Container Ship Market Size, Share & Industry Analysis, By Component (Propulsion Unit, Power Generation & Distribution, Auxiliary Equipment, Hydraulic, Ship Systems & Pumps, Ship Specific Systems, Hull & Fittings, and Navigation Aids & Communication systems), By Fuel Type (Diesel and Gasoline, Electric, LNG, LPG, and Others), By Deadweight (Below 75,000 DWT, 75,000 – 2,00,000 DWT, and Above 2,00,000 DWT), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

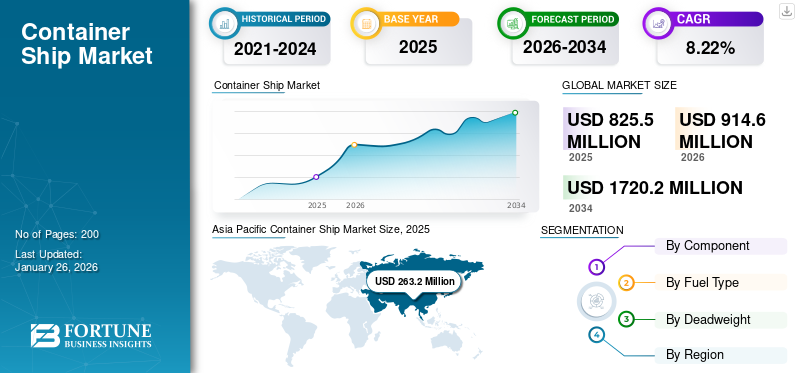

The global container ship market size was valued at USD 825.5 million in 2025 and is projected to grow from USD 914.6 million in 2026 to USD 1720.2 million by 2034, exhibiting a CAGR of 8.22% during the forecast period. Asia Pacific dominated the container ship market with a market share of 31.88% in 2025.

Container ships, commonly known as "box ships," are essential to global commerce as they ferry standardized containers that hold a significant portion of the world's manufactured products. These ships are engineered to optimize cargo capacity by using standard containers, usually measured in 20- or 40-foot equivalent units (TEUs and FEUs), which are arranged on the vessel's hatch covers and upper deck. The items inside these containers can vary from non-perishable products such as electronics and machinery to perishable goods such as fresh produce, which are frequently transported in refrigerated containers to preserve their quality during transport.

Container vessels play a fundamental role in commercial intermodal freight transport, functioning on regular liner services that link significant major ports around the globe. This framework facilitates the efficient and economical modes of transport between continents, bolstering international trade and economic development aids market growth.

Download Free sample to learn more about this report.

Global Container Ship Market Key Takeaways

Market Size & Forecast

- 2025 Market Size: USD 825.5 million

- 2026 Market Size: USD 914.6 bmllion

- 2034 Forecast Market Size: USD 1720.2 million

- CAGR: 8.22% from 2026–2034

Market Share

- Asia Pacific dominated the container ship market with a 31.88% share in 2025, driven by its extensive shipbuilding industry, strong manufacturing exports, and rising maritime trade across China, South Korea, and Japan. The region’s established infrastructure, skilled workforce, and competitive pricing have positioned it as the global leader in container ship production and operation.

- By deadweight, the 75,000–200,000 DWT segment held the largest share in 2024, offering a cost-effective balance between cargo capacity and operational flexibility, making it suitable for both major and regional ports.

Key Country Highlights

- China: Leads global shipbuilding with significant capacity expansions, green technology adoption, and strategic initiatives like the Belt and Road, boosting container ship demand.

- United States: Maritime trade and port modernization projects drive steady demand, though trade policies and tariffs influence growth trends.

- Japan & South Korea: Remain key shipbuilders, focusing on high-tech, energy-efficient vessels to maintain competitive advantage in global shipping markets.

- Europe: Growth supported by advanced green shipbuilding practices and adoption of autonomous vessel technologies in specialized markets.

MARKET DYNAMICS

MARKET DRIVERS

Rise in Maritime Trade, Government Backing, and Strategic Partnerships to Boost the Market

The global shipping sector accounts for approximately 80% of international trade. The expansion of maritime trade offers advantages to consumers globally by providing lower shipping costs. Key factors contributing to the industry's continued container ship market growth include enhanced efficiency in containerized shipping solutions as a transportation method and greater economic liberalization.

- For instance, reports indicate that the volume of traffic on the Northern Sea Route is projected to reach 80 million tons of cargo annually by 2025 in Arctic shipping. This swift growth presents economic, environmental, political, and social issues that various governments are currently prioritizing.

In recent years, there has been consistent growth in ship deliveries worldwide from nations that are not part of the OECD Council Working Party on Shipbuilding (WP6). In 2021, non-WP6 countries accounted for 47.4% of global deliveries, largely due to the swift increase in ship completions in China, which represented 41.1% of total global completions.

- For instance, in November 2024, Hapag-Lloyd entered into agreements with two Chinese shipyards for a total of 24 new container vessels. Among these, Yangzijiang Shipbuilding Group will construct 12 new ships, each capable of carrying 16,800 TEU. These vessels will enhance the capacity of existing services. Additionally, New Times Shipbuilding Company Ltd. will produce 12 more ships, each with a capacity of 9,200 TEU.

MARKET RESTRAINTS

Cyclic Nature of the Market Raises Concern about Annual Shipbuilding Capacity, Order Backlog, and Profitability of Shipbuilders Hamper Market Growth

The shipbuilding sector experiences cycles, leading to surplus capacity challenges for shipbuilders during peak periods, which impacts operational processes and the profitability of manufacturers. Due to this cyclical pattern and the rising costs of raw materials, particularly steel, most manufacturers have encountered losses in recent years.

In addition to a few companies, leading shipbuilders such as Korea Shipbuilding & Offshore Engineering Co. (KSOE), Samsung Heavy Industries, and Daewoo Shipbuilding & Marine Engineering Co. have been experiencing financial losses in recent years. The primary reasons for these losses include stagnant contract prices, extended contract durations, and rising material costs. As a result, the number of shipyards has declined over the past twenty years.

Typically, delivering a ship from the time a contract is signed requires a timeframe of two to three years. As a result of the competitive and consolidated market, manufacturers experience decreased profitability under fixed-price contracts. For instance, Samsung Heavy Industries is projected to have incurred a cumulative loss exceeding USD 4.5 billion since 2015 despite a significant number of orders. Numerous other companies in the industry face similar challenges.

MARKET OPPORTUNITIES

Major Breakthroughs in Container Design Are Influencing the Progress of Future Transportation and Driving Market Expansion

The focus on bigger ships highlights the significance of economies of scale, though it requires considerable investments in port facilities. Factors such as port accessibility and cargo throughput remain influential in the transformation of container vessels, reflecting the need to balance technological advancements with economic viability.

In recent times, there has been significant research and development in autonomous shipping technologies. Different companies and research organizations are investigating the viability of unmanned or autonomous cargo ships with the goal of improving efficiency and lowering operational expenses. These innovative designs picture ships outfitted with sophisticated sensor systems, artificial intelligence, and autonomous navigation functions, which could fundamentally transform the maritime sector.

Furthermore, the design of future container vessels goes beyond size and carrying capacity. New ideas for next-generation container ships feature advanced propulsion methods, including hydrogen fuel cells and wind-assisted technology. Moreover, there is an increasing focus on modular ship designs that allow for rapid adjustments to evolving cargo needs and operational demands.

MARKET CHALLENGES

Geopolitical and Trade Disruptions Challenge Market Growth

Overcapacity and Rate Volatility: The influx of new ultra-large container vessels is surpassing demand, resulting in surplus capacity and fluctuating freight rates, which complicates profitability for shipping companies.

Port Congestion and Infrastructure Bottlenecks: Key ports, particularly in Asia, Europe, and North America, are facing considerable congestion due to rising cargo volumes, a shortage of labor, and aging infrastructure, leading to delays and increased expenses.

Geopolitical and Trade Disruptions: Current geopolitical tensions, changes in trade policies, and regional conflicts (including the Red Sea crisis and US-China trade disputes) are interrupting shipping routes and generating uncertainty in global trade patterns.

Rising Operational and Regulatory Costs: Adherence to more stringent environmental regulations, such as the IMO's EEXI and CII, along with varying fuel prices and heightened tariffs, is driving up expenses, particularly affecting smaller operators.

CONTAINER SHIP MARKET TRENDS

Industries Evolve Significantly Due to Growing Need for Greater Efficiency, Sustainability, and Transparency

Autonomous and Automated Ships: Autonomous ships driven by AI and automation in cargo management are minimizing the need for human involvement, enhancing safety, and decreasing operational expenses.

Smart Containers and IoT: Containers fitted with IoT sensors, GPS, and RFID enable real-time tracking, monitor cargo conditions, and improve visibility in the global supply chain efficiency.

Big Data and Analytics: Sophisticated analytics enhance route planning, forecast maintenance requirements, and boost fuel efficiency, resulting in cost reductions and lower emissions.

Green Technologies: Sustainable propulsion technologies, such as electric, hybrid, and wind-assisted vessels, along with designs focused on energy efficiency, are aiding the industry in complying with more stringent environmental regulations.

Digital Twins and Predictive Maintenance: Digital representations of vessels and cargo facilitate immediate oversight and forecasted upkeep, reducing both downtime and operational interruptions.

- Asia Pacific witnessed container ship market growth from USD 5.06 Billion in 2023 to USD 6.46 Billion in 2024.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component

Surging Need to Transport Goods Efficiently Fueled Demand for Ship Specific Systems

Based on component, the market is classified into propulsion unit, power generation & distribution, auxilary equipment, hydraulic, ship systems & pumps, ship specific systems, hull & fittings, and navigation aids & communication systems.

The ship specific systems segment dominated the global container ship market share in 2024. The system covers the lashing systems, buttress systems, hatch covers, cargo cranes, energy systems, and so on. These systems are integral to the operation of container ships, enhancing their ability to transport goods efficiently and safely across the globe. Overall, the growth of the global shipping industry is closely tied to the development and optimization of ship-specific systems, which play a crucial role in enhancing operational efficiency, safety, and sustainability.

By Fuel Type

Significant Move Toward Decarburization Fostered Diesel and Gasoline Segment Growth

Based on fuel type, the market is divided into diesel and gasoline, electric, LNG, LPG, and others.

The diesel and gasoline segment dominated the global market share in 2024. The increasing demand for decarbonizing the environmental situation by various key players using advanced fuels and gases for marine propulsion is significantly growing the segmental growth. The shipping industry is undertaking great efforts to decarbonize and due to its drop-in compatibility, synthetic marine diesel oil (MOD) is directly replacing the conventional fossil.

For instance, in January 2023, MPC Container Ships and INERATEC signed a contract for the supply of synthetic marine diesel oil (MOD) made from biogenic CO2 and renewable hydrogen.

By Deadweight

75,000 – 2,00,000 DWT Segment Led the Market as It is Cost-Effective to Operate Than Mega Ships

Based on deadweight, the market is segmented into Below 75,000 DWT, 75,000 – 2,00,000 DWT, and Above 2,00,000 DWT.

The 75,000 – 2,00,000 DWT segment dominated the global market in 2024 and is estimated to be the fastest-growing segment during the forecast period. Ships in this DWT range strike a balance between cargo capacity and navigational adaptability, and smaller ports and regional routes often lack infrastructure for ultra-large vessels, making mid-sized ships essential for broader geographic coverage. Moreover, Mid-sized ships are more cost-effective to operate than mega-ships, which require specialized crew and consume significantly more fuel.

- For instance, in January 2022, K Shipbuilding, Korea, signed a contract to build a container ship. The build period of the tanker was 1129 days. Under the contract, the company built 1,92,000 DWT, and the total value of the contract was around USD 130 million. The scheduled delivery of the ship is in 2025.

Container Ship Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Container Ship Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for the largest share in 2025 and is likely to remain dominant throughout the forecast period. In 2025, Asia Pacific generated USD 263.2 million, contributing 31.88% to global market revenue, and is projected to grow to USD 293.5 million in 2026. The Asia Pacific region, particularly China, South Korea, and Japan, accounts for a significant portion of global shipbuilding output. This dominance is due to established infrastructure, skilled labor, and competitive pricing. The region is driven by strong demand for efficient cargo vessels, technological advancements, and supportive government policies.

- According to the UNCTAD Report 2022, 94% of global shipbuilding occurred in China, the Republic of Korea, and Japan in 2022. In addition, half of the world's fleet is owned by the Asian Companies.

- Dominates the shipbuilding industry with a significant share of global orders. China continues to expand its capacity and adopt green technologies.

North America

The North America region captured 19.28% of the global market in 2025, generating USD 159.2 million in revenue, and is projected to reach USD 175.8 million in 2026. The North American market is influenced by various factors, including trade dynamics, capacity growth, and geopolitical events. The U.S. continues to be a significant player in North American trade, with strong demand for imports. However, potential tariff increases and trade policies could impact this demand. These countries also play important roles in regional trade, with Canada focusing on diversifying its trade partners and Mexico experiencing high market rates despite capacity additions.

Europe

Europe maintained a strong presence in the global market, reaching USD 210.9 million in 2025, accounting for 25.55% share, and is expected to reach USD 237.1 million in 2026. Europe holds a significant position in the global market. The European shipbuilding industry is expected to grow, driven by technological advancements, green shipbuilding practices, and demand for specialized vessels. European shipyards are at the forefront of integrating advanced technologies such as green shipbuilding practices and autonomous vessel technologies. This expertise helps maintain their competitive position in specialized vessel construction.

Rest of the World

The rest of the World consists of Middle East & Africa and Latin America. The Latin America market generated USD 84 million in 2025, representing 10.17% of the global market landscape, and is expected to reach USD 89.8 million in 2026. The Middle East & Africa region is experiencing growth driven by strategic locations, infrastructure investments, and increasing maritime trade. Middle East & Africa recorded a market size of USD 108.3 million in 2025, capturing 13.12% of the global market share, and is projected to reach USD 118.4 million in 2026. The Middle East, particularly countries such as UAE, is strategically positioned at the crossroads of international trade routes. This location enhances its role as a major trading hub, driving demand for container ships. Furthermore, governments in Latin America are investing in port congestion expansions and modernization, which enhances the capacity for shipbuilding and repair operations. Economic growth in Latin America contributes to increased demand for maritime services, including container ships. This growth is driven by expanding industries such as agriculture, energy, and manufacturing.

COMPETITIVE LANDSCAPE

Key Industry Players

Ongoing Technological Advancements and the Launch of Innovative Products by Leading Firms Have Led to Their Prevailing Presence in the Market

The container shipbuilding industry is highly competitive, with key players competing on factors such as technological innovation, production capacity, and cost efficiency.

The shipbuilding industry is dominated by Asian countries, particularly South Korea, China, and Japan. These nations have large-scale shipyards with high production capacities and competitive pricing, making them leaders in the global market. Major companies such as Hyundai Heavy Industries, Samsung Heavy Industries, and China State Shipbuilding Corporation are at the forefront of the industry. They focus on developing eco-friendly vessels and implementing advanced technologies to enhance efficiency.

The container ship industry is characterized by intense competition among Asian leaders, technological innovation, and strategic alliances. The focus on sustainability and digitalization is expected to drive future growth and competitiveness in the market.

LIST OF KEY CONTAINER SHIP COMPANIES PROFILED

- Damen Shipyards Group (Netherlands)

- COSCO SHIPPING LINES CO., LTD (China)

- Hanwha Ocean (South Korea)

- Hyundai Heavy Industries (South Korea)

- Japan Marine United Corporation (Japan)

- Kawasaki Heavy Industries (Japan)

- Garden Reach Shipbuilders & Engineers (India)

- Mitsubishi Heavy Industries (Japan)

- Samsung Heavy Industries (South Korea)

KEY INDUSTRY DEVELOPMENTS

- February 2025: Samsung Heavy Industry revealed that it has completed the delivery of its inaugural large container vessel with a capacity of 15,000 TEU, which features SAVER WIND, a self-engineered device for air assistance reduction.

- February 2025: Shipping powerhouse MSC has placed an order for as many as eight 22,000 TEU liquefied natural gas dual-fuel container vessels in China. Zhoushan Changhong International Shipyard announced that it has entered into an agreement for 4+2+2 environmentally friendly units with MSC.

- November 2024: Samsung Heavy Industries has revealed that it has entered into a contract to construct four container ships, each with a capacity of 16,000 TEU (Twenty-foot Equivalent Unit), for an Asian shipowner. The overall value of the contract is 1.0985 trillion won, and the delivery of these vessels is planned for December 2027.

- September 2024: Lloyd’s Register (LR) and Samsung Heavy Industries (SHI) signed a joint development project (JDP) focused on an ammonia-powered container ship with a capacity of 9,300 TEU. As part of this agreement, SHI will partner with Eastern Pacific Shipping to perform design studies for the ammonia-powered container vessel. At the same time, LR will assess SHI's outputs and provide technical guidance for subsequent design enhancements.

- September 2024: Hanwha Ocean Co., the third-largest shipbuilder in South Korea, announced it secured its inaugural container ship contract from A.P. Moller–Maersk A/S, the world's second-largest shipping firm, in a transaction valued at approximately USD 2.2 billion.

REPORT COVERAGE

The global container ship market analysis provides market size & forecast by all the segments included in the report. It includes details on the market dynamics and global market trends expected to drive the container ship market growth in the forecast period. It offers information on the prevalence of malocclusion in key regions/countries, key industry developments, new product launches, details on partnerships, mergers & acquisitions and number of orthodontists in key countries. The report covers detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.22% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Component

|

|

By Fuel Type

|

|

|

By Deadweight

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 825.5 million in 2025 and is projected to reach USD 1720.2 million by 2034.

In 2025, the market value stood at USD 263.2 billion.

The market is expected to exhibit a CAGR of 8.22% during the forecast period of 2026-2034.

By component, the ship specific systems segment dominated the market in 2025.

The rise in maritime trade, government backing, and strategic partnerships will boost the market.

Damen Shipyards Group (Netherlands), Hyundai Heavy Industries (South Korea), and Samsung Heavy Industries (South Korea) are the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us