Connected Ships Market Size, Share, Industry Analysis, and Russia-Ukraine War Impact Analysis, By Application (Fleet Operations, Vessel Traffic Management, and Fleet Health Monitoring), By Installation Type (On-board and Onshore), By Fit (Line Fit and Retrofit), By Ship Type (Commercial and Defense), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

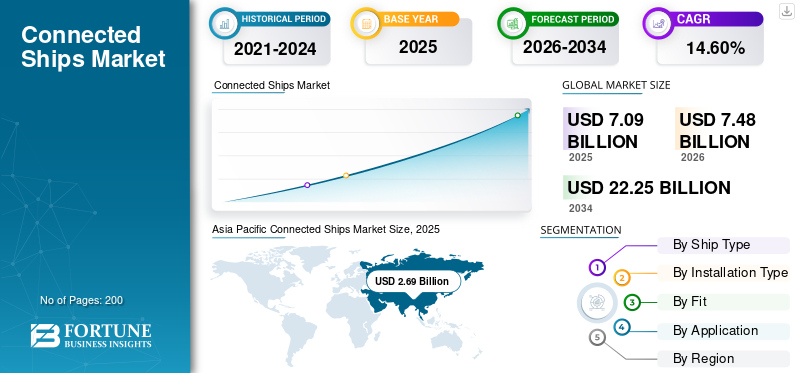

The global connected ships market size was valued at USD 7.09 billion in 2025 and is projected to grow from USD 7.48 billion in 2026 to USD 22.25 billion by 2034, exhibiting a CAGR of 14.60% during the forecast period. Asia Pacific dominated the connected ships market with a market share of 37.90% in 2025.

Connected ships are used in the marine and maritime industries to increase safety and navigation by combining connected technology. The application of connected technology on ships or vessels includes the improved management of critical ship operations, ship condition monitoring for preventive maintenance, and ship traffic management, among others. With the rise of industrial internet, the integration of automation and Big Data has touched every aspect of shipping.

Connected ship is a model where ships are tracked and managed with the help of satellites. This provides more streamlined reporting and helps improve the efficiency of ship operations, including fuel management. Sensor technologies and monitoring tools would alert both offshore and onshore management teams of potential problems and use predictive energy models to enable data-driven decision-making.

The shutdown caused by the COVID-19 pandemic in the first two quarters of 2020 resulted in lower revenues in the shipping sector. Shipyards, shipbuilding companies, and other vendors had to adjust their operations to the restrictions set by the government, which caused the suspension of shipbuilding activities.

- For instance, Italy's Fincantieri shipyard completely halted its production from 12th March to mid-April in 2020.

Download Free sample to learn more about this report.

Connected Ships Market Key Takeaways

- 2025 Market Size: USD 7.09 billion

- 2026 Market Size: USD 7.48 billion

- 2034 Forecast Market Size: USD 22.25 billion

- CAGR: 14.60% from 2026–2034

- Asia Pacific dominated the connected ships market with a 37.90% share in 2025.

- The Commercial segment is projected to account for 70.87% of the market in 2026.

- The On-board segment is expected to lead with a 63.79% market share in 2026.

Asia Pacific

Asia Pacific generated USD 2.69 billion in 2025 and is projected to reach USD 2.84 billion in 2026.

North America

North America accounted for USD 1.80 billion in 2025 and is expected to grow to USD 1.93 billion in 2026.

Europe

Europe reached USD 1.65 billion in 2025 and is projected to attain USD 1.72 billion in 2026.

U.S.

U.S. remains a key contributor to North America's growth through rising investments in ship digitization.

Japan

Japan is expected to benefit from Asia Pacific's expanding maritime trade and connected shipping ecosystem.

Read More

RUSSIA-UKRAINE WAR IMPACT

Russia and Ukraine War Disrupted the Shipping Industry's Supply Chain Leading to Higher Freight Rates and Container Shortages

The conflict between Russia and Ukraine is affecting the global logistics market at every level. The impact of the pandemic on storage capacity and container availability was only beginning to fade when the war between Russia and Ukraine began to affect the industry. The war disrupted the flow of goods, increasing costs and product shortages, resulting in devastating food shortages across the globe.

Russia destroyed Ukraine's agricultural infrastructure and disrupted entire supply chains. The Black and Azov Seas were blocked by Russia, and Ukrainian grain shipments were hijacked in the first months of the offensive. However, in July 2023, Russia and Ukraine signed a UN agreement to unblock Ukrainian grain exports from three Black Sea ports and ease the shortage. Despite the agreement, hours after signing the agreement, Russia attacked the port of Odessa with cruise missiles. This created high uncertainty in supply chains across the globe.

The war closed several ports and raised sea freight costs. Ships had to be diverted, causing congestion and delays in cargo flows, exacerbating conditions in the global supply chains. In addition, sanctions and restrictions encouraged a shift from rail to sea shipments, increasing pressure and exacerbating container shortages.

Connected Ships Market Overview & Key Metrics

Market Size & Forecast:

- 2025 Market Size: USD 7.09 billion

- 2026 Market Size: USD 7.48 billion

- 2034 Forecast Market Size: USD 22.25 billion

- CAGR: 1460% from 2026–2034

Market Share:

- Asia Pacific dominated the connected ships market with a 37.90% share in 2025, driven by increasing maritime traffic, rapid port infrastructure expansion, and growing adoption of digital technologies in China, South Korea, and Southeast Asia.

- By application, vessel traffic management is projected to hold the largest market share by 2025 due to rising demand for safety, efficient navigation, and real-time traffic monitoring in congested sea lanes.

Key Country Highlights:

- China: Growth fueled by Belt and Road Initiative, major port development projects, and high demand for digitalized fleet monitoring systems.

- United States: Digitalization initiatives and naval modernization programs are accelerating adoption of connected ship technologies, supported by defense contracts and maritime trade expansion.

- Japan: Increasing need for advanced vessel monitoring in earthquake-prone regions and government focus on reducing maritime accidents with AI and IoT solutions.

- Europe (France, Germany): Presence of leading shipbuilders and demand for autonomous vessels under EU’s sustainability and digital transformation goals.

Connected Ships Market Trends

Increasing Technological Developments in Vessel Monitoring Systems is a Leading Industry Trend

The ship building sector is undergoing a rapid transition to digitalization. The development of networking solutions in the field of shipping, such as cargo tracking systems and ship monitoring systems to ensure safety and business efficiency, has been driven by the growing maritime traffic. Cargo monitoring systems allow data reading and alarm monitoring of cargo tank pressure, temperature, and other parameters. A number of companies are investing in the development of satellite surveillance systems.

- For instance, in May 2021, Iridium Communications Inc. developed a product called Iridium Certus, which is a reliable satellite link that facilitates the uninterrupted transmission of cargo or ship tracking information.

- Asia Pacific witnessed connected ships market growth from USD 2.18 Billion in 2022 to USD 2.35 Billion in 2023.

Depending on the functionality needs of the system to be installed, the VMS component cost will vary. Generally speaking, the higher the functionality, the higher the cost of the equipment and the higher the cost of the data link, the higher the airtime costs. The cost of the VMS system will, therefore, differ according to individual Member States' needs as well as the level of government aid.

For instance, in the EU and the U.S., VMS systems will require expensive on-board equipment and a large amount of data over satellite link, which will lead to higher airtime charges. However, they will also provide very high functionality. In other regions, where per vessel costs are high and large fleet sizes are a problem, communication technologies such as AIS are deployed which significantly reduced the equipment and airtime costs while providing acceptable basic functionality of the VMS system.

Download Free sample to learn more about this report.

Connected Ships Market Growth Factors

Market Growth is Being Driven by Increasing Demand for Smooth Traffic in the Congested Sea Lanes

An important growth driver for the intermodal transport market is expected to be increasing international trade. Traffic congestion in the sea lanes is projected to increase as a result of increased marine transport. Up to 80% of global trade occurs by sea at various ports, as stated by the UN Conference on Trade and Development.

- For instance, in December 2022, the National Marine Dredging Company (NMDC) won a USD 272 million contract for the dredging of Egypt's Suez Canal.

Effective management of port traffic and congestion at major ports is thus becoming increasingly necessary. The demand for ship traffic management and Realtime Navigation Systems, which are expected to fuel the growth of the interconnected ships market, is increasing as marine trade and transport grow.

- For instance, in June 2021, CNES (Competitors of the European Union for the Shipbuilding Industry) entered a strategic partnership agreement with the world’s largest global maritime freight forwarding company (CMA CGM) for introducing innovative solutions for the shipping industry. In the framework of this partnership, CNES’ experts would focus on smart ship routing to improve safety at sea, support crews, and closely manage the environmental impact of shipping.

Increasing Investment in Digitalization by Shipping Companies to Fuel Market Growth

With increased situational awareness of fleet owners, carriers are heavily investing in ship digitization. The combined ship is in charge of shipping. In order to reduce damage claims for charterers, connected vessels provide remote access to container and cargo surveillance systems. The cost of insurance for the ship will, therefore, be reduced. Furthermore, substantial cost improvement of operational capacity and maintenance can be achieved through the combination of ship technologies. As a result, the benefits of this are precisely what makes shipping companies invest in digitization.

- For instance, in April 2023, Seaspan Shipyards awarded USD 2.6 million to a Canadian company to develop cutting-edge digital technologies that will energize the shipbuilding industry. The deal includes partnerships with companies that will use Seaspan's revolutionary Digital Holoship program as the basis for their own new marine technology developments.

Digitalization should be seen as a transformation in the delivery of business through the introduction of Industry 4.0 technologies such as Artificial Intelligence (AI), Business Domain Awareness (BDA), Consumer Condition Control (CC), the Internet of Things (IoT), Digital Security, Augmented Reality/Virtual Reality (AR/VR), Advanced Robotics, Augmented Managed (AM) and Advanced Simulation. In order to improve their competitive position and cut costs, large players have been adopting digitization through asset optimization and the realization of customer needs, an instance of the same being container monitoring.

- For instance, in October 2022, Kongsberg Digital and Alpha Ori Technologies entered a new partnership agreement. The partnership would enable Alpha Ori Technologies to integrate with Vessel Insight, which is a secure vessel to cloud data infrastructure of Kongsberg Digital. Vessel Insight would deliver real-time visibility into fleet and vessel-specific dashboards as well as ad hoc reporting and analysis tools.

RESTRAINING FACTORS

Vulnerability to Cyberattacks and High Cost of Digitalization to Hamper Market Growth

The large initial investment required to digitize ships is expected to dampen the growth of this market. In addition, the incorporation of telecommunications technology into maritime systems leads to a number of cyber-attacks. Ships can be vulnerable to cyber-attacks and cause severe losses that will hinder market growth.

Navigation is one of the key components that can be accessed. The hacker can send false navigational information to the ship’s crew, see the vessel sailing off course, or send false information regarding the position of the ship to shore-side teams. Monitoring and control systems can also be accessed. Today’s interconnected systems can be accessed from systems such as the water treatment system or the engine management system.

- For instance, in January 2023, DNV, one of the world’s largest shipping classification societies, confirmed that its systems have been affected by a ransomware attack on 7th January, affecting about 1,000 vessels that use its technology. The Norwegian company, based in Oslo, stated in a statement that the ShipManager software was infected with file-encoding malware, causing the company to shut down its servers.

Connected Ships Market Segmentation Analysis

By Ship Type Analysis

Commercial Segment to Witness the Highest CAGR over the Forecast Period Owing to Rising Demand for Commercial Fleet

Based on ship type, the market is segmented into commercial and defense.

The commercial segment is expected lead the market share with share of 70.87% in 2026, and witness the fastest CAGR during the forecast period. The increasing demand for commercial fleet for transport or import-export of goods, including electronic devices, FMCG products, automobiles, and others is expected to boost the segment growth over the forecast period. In addition, the demand for connected ships in the business sector is expected to increase further owing to the reduction of transportation times by determining which route would be the quickest on an interconnected transport network.

- For instance, in February 2023, Grimaldi Group re-committed Kongsberg Maritime to provide engineering and technology to build two new LR 7800 roll-on-roll-off (RO-Ro) roll-off vessels at China merchant Jinling shipyard. The order was signed in the fourth quarter of 2022 and ships are due to be put into service by 2025.

Over the forecast period, the defense segment is anticipate to witness significant growth. To strengthen the navy, governments are investing more and more in ships with maritime links.

- For instance, in May 2023, the U.S. Navy awarded a contract for the detailed design and construction of a new class of ocean surveillance vessels to Astraal USA, located in Mobile, Alabama. A new class of ships, known as auxiliary general ocean surveillance vessels AGOS 25, is under contract. It is estimated that the value of the contract will be up to USD 3.19 billion.

By Installation Type Analysis

On-board Segment to Dominate the Market Owing to Increase in Monitoring & Controlling of On-board Operations

Based on installation type, the market is classified into on-board and onshore.

The on-board segment will dominate the market share with share of 63.79% in 2026 and is expected to continue leading the market during the forecast period. Ships are mainly utilized to carry out onboard operations, which involve monitoring and controlling the function of an ongoing ship.

- For instance, in July 2021, Sperry Marine won a fleet-wide order for the new SperrySphere Connected ECDIS to be installed on 36 vessels operated by China Navigation Company (CNCo), part of the Swire Group. Connected ECDIS was the newest addition to Sperry Marine's portfolio of intelligent bridging solutions, connected via its own SperrySphere platform.

The onshore segment is expected to grow at a substantial rate over the study period. This is owing to the rising use of connected ships data to track traffic status and the management of port activities. Fleets benefit from connected ships as they allow for better communication with onshore and reliable information on safe and cost-effective sea routes, resulting in efficient fleet health monitoring.

- For instance, in June 2023, the U.K.’s two leading ports and the U.K.’s Peel Ports Group (Peel Ports Group) signed MoUs with UKHO to enhance the provision, management, and exchange of hydrographic and marine data.

By Fit Analysis

Line Fit Segment to Hold the Highest Market Share due to Increasing New Ship Orders

Based on fit, the market is classified into line fit and retrofit.

The line fit segment will hold the highest market share of 72.08% in 2026 and is predicted to continue its dominance throughout the projection period. This is owing to the growing investment in naval defense and surge in seaborne trade activities across the globe. In addition, an increase in new ship orders is predicted to propel the growth of the segment.

For instance, in June 2023, a shipbuilding contract en bloc for five 15,500 TEU Dual Fuel Container Vessels (LNG) was signed between the Korean shipbuilding company, Yang Ming Marine Transport Corporation (Yang Ming), and Hong Kong-based heavy equipment manufacturer, Hyundai Heavy Industries CO., Ltd.

The retrofit segment is expected to showcase significant growth over the study period. This is owing to the ship modernization programs by naval forces and by the commercial fleet operators of various countries.

- For instance, in July 2023, MAN SOLUTIONS entered a Conversion Commitment Agreement (CCA) with the world’s leading containership owner and manager, Seaspan, in partnership with liner shipping’s largest shipping company, Hapag Lloyd. Man PrimeServ, the after-sale division of MAN SOLUTIONS, would provide 15 solutions for engine retrofit for the conversion of Seaspan’s fleet of single-fuel diesel-powered vessels (“S90” vessels) powered by individual S90s (“B&W”) fuel-oil powered engines from Seaspan (“The Seaspan” or “The Seabird” vessels) to double-fuel diesel engines (“ME-LGIM”, “green methanol” vessels).

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Vessel Traffic Management to Hold the Largest Revenue Due to Increasing Demand for Safety and Efficient Navigation

Based on application, the market is classified into fleet operations, vessel traffic management, and fleet health monitoring.

The vessel traffic management segment will hold the largest market share of 56.94% in 2026. Growing demand for maritime safety, efficient navigation, and other life safety features at sea is driving the segment growth. Moreover, the use of vessel traffic management systems in seaports for efficiently handling large volumes of containers is expected to fuel segment growth.

- For instance, in July 2023, Marubeni Corp. announced the conclusion of a strategic partnership for the sale of the world’s most advanced Vessels Situational Awareness Platform (SAT Platform) with the company that developed the Platform. The SAT Platform functions as a fully-automated watch-keeper. It uses Computer Vision (CV) and Deep Learning (DL) algorithms to identify, locate, and monitor other vessels and other targets that could pose a threat to a vessel and measure the distance between those risks and the vessel.

The fleet health monitoring segment is anticipated to grow at the highest CAGR during the forecast period. This is due to the growing demand for preventive maintenance and predictive diagnostics of vessels across the globe.

- For instance, in June 2022, to improve the uptime of the LNG carrier, the Finnish technology company Wärsilä concluded a 15-year Guaranteed Asset Performance (GAP) agreement with the Japanese LNG ship management company NYK. Wärsilä would be responsible for the management of the vessel’s engines and associated equipment. The agreement covers the following: 3 WärTSILA 50DF dual fuel engines for the carrier, together with Gas Valve Units (GVUs) and turbochargers.

REGIONAL INSIGHTS

By region, the global market is segmented into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific Connected Ships Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 2.69 Billion in 2025, accounting for 37.90% share, and is expected to reach USD 2.84 Billion in 2026. Growing traffic between developing Asia Pacific countries such as China, South Korea, and other ports is driving the growth of the market. The development of new ports in Indonesia, Hong Kong, and the rest of Asia Pacific is expected to create new opportunities for market expansion in the region. In addition, improving trade relations and increasing imports and exports are expected to increase the demand for ships in the region.

Europe

The Europe region captured 23.20% of the global market in 2025, generating USD 1.65 Billion in revenue, and is projected to reach USD 1.72 Billion in 2026. Europe will witness significant growth during the forecast period due to increasing demand for autonomous and connected ships and cruises in France, the U.K., and others. Additionally, the presence of major shipbuilding companies in France, Italy, Germany, and others is expected to contribute to the market growth in the region.

North America

In 2025, the North America market stood at USD 1.8 Billion, representing 25.40% of global demand, and is projected to grow to USD 1.93 Billion in 2026. The growth of the North America market is accelerated by rising ICT developments in the North American maritime sector and the presence of major players in the region. In addition, the market is further influenced by the increasing budgets of shipping companies for digitization of ships. Additionally, increasing maritime tourism and maritime traffic in the region is expected to drive the market growth in the coming years.

Rest of the World

The Rest of the World market generated USD 0.95 Billion in 2025, representing 13.40% of the global market landscape, and is expected to reach USD 0.99 Billion in 2026.

Key Industry Players

Wartsila Focuses on Developing Innovative Technology to Maintain its Leading Position

Wartsila is a major player in the connected shipping market. The company offers a propulsion control system designed for technologically advanced naval and military vessels. Other major players such as Northrop Grumman, General Electric, Kongsberg Gruppen, Marlink, and Schneider Electric are investing in the research and development of connected ships with the adoption of artificial intelligence, augmented reality, and the Internet of Things.

List of Top Connected Ships Companies:

- Northrop Grumman Corporation (U.S.)

- Wartsila Oyj (Finland)

- General Electric Company (U.S.)

- Kongsberg Gruppen (Norway)

- Marlink (U.S.)

- Schneider Electric SE (France)

- Emerson Electric Co. (U.S.)

- ABB Ltd. (Switzerland)

- Rockwell Automation Inc. (U.S.)

- Ulstein Group ASA (Norway)

- Valmet Oyj (Finland)

- Jason Inc (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- January 2023 – Marlink announced an agreement with Singapore-based ship manager Thome Group for the delivery of hybrid network connectivity services for at least 100 ships.

- November 2021 – French certification company Bureau Veritas granted Approval in Principle (AiP) to a Liquefied Natural Gas (LNG) carrier design from Samsung Heavy Industries (SHI). SHI secured the AiP for its VESSEL smart chip solution, making it the first shipbuilder to receive such approval.

- November 2021 – Wartsila successfully delivered its advanced integrated bridge and navigation solution for Lindblad Expedition’s polar expedition cruise vessel.

- July 2021 – ABB Ltd. launched a new online platform “ABB Ability Marine Fleet Intelligence-Advisory” which can collect data from a wide variety of vessel systems. ABB offered it as a Software as a Service (SaaS) solution.

- April 2021 – Inmarsat, a leading mobile satellite communications provider, announced a partnership with OneOcean, a leader in compliance and navigation services for the maritime industry, for the development of digitalization of navigation and compliance in the maritime industry.

REPORT COVERAGE

The connected ships market research report provides a detailed analysis of the industry and focuses on key aspects such as key players, vessel types, facility, connected vessel suitability, and applications. Furthermore, the report provides information on related shipping market industry trends, costs of marine broadband connectivity, drivers, restraints, competitive landscape, market competition, product pricing, fleet operators, market status, budgets of shipping companies for digitalization of vessels, and highlights key industry developments. Apart from the factors mentioned above, it includes several direct and indirect factors that have influenced the global market growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 14.60% (2026-2034) |

|

Unit |

Value (USD Billion) |

|

By Geography

|

By Ship Type

|

|

By Installation Type

|

|

|

By Fit

|

|

|

By Application

|

|

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 7.09 billion in 2025 and is projected to reach USD 22.25 billion by 2034.

Registering a CAGR of 14.60%, the market will exhibit steady growth over the forecast period (2026-2034).

Based on ship type, the commercial segment is expected to lead this market during the forecast period.

Wartsila Oyj is the leading player in the global market.

In terms of share, Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us