Complement Inhibitors Market Size, Share & Industry Analysis, By Drug (Eculizumab, Ravulizumab, Pegcetacoplan, Iptacopan, Sutimlimab, Avacincaptad pegol, & Others), By Disease Indication (PNH, Atypical Hemolytic Uremic Syndrome, Generalized Myasthenia Gravis, Geographic Atrophy, Cold Agglutinin Disease), By Age Group, By Type (Branded, Biosimilar, & Others), By Target Pathway Inhibitors (C5, C3, C1s, Factor B, Factor D, & Others), By Route of Administration, By Distribution Channel (Hospital Pharmacies, Drug Stores, Retail/Online Pharmacies, & Others), & Regional Forecast, 2026-2034

Complement Inhibitors Market Size and Future Outlook

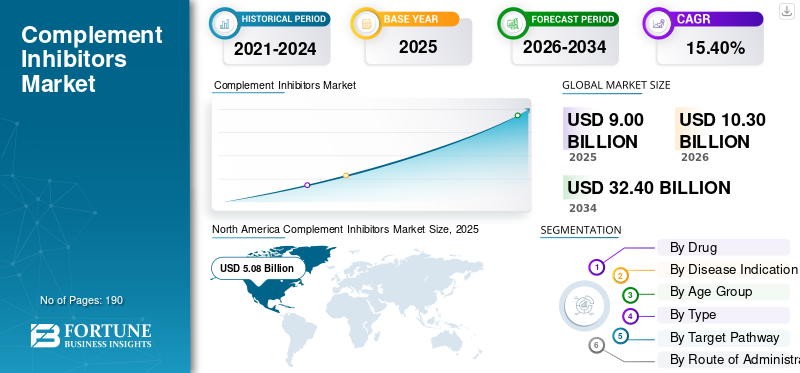

The global complement inhibitors market size was valued at USD 9.00 billion in 2025. The market is projected to grow from USD 10.30 billion in 2026 to USD 32.40 billion by 2034, exhibiting a CAGR of 15.40% during the forecast period. North America dominated the complement inhibitors market with a market share of 56.44% in 2025.

The global complement inhibitors market is witnessing steady growth as drug developers expand the use of complement-targeting therapies beyond rare blood disorders into kidney, neurology, and other immune-mediated diseases. This is increasing the market's commercial potential as broader approved use across multiple indications helps companies reach larger patient pools and strengthen long-term revenue visibility. At the same time, continued innovation in C5, C3, Factor B, and Factor D targeting is improving treatment choice, dosing convenience, and disease control, which is supporting wider physician adoption and sustaining market expansion.

- For instance, in March 2026, Novartis showcased positive results from final two-year Phase III APPLAUSE-IgAN that reported Fabhalta (iptacopan) slowed kidney function decline in IgA nephropathy, while also noting FDA priority review for traditional approval in this indication. This development reflects how companies in the market are expanding complement inhibitors into broader, high-value renal indications, which can accelerate the global market growth by increasing addressable demand beyond traditional rare-disease use.

Furthermore, key players, such as Alexion Pharmaceuticals, Inc., Novartis AG, F. Hoffmann-La Roche Ltd, and Apellis Pharmaceuticals, Inc., are expanding their product offerings in the market.

Download Free sample to learn more about this report.

COMPLEMENT INHIBITORS MARKET TRENDS

Expansion of Complement Inhibitors into Broader Disease Indications is a Prominent Trend Observed

A key global market trends observed is the expansion of complement inhibitors into broader disease indications. As clinical success extends beyond traditional indications such as PNH and aHUS, companies are actively positioning complement inhibitors in diseases with higher patient volumes and longer treatment durations. This creates a cause-and-effect growth pattern: wider label expansion increases physician awareness and patient eligibility, which in turn improves commercial adoption and encourages further pipeline investment. As a result, the market is gradually shifting from a limited orphan-drug segment toward a more diversified immunology and nephrology opportunity.

- For instance, in March 2025, Novartis announced that Fabhalta (iptacopan) received U.S. FDA approval for C3 glomerulopathy (C3G), making it an approved treatment for this condition. This development shows how companies in the market are extending complement inhibition into new renal indications, which supports market expansion by opening additional treatment pathways beyond established hematology use.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Approvals of Complement-Targeted Therapies Across Rare and Chronic Diseases is Driving Market Growth

The complement inhibitors market growth is being driven by rising approvals, as regulatory success directly enhances product credibility and accelerates treatment adoption in clinical practice. When more complement inhibitors receive approval for different diseases, companies gain access to larger patient pools and create stronger long-term revenue opportunities. This also reduces dependence on a single indication and helps the market expand from highly specialized rare disorders into chronic disease settings with wider demand. In turn, growing approval momentum is attracting more pipeline investment and increasing competitive activity across the complement pathway space.

Moreover, key companies are focusing on regulatory approvals and new product launches to strengthen their market position.

- For instance, in August 2024, F. Hoffmann-La Roche Ltd received approval from the European Commission for PiaSky (crovalimab), indicated for people with Paroxysmal Nocturnal Hemoglobinuria (PNH), describing it as the first monthly subcutaneous treatment for this condition in the European Union. This development supports improved treatment convenience, which can help broaden physician uptake and patient acceptance.

MARKET RESTRAINTS

High Therapy Cost and Reimbursement Pressure Limiting Wider Access Restricts Market Growth

A major market restraint is the high therapy cost and reimbursement pressure. Complement inhibitors are often used as long-term or lifelong therapies, so their budget impact becomes very high even when patient numbers are small. This creates a cause-and-effect challenge for the market: when treatment cost is extremely high, payers apply tighter reimbursement controls, health technology assessment bodies demand stronger value evidence, and some patients face delayed or limited access. As a result, commercial uptake can remain narrower than the actual clinical need, which restrains broader market growth.

- For instance, a recent article in Health Technology Assessment on atypical hemolytic uraemic syndrome highlighted that eculizumab costs about USD 409 per adult patient per year in the U.K., and the study specifically examined whether stopping lifelong therapy with monitoring could be a safer and more cost-effective alternative given this high cost burden.

MARKET OPPORTUNITIES

Strong Pipeline Development Across Multiple Complement Targets Creating Future Expansion Opportunities for Market

A major market growth opportunity is the strong pipeline development across multiple complementary targets. This creates an opportunity as broader target diversification reduces dependence on a single mechanism and increases the likelihood of addressing different disease biology more effectively. When companies develop therapies against targets such as Factor B, Factor D, C1q, C3, and C5, they can expand into new indications across nephrology, neurology, ophthalmology, and hematology. This creates a cause-and-effect growth pattern: a broader scientific pipeline increases the likelihood of differentiated products, which in turn attract more investment, support more clinical programs, and improve the market’s long-term expansion potential. In turn, this helps the market move from a narrow orphan-drug category toward a more diversified specialty-care opportunity.

- For instance, in May 2025, Annexon announced presentations at the 2025 ARVO Annual Meeting showing neuroprotective effects of ANX007, its C1q inhibitor, including evidence of benefit against inflammation and neuronal damage across diseases. This development is important for the market as it shows that complement inhibition is expanding beyond traditional blood disorders into neuroinflammatory and ophthalmic settings, potentially opening new high-value treatment opportunities and strengthening future market growth.

MARKET CHALLENGES

Maintaining Regulatory Compliance and Manufacturing Quality Across Markets Poses a Challenge to Market Growth

The major challenge faced by the market is maintaining consistent regulatory compliance and manufacturing quality across different regions. As companies expand branded generic portfolios across multiple countries, they must meet strict approval, bioequivalence, labeling, and plant-quality requirements in each market. This makes operations more complex and increases the risk of delays, remediation costs, warning letters, or product recalls when quality systems fall short. These factors can result in supply disruptions, higher compliance spending, and reputational pressure, slowing portfolio expansion and reducing the commercial momentum of branded generics.

- For instance, in April 2025, Arab Times published an article titled ‘Dozens of life-saving drugs pulled for violating safety standards ‘, reporting that nearly 40 medicines made by Glenmark Pharmaceuticals were recalled in the U.S. due to manufacturing practice concerns at its India facility. Such instances can trigger regulatory action and create additional pressure on companies operating in the generics space.

Segmentation Analysis

By Drug

Broader Lifecycle Expansion of Ravulizumab Led Segmental Growth

Based on drug, the market is categorized into eculizumab, ravulizumab, pegcetacoplan, iptacopan, sutimlimab, avacincaptad pegol, and others.

Among these, the ravulizumab dominated the complement inhibitors market share. The high share is allocated to the segment as the drug has demonstrated clinical efficacy earlier than C5 inhibition, offers a longer dosing interval, broadens its lifecycle across major complement-mediated diseases, and provides greater efficiency. These factors helped improve physician confidence and made it easier for treatment centers to continue using a familiar mechanism with a more convenient maintenance schedule. As a result, ravulizumab strengthened its commercial position in core high-value indications and captured a strong share within the branded complement inhibitor space.

- For instance, in January 2025, AstraZeneca presented positive long-term ALPHA Phase III data showing that Voydeya, as an add-on to Ultomiris or Soliris, maintained clinical improvements in patients with PNH experiencing clinically significant extravascular hemolysis. This underscores Ultomiris's continued centrality in the treatment pathway, reinforcing ravulizumab’s strong market position.

The others segment is expected to grow at a CAGR of 28.67% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

Early Approval of Complement Inhibitors for PNH Diseases Led to Dominance of Segment

Based on disease indication, the market is segmented into paroxysmal nocturnal hemoglobinuria (PNH), atypical hemolytic uremic syndrome (aHUS), generalized myasthenia gravis, neuromyelitis optica spectrum disorder, geographic atrophy, cold agglutinin disease, and others.

In 2025, the Paroxysmal Nocturnal Hemoglobinuria (PNH) dominated the market as it is one of the earliest and most clinically established indications for complement inhibition. Due to these factors, the segment has a much longer commercialization runway than newer indications. Since PNH is directly driven by uncontrolled complement activity and carries serious risks, such as hemolysis and thrombosis, complement inhibitors have become deeply embedded in its treatment pathway. As a result, the disease generated strong demand, early adoption, and sustained use for premium complement-targeted therapies.

- For instance, in June 2025, Novartis AG presented data in the New England Journal of Medicine and reported that Fabhalta delivered statistically significant and clinically meaningful improvements in hemoglobin in a new patient population with PNH in the APPULSE-PNH study.

The others segment is projected to grow at a CAGR of 30.82% during the forecast period.

By Age Group

Commercialized and Subsequently Studied More Broadly in Adult Patient Populations Boosted Segmental Growth

Based on age group, the market is segmented into pediatric and adults.

In 2025, the adults segment dominated the market based on age group. The high share is allocated to the segment as most approved complement inhibitors were first commercialized and subsequently studied more broadly in adult patient populations across hematology, nephrology, neurology, and ophthalmology. These factors created a larger treated base, stronger prescribing familiarity, and faster commercial uptake among adults, contributing to a higher share.

- For instance, in March 2026, UCB showcased a positive CHMP opinion for a new ZILBRYSQ pre-filled pen for adults living with generalized myasthenia gravis in Europe. Such instances show how ongoing product optimization and label support continue to focus heavily on adult populations, reinforcing the segment’s dominant market position.

The pediatric segment is projected to grow at a CAGR of 16.10% during the forecast period.

By Type

Strong Clinical Differentiation Boosted Segmental Growth of Branded Therapies

Based on type, the market is segmented into branded, biosimilar, and others.

In 2025, the branded type dominated the market as complement inhibitors are a highly specialized therapy. These therapy classes are led mainly by innovative originator drugs with orphan positioning, strong clinical differentiation, and premium pricing. Since these therapies require extensive development, specialist education, and post-marketing safety infrastructure, branded manufacturers have retained stronger commercial control than biosimilar competition. Key pharmaceutical companies are focusing on strategic collaborations and expanding their offerings in the market.

- For instance, in April 2023, Astellas Pharma Inc. and Iveric Bio, Inc. entered into a definitive agreement to acquire Iveric Bio. The development provided the company access to ACP, a complementary C5 inhibitor, an investigational drug for GA secondary to AMD.

The biosimilar segment is projected to grow at a CAGR of 32.39% during the forecast period.

By Target Pathway

Clinical Validation of C5 Inhibitors Boosted Segmental Growth

Based on target pathway, the market is segmented into C5 inhibitors, C3 inhibitors, C1s inhibitors, Factor B inhibitors, Factor D inhibitors, and others.

In 2025, the C5 inhibitors dominated the market as they were the first complement-targeted therapies to achieve broad clinical validation and regulatory success across multiple major indications. This early lead created a strong cause-and-effect advantage: earlier approvals built physician trust, physician trust supported wider adoption, and wider adoption encouraged further investment in additional C5-based products and lifecycle extensions. As a result, C5 inhibition remained the largest and most established target pathway in the market.

- For instance, in December 2023, UCB received European Commission approval for ZILBRYSQ, a C5 inhibitor for generalized myasthenia gravis. This development highlights how C5 continued to attract new product entries and indication expansion, helping the pathway maintain its leading share.

The factor B inhibitors segment is projected to grow at a CAGR of 28.44% during the forecast period.

By Route of Administration

Increasing Use of Intravenous Administration for Controlled Administration to Boost Segmental Growth

Based on route of administration, the market is segmented into intravenous, subcutaneous, intravitreal, and others.

In 2025, intravenous segment dominated the market. Leading complement inhibitors were initially introduced as infusion-based therapies in hospital-led settings for rare diseases. This gave IV treatment a first-mover advantage, especially in serious conditions where physicians preferred controlled administration, close monitoring, and established infusion protocols. As a result, IV therapy built the largest installed base before newer subcutaneous or intravitreal options began expanding.

- For instance, in March 2024, AstraZeneca announced FDA approval of Ultomiris for NMOSD, noting that the drug is administered intravenously every 8 weeks in adults after a loading dose. This reflects the continued expansion of major complementary therapies through IV-based treatment pathways, supporting the dominance of the intravenous segment.

The intravitreal segment is projected to grow at a CAGR of 23.57% during the forecast period.

By Distribution Channel

Safety Requirements such as Vaccination Protocols and REMS-Linked Controls Led to Hospital Pharmacies Segmental Dominance

Based on distribution channel, the market is segmented into hospital pharmacies, specialty pharmacies, drug stores & retail pharmacies, online pharmacies, and others.

By distribution channel, the hospital pharmacies dominated the market as complement inhibitors are high-cost specialty therapies used in severe diseases that are usually diagnosed, initiated, and monitored in specialist care settings. In addition, safety requirements such as vaccination protocols, REMS-linked controls, and infusion or supervised initiation pathways make hospital-based dispensing more practical than mass retail distribution. As a result, hospital pharmacies became the primary channel for accessing and managing these therapies.

- For instance, in November 2024, Recordati announced the completion of the acquisition of the global rights to Enjaymo, strengthening its rare disease franchise. This development aligns with the hospital-pharmacy dominance trend as rare disease biologics such as complement inhibitors are typically commercialized through specialist hospital-centered treatment networks rather than broad retail channels.

The online pharmacies segment is projected to grow at a CAGR of 23.42% over the study period.

Complement Inhibitors Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Complement Inhibitors Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 4.60 billion and maintained its leading position in 2025 at USD 5.08 billion. The market is growing strongly in North America as the region continues to lead in regulatory approvals, rare-disease diagnosis, and the adoption of premium specialty therapies, which directly support higher market uptake.

U.S. Complement Inhibitors Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated to be valued at around USD 5.37 billion in 2026, accounting for roughly 52.10% of the global market.

Europe

Europe is projected to grow at 14.64% over the coming years, the second-highest among all regions, and reach a valuation of USD 2.47 billion by 2026. The market is growing in Europe as the region sees steady approval of newer complement inhibitors, along with broader treatment options for physicians and patients.

U.K Complement Inhibitors Market

The U.K. market is estimated to be valued at around USD 0.49 billion in 2026, representing roughly 4.74% of the global market.

Germany Complement Inhibitors Market

Germany's market is projected to reach a valuation of approximately USD 0.55 billion in 2026, equivalent to around 5.34% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 1.52 billion in 2026 and secure the position of the third-largest region in the market. The market is growing as China and Japan are moving faster on approvals and launches of complement inhibitors.

Japan Complement Inhibitors Market

The Japanese market is estimated at around USD 0.36 billion in 2026, accounting for approximately 3.53% of the global market.

China Complement Inhibitors Market

China's market is projected to be one of the largest globally, with 2026 revenues estimated at around USD 0.56 billion, representing approximately 5.48% of global sales.

India Complement Inhibitors Market

The Indian market is estimated at around USD 0.18 billion in 2026, accounting for roughly 1.72% of global revenue.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The market in Latin America is estimated to reach a valuation of USD 0.32 billion during the forecast period. The market in Latin America is growing as reimbursement and public-sector inclusion for high-cost, rare-disease drugs are gradually improving.

GCC Complement Inhibitors Market

The GCC market is set to reach USD 0.07 billion in 2026.

South Africa Complement Inhibitors Market

The South African market is projected to reach approximately USD 0.04 billion by 2026, accounting for roughly 0.40% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Expansion into New Clinical Indications to Propel Market Progress

The global complement inhibitors market reflects a competitive structure with significant market consolidation, with companies such as Alexion Pharmaceuticals, Inc., Novartis AG, F. Hoffmann-La Roche Ltd, Apellis Pharmaceuticals, Inc., UCB S.A., and Amgen Inc. holding significant market share. Presence of legacy products, expansion into new clinical indications, key regulatory approvals, and the launches of newer complement-targeted therapies across hematology, neurology, nephrology, and ophthalmology is projected to bolster the market shares of these companies in the market.

- For instance, in October 2023, UCB, a global biopharmaceutical company, received U.S. FDA approval for ZILBRYSQ, a C5 inhibitor for the treatment of generalized myasthenia gravis (gMG) in adult patients who are anti-acetylcholine receptor (AChR) antibody-positive.

Other notable players in the global market include Regeneron Pharmaceuticals, Inc., Omeros Corporation, and Annexon, Inc. These companies are expected to strengthen their market share in the global market, particularly through pipeline development and emerging complement-pathway programs. These companies are focusing on strategic collaborations, clinical expansion into additional complement-mediated diseases, and new product launches to bolster their market positions over the forecast period.

LIST OF KEY COMPLEMENT INHIBITORS COMPANIES PROFILED IN REPORT

- Alexion Pharmaceuticals, Inc. (U.S.)

- Novartis AG (Switzerland)

- Hoffmann-La Roche Ltd (Switzerland)

- Apellis Pharmaceuticals, Inc. (U.S.)

- UCB S.A. (Belgium)

- Amgen Inc. (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Omeros Corporation (U.S.)

- Annexon, Inc. (U.S.)

- BioCryst Pharmaceuticals, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Royalty Pharma plc announced a research and development (R&D) co-funding agreement with Johnson & Johnson for a total of USD 500.0 million to advance the development of JNJ-4804, an investigational complementary interleukin‑23 (IL‑23) inhibitor medicine for autoimmune diseases.

- December 2025: Akebia Therapeutics, Inc. announced the establishment of its rare kidney disease pipeline, comprising two core product candidates: ADX-097, a next-generation complement inhibitor, and praliciguat, a soluble guanylate cyclase (sGC) stimulator.

- August 2025: AstraZeneca Pharma India Ltd announced that it will launch Eculizumab (Soliris) in India. The company received the import and market permission for it from the Drugs Controller General of India (DCGI) in January under Form CT-20.

- June 2025: Sanofi received orphan drug designation to riliprubart, a monoclonal antibody that selectively inhibits activated C1S in the classical complement pathway for people with chronic inflammatory demyelinating polyneuropathy (CIDP) from the Ministry of Health, Labor, and Welfare (MHLW) in Japan.

- September 2022: Asahi Kasei Pharma Corp. and Swedish Orphan Biovitrum Japan Co., Ltd. collaborated in Japan on pegcetacoplan, a complement C3 inhibitor for paroxysmal nocturnal hemoglobinuria (PNH), and avatrombopag, an agent for improving thrombocytopenia associated with chronic liver disease.

REPORT COVERAGE

The market report provides a detailed global complement inhibitors market analysis across key drug types, disease indications, age groups, target pathways, routes of administration, and distribution channels. It explains how the market is evolving as complement-targeted therapies gain wider use in rare hematologic, neurologic, renal, and ophthalmic disorders. The report also examines how innovation in drug design, broader regulatory approvals, and increasing clinical adoption are supporting market expansion across major regions. The report coverage includes detailed analysis of market size and forecast, competitive landscape, pipeline and product positioning, and regional growth trends. It further highlights the main factors driving market growth, the restraints affecting wider adoption, the emerging opportunities across newer disease areas, and the challenges linked to safety monitoring, treatment cost, and access. In addition, the study covers company profiling, recent product approvals, partnerships, acquisitions, and other strategic developments shaping the market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 15.40% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Drug, Disease Indication, Age Group, Type, Target Pathway, Route of Administration, Distribution Channel, and Region |

| By Drug |

|

| By Disease Indication |

|

| By Age Group |

|

| By Type |

|

| By Target Pathway |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 9.00 billion in 2025 and is projected to reach USD 32.40 billion by 2034.

In 2025, North America’s market value stood at USD 5.08 billion.

The market is expected to grow at a CAGR of 15.40% over the forecast period of 2026-2034.

The ravulizumab drug segment is expected to lead the market.

The market is driven by rising approval of complement-targeted therapies across rare and chronic diseases.

Alexion Pharmaceuticals, Inc., Novartis AG, F. Hoffmann-La Roche Ltd, Apellis Pharmaceuticals, Inc., and UCB S.A. are the top players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us