Consumer Packaging Market Size, Share & Industry Analysis, By Material (Plastic, Paper & Paperboard, Glass, Metal, and Others), By Packaging Type (Flexible Packaging, Rigid Packaging, and Semi-Rigid Packaging), By Product Type (Bottles & Jars, Cans & Containers, Boxes & Cartons, Pouches & Bags, Trays & Clamshells, Tubes, Blister & Strip Packs, Wraps & Films, and Others), By End-use Industry (Food & Beverages, Personal Care & Cosmetics, Pharmaceuticals & Healthcare, Consumer Electronics, Industrial & Automotive, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

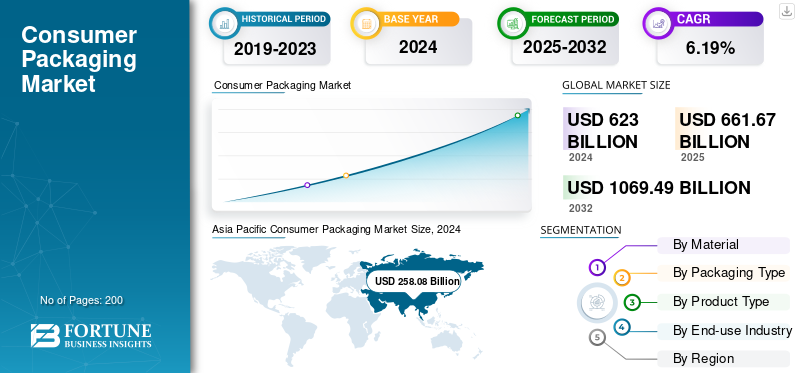

The global consumer packaging market size was valued at USD 661.67 billion in 2025. The market is projected to grow from USD 703.92 billion in 2026 to USD 1,245.30 billion by 2034, exhibiting a CAGR of 7.39% during the forecast period. Asia Pacific dominated the global market with a share of 42.04% in 2025.

The consumer packaging market plays a pivotal role in safeguarding, presenting, and promoting products across diverse industries such as food and beverages, personal care, healthcare, household goods, and electronics. It encompasses a wide range of materials, such as plastic, paper and paperboard, metal, glass, and flexible laminates, engineered to ensure product protection, convenience, and extended shelf life. In recent years, the market has undergone a significant transformation driven by evolving consumer lifestyles, rapid urbanization, and the growing influence of e-commerce. Sustainability has emerged as a defining trend, prompting manufacturers to shift toward materials such as biodegradable plastics, recyclable and lightweight packaging solutions.

Additionally, innovations in smart and active packaging technologies are enhancing product traceability, freshness, and safety, further reshaping the industry landscape. Government regulations aimed at reducing plastic and other packaging waste and carbon emissions are accelerating the adoption of eco-friendly alternatives, while brand owners increasingly view packaging as a key differentiator in marketing and consumer engagement. With rising global consumption and a heightened emphasis on environmental responsibility, the consumer packaging market growth is expected to experience robust growth, characterized by material diversification, design innovation, and digital integration across the value chain.

Leading players in the consumer packaging market analysis, including Amcor plc, Berry Global, Mondi Group, Smurfit Kappa, and Sealed Air Corporation, are actively investing in automation, lightweighting technologies, and circular material innovations to enhance efficiency and reduce environmental impact. Companies are increasingly shifting toward mono-material and recyclable packaging formats, aligning with global sustainability mandates and consumer demand for eco-conscious products. Strategic partnerships between packaging manufacturers and FMCG, foodservice, and e-commerce brands are expanding, aiming to develop customized, brand-centric designs that improve shelf appeal and functionality. In addition, the integration of digital printing and smart labeling is enabling better traceability, product authentication, and interactive consumer engagement.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Integration of Smart Materials and Biodegradable Polymers to Drive Market Demand

Technological advancements in sustainable packaging industry is increasingly driven by the development and integration of smart materials and biodegradable polymers. Unlike conventional packaging, these innovative materials reduce environmental impact and improve product shelf life, consumer convenience, and brand perception. Companies are now leveraging nanotechnology, bio-based polymers, and active packaging materials to meet evolving consumer demands for sustainability while maintaining performance standards.

One key aspect is the rise of biodegradable and compostable polymers derived from renewable sources such as cornstarch, sugarcane, and cellulose. These materials can decompose under natural conditions, significantly lowering their ecological footprint compared to traditional plastics.

- For instance, in August 2025, Nestlé announced a new line of snack packaging made from bio-based polymers that are fully compostable and designed to degrade within six months in industrial composting facilities. This reflects a broader industry trend, where multinational companies are actively incorporating research-driven sustainable solutions to comply with global environmental regulations and align with the circular economy principles.

MARKET RESTRAINTS

High Costs and Supply Chain Challenges of Sustainable Packaging Materials Hinder Market Growth

One of the most significant restraints in the global consumer packaging market is the high cost and supply chain complexity associated with advanced and eco-friendly packaging materials. While the shift toward eco-friendly and technologically advanced packaging is accelerating, manufacturers often face financial and operational challenges in sourcing, producing, and scaling these materials for mass-market applications. Compared to conventional plastics or metals, biodegradable polymers, compostable films, and smart packaging components come at a premium price, making large-scale adoption economically challenging for many brands, particularly small and medium-sized enterprises (SMEs).

The cost disparity stems from multiple factors. First, raw materials for sustainable packaging such as polylactic acid (PLA), cellulose-based films, or bio-resins are less abundant and more labor-intensive to produce than petroleum-based plastics. Additionally, the manufacturing processes for these materials often require specialized equipment, temperature-controlled processing, or precise blending techniques, all of which increase production overheads.

- For instance, in September 2025, a report from a European packaging consortium highlighted that SMEs in the region faced a 25–30% higher production cost for compostable food packaging compared to conventional plastic alternatives, limiting their ability to competitively price their products.

MARKET OPPORTUNITIES

Rising Demand for E-commerce and Customized Packaging Solutions Fuels Market Expansion

The global consumer packaging market is witnessing a significant growth opportunity driven by the rapid expansion of e-commerce and the increasing demand for personalized and customized packaging solutions. With online retail experiencing exponential growth, particularly in regions such as North America, Europe, and Asia-Pacific, there is a heightened need for packaging that ensures product protection during transit, enhances brand experience, and provides convenience for consumers. E-commerce packaging demands durability, lightweight materials, and innovative design, creating fertile ground for packaging companies to innovate and expand their offerings.

A key aspect of this opportunity is the rise of customized and branded packaging solutions. Consumers today are more conscious of the unboxing experience, often sharing it on social media, which creates marketing value beyond the product itself. Companies are leveraging this trend to differentiate their brands and strengthen customer loyalty.

- For example, in October 2025, Tetra Pak announced a partnership with a leading Asian e-commerce platform to provide customizable, sustainable cartons featuring brand-specific designs and QR codes for consumer engagement. This move reinforced the brand’s commitment to and catered to the growing trend of personalized consumer experiences.

CONSUMER PACKAGING MARKET TRENDS

Growing Adoption of Sustainable and Eco-Friendly Packaging Solutions Is Key Market Trend

A prominent trend shaping the global consumer packaging market share is the accelerated adoption of sustainable and eco-friendly packaging solutions. Driven by increasing consumer awareness, stricter environmental regulations, and corporate sustainability commitments, companies across industries are shifting from traditional plastics and non-recyclable materials toward renewable, recyclable, and biodegradable alternatives. This trend addresses environmental concerns and serves as a competitive differentiator in a market where consumers increasingly value brands that demonstrate responsibility toward the planet.

A key driver behind this trend is regulatory pressure worldwide. Governments and international organizations are introducing bans on single-use plastics, incentives for recycled materials, and mandates for sustainable packaging in specific sectors.

- For instance, in July 2025, the European Union updated its Single-Use Plastics Directive, urging consumer goods manufacturers to adopt recyclable, compostable, or reusable packaging. Compliance with such regulations has become a critical strategic priority, prompting companies to innovate in material selection and packaging design.

MARKET CHALLENGES

Rising Raw Material Costs and Supply Chain Volatility Hinder Market Expansion

One of the foremost challenges facing the global consumer packaging market is the escalating cost of raw materials combined with ongoing supply chain volatility. Packaging manufacturers rely heavily on materials such as plastics, paper, metals, and glass, which are increasingly affected by price fluctuations, geopolitical tensions, and environmental regulations. This unpredictability impacts profit margins and complicates production planning and market pricing strategies.

In recent years, global events such as the COVID-19 pandemic, regional trade disputes, and energy crises have exposed critical vulnerabilities in the packaging supply chain. For example, the rising cost of recycled plastics, which are critical for sustainable packaging solutions, has significantly affected manufacturers aiming to reduce their environmental footprint.

- In August 2025, a European packaging consortium reported that the average cost of post-consumer recycled (PCR) plastics increased by over 20% compared to the previous year, driven by higher collection, processing, and transportation expenses. Such fluctuations make it difficult for brands to maintain competitive pricing while meeting sustainability targets.

Download Free sample to learn more about this report.

Segmentation Analysis

By Material

Widespread Adoption of Plastic Across End-User Industries Boosted Segment Growth

On the basis of material, the consumer packaging market is segmented into plastic, paper & paperboard, glass, metal, and others.

In 2026, plastic dominated the segment with a market share of 45.68%, attributed to its widespread adoption across food, beverage, household, and personal care industries. Its lightweight, flexibility, cost-effectiveness, and superior barrier properties make it the preferred choice for preserving product freshness and extending shelf life. Moreover, the ease of molding, sealing, and printing enhances its suitability for high-volume and customized packaging formats.

- Leading players such as Amcor plc, Berry Global, and Sealed Air Corporation continue to advance recyclable and mono-material plastic packaging solutions to meet sustainability goals.

The paper and paperboard segment is witnessing strong growth, driven by the increasing shift toward eco-friendly and compostable packaging alternatives, particularly in foodservice and e-commerce sectors. Glass packaging retains relevance in premium beverages and cosmetics due to its inertness and recyclability, while the metal segment, led by aluminum cans and containers benefits from high durability and product protection in food and aerosol packaging.

By Packaging Type

Flexible Packaging Segment Dominated due to Its Benefits

On the basis of packaging type, the consumer packaging market is segmented into flexible packaging, rigid packaging, and semi-rigid packaging.

In 2026, flexible packaging dominated the segment with a market share of 45.89%, driven by its lightweight, cost-effectiveness, and versatility across food, beverage, personal care, and e-commerce applications. Flexible formats such as pouches, bags, and sachets provide excellent barrier properties, easy sealing, and extended shelf life, making them highly attractive for fast-moving consumer goods. Additionally, the ability to customize designs, incorporate multi-layer films, and integrate smart or active packaging features has further strengthened the adoption of flexible packaging globally.

The rigid packaging segment, which includes pet bottles, jars, and cartons, remains significant due to its robust protection, reusability, and premium appearance, particularly in beverages, cosmetics, and pharmaceutical sectors. The semi-rigid packaging category, such as trays and clamshells, is gaining traction in frozen food, ready-to-eat meals, and electronics due to its balance of strength and lightweight properties. Overall, the packaging type landscape highlights a strong preference for flexible solutions, while rigid and semi-rigid formats continue to grow in specialized applications, supported by sustainability and material optimization initiatives.

By Product Type

Pouches & Bags Segment Led the Market due to its Cost-Effective Nature

On the basis of product type, the consumer packaging market is segmented into bottles & jars, cans & containers, boxes & cartons, pouches & bags, trays & clamshells, tubes, blister & strip packs, wraps & films, and others.

In 2026, pouches & bags dominated the segment with a market share of 20.72%, owing to its lightweight, flexible, and cost-effective nature, which makes it highly suitable for food, beverages, personal care, and household applications. These formats offer excellent barrier properties, ease of sealing, and convenient portability, driving their adoption in both retail and e-commerce channels.

The bottles & jars segment continues to hold significant market relevance, particularly in beverages, cosmetics, and pharmaceutical sectors due to its premium appearance, durability, and reusability.

Cans & containers maintain steady demand in processed foods and beverages, while trays & clamshells are increasingly used in ready-to-eat meals and frozen foods.

Other segments, including tubes, blister packs, and wraps & films, are witnessing niche growth driven by specialized applications. Overall, the product type landscape emphasizes a strong preference for pouches & bags, supported by innovation, convenience, and sustainability trends in molded pulp packaging.

By End-use Industry

Widespread Usage in Packaged Foods and Ready-to-Eat Products Supplemented Food & Beverages Segment Growth

On the basis of end-use industry, the consumer packaging market is segmented into food & beverages, personal care & cosmetics, pharmaceuticals & healthcare, consumer electronics, industrial & automotive, and others.

To know how our report can help streamline your business, Speak to Analyst

In 2026, food & beverages dominated the segment with a market share of 43.30%, driven by the high demand for sustainable packaging solutions, molded pulp and other across packaged foods, ready-to-eat meals, dairy, beverages, and confectionery products. Packaging in this segment is favored for its excellent barrier properties, lightweight nature, cost-efficiency, and ability to maintain product freshness, making it highly suitable for fast-moving consumer goods.

The personal care & cosmetics segment is witnessing steady growth due to rising demand for premium, visually appealing, and sustainable packaging solutions. Pharmaceuticals & Healthcare benefit from tamper-evident, protective, and compliance-focused packaging, while consumer electronics and industrial & automotive segments increasingly require customized protective and transport packaging.

Consumer Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific Consumer Packaging Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

In 2025, Asia Pacific represented USD 278.18 Billion, accounting for 42.04% of the worldwide market, and is projected to grow to USD 300.31 Billion in 2026. The region remains the largest market, supported by rapid urbanization, rising e-commerce penetration, increasing disposable incomes, and strong demand for both traditional and innovative packaging solutions. China, India, Japan, and Southeast Asian countries continue to drive packaging consumption across multiple end-use industries. The China market is projected to reach USD 124.95 Billion in 2026, while the India market is projected to reach USD 51.05 Billion in 2026 and the Japan market is projected to reach USD 34.36 Billion in 2026.

- In July 2025, Dow introduced its innovative INNATE TF 220 Precision Packaging Resin, designed to enhance the recyclability and performance of flexible plastic packaging. This resin is utilized in the production of BOPE (Biaxially Oriented Polyethylene) films, which are commonly applied in packaging for food, personal care, and cleaning products.

Europe

Europe recorded a market size of USD 171.75 Billion in 2025, capturing 25.96% of the global market share, and is projected to reach USD 181.45 Billion in 2026. The region continues to witness strong demand for sustainable and technologically advanced packaging solutions. Regulatory initiatives promoting recyclable, reusable, and biodegradable packaging materials are encouraging manufacturers to adopt environmentally friendly packaging formats. The UK market is projected to reach USD 22.21 Billion in 2026, while the Germany market is projected to reach USD 32.92 Billion in 2026.

North America

The North America market accounted for USD 150.33 Billion in 2025, representing 22.72% of the global industry, and is expected to reach USD 157.95 Billion in 2026. High consumer awareness, stringent environmental regulations, and the presence of leading packaging manufacturers continue to support market growth. Sustainability initiatives and increasing adoption of recyclable and compostable packaging solutions are accelerating innovation across the region. The U.S. market is projected to reach USD 115.34 Billion in 2026.

Latin America

The Latin America market was valued at USD 47.12 Billion in 2025, capturing 7.12% of global revenue, and is estimated to reach USD 49.43 Billion in 2026. Growth in the region is supported by expanding food & beverage, personal care, and consumer goods industries. Rising urbanization and increasing demand for packaged products are contributing to market expansion, although supply chain and infrastructure challenges remain key considerations.

Middle East & Africa

Middle East & Africa contributed 2.16% to the global market in 2025, with a valuation of USD 14.29 Billion, and is projected to reach USD 14.79 Billion in 2026. Market growth is driven by urbanization, expansion of organized retail, and increasing demand for packaged consumer products. Regulatory support for modern packaging solutions and investments in manufacturing infrastructure are further supporting regional market development.

COMPETITIVE LANDSCAPE

Key Industry Players

Wide Range of Product Offerings, Coupled with a Strong Distribution Network of Key Companies, Supported their Leading Position

The global consumer packaging market shows a semi-concentrated structure with numerous small-to-mid-size companies actively operating across the globe. These players are actively engaged in product innovation, strategic partnerships, and geographic expansion.

Amcor, Mondi, and Berry Global are some of the dominating players in the market. Their comprehensive portfolios of metalized films and laminates, global presence through extensive manufacturing and distribution networks, and continuous investment in sustainable flexible packaging innovations are a few factors supporting their market dominance.

Apart from this, other prominent players in the market include Smurfit Kappa Group, Sealed Air Corporation, WestRock Company, and Huhtamaki Oyj. These companies are undertaking various strategic initiatives such as mergers & acquisitions, capacity expansions, and development of recyclable consumer packaging structures to enhance their market presence and meet the rising demand across the food, pharmaceuticals, and personal care industries.

LIST OF KEY CONSUMER PACKAGING COMPANIES PROFILED

- Amcor plc (Switzerland)

- Mondi Group (Austria)

- Berry Global Inc. (U.S.)

- Smurfit Kappa Group (Ireland)

- Sealed Air Corporation (U.S.)

- WestRock Company (U.S.)

- Huhtamaki Oyj (Finland)

- DS Smith plc (U.K.)

- Sonoco Products Company (U.S.)

- Tetra Pak International S.A. (Switzerland)

- Graphic Packaging Holding Company (U.S.)

- Constantia Flexibles Group GmbH (Austria)

- International Paper Company (U.S.)

- ALPLA Werke Alwin Lehner GmbH & Co KG (Austria)

- Crown Holdings, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Confectionery company Cadbury is rolling out 300,000 paper-based ‘Heroes’ tubs, in a U.K.-first initiative aimed at cutting plastic waste and testing consumer appetite for recyclable packaging.

- August 2025: Mondi, a global leader in sustainable packaging and paper, is expanding its range of high-performance barrier papers with the rollout of FunctionalBarrier Paper Ultimate, a paper-based solution that meets even the most demanding packaging requirements.

July 2025 - Amcor collaborated with Mediacor to launch a 2-litre spouted stand-up pouch for its Nana brand liquids (home-care / cleaning) in Italy, Germany & Austria, which is recycle-ready and supports post-consumer recycled content. - April 2025: Stora Enso is expanding its core packaging material offering with the launch of Performa Nova, a next-generation folding boxboard (FBB) that combines high yield with exceptional performance. The new board is designed to meet the growing demand for renewable, recyclable, and efficient packaging solutions in segments such as dry, frozen, and chilled food, chocolate, and confectionery.

- October 2025: US-based packaging company Closure Systems International (CSI) has unveiled the Omni mini XP 26mm closure. The newly developed closure is designed for carbonated cold-fill and ambient-fill beverage applications. The launch adds to the company’s range of sustainable packaging solutions for PET non-returnable bottles.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.39% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material, By Packaging Type, By Product Type, and By End-use Industry and Region |

|

By Material |

|

|

By Packaging Type |

|

|

By Product Type |

|

|

By End-use Industry |

|

|

By Geography |

North America (By Material, Packaging Type, Product Type, End-use Industry and Country)

Europe (By Material, Packaging Type, Product Type, End-use Industry , and Country)

Asia Pacific (By Material, Packaging Type, Product Type, End-use Industry, and Country)

Latin America (By Material, Packaging Type, Product Type, End-use Industry and Country)

Middle East & Africa (By Material, Packaging Type, Product Type, End-use Industry and Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 661.67 billion in 2025 and is projected to reach USD 1,245.30 billion by 2034.

In 2025, the market value stood at USD 278.18 billion.

The market is expected to exhibit a CAGR of 7.39% during the forecast period (2026-2034).

The plastic segment led the market by material.

Integration of smart materials and biodegradable polymers is a key factor driving the market.

Amcor, Mondi, and Berry Global are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

Growing adoption of sustainable and eco-friendly packaging solutions is expected to favor market expansion.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us