Commercial Vehicle Steel Wheels Market Size, Share & Industry Analysis, By Vehicle Type (Light Commercial Vehicles, Medium Commercial Vehicles, and Heavy Commercial Vehicles), By Rim Size (Up to 16 inches, 16-20 inches, and Above 20 inches), By Sales Channel (OEM and Aftermarket), By Manufacturing Process (Stamped Steel Wheels and Forged Steel Wheels), By Application (Freight Transportation, Passenger Transport, Construction Vehicles, Mining Vehicles, and Others), and Regional Forecasts, 2026-2034

Commercial Vehicle Steel Wheels Market Size and Future Outlook

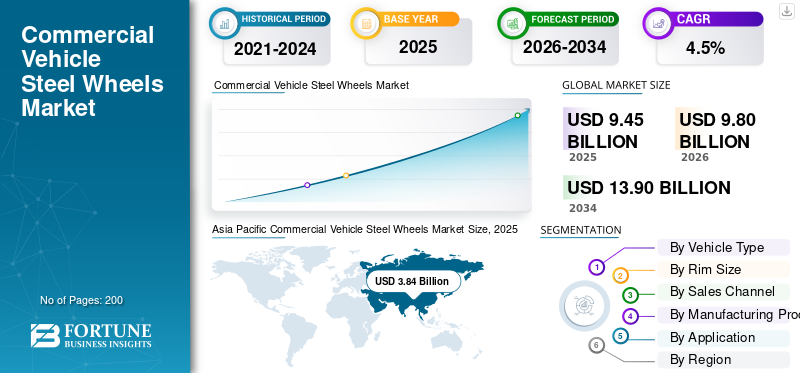

The commercial vehicle steel wheels market size was valued at USD 9.45 billion in 2025. The market is projected to grow from USD 9.80 billion in 2026 to USD 13.90 billion by 2034, exhibiting a CAGR of 4.5% during the forecast period. Asia Pacific dominated the commercial vehicle steel wheels market with a market share of 40.63% in 2025.

The market represents production and distribution of durable steel wheels used in commercial vehicles such as trucks, buses, and trailers. These wheels are essential components in heavy-duty transportation, supporting high load-bearing capacity and long operational life. The market is influenced by continuous advancements in wheel manufacturing, improvements in material strength, and evolving transportation needs across regions such as North America, Europe, Asia Pacific and Latin America.

The market is witnessing steady expansion, primarily due to the growing demand for logistics and freight transportation services. Rapid urbanization and industrialization in countries such as China and India are significantly contributing to the rising demand for commercial vehicles. As a result, the market is being driven by increased vehicle production, especially in the heavy commercial vehicle segment. Additionally, the expansion of e-commerce and supply chain networks has increased the need for reliable transportation, further strengthening demand for steel wheels.

From an application perspective, steel wheels are widely used across freight transportation, construction, mining, and passenger transport. Their durability and cost-effectiveness make them a preferred choice over alternative materials, especially in cost-sensitive markets. The aftermarket segment also plays a vital role, driven by replacement demand and maintenance requirements of existing vehicle fleets.

Looking ahead, the industry is expected to evolve with innovations in lightweight steel solutions and enhanced manufacturing processes. Increasing focus on fuel efficiency and operational performance will further influence product development. Leading key players, including companies such as Accuride Corporation and Maxion Wheels, are investing in advanced technologies and expanding their global footprint to strengthen their position in the market.

Download Free sample to learn more about this report.

COMMERCIAL VEHICLE STEEL WHEELS MARKET TRENDS

Shift Toward Lightweight and High-Performance Steel Wheel Solutions is Emerging Market Trend

A key trend in the market is the development of lightweight and high-performance steel wheels. Manufacturers are focusing on improving strength-to-weight ratio to enhance fuel efficiency and vehicle performance. This trend is gaining traction among key players such as Accuride Corporation, as fleets look to reduce operating costs. The trend supports rising demand for advanced products while maintaining durability in both OEM and aftermarket segment applications.

- For instance, in September 2024, Accuride unveiled its AeroLight concept at IAA Transportation and presented Europe’s lightest front axle and trailer wheel at 2 kg, highlighting the shift toward lighter, performance-oriented wheel solutions.

Download Free sample to learn more about this report.

MARKET DRIVERS

Expansion of Logistics and Freight Transportation Drives Market Growth

The rapid expansion of logistics networks and freight transportation is significantly contributing to the commercial vehicle steel wheels market growth. With increasing global trade and e-commerce activity, transportation fleets are expanding, particularly in the heavy commercial vehicle segment. This trend is driven by increased vehicle production and the need for durable components. As a result, demand for reliable steel wheels continues to rise, supporting overall market expansion and strengthening global supply chains.

- For instance, ITF (International Transport Forum) mentioned world trade volumes rose 2.9% in 2024 and air freight ton-kilometers increased 11.3%, reflecting stronger goods movement across freight networks that support CV wheel demand.

MARKET RESTRAINTS

Rising Raw Material Costs and Steel Price Volatility Restrain Market Growth

Fluctuations in steel prices pose a major challenge to the market. Since steel is the primary raw material in wheel manufacturing, price volatility directly affects production costs and profit margins. This can discourage expansion and investment by key players, especially in cost-sensitive regions. As a result, unstable pricing conditions may slow down the growth of market and impact long-term planning across global supply chains.

- For instance, in April 2024, worldsteel said the industry had faced two years of negative growth and severe market volatility since the COVID crisis, underlining raw-material uncertainty for steel-intensive manufacturing sectors such as wheel production.

MARKET OPPORTUNITIES

Growing Infrastructure Development in Emerging Economies Creates Market Opportunities

Infrastructure development across countries including India and China is creating strong opportunities in the market. Increasing investments in construction, mining, and transportation projects are boosting demand for heavy commercial vehicle fleets. This leads to higher consumption of steel wheels, particularly in developing regions across North America, Europe, Asia Pacific, and Latin America. Such developments are expected to accelerate market expansion and increase the adoption of advanced wheel solutions.

- For instance, in 2024, India’s Budget documents allocated USD 3,421.68 to the Ministry of Road Transport and Highways, including support for highways and multimodal logistics parks, which can stimulate CV deployment and wheel demand.

MARKET CHALLENGES

Competition from Alternative Materials Such as Alloy Wheels Challenges Market Growth

The increasing adoption of alternative materials such as aluminum alloy wheels presents a challenge to the market expansion. While steel wheels remain dominant due to cost advantages, alloy wheels offer benefits such as reduced weight and improved fuel efficiency. This creates competitive pressure for traditional wheel manufacturing companies and may limit the growth of the market in certain premium applications.

- For instance, in September 2024, Maxion Wheels introduced its first forged aluminum truck wheels at IAA Transportation 2024, showing that lightweight alternative wheel materials are becoming stronger competitors in selected commercial applications.

Segmentation Analysis

By Vehicle Type

Heavy Commercial Vehicles Dominate Due to Higher Load and Wheel Requirements

On the basis of vehicle type, the market is segmented into light commercial vehicles, medium commercial vehicles, and heavy commercial vehicles.

The heavy commercial vehicle segment held the largest commercial vehicle steel wheels market share due to higher wheel count, larger rim sizes, and extensive usage in freight and industrial applications. These vehicles contribute significantly to the market as they require durable components for long-haul operations. The dominance is further supported by growing demand from logistics and construction sectors, especially in countries including China and India, where commercial activity is expanding rapidly.

- For instance, Maxion Wheels on its official website mentions it sells more than 10 million truck and trailer steel wheels a year and supplies nearly every major commercial vehicle producer, underscoring the scale of HCV and trailer-linked demand.

Medium commercial vehicles segment is expected to grow at a CAGR of 3.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Rim Size

Above 20 Inches Segment Dominates Due to Heavy-Duty Vehicle Demand

On the basis of rim size, the market is segmented into up to 16 inches, 16-20 inches, and above 20 inches.

The above 20 inches segment dominates due to its extensive use in heavy commercial vehicle and trailer applications. Larger wheels are essential for load-bearing capacity and durability, making them critical in freight and construction sectors. The segment benefits from rising demand in logistics and mining industries, contributing to overall market expansion across regions including North America, Europe, Asia Pacific, and Latin America.

- For instance, in September 2024, Accuride presented Europe’s lightest 22.5 x 9.00 truck wheel, showing continued product development around large-diameter truck wheels used in heavy-duty commercial applications.

The 16-20 inches segment is expected to grow at a CAGR of 3.4% over the forecast period.

By Sales Channel

OEM Segment Dominates Due to Strong Vehicle Production and Supply Contracts

On the basis of sales channel, the market is segmented into OEM and aftermarket.

The OEM segment dominates the market due to strong alignment with vehicle production cycles. As the market is driven by increased vehicle production, OEM demand remains high across all regions. Manufacturers establish long-term contracts with automakers, ensuring consistent supply. The segment is particularly strong in developing regions where new vehicle sales are increasing rapidly, strengthening global supply chains.

Aftermarket segment is expected to grow at a CAGR of 2.8% over the forecast period.

By Manufacturing Process

Stamped Steel Wheels Dominate Due to Cost Efficiency and Mass Production Capability

On the basis of manufacturing process, the market is segmented into stamped steel wheels and forged steel wheels.

Stamped steel wheels dominate due to their cost-effectiveness and scalability in wheel manufacturing. They are widely used across both light commercial vehicle and heavy commercial vehicle segments due to their durability and affordability. The process supports high-volume production, making it suitable for global markets.

- For instance, in April 2024, Topy Industries showcased its Brilliant Wheel, described as Japan’s first steel wheel for commercial vehicles with a three-layer coating structure, demonstrating continuing innovation within steel wheel production.

The forged steel wheels segment is expected to grow at a CAGR of 7.3% over the forecast period.

By Application

Freight Transportation Dominates Due to Expanding Logistics and E-Commerce Activities

On the basis of application, the market is segmented into freight transportation, passenger transport, construction vehicles, mining vehicles and others.

Freight transportation dominates the market as it represents the largest application of commercial vehicles. The surge in logistics operations and e-commerce has led to a growing demand for transportation fleets. This segment drives both OEM and aftermarket segment demand, contributing significantly to market expansion across global regions.

Construction vehicles segment is expected to grow at a CAGR of 4.7% over the forecast period.

Commercial Vehicle Steel Wheels Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America and Middle East & Africa.

Asia Pacific

Asia Pacific Commercial Vehicle Steel Wheels Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valuing at USD 3.84 billion, and also maintained the leading share in 2024, with USD 3.75 billion. Asia Pacific dominates the market as countries including China and India combine large truck production, expanding logistics fleets, and heavy infrastructure activity. The region is being driven by increased vehicle production, especially in heavy commercial vehicle applications, while local wheel manufacturing ecosystems support cost-efficient supply. Strong freight movement, construction spending, and replacement demand together sustain market expansion and reinforce the region’s leadership across global market.

- For instance, in January 2025, SIAM Director General said India’s passenger vehicles, commercial vehicles, and three-wheelers posted their highest ever Q3 sales, pointing to strong transport demand in one of APAC’s core commercial vehicle markets.

China Commercial Vehicle Steel Wheels Market

China’s market is projected to be one of the largest globally, and in 2025 it reached USD 2.32 billion, representing 24.6% of market.

India Commercial Vehicle Steel Wheels Market

India market in 2025 reached USD 0.52 billion, accounting for 5.5% of global revenues.

North America

North America market is estimated to reach USD 3.31 billion in 2026 and secure the position of the second-largest region in the market. North America is expected to grow steadily due to strong freight movement, trailer demand, and replacement activity in the aftermarket segment. The region benefits from mature supply chains, fleet renewal, and steady OEM demand for both light commercial vehicle and heavy commercial vehicle platforms. The U.S. remains the core growth engine due to its scale in pickups, vans, heavy trucks, and trailers, which together support a broad installed base for steel wheels.

U.S. Commercial Vehicle Steel Wheels Market

Based on North America’s strong contribution, the U.S. market reached USD 2.61 billion in 2025, representing 34.0% of the market.

Europe

Europe is projected to record a growth rate of 4.1% in the coming years, and reach a valuation of USD 0.36 billion by 2026. Europe will grow at a steady rate, supported by fleet replacement, trailer activity, and demand for durable wheels in logistics and bus operations. Growth is likely to remain selective, with Spain outperforming some major markets in trucks while bus registrations also improved.

Germany Commercial Vehicle Steel Wheels Market

Germany market in 2025 reached at USD 0.27 billion, accounting for 2.8% of global revenues.

U.K. Commercial Vehicle Steel Wheels Market

The U.K. market in 2025 was at USD 0.21 billion, accounting for 2.2% of global sales.

Latin America

Latin America is projected to record a growth rate of 4.6% in the coming years, and reach a valuation of USD 0.59 billion by 2026. Latin America is likely to see gradual growth as freight, agriculture, mining, and construction keep commercial fleets active. Brazil remains the region’s main anchor, while Argentina and other markets support replacement demand.

Middle East & Africa

Middle East & Africa is projected to record a growth rate of 5.9% in the coming years, and reach a valuation of USD 0.42 billion by 2026. Middle East & Africa market grows through logistics corridor investments, construction activity, mining exposure, and selective fleet renewal. Turkey and South Africa are the clearest production anchors, while Gulf markets support replacement demand through transport and infrastructure projects.

COMPETITIVE LANDSCAPE

Key Industry Players

Increasing Focus of Key Players on Improving Reach and Innovation Influences Market Competition

The competitive landscape of the market is defined by manufacturers that combine large-scale wheel manufacturing capacity, deep OEM relationships, technical product development, and resilient supply chains. Competition is strongest among companies that can serve multiple vehicle type categories, from light commercial vehicle platforms to heavy commercial vehicle applications, while also supporting fleets and distributors in the aftermarket segment. Leading key players are strengthening their positions through plant expansion, lighter-weight wheel designs, corrosion-resistant coatings, and region-specific product portfolios aligned with regulations and fleet operating conditions. Public company information from Accuride Corporation and Maxion Wheels shows that the market is highly driven by OEM programs, commercial fleet needs, and global truck-and-trailer demand.

Accuride Corporation emphasizes its role as a single-source supplier for OEMs, fleets, and distributors, while Maxion Wheels highlights its global manufacturing footprint and supply capability to nearly every major truck and trailer OEM. This indicates that competitive strength depends not only on pricing, but also on engineering support, coating technology, delivery reliability, and the ability to adapt products for regional demand across different regions. As the industry sees growing demand and rising demand for commercial transport, companies that can localize production and secure raw materials are better positioned for market expansion and long-term gains market.

Moreover, Maxion Wheels is commercializing lower-CO2 and lightweight steel wheel options, while suppliers such as Accuride Corporation continue to stress lightweight and durable wheel solutions for OEM and replacement channels. In practical terms, the market is being driven by increased vehicle production in freight, trailer, and industrial applications, especially in countries such as China and India, where logistics and infrastructure activity continue to expand.

LIST OF KEY COMMERICAL VEHICLE STEEL WHEELS COMPANIES PROFILED

- Maxion Wheels (Brazil)

- Accuride Corporation (U.S.)

- Topy Industries Ltd. (Japan)

- Wheels India Ltd. (India)

- Steel Strips Wheels Ltd. (India)

- Jingu Company (China)

- Mefro Wheels GmbH (Germany)

- Central Motor Wheel of America, Inc. (U.S.)

- Jantsa Jant Sanayi ve Ticaret A.S. (Turkey)

- Gianetti Ruote S.r.l. (Italy)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Steel Strips Wheels announced continued expansion of its global OEM business, highlighting increasing participation in international commercial vehicle programs, particularly in truck and trailer wheel segments.

- December 2025: Steel Strips Wheels confirmed new export orders for trailer wheel segments in the U.S. worth USD 1 million, marking renewed engagement with American OEM and aftermarket customers.

- October 2025: Maxion Wheels showcased its full commercial vehicle wheel portfolio at SOLUTRANS, including heavy-duty steel wheels designed for truck and trailer applications. The company highlighted wheels engineered for high load-bearing capacity, durability, and compatibility with larger rim sizes (20+ inches), aligning with increasing demand in freight transportation and long-haul logistics segments.

- September 2025: Steel Strips Wheels secured a major export order from a European OEM, with supply expected from its Chennai facility, reinforcing its role in long-term OEM programs.

- July 2025: Accuride announced improvements to its Steel Armor corrosion protection coating, with upgraded products shipping from the U.S. and Mexico facilities to improve durability and lifecycle performance.

- April 2025: Maxion Wheels presented advanced truck and trailer steel wheel solutions at Transport Logistic in Munich. The showcased products emphasized high-strength steel construction, optimized weight design, and corrosion-resistant coatings, tailored for heavy commercial vehicles. These specifications support enhanced performance, longer lifecycle, and efficiency in demanding logistics and supply chain operations.

- January 2025: Wheels India announced improved profitability in Q3 FY2024-25, supported by stable demand in commercial vehicles and industrial segments, including truck and bus wheel production.

REPORT COVERAGE

The commercial vehicle steel wheels market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, Rim Size, Sales Channel, Manufacturing Process, Application, and Region |

| By Vehicle Type |

|

| By Rim Size |

|

| By Sales Channel |

|

| By Manufacturing Process |

|

| By Application |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 9.45 billion in 2025 and is projected to reach USD 13.90 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 3.84 billion.

The market is expected to exhibit a CAGR of 4.5% during the forecast period of 2026-2034.

Heavy commercial vehicles segment led the market by vehicle type.

Expansion of logistics and freight transportation is driving the market growth.

Maxion Wheels, Accuride Corporation, Topy Industries Ltd. and Jingu Company are some of the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us