Computer Vision in Healthcare Market Size, Share & Industry Analysis, By Product Type (Hardware {Smart Cameras, Sensors, Memory Devices, and Others}, Software, and Services), By Application (Medical Imaging, Patient Monitoring, Surgical Assistance, Diagnostic Assistance, and Others), By End User (Hospitals & Specialty Clinics, Diagnostic Centers, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

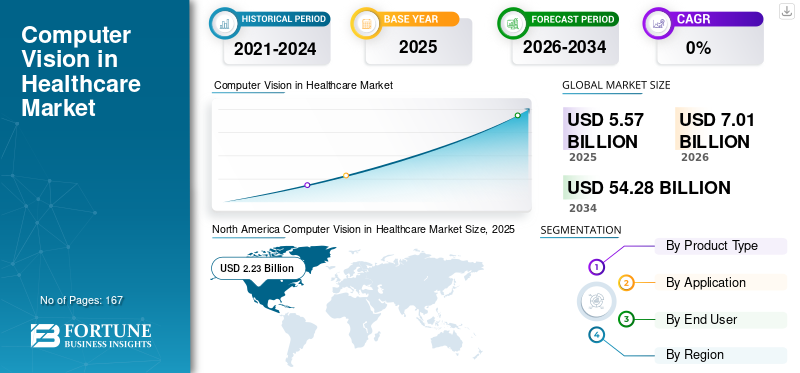

The global computer vision in healthcare market size was valued at USD 5.57 billion in 2025. The market is projected to grow from USD 7.01 billion in 2026 to USD 54.28 billion by 2034, exhibiting a CAGR of 29.17% during the forecast period. North America dominated the global computer vision in healthcare market with a market share of 40.03% in 2025.

The computer vision in healthcare market is projected to witness exponential growth in the coming years, driven by the rising burden of diseases and increasing global demand for precise diagnostics and patient management through computer vision in healthcare. These computer vision systems enable enhanced treatment accuracy, streamlined hospital operations, and improved diagnostic efficiency. These systems also help analyze medical images, such as X-rays, CT scans, and MRIs, track and monitor patients remotely for safety, offer personalized treatments, and even predict health outcomes. The wide range of applications for these systems is anticipated to drive market growth. Emphasizing the wide array of applications motivates various key players to focus on strategic activities, such as collaboration and acquisitions, to enhance their product offerings.

- For instance, in August 2023, Google Health launched its AI-powered computer vision technologies in various hospitals across the U.K. The technology was specifically designed to analyze early detection for breast cancer based on the symptoms shown by female patients.

Furthermore, the market is dominated by several key players, with IBM, Siemens Healthineers AG, GE HealthCare, Koninklijke Philips N.V., and Stryker occupying the leading positions. Advanced technology integration and strengthening product offerings through collaborations further enhance the position of these companies in the global market by providing innovative services.

Download Free sample to learn more about this report.

Computer Vision in Healthcare Market KEY TAKEAWAYS

- 2025 Market Size: USD 5.57 billion

- 2026 Market Size: USD 7.01 billion

- 2034 Forecast Market Size: USD 54.28 billion

- CAGR: 29.17% from 2026–2034

- North America dominated the computer vision in healthcare market with a 40.03% share in 2025.

- The leading segment is anticipated to account for a 57.9% share in 2026.

- Another key segment is projected to dominate with a 65.9% share in 2026.

North America

North America maintained its leadership position in 2025, with the market valued at USD 2.23 billion.

Europe

Europe is projected to grow at a CAGR of 27.23% and reach USD 1.96 billion by 2026.

Asia Pacific

Asia Pacific is estimated to reach a market value of USD 1.66 billion in 2026, driven by expanding healthcare digitalization initiatives.

U.S.

U.S. The market is projected to reach USD 2.64 billion by 2026, supported by increasing adoption of AI-enabled healthcare technologies.

Japan

Japan Rising adoption of AI-powered diagnostic imaging solutions and growing demand for advanced disease detection technologies are driving market growth in the country.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Growth in Surgical Automation & Image-Guided Procedures to Drive Market Growth

The growing shift toward surgical automation and image-guided procedures is a prominent factor driving the global computer vision in healthcare market growth. The modern operating rooms demand higher precision. As surgical cases become more complex and minimally invasive procedures increase, the need for real-time visualization, guidance, and decision support also increases. Computer vision facilitates these workflows, enabling real-time anatomical mapping, 3D reconstruction, and informed visual judgment. These factors are facilitating image-guided and robotic procedures, which are expanding rapidly.

- For instance, in March 2025, Artisight collaborated with KARL STORZ, a leader in Operating Room (OR) integration, and NVIDIA, to bring solutions to smart operating rooms. The collaboration aimed to introduce KARL STORZ's AI computing platform for the OR, Pathway.AI, to bring real-time surgical insights to clinicians and hospital administrators. This platform utilizes computer vision and ambient listening to automate OR and perioperative tasks such developments are expected to augment market growth.

MARKET RESTRAINTS:

High Cost and Operational Complexity of Surgical Automation & Image-Guided Systems to Limit Adoption, Hampering Market Growth

One of the prominent factors hampering the adoption of these computer-vision-enabled surgical automation is the high upfront cost and complex system integration. These advanced robotic and image-guided platforms require expensive hardware, such as specialized cameras, sensors, and embedded vision processors, among others, which drive up the cost. Additionally, these systems require surgeon training, IT integration with OR equipment, and strict compliance with regulatory and safety standards, increasing deployment time and operational burden. Collectively, these factors increase the implementation cost and slow down adoption, hampering market growth.

- For instance, in May 2024, East Sussex Healthcare NHS Trust published an article reporting that a da Vinci XI robotic-assisted surgical system, which utilizes advanced vision and robotics technology, cost USD 2.16 million in the U.K.

MARKET OPPORTUNITIES:

Technological Advancement and AI Integration in Computer Vision Systems to Offer Growth Opportunities

Technological advancements and AI integration present lucrative opportunities for growth in the global computer vision healthcare market. Modern AI models can analyze complex medical images, detect subtle patterns, and support clinical decisions with greater confidence. The shift from basic image processing to deep-learning-powered insights is creating new applications in diagnostics, surgery, as well as patient monitoring. These innovations also attract strong funding and partnerships, encouraging more companies to launch advanced products. Furthermore, the rapid pace of AI-driven improvement is creating lucrative growth opportunities for companies operating in the market.

- For instance, in November 2024, Lumenalta formed a strategic partnership with Roboflow, a leading computer vision development platform, to revolutionize AI data management, model training, and application development. The collaboration aimed to integrate the company’s expertise in digital transformation and custom AI software with Roboflow’s advanced computer vision technology. Such strategic collaboration to boost market growth.

COMPUTER VISION IN HEALTHCARE MARKET TRENDS:

Integration with Clinician Workflows with Emphasis on AI is a Prominent Trend Observed

The integration of AI-enabled computer vision into clinician workflows, particularly for radiologists and pathologists, is a prominent trend observed. As imaging volumes rise, AI systems that can automatically prioritize urgent cases, quantify disease progression, and provide explainable outputs that are becoming essential workflow partners for radiologists. The global computer vision in healthcare market trend is also fueled by hospitals demanding solutions that integrate seamlessly with PACS, LIS, and reporting systems, as well as strategic collaborations among key operating players for innovation.

- For instance, in March 2025, GE HealthCare collaborated with NVIDIA to focus on innovation in autonomous imaging, beginning with autonomous X-ray technologies and autonomous applications within ultrasound. Such developments are expected to drive growth in the global healthcare market.

MARKET CHALLENGES:

Concerns in Regards with Data Security & Privacy Pose a Significant Challenge for Market Growth

Concerns around data security and privacy are a key restraint to computer vision in the healthcare market, as medical images often contain sensitive patient identifiers and protected health information. Hospitals remain cautious due to the increasing number of data breaches. The use of cloud platforms and AI tools also raises concerns about HIPAA/GDPR non-compliance, particularly when healthcare workers inadvertently upload PHI to generative AI or unsecured storage. These risks not only slow adoption but also increase the cost of compliance and liability management for vendors.

- For instance, in May 2025, The HIPAA Journal reported that research conducted by the cybersecurity company Netskope indicated healthcare workers routinely expose sensitive data, such as protected health information (PHI), by using generative AI tools such as ChatGPT and Google Gemini and by uploading data to personal cloud storage services such as Google Drive and OneDrive. Such incidences hamper consumer trust and restrain market growth.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Scalability of Cloud and SaaS Models Led to Segment’s Dominance

Based on product type, the global computer vision in healthcare market is segmented into hardware, software, and services.

To know how our report can help streamline your business, Speak to Analyst

In 2025, the software segment dominated the global computer vision in healthcare market due to a wide array of applications in image analysis, diagnostic precision, and workflow automation across various specialties. The dominance of the segment is reinforced by the scalability of cloud and SaaS models, which allow for rapid deployment across hospitals.

Additionally, major operating players in the market are streamlining their resources toward new product launches, FDA clearances, upgrades, and strategic mergers and acquisitions, positioning software as a leading segment.

- For instance, in October 2025, EssilorLuxottica acquired Ikerian AG, a health technology company specializing in AI and data management in the eye care sector. This development reinforced the company’s ambition to develop advanced software powered by machine learning and computer vision, streamlining clinical, research, and pharmaceutical workflows to facilitate healthcare professionals and enhance patient care.

On the other hand, the hardware segment is expected to grow at a CAGR of 25.72% during the forecast period.

By Application

Large Volume Data Generation by Medical Imaging Segment to Drive Segmental Growth

In terms of application, the market is categorized into medical imaging, patient monitoring, surgical assistance, diagnostic assistance, and others.

The medical imaging segment accounted for the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 57.9% share. The segment's dominance is attributed to the large volume of data generated by patients and intensive adoption of AI in various applications. Such factors, along with the expanding applications of the segment, are attracting significant investment opportunities that will further strengthen the segment's market dominance.

- For instance, in October 2025, MediView XR, Inc. received USD 24.0 million in funding from the Cleveland Clinic, Emplify Health, and other investors to develop surgical navigation and medical imaging solutions utilizing Augmented Reality (AR). Such developments are necessary to ensure the segment's growth.

The patient monitoring segment is expected to grow at a CAGR of 33.82% over the forecast period.

By End User

Increasing Bioprocessing Activities to Drive the Pharmaceutical & Biotechnology Companies Segmental Growth

In terms of end users, the market is categorized into hospitals & specialty clinics, diagnostic centers, and others.

The hospitals & specialty clinics segment accounted for the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 65.9% share. These settings are anticipated to high segmental share due to their vital role in handling large patient volumes and complex imaging workloads, creating strong demand for AI-driven efficiency and accuracy. They are the primary adopters of these CV solutions, integrating them into healthcare systems for various applications, including radiology, cardiology, ophthalmology, oncology, and others.

Additionally, hospitals have better access to infrastructure, reimbursement pathways, and multi-specialty expertise, making them the central hubs for deploying and scaling CV technologies compared to diagnostic centers or primary care facilities.

- For instance, in August 2025, Artisight launched its Smart Hospital platform, which is capable of autonomously documenting operating room activity into a patient's electronic health record (EHR). The platform uses voice-activated sensors and computer vision technology, enabling real-time observation, virtual nursing, and automated EHR documentation. Such industry-specific product launches are designed to boost the adoption of these technologies and support market growth.

The diagnostic centers segment is expected to grow at a CAGR of 29.46% over the forecast period.

Computer Vision in Healthcare Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

NORTH AMERICA

North America Computer Vision in Healthcare Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant computer vision in healthcare market share in 2024, valuing at USD 1.80 billion, and also maintained the leading share in 2025, with USD 2.23 billion. The region is anticipated to dominate and growth with a significant CAGR due to regulatory approvals, high imaging volumes, and strong venture investment into AI MedTech companies. In 2026, the U.S. market is estimated to reach USD 2.64 billion. Underscoring these advantages, key companies are focusing on strategic activities, such as mergers and collaborations, as well as new product launches, to expand and enhance their product offerings, thereby driving growth.

- For instance, in September 2024, Advanced Micro Devices, Inc. launched the AMD Versal Premium Series Gen 2, an adaptive SoC platform designed to deliver system acceleration for a wide range of workloads. Such developments ensure that data is moved rapidly and efficiently between processors and accelerators.

EUROPE and ASIA PACIFIC

Other regions, such as Europe and the Asia Pacific, are expected to experience notable growth in the coming years. During the forecast period, the European region is projected to record a growth rate of 27.23%, the second-highest among all regions, and reach a valuation of USD 1.96 billion by 2026. This growth is primarily driven by a mature regulatory environment that places an increasing emphasis on clinical validation and data protection. Backed by these factors, countries including the U.K. anticipates to record the valuation of USD 0.44 billion, Germany to record USD 0.40 billion, and France to record USD 0.32 billion in 2026. After Europe, the market in Asia Pacific is estimated to reach USD 1.66 billion in 2026 and secure the position of the third-largest region in the market. In the region, India and China are both estimated to reach USD 0.39 billion and USD 0.40 billion each in 2026.

LATIN AMERICA and MIDDLE EAST & AFRICA

During the forecast period, the Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space. The Latin America market in 2026 is set to reach a valuation of USD 0.35 billion. Rising adoption of diagnostic screening programs in the region is expected to drive growth. In the Middle East & Africa, the GCC is set to reach a value of USD 0.12 billion by 2026.

COMPETITIVE LANDSCAPE

Key Industry Players:

Strategic Collaborations Supported their Leading Position

The global computer vision in healthcare market exhibits a concentrated structure, with a few companies actively operating worldwide. These players are actively involved in product innovation, strategic partnerships, and geographic expansion. They actively invest in technology advancement and offer a wide array of product offerings for innovative computer vision systems.

Siemens Healthineers AG, IBM, GE Healthcare, and Koninklijke Philips N.V. are some of the significant players in the market. A comprehensive range of various computer vision products and services to improve patient care outcomes and assist in various applications.

- For instance, in March 2025, NVIDIA collaborated with GE HealthCare to advance innovation in autonomous imaging, focusing on the development of autonomous X-ray technologies and ultrasound applications.

Apart from this, other prominent players in the market include Tempus AI, Inc., NVIDIA Corporation, Fujitsu, and others. These companies are undertaking various strategic initiatives, such as investments in R&D to enhance their market presence.

LIST OF KEY COMPUTER VISION IN HEALTHCARE COMPANIES PROFILED:

- IBM (Germany)

- Siemens Healthineers AG (U.S.)

- GE HealthCare (U.S.)

- Koninklijke Philips N.V.,(The Netherlands)

- Stryker (U.S.)

- Fujitsu (Japan)

- Google LLC (U.S.)

- Tempus AI, Inc. (U.S.)

- NVIDIA Corporation (U.S.)

- Microsoft (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- October 2025: Arteris, Inc. collaborated with Axelera AI and licensed the company’s FlexNoC 5 interconnect IP for use in developing the Europa platform, expanding their product line from edge to the data center. The platform is designed to enable high performance in a power-efficient platform supporting everything from computer vision to complex generative AI

- January 2025: Blaize Holdings, Inc. partnered with alwaysAI, a leader in computer vision solutions. This collaboration integrated alwaysAI's advanced computer vision technology and remote deployment capabilities with Blaize's cutting-edge chipsets and edge devices to make edge deployments more accessible globally.

- August 2024: Caregility Corporation launched a new fall risk detection capability in its iObserver solution. The AI-powered solution offers continuous observation of patients at risk of self-harm or falls. The solution uses computer vision to analyze visual information, detect fall risks, and alert caregivers accordingly.

- May 2024: CareView Communications launched ‘Software Version 5.12’, marking a significant advancement in its virtual care technology and patient safety. The software update included Virtual Room Rails, an advanced feature designed to monitor patients at risk of elopement by using computer vision to alert staff when such patients approach an exit.

- May 2023: LandingAI launched a validation-ready version of its LandingLens platform. The platform comprises computer vision software for the U.S. FDA-regulated manufacturers. This new platform version targets regulated industries, such as life sciences, drug, and medical device

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 29.17% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Application, Technique, Scale of Operation, End User, and Region |

|

By Product Type |

· Hardware o Smart Cameras o Sensors o Memory Devices o Others · Software · Services |

|

By Application |

· Medical Imaging · Patient Monitoring · Surgical Assistance · Diagnostic Assistance · Others |

|

By End User |

· Hospitals & Specialty Clinics · Diagnostic Centers · Others |

|

By Region |

· North America (By Product Type, Application, End User, and Country) o U.S. o Canada · Europe (By Product Type, Application, End User, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Product Type, Application, End User, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Product Type, Application, End User, and Country/Sub-region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Product Type, Application, End User, and Country/Sub-region) o GCC o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.57 billion in 2025 and is projected to reach USD 54.28 billion by 2034.

In 2025, the market value stood at USD 2.23 billion.

The market is expected to exhibit a CAGR of 29.17%during the forecast period of 2026-2034.

The software segment is expected to lead the market in terms of type.

The demand for precise imaging for diagnostic and surgical purposes, as well as patient monitoring, is expected to drive market growth, meeting the increasing demand.

Google LLC., Basler AG, NVIDIA Corporation, and AiCure are some of the prominent players in the market.

North America dominated the market in 2024.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us