Consolidated Region 30MM Ammunition Market Size, Share & Industry Analysis, By Weapon Type (Autocannon, Rotary Cannon, Naval Gun, Anti-material Gun, Anti-aircraft Gun, and Others), By Ammunition Type (High Explosive Incendiary (HEI), High Explosive Incendiary - Tracer (HEI-T), High Explosive Incendiary/Tracer - Self Destruct (HEI/T - S.D.), Semi-armor Piercing High Explosive Incendiary - Tracer/Self Destruct, and Others), By Platform (Airborne, Naval, and Land), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

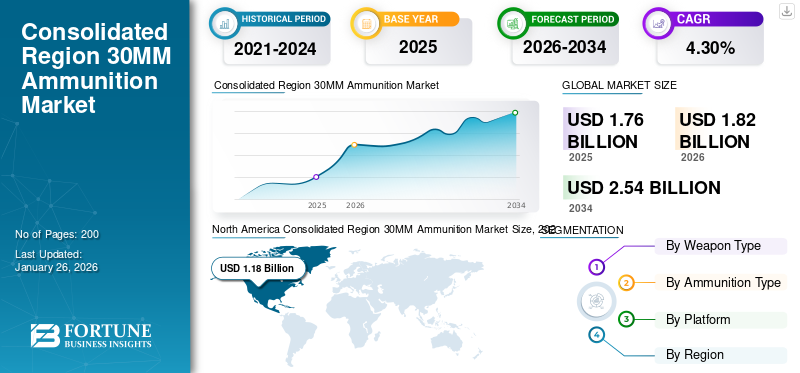

The consolidated region 30MM ammunition market size was valued at USD 1.76 billion in 2025. The market is projected to grow from USD 1.82 billion in 2026 to USD 2.54 billion by 2034, exhibiting a CAGR of 4.30% during the forecast period. North America dominated the consolidated region 30MM ammunition market with a market share of 66.92% in 2025.

Terrorist activities, geopolitical tensions, and hostilities across regions are likely to surge the procurement of defense equipment by prominent militaries and law enforcement agencies. This impact will hit the market expansion over the forecast period. Moreover, technological advancements have introduced next-generation munitions for all military platforms, such as land, naval, and air forces, to protect against all threats, propelling the market growth.

Technological innovations, particularly in Case-less Ammunition, Programmable Munitions, and Advanced Proximity Fuze, and strategic partnerships and mergers to improve product efficiency and quality, are also fueling market growth and making systems more efficient and reliable. However, the market faces some challenges, such as technologically advanced alternative systems. Key players, such as Elbit System Ltd., BAE System PLC., Northrop Grumman Corporation, and others, are focused on research and development to improve 30MM Ammunitions and actively innovating solutions to address these challenges, enhance system efficiency, and expand their global presence. These factors position the market for continued growth in the coming years.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Increasing Defense Budgets for Military Modernization and Upgrade of Ammunition to Foster Market Growth

The rising incidence of armed national and international conflicts has driven several countries to enhance their military strength by procuring advanced ammunition and equipment. Modernization is currently undertaken across most emerging countries, such as the U.S., the U.K., Germany, Russia, France, and others. The medium caliber segment includes high-performance 30MM cartridges for an extensive range of applications, including sea, land, and air, with the ability to penetrate light armor, material, and personnel objectives. The growing application of armaments by prominent militaries across the region is anticipated to boost the demand for medium-caliber ammunition.

This defense expenditure for ammunition procurement and Research, Development, and Testing (RDT) activities has increased significantly across regions over the past few years. For instance, in June 2022, American defense manufacturer Rheinmetall developed a new medium caliber 30MM x 173 MK 340 MOD 0 Kinetic Energy Electronically Timed (KEET) airburst munition for the U.S. Navy. The MK 340 KEET is derived from the NATO standards.

These countries are spending significantly on military modernization programs to enhance and upgrade their self-protection capabilities and firepower assets in lethality, range, and precision, driving the consolidated region 30MM ammunition market growth.

High Demand for Conventional Ammunition Amid the Advent of Contemporary Next-generation Weapon Systems to Bolster Market Growth

The 30mm ammunition market is experiencing robust growth, driven by sustained demand for conventional ammunition alongside advancements in next-generation weapon systems. This growth is attributed to military modernization efforts, geopolitical tensions, and increasing defense budgets worldwide. Countries are investing heavily in modernizing their armed forces, including upgrading ammunition for autocannons, rotary cannons, and naval guns.

According to the U.K. MOD's Defense Equipment Plan 2021-2031, in November 2020, the Ministry of Defense awarded a 15-year munitions contract worth USD 3.28 billion to BAE Systems Land U.K. for the continuous supply and support of 39 different munitions for the U.K. Armed Forces. The 39 munitions include large-caliber tanks and artillery shells, medium-caliber ammunition, small arms, and mortars.

According to the European Security & Defense Report, significant investments by market players have been made in developing 30MM air-bursting munitions (ABM), which are programmable for maximum effect. For instance, a dual-feed 30MM M.K. 30-2 ABM cannon with a remote-controlled turret is mounted on a PSM Puma IFV, which can fire ABM or APFSDS-T (Armor Piercing Fin Stabilized Discarding Sabot – Tracer).

The ESD Report also mentions that Russian counterparts utilize 30x280MM ammunition rather than their NATO counterparts, who use 30x173MM ammunition. For instance, in May 2019, MECAR developed and undertook the development of their new 30MM APFSDS-T shell for 2A42 and 2A72 cannons.

Market Restraints

Presence of Conventional Kinetic Ammunition-based Weapon System Substitutes to Hinder Market Growth

Armed forces globally are anticipated to reduce their dependence on conventional ammunition and relevant weapon systems in a phased manner during the forecast period. This development is impacted by the advent of technologically advanced modern weapon systems, such as directed energy weapons, which are in the development stage.

In September 2021, according to the Congressional Research Service (CRS) Report – Department of Defense (DOD) Directed Energy Weapons (DEW), directed energy weapons can destroy a vast array of electronic systems, which may include both commercial and military systems. They can disable, hinder, or destroy electronic systems under their electromagnetic cone. This factor is expected to drive market growth owing to the demand for weapon systems based on high-energy lasers and high-performing particle beams on naval, airborne, and land platforms.

The operation, support, and maintenance of conventional kinetic ammunition-based weapon systems are time-consuming and expensive compared to the next-generation weapon systems, which don't require periodic maintenance and procurement. The procurement and maintenance costs of conventional kinetic weapons cost the government significant budgetary allocations to maintain and support current ammunition stockpiles and future scheduled deliveries. All these factors are restricting market growth.

Market Opportunities

Rapid Technological Advancements in Caseless Ammunition and Advanced Proximity Fuze Technology in 30MM Munitions Fuel Market Growth

Technological advancements in the consolidated region of 30mm munitions, aimed at improving effectiveness on the battlefield and countering terrorism activity, are providing new opportunities in the market. Caseless ammunition, which eliminates the need for traditional cartridge cases, offers improved efficiency and reduced weight, making it ideal for modern weaponry.

Programmable munitions allow for precise control over detonation timing and explosive effects, enabling military forces to adapt to varying combat scenarios and engage a diverse range of targets effectively. For instance, advancements, such as air-bursting munitions, enable projectiles to detonate in proximity to the target, maximizing damage and optimizing lethality while minimizing collateral damage. Coupled with advanced proximity fuzes that enable munitions to detonate at certain distances from targets, these advancements are reshaping the capabilities of defense systems.

As defense forces across the globe are focusing on modernizing their munitions with more efficient and reliable munitions, the demand for these high-tech solutions continues to surge, propelling market growth in the defense sector. For instance, in November 2024, the U.S. Army will develop 30mm programmable proximity airburst munitions that can counter Unmanned Aircraft Systems (UASs).

Global Consolidated Region 30MM Ammunition Market Overview

Market Size & Forecast

- 2025 Market Size: USD 1.76 billion

- 2026 Market Size: USD 1.82 billion

- 2034 Forecast Market Size: USD 2.54 billion

- CAGR: 4.30% from 2026–2034

Market Share

- North America dominated the consolidated region 30MM ammunition market with a 66.92% share in 2025, driven by the U.S. defense modernization programs, high defense budgets, and widespread use of 30MM ammunition in land, naval, and airborne platforms.

- By weapon type, autocannons held the largest market share in 2024 due to their increasing integration in armored vehicles and fighter aircraft. Meanwhile, high explosive incendiary (HEI) ammunition is projected to remain dominant due to its versatility and high effectiveness in modern combat operations.

Key Country Highlights

- United States: Largest consumer of 30MM ammunition, supported by extensive military modernization programs and development of advanced programmable munitions for unmanned systems and next-gen defense platforms.

- Germany: Rising adoption of 30MMx173 airburst munitions (ABM) across infantry fighting vehicles and participation in NATO programs boosting market demand.

- Russia: Focus on indigenous 30x280MM ammunition development for armored vehicles and heavy weapon platforms amid geopolitical tensions and heightened border security.

- United Kingdom: Long-term munitions contracts, such as the USD 3.28 billion agreement with BAE Systems Land U.K., ensuring continuous supply of medium-caliber ammunition to meet modernization objectives.

Consolidated Region 30MM Ammunition Market Trends

High Adoption Rates and Development of Air Bursting Munitions (ABM) to Drive Market Trends During the Forecast Period

According to NATO Medium Caliber Gun Ammunition Effectiveness Studies, medium caliber munitions are traditionally utilized across the land, airborne, or naval platforms. Conventionally, medium caliber munitions use single penetrator or fragmentation projectiles. In contrast, Air Bursting Munitions (ABM) facilitate a similar overall damage pattern with preset initiation compared to Penetrators with Enhanced Lateral Efficiency (PELE) or fragmentation munitions.

In June 2022, Rheinmetall AG announced that it is developing new medium caliber ammunition for the U.S. Navy, which will be supplied by American Rheinmetall Munitions Inc., which had been awarded a contract worth USD 14.3 million under the U.S. Navy Other Transactions Agreement (OTA). The contract is critical to the U.S. Navy, as it intends to enhance the cost-effective engagement capability of existing and future naval gun weapon systems in surface-to-air and surface-to-surface threats.

- North America witnessed consolidated region 30MM ammunition market growth from USD 1.09 Billion in 2023 to USD 1.14 Billion in 2024.

The Rheinmetall prototype will undergo an Initial Operational Clearance for 30MMx173 MK 340 MOD 0 KEET (Kinetic Energy Electronically Timed) airburst munitions, a derivative of NATO-qualified Rheinmetall 30MMx173 KETF (Kinetic Energy Timed Fuze) munition.

European NATO Armed Forces, such as the Australian, German, and Hungarian Armed Forces, utilize the 30MMx173 KETF. Owing to enhanced accuracy and increased first-ammunition hit probability, the munition will facilitate a significant increase in lethality and reduction in munitions utilized by the target.

Download Free sample to learn more about this report.

Impact of Russia-Ukraine War

Rising Border Security Issues in Russia and Ukraine Will Facilitate Product Demand

In the ongoing war between Ukraine and Russia, many countries dependent on Russia and Ukraine for defense supplies have started focusing on self-reliance in defense. As the Russian-Ukraine war changes, the world is under the influence of a new wave of accelerating defense spending. However, these conflicts can have a more significant impact than the military budget. It can also catalyze changes in procurement priorities.

The Russian-Ukraine war has also changed the balance of defense procurement, and the defense needs to prepare for that change. However, developed and developing countries such as the U.S., the U.K., Germany, and China witnessed increased military expenditure in 2021. For instance, according to an analysis by the Stockholm International Peace Research Institute (SIPRI), consolidated regional military spending increased by 2.6% and reached a value of USD 1981 million in 2021.

For instance, in May 2021, General Dynamics Corporation won the firm's fixed-price contract worth USD 6.1 million to deliver 30 MM ammunition. The buyer is undisclosed, and the total delivery will be completed in February 2023.

SEGMENTATION ANALYSIS

By Weapon Type

Autocannons are Set to Lead the Market Due to Their Rising Adoption in Armored Vehicles and Fighter Aircraft

The 30MM ammunition market is divided by weapon type into autocannon, rotary cannon, naval gun, anti-material gun, anti-aircraft gun, and others.

The Autocannon segment is projected to dominate the market with a share of 28.93% in 2026. The autocannon segment is expected to dominate the forecast period due to its rising adoption in armored vehicles and fighter aircraft. The autocannon segment will witness significant growth during the forecast period. In addition, Nations are increasingly modernizing their armed forces to enhance combat capabilities, leading to a rise in demand for effective weaponry, including autocannons that utilize 30mm ammunition. For instance, in August 2021, the Spanish MoD was awarded the contract to General Dynamics European Land Systems to provide 348 8×8 Dragon VCR infantry fighting vehicles. The contract's total value was USD 1.97 billion, and the delivery started in 2022 and will end in 2029. This vehicle has 30MM auto guns provided by the Spanish company Escribano.

The rotary cannon segment is anticipated to grow at the highest CAGR during the forecast periods. The growth is attributed to several factors, including the increasing demand for advanced weaponry in both military and defense applications. Additionally, technological improvements are leading to enhanced performance, reliability, and efficiency of rotary cannons, fueling the demand for modern warfare. Their ability to deliver sustained firepower makes them useful for a wide range of operations, which is contributing to their rising demand amid the armed forces.

By Ammunition Type

HEI Ammunition Is Anticipated to Remain Strong Due to Its Critical Role in Modern Military Operations

The High Explosive Incendiary (HEI) segment is expected to lead the market, contributing 36.78% globally in 2026. The market is classified by ammunition type into high explosive incendiary (HEI), high explosive incendiary - tracer (HEI-T), high explosive incendiary/tracer—self-destruct (HEI/T—S.D.), semi-armor piercing high explosive incendiary - tracer/self-destruct, and others.

High Explosive Incendiary (HEI) is the fastest-growing ammunition type segment. HEI ammunition has a significant adoption within the 30mm category due to its versatility and effectiveness in various military applications, making it a preferred choice for many armed forces. Ongoing conflicts and regional security concerns are driving increased defense spending globally, leading to higher demand for effective munitions such as HEI rounds.

For instance, in July 2022, the U.S. Navy awarded a contract to Rheinmetall AG to create a new high-performing medium caliber 30MM X 173 Airburst munition against naval threat protection.

The semi-armor-piercing high explosive incendiary-tracer/self-destruct segment is projected to show the fastest growth with the highest CAGR during 2025-2032. These munitions are designed to penetrate armor effectively and deliver explosive incendiary effects, making them highly demanded in modern military and defense applications.

By Platform

Rise in Cross Border Terrorism & Conflicts Boost Airborne Segment Growth

The Airborne segment will account for 41.97% market share in 2026. By platform, the 30MM ammunition market has been divided into airborne, naval, and land. Airborne is the leading segment among platforms. The airborne segment dominates the consolidated region 30MM ammunition market share, with an increased focus on improving airborne capabilities by nations and adopting UAVs in military forces. Moreover, increasing border conflicts and international terrorism threats have strengthened the armed forces on different platforms for multiple threat protections. Emerging economic countries have increased their government budgets to acquire a new and upgraded fleet of platforms such as armed land, air, and naval forces. For instance, in April 2022, Estonia's defense forces procured 220-wheeled armored vehicles worth around USD 197.44 million. No specific potential manufacturer has been named for the new procurement. The delivery of specified types of vehicles will be completed by the end of 2024.

- The airborne segment is expected to hold a 44.06% share in 2024.

The land platform has the second-largest share of the market. With increasing geopolitical tensions, the land-based platform is anticipated to grow further during the forecast period. A land-based platform plays a crucial role in monitoring the nation's territory in remote locations, fueling the demand for 30mm ammunition in land-based platforms.

To know how our report can help streamline your business, Speak to Analyst

Supply Chain Analysis

Raw Material Suppliers

- Components: The primary materials involved in the production of 30MM ammunition include metals (e.g., brass for casings, lead for projectiles), explosives (such as TNT or RDX), and specialized materials for enhanced performance (e.g., fragmentation or armor-piercing capabilities).

- Challenges: Fluctuations in commodity prices, supply disruptions due to geopolitical tensions, and stringent regulations concerning material sourcing and handling can impact raw material availability and cost.

Manufacturers

- Production Facilities: Various defense contractors and ammunition manufacturers produce 30MM ammunition using advanced manufacturing techniques and technologies to ensure quality and efficacy. Major manufacturers, such as Rheinmetall and BAE Systems, are involved in the design and production of these munitions.

- Technology Integration: The incorporation of new technologies, such as programmable airburst munitions and electronic timing mechanisms, plays a significant role in the manufacturing process. Continuous investment in R&D ensures that manufacturers stay competitive.

- Challenges: Manufacturers face critical challenges in maintaining production capacity, managing production costs, and complying with government regulations and quality standards.

Regulatory and Compliance Factors

- Government Policies: The ammunition supply chain is heavily regulated at local, national, and international levels. Compliance with arms control regulations, export controls, and hazardous materials handling is mandatory.

- Impact of Regulations: Changes in government policies can influence production schedules and procurement strategies by defense contractors and military organizations.

End Users

- Military Forces

- Law Enforcement Agencies

- Emerging Markets

Role of ITAR in Supply Chain

- The International Traffic in Arms Regulations (ITAR) significantly influences the supply chain for airborne countermeasures by regulating defense-related exports:

- Impacts:

- Compliance Necessity: Companies must comply with ITAR to prevent unauthorized access to sensitive technologies.

- Collaboration Complications: ITAR compliance complicates international partnerships due to export licensing requirements.

- Cost and Delay Increases: Adhering to ITAR can lead to higher administrative costs and potential delays in product delivery.

CONSOLIDATED REGION 30MM AMMUNITION MARKET REGIONAL OUTLOOK

The consolidated region 30MM ammunition market is studied across North America and Europe.

North America

North America Consolidated Region 30MM Ammunition Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market with a valuation of USD 1.18 billion in 2025 and is projected to reach USD 1.21 billion in 2026. North America dominated the market in 2025, with the U.S. having the highest defense budget. The rise in the adoption of next-generation weapon systems and R&D on advanced ammunition by key regional manufacturers, such as General Dynamics Corporation, Northrop Grumman Corporation, and others, are anticipated to fuel market growth in North America. Moreover, increasing the federal budget for military procurement plans for all military platforms, such as air, sea, and land, is leading to market growth. The United States market is projected to reach USD 1.01 billion by 2026.

Europe

In 2025, the Europe market stood at USD 0.58 billion, representing 33.08% of global demand, and is projected to grow to USD 0.61 billion in 2026. The European market is predicted to grow significantly during the estimated period. The increasing adoption of weapons systems in land-based platforms for various threat protection applications across several countries, such as Germany, France, Russia, Spain, and the U.K., is projected to support the market growth in Europe in the upcoming years. The United Kingdom market is projected to reach USD 0.14 billion by 2026, while the Germany market is projected to reach USD 0.08 billion by 2026.

Competitive Landscape

Key Industry Players

Diversified Product Portfolio Offered by Key Market Players to Offer Competitive Edge

The consolidated region 30MM ammunition market is characterized by a competitive landscape featuring key players, such as Elbit System Ltd., BAE System PLC., Northrop Grumman Corporation, Poongsan Corporation, Rheinmetall AG, and others. Key players focus on growing investment in research and development, a diversified product portfolio of 30MM ammunition, and strategic acquisitions. Key market players focus on business expansion strategies such as agreements, mergers and acquisitions, product portfolio expansion, and long-term contracts with multinational companies included in the market.

These companies are leveraging advanced technologies, including Case-less Ammunition, Programmable Munitions, and Advanced Proximity Fuze, to improve weapons efficiency and reliability. Overall, the focus on technological integration with different platforms, land, naval, and especially airborne and modernization in materials will drive significant growth in the consolidated region 30MM ammunition market in the coming years.

LIST OF KEY CONSOLIDATED REGION 30MM AMMUNITION COMPANIES PROFILED

- BAE Systems Plc (U.K.)

- CBC - COMPANHIA BRASILEIRA DE CARTUCHOS (Brazil)

- Denel SOC Ltd. (South Africa)

- Elbit Systems Ltd. (Israel)

- General Dynamics Corporation (U.S.)

- KNDS N.V. (Krauss-Maffei Wegmann + Nexter Defense Systems N.V.) (Netherlands)

- MSM Group s.r.o. (Slovak Republic)

- Nammo A.S. (Norway)

- Northrop Grumman Corporation (U.S.)

- Poongsan Corporation (Korea)

- Rheinmetall AG (Germany)

- Thales Group (France)

KEY INDUSTRY DEVELOPMENTS

- February 2025 – The EM&E Group, a Spanish defense systems firm, has obtained a contract to provide the Royal Thai Navy with two units of its Sentinel 30 naval remote-controlled weapon station (RCWS). Each station will come with two ammunition storage compartments, each having the capacity for 200 rounds, which will include both programmable airburst ammunition and standard 30 mm ordnance.

- October 2024 - The Project Manager for Maneuver Ammunition Systems (PM MAS) at the Joint Program Executive Office Armaments and Ammunition awarded a production contract worth USD 78.5 million on a firm fixed price basis to Northrop Grumman Defense Systems (NGDS) for the new 30x173mm XM1182 High Explosive Airburst with Tracer (HEAB-T) round.

- January 2024 – The German Bundeswehr has engaged Rheinmetall to manufacture and provide medium-caliber ammunition for the Puma infantry fighting vehicle. This order is a call-off from a prior framework agreement and includes several hundred thousand rounds of 30mm x 173 DM21 service ammunition. The total value of the order exceeds €350 million, which includes value-added tax. Following the verification of perfect functionality, deliveries are scheduled to start this year and will extend through 2027.

- March 2022 - French government-owned weapons manufacturer, Nexter Munitions and Indonesia's PT Pindad signed a Memorandum of Understanding (MOU) contract associated with Medium Caliber Munitions and Large Caliber Munitions. Under the MOU, Medium Caliber Munition and Large Caliber Munition products such as 120MM, 105MM, 20MM, and 30MM ammunition for the Rafale multirole combat aircraft.

- July 2020 - The U.S. Army awarded a contract to Northrop Grumman under the project called Project Manager for Maneuver Ammunition Systems (PM-MAS) to develop and manufacture the next generation Airbrust Cartridge for the 30MM X M813 Bushmaster and Chain Gun. Furthermore, this XM813 and Bushmaster Chain Gun required the same 30x173MM cannon combined on air, land, and naval platforms across the globe.

REPORT COVERAGE

The research report delivers a detailed analysis of the market and emphasizes key aspects such as key players, offerings, objects, and end-users of 30MM ammunition. Moreover, the report deals with insights into market trends, competitive landscape, market competition, product pricing, regional analysis, market players, competition landscape, and the market status and highlights key industry growths. In addition to the factors stated above, the report encompasses several direct and indirect influences that have subsidized the sizing of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.30% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Weapon Type

|

|

By Ammunition Type

|

|

|

By Platform

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the United States Contract Research Organization (CROs) Market is projected to grow from USD 17.5 Billion in 2023 to USD 54.5 Billion by 2033, at a CAGR of 12.03% during the forecast period 2023–2033.

The market will likely grow at a CAGR of 4.30% over the forecast period (2026-2034).

The growth is driven by increased outsourcing of R&D by pharmaceutical and biotech companies, a rise in clinical trial activity, cost efficiency offered by CROs, and technological advancements in drug development.

Clinical research services dominate the U.S. CRO market, especially Phase III and Phase II trials, followed by data management, regulatory consulting, preclinical testing, and post-approval services.

Key players in the U.S. CRO market include IQVIA Inc., ICON plc, Syneos Health, Charles River Laboratories, Parexel International, and Medpace. These companies offer comprehensive clinical and preclinical development solutions.

CROs help pharmaceutical companies reduce drug development costs, improve time-to-market, ensure regulatory compliance, and access global trial networks, which enhances R&D productivity and efficiency.

Key challenges include regulatory complexities, increasing trial costs, high competition, and ensuring data privacy and quality control during outsourced operations.

Therapeutic areas with high CRO involvement include oncology, cardiology, neurology, infectious diseases, and rare diseases, due to the high number of clinical trials and funding in these sectors.

Yes, digital tools like eClinical solutions, AI-driven analytics, decentralized trials, and remote monitoring are transforming how CROs manage trials, improving patient engagement and trial efficiency.

CROs assist in preparing regulatory submissions, navigating FDA guidelines, conducting audits, and ensuring that trials meet Good Clinical Practice (GCP) and ethical standards.

The U.S. CRO industry is expected to see strong growth due to increased clinical trial complexity, rising biotech investments, and expanding partnerships between CROs and pharma companies aiming for global trial execution.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us