Autonomous Ships Market Size, Share, Industry Analysis & Russia-Ukraine War Analysis, By Autonomy (Partial Automation, Fully Autonomous and Remotely Operated), By Solution (Hardware and Software), By Ship Type (Commercial (Bulk Carriers, Tankers, Dry Cargo, Containers, and Others) and Defense), By End User (Line Fit and Retrofit), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

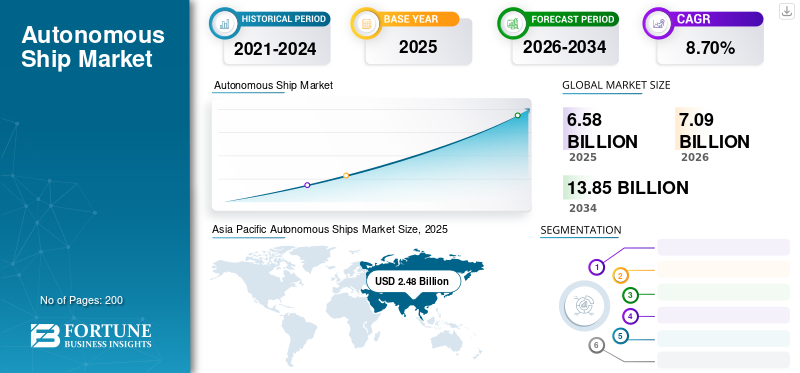

The global autonomous ships market size was valued at USD 6.58 billion in 2025 and is projected to grow from USD 7.09 billion in 2026 to USD 13.85 billion by 2034, exhibiting a CAGR of 8.70% during the forecast period. Asia Pacific dominated the autonomous ship market with a market share of 37.70% in 2025.

Autonomous ships are remotely piloted or highly automated ships. These vessels are equipped with the latest Internet of Things (IoT) technology, data analysis technology, and land-based monitoring centers connected to broadband networks. Advanced hardware and software automatically handle all tasks related to ship operations. Automated systems provide critical information such as equipment status monitoring, environmental monitoring, engine control, cargo control/loading, vessel control, docking, and undocking.

Technological advances in sensors, electromechanical drives, cameras, and satellite technology move automatic ships across oceans without human intervention. Committee Maritime International (CMI) and the International Maritime Organization (IMO) are investigating how autonomous ships would fit into the recent agenda of international maritime law.

Download Free sample to learn more about this report.

The maritime sector faced unprecedented challenges globally amid the COVID-19 pandemic. Production shutdowns, supply chain disruptions, and crew and staff quarantine periods hindered the growth of the market. Due to the novel coronavirus disease (COVID-19), local authorities banned several cargo and passenger ships from entering the port. As a result, some merchant seamen remained on board, while the ship owners incurred additional costs due to their extended stay in territorial waters.

Download Free sample to learn more about this report.

GLOBAL AUTONOMOUS SHIPS MARKET OVERVIEW

Market Size & Forecast

- 2025 Market Size: USD 6.58 billion

- 2026 Market Size: USD 7.09 billion

- 2034 Forecast Market Size: USD 13.85 billion

- CAGR: 8.70% from 2026–2034

Market Share

- Asia Pacific dominated the autonomous ships market in 2025 with a 37.70% share, valued at USD 2.48 billion. The region's leadership is driven by robust maritime trade, significant government investments in smart ship technology, and rapid adoption of AI and IoT-based vessel automation.

- By autonomy type, the fully autonomous segment is projected to exhibit the highest growth during the forecast period, supported by advancements in navigation software, reduced delivery times, and minimized human error.

Key Country Highlights

- United States: The U.S. autonomous ships market is accelerating due to the Department of Navy's large-scale investments in unmanned surface vessels and strategic defense contracts focused on AI-driven marine systems.

- South Korea: Backed by government funding, South Korea is leading in intelligent navigation systems and integrated ship platforms to enhance situational awareness and safety.

- United Kingdom: A hub for autonomous naval innovation, the U.K. is actively developing AI-powered patrol and surveillance vessels for maritime defense applications.

- Japan: Regulatory caution limits fully autonomous deployments; however, the country continues to invest in semi-autonomous systems for commercial shipping under strict cybersecurity guidelines.

- China: Extensive state-led investments and military interest in autonomous sea power have positioned China as a major contributor to regional and global market expansion.

- India: Naval modernization under the SPRINT initiative and collaborations with private defense startups are driving the integration of unmanned ship systems for national defense.

RUSSIA-UKRAINE WAR IMPACT

Russia-Ukraine War Positively Impacted the Market Growth due to the Rising Demand for the Product

Autonomous ships are appealing to naval forces as they offer several advantages over conventional manned vessels, and many countries have developed or experimented with autonomous ships in recent years. The U.S. has invested heavily and developed a strategic plan to acquire medium, large, and extra-large "unmanned vehicles" for surface and undersea operations. Other navies don't want to be left behind and are aggressively developing unmanned autonomy capabilities. These include China, the U.K., South Korea, Japan, Singapore, Australia, and others.

For Instance, in September 2022, Ukraine successfully used self-propelled "drone" boats in a full-scale attack on the Russian navy in Sevastopol, Crimea. It was a pivotal moment that changed the future of naval warfare. While autonomous ships have been deployed before, this is the first time multiple armed autonomous ships have been simultaneously deployed in combination with drones to conduct offensive naval operations against military targets successfully.

Several Russian ships were damaged in the attack, and the USV reportedly penetrated the harbor defenses and damaged vessels at protected anchorages. This development will lead to a rethinking of the role of unmanned ships in port defense to defend against aggressive naval operations and such attacks.

Autonomous Ships Market Trends

Technological Inventions in Maritime Navigation Software to Propel Market Growth

In recent years, a number of market players have come up with solutions for improving maritime security. The market growth is expected to be driven by the adoption of advanced technologies such as artificial intelligence, augmented reality, and navigational systems. For instance, in December 2023, Serco Inc., a provider of professional, technology, engineering, and management services, has been awarded the Autonomy and Vehicle Control Systems/ Testing and Evaluations contract to support the Naval Surface Warfare Center Carderock Division’s (NSWCCD) Naval Architecture and Engineering Department. Asia Pacific witnessed autonomous ships market growth from USD 1.96 Billion in 2022 to USD 2.12 Billion in 2023.

Autonomous Ships Market Growth Factors

Rising Investments in Advanced Ship Technology Developments to Boost Market Growth

Increasing investments in cutting-edge technology by various countries is accelerating market growth. Autonomy helps reduce collisions at sea, work long hours without distractions, increase fuel efficiency, and perform mission-critical tasks.

For instance, in October 2021, the autonomous ship project was financed by South Korea. A system capable of intelligent navigation, collision, and accident prevention, an integrated platform for system management, decision making, and situational awareness has been included in the project.

The global market growth will be driven by the deployment of technologies such as artificial intelligence, the Internet of Things (IoT), and Big Data analytics.

Development of Technologically Advanced Next-Generation Autonomous Ships Drives the Market Growth

Autonomous ships are revolutionizing the maritime industry by introducing new technologies, processes, and business models that have the potential to transform the way ships traditionally operate. Improved efficiency and security of the ship, data driven operations as well as enhanced capabilities are among the advantages of these ships. Therefore, the increasing development of next-generation ships will accelerate market growth. For instance, in November 2023, the U.S. Department of Navy, Naval Sea Systems Command, NAVSEA, launched a process to explore what can be done to develop a large autonomous surface vessel, LUSV, by inviting industry participants.

RESTRAINING FACTORS

Threats Connected with Cyber Security Hinders the Autonomous Ships Market Growth

The shipping industry has faced constant changes due to the digitization and automation of ships. Autonomous ship infrastructure includes a combination of electromechanical systems and highly integrated software and hardware that form computer networks. Censorship and networking between modern ships and computers in ports, terminals, shipping companies, and shipyards hinder information security, which is more vulnerable to cyberattacks and piracy. Increasing digitization and modernization lead to cyberattacks which affect overall market growth.

For instance, regulations in Japan do not allow fully autonomous vessels to operate without people on board. This regulation by the Government of Japan is an important decision as potential cyber threats, and attacks have not been thoroughly evaluated and addressed, as limited information is known about the overall architecture of autonomous type of ships.

Autonomous Ships Market Segmentation Analysis

By Autonomy Analysis

Fully Autonomous Ship Segment to Witness the Highest Growth from 2024 to 2032 Owing to Rising Demand

Based on autonomy, the market is classified into partial automation, remotely operated, and fully autonomous. In 2023, the remotely operated division held the largest share. A remotely-operated vessel is operated from a remote center, allowing the vessel to be steered from a vantage point or a safe location. The remotely operated segment is expected to hold a 51.40% share in 2026.

For instance, in September 2020, offshore service operator SeaOwl launched its new Remotely Powered Service at Sea (ROSS).

The highest growth is expected for the fully autonomous segment over the period under consideration. The benefits of reduced delivery times, shortened port calls, cheaper operating costs, no accidents caused by human error, and lesser freight rates are the factors driving this increase.

To know how our report can help streamline your business, Speak to Analyst

By Solution Analysis

Hardware Segment Holds Highest Share Owing to Growing Use of Automated Navigation Systems and Advanced Sensors

Based on the solution, the market is segmented into hardware and software. The hardware segment is set to account for a significant 57.96% share in 2026. The growth is attributed to the growing adoption of hardware components such as sensors, GPS trackers, automated navigation systems, propulsion & auxiliary systems, and others.

The software segment will exhibit the highest growth due to the demand for advanced software solutions for autonomous operations during the forecast period. In January 2020, Robosys Automation Limited launched the newest version of Voyager 100. It is an AI software that allows bridge watchkeepers to control ships and improve safety.

By Ship Type Analysis

Commercial Segment to Witness Highest Growth Due to Rising Demand for Next Generation Cargo Ships

By ship type, the market is classified into commercial and defense. The commercial segment is divided into bulk carriers, tankers, dry cargo, and containers.

The commercial segment is expected to hold a considerable share of 79.98% in 2026. The growth is attributed to increasing tourism and international seaborne trade. According to the International Chamber of Shipping, the total value of the annual global shipping industry trade stood at USD 14 trillion in 2019.

The defense segment is projected to show significant growth due to the rising demand from naval forces for border patrol, transportation of military forces, and others. For instance, in January 2023, Austal Limited presented a solid financial future with an early-stage contract that could exceed USD 108 million, including work on an autonomous patrol vessel for the Royal Australian Navy (RAN).

By End User Analysis

Line fit Segment Dominates the Market Owing to Increased Spending on Naval Defense

By end-user, the market is segmented into line fit and retrofit. Among these, the line fit segment hold the highest autonomous ships market share of 80.34% in 2026. The growth is due to increasing investments from naval defense forces and growing international maritime trade. The procurement of advanced ships due to growing tourism drives segmental growth.

For instance, in January 2023, The Indian Navy signed an agreement with Sagar Defense Engineering Pvt. to help acquire a fleet of armed autonomous boats under the "SPRINT" initiative, which aims to encourage the development and use of homegrown defense technology by domestic companies.

The retrofit segment will witness remarkable growth during the forecast period. Growing upgrades, modernization programs, and changing regulatory energy and emission standards drive market growth.

REGIONAL INSIGHTS

The market is studied across North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific Autonomous Ships Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

In 2025, the Asia Pacific market stood at USD 2.48 billion, representing 37.70% of global demand, and is projected to grow to USD 2.68 billion in 2026. The growth of the market is attributed to the rapid economic development of the region and growing maritime trade. According to UNCTAD's Maritime Transport Review 2022, the Asia-Pacific region remained the world's crucial maritime cargo handling center in 2021, accounting for 42% of exports and 64% of imports. The Japan market is projected to reach USD 0.574 billion by 2026, the China market is projected to reach USD 0.687 billion by 2026, and the India market is projected to reach USD 0.288 billion by 2026.

North America

The market in North America reached USD 1.54 billion in 2025, representing 23.30% of total market revenue, and is projected to reach USD 1.64 billion in 2026. North America is observing significant growth due to increasing investment in developing advanced commercial and defense vessels. Growing shipping in the U.S. and the presence of major companies such as IBM Corporation, GE, Northrop Grumman, Honeywell International Inc., and others drive market growth.

- The U.S. market is projected to reach USD 1.254 billion by 2026.

Europe

Europe contributed approximately USD 1.65 billion to the global market in 2025, accounting for 25.00% share, and is expected to reach USD 1.78 billion in 2026. Behind the growth are increased investments in developing advanced ship projects from various European countries, driving the market growth. In January 2020, the European research program Horizon 2020 awarded USD 22 million to the Autonomous Marines project developed by the Norwegian maritime cluster. Major players such as ABB, Fugro, Kongsberg Maritime, Rolls-Royce Plc, and others contribute to regional market growth. The UK market is projected to reach USD 0.525 billion by 2026, while the German market is projected to reach USD 0.378 billion by 2026.

Rest of the World

The rest of the World recorded a market size of USD 0.92 billion in 2025, capturing 13.90% of the global market share, and is projected to reach USD 0.99 billion in 2026. The rest of the world shows moderate growth between 2024 and 2032. The growth is due to the increase in spending by the navies of the Middle Eastern countries. In 2019, Unique Group developed the UnI-Cat vessel in the United Arab Emirates for unmanned exploration in shallow waters. The company designs and integrates the ship's autonomous sensor and communication technology.

KEY INDUSTRY PLAYERS

Key Players are Focusing on Developing Advanced Technologies for Next-Generation Autonomous Vessels

Players operating in this industry focus on business expansion by developing next-generation ships and systems. In October 2022, Kongsberg Maritime announced that a supply contract for the HUGIN Endurance Autonomous Underwater Vehicle (AUV) system had been awarded to an undisclosed partner. The HUGIN Endurance is a long-range AUV designed for land-to-shore operations. It is the major member of the HUGIN AUV family, with a diameter of 1.2 meters, a length of about 11 meters, and a weight of about 7,000 kilograms.

List of Top Autonomous Ship Companies:

- ABB (Switzerland)

- ASELSAN A.Ş. (Turkey)

- BAE Systems (U.K.)

- Fugro (Netherlands)

- GE (U.S.)

- Honeywell International Inc. (U.S.)

- Kongsberg Gruppen Maritime (Norway)

- L3 ASV (U.S.)

- Northrop Grumman (U.S.)

- Rolls Royce plc (U.K.)

- Siemens Energy (Germany)

- Wärtsilä (Finland)

- Marine Technologies LLC (U.S.)

- Ulstein Group ASA (Norway)

- Mitsui (Japan)

- Sea Machines Robotics Inc. (U.S.)

- Neptec Technologies Corp. (Canada)

KEY INDUSTRY DEVELOPMENTS:

- May 2023 – L3Harris Technologies partnered with BigBear.ai to provide advanced autonomous surface vessels (ASVs) and artificial intelligence (AI) to current and future maritime defense programs. Under the agreement, L3Harris' ASView system would be integrated with BigBear.ai's predictive computer vision technology to identify better and classify vessels, improve situational awareness, and support manned and unmanned group missions.

- March 2023 - Samsung Heavy Industries Co. (SHI) and Kongsberg Maritime (KM) signed a joint development project agreement (JDA) to design a next-generation autonomous 174K LNG carrier that uses autonomous remote control and low-emission technology.

- February 2023 – Lloyd's Register Unmanned Marine Systems certified the BAE Systems Autonomous Pacific 24 (AP24) rigid inflatable boat (RIB). The AP24 RIB was developed for the Royal Navy by BAE Systems with funding from the NavyX Autonomy and Lethal Accelerator programme, which aims to deliver new technology quickly.

- July 2022 - Fugro signed a contract with Kooiman Engineering and Van Oossanen Naval Architects to develop Blue Prism, its next-generation unmanned surface vessel (USV), designed specifically for coastal and offshore environments. Blue Prism design combines a very low carbon footprint with extensive data collection capabilities

- August 2022 - The U.S. Navy is testing its first full sized autonomous ship. The U.S. Navy added autonomous navigation capability to another vessel, the future Spearhead-class expeditionary fast transport USNS Apalachicola (EPF 13) for Military Sealift Command. The service tested autonomy retrofit systems and purpose built autonomous prototypes. However, this will be the first true numbered hull in the U.S. Navy with built onboard autonomy.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.70% over 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Autonomy

|

|

By Solution

|

|

|

By Ship Type

|

|

|

By End-User

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 6.58 billion in 2025 and is projected to reach USD 13.85 billion by 2034.

The market is projected to grow at a CAGR of 8.70% during the forecast period (2026-2034).

The hardware in the solutions segment is expected to be the leading segment in this market during the forecast period.

KONGSBERG is the leading player in the global market.

Asia Pacific held the highest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us