over the forecast period (2025-2045).

The top ten players in the industry are Honeywell Aerospace, Safran Aerosystems, Liebherr-Aerospace, Collins Aerospace (Raytheon Technologies), Parker Aerospace, ST Engineering AAR Corp., Lufthansa Technik, SR Technics, Wencor Group, and HAECO Group are based on parameters such as Services Portfolio, Regional Presence, and Industry Experience.

North America dominates the market.

The global rise in need for MRO services is the key factor driving the growth of the market.

High certification costs and supply chain challenges are the key factors hindering market growth.

- 2019-2045

- 2024

- 2019-2023

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us