Marine Hybrid Propulsion Market Size, Share & Industry Analysis, By Operation Type (Parallel Hybrid Propulsion System and Serial Hybrid Propulsion System), By RPM (0-250, 250-500, 500-750, 750-1000, and Above 1000), By Power Rating (Up to 100, 100–500, 500–1,000, and Above 1,000), By Component (I.C. Engine, Generator, Power Management System, Battery, Gearbox, and Others), By Ship Type (Container Ship, Passenger Ship, Fishing Vessel, Tugs, Offshore support vessels, Ferries, Yacht, Tanker, and Others), By Installment (Line Fit and Retrofit), and Regional Forecast 2026-2034

(Offer valid till 15th Jul 2026)

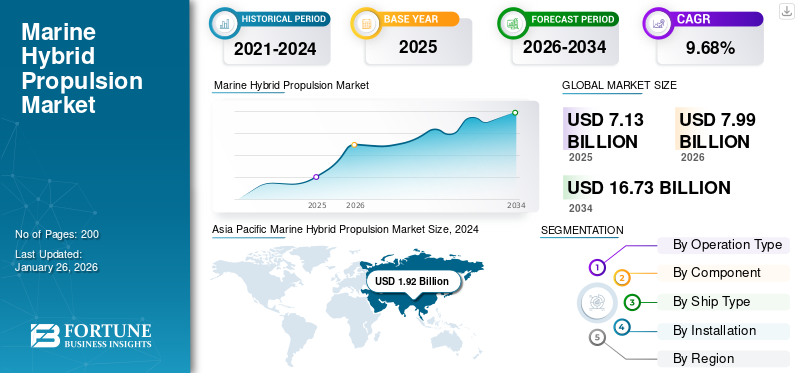

Marine Hybrid Propulsion Market Size and Future Outlook

The global marine hybrid propulsion market size was valued at USD 8.86 billion in 2025. The market is projected to grow from USD 9.62 billion in 2026 to USD 22.45 billion by 2034, exhibiting a CAGR of 11.17% during the forecast period. Asia Pacific dominated the marine hybrid propulsion market with a market share of 44.36% in 2025.

Marine hybrid propulsion refers to ship propulsion systems that combine conventional prime movers (typically diesel or dual‑fuel engines) with electric motors, batteries, and an energy management system to optimize power use. These systems allow vessels to operate on electric power in ports and low‑load conditions, while switching to mechanical or diesel‑electric drive for transit or high‑power operations.

The market is growing significantly because hybrid systems directly address tightening emissions and environmental regulations and fuel‑cost pressures in shipping. IMO decarbonization measures, CII and EEXI rules, and regional schemes such as EU ETS and FuelEU Maritime are pushing owners to cut greenhouse‑gas and pollutant emissions without sacrificing operational flexibility. Hybrid architectures can deliver 10–40% fuel savings depending on duty cycle, reduce engine hours, and enable zero‑emission operation in ports and emission control areas, which improves both compliance and total cost of ownership.

Competitionally, the landscape is fragmented but led by large marine and electrical OEMs that supply integrated hybrid packages. Companies such as ABB, Wärtsilä, Siemens, MAN Energy Solutions, Nidec, Caterpillar, GE, and BAE Systems leverage extensive references, global service networks, and strong systems‑integration capabilities to dominate large commercial and naval projects, especially in diesel‑electric configurations.

Download Free sample to learn more about this report.

Marine Hybrid Propulsion Market Trends

Battery‑Centric Hybridization Programs and Digital Energy Management Catalyze the Market Trends

Technologically, marine hybrid propulsion is evolving rapidly from relatively simple battery‑assisted diesel‑electric concepts toward highly integrated power systems that combine large‑scale energy sources, DC distribution, sophisticated energy management software, and, increasingly, interfaces to alternative fuels and shore power.

DNV's guideline for large maritime battery systems and its "Battery and hybrid ships" advisory underscore how all‑electric and hybrid ships with large Li‑ion batteries can deliver significant reductions in fuel cost, maintenance, and emissions, as well as improved responsiveness and safety, provided that systems are carefully sized and controlled.

Download Free sample to learn more about this report.

Market Dynamics

MARKET DRIVER

Growing IMO Regulatory Pressure for Decarbonisation Drives the Market Development

From a strategic standpoint, the dominant growth driver for marine hybrid propulsion is the tightening decarbonisation and air‑quality regime, which is forcing shipowners to redesign power architectures to reduce both lifecycle emissions and compliance risk.

The International Maritime Organization's 2023 GHG Strategy commits international shipping to reach net‑zero GHG emissions "by or around" 2050, with interim checkpoints of at least 20–30% absolute emission reduction by 2030 and 70–80% by 2040 versus 2008, and an explicit target that at least 5–10% of shipping energy use by 2030 should come from zero or near‑zero GHG fuels and technologies.

These ambitions are underpinned by regulatory tools such as EEDI/EEXI for design efficiency and CII for in‑service carbon intensity ratings, all of which directly reward hybrid architectures that can lower fuel consumption and allow more efficient engine loading profiles.

MARKET RESTRAINT

Commercial Demand from Charterers and Supply Chain Partners Hampers the Market Growth

A pivotal additional driver accelerating the marine hybrid propulsion market growth is the escalating commercial demand from charterers, cargo owners, and supply chain partners who are increasingly specifying low‑emission vessels in contracts to meet their own sustainability targets and de‑risk exposure to future carbon pricing.

Major liner operators such as AP Moller Maersk have explicitly integrated decarbonisation into their fleet renewal strategies, as evidenced by their December 2024 announcement of completed orders for 20 dual‑fuel vessels totaling 300,000 TEU capacity, with first deliveries in 2028 and last in 2030, as part of a broader program to phase in 800,000 TEU of methanol and liquefied gas dual‑fuel tonnage while replacing older capacity.

These vessels are designed with hybrid‑ready architectures to optimize energy use across fuels, reflecting how leading owners are positioning their fleets to win preferential charter contracts from clients demanding verifiable emissions reductions.

MARKET OPPORTUNITY

Regulatory Exposure and Public Funding Support Drive Hybrid Marine Growth Opportunities

There are several opportunity spaces for marine hybrid propulsion systems that lie in those segments where operating profiles, regulatory exposure, and public funding converge to produce compelling total‑cost‑of‑ownership advantages, notably short‑sea ferries, coastal Ro‑Pax, offshore wind and research vessels, harbor craft, and regional logistics chains.

DNV's assessment of battery and hybrid ships identifies ferry routes, offshore units, tugs, and other vessels with large load variations or extended low‑load operation as ideal candidates for hybridisation, given the potential for substantial fuel, maintenance, and emissions reductions alongside improved maneuverability and redundancy.

As governments seek to decarbonise domestic transport and regional supply chains, these segments are being specifically targeted by grant programs and public procurement strategies that lower the effective cost of capital for hybrid vessels.

MARKET CHALLENGES

High Initial Investment for Hybrid and Full-Electric Propulsion Packages Stifles the Market Growth

High initial investment for hybrid and full‑electric propulsion packages, including batteries, power electronics, and integration, remains the primary restraint. Industry reports emphasize that retrofitting existing vessels demands substantial structural and systems modifications, while the limited availability of port charging and grid upgrades outside early‑adopter regions further delays broader roll‑out.

Hybrid propulsion architectures and energy‑management systems are significantly more complex than conventional mechanical drives, raising design and integration risk for shipyards and operators and making it harder to optimize performance across diverse operating profiles. Moreover, maritime battery systems have noted that fragmented and largely optional standards for onboard energy storage and shore power can compromise safety and slow electrification, underscoring the need for clearer international rules before many owners commit at scale.

SEGMENTATION ANALYSIS

By Operation Type

Parallel Hybrid Propulsion System Leads the Market Due to Less Integration Risk and Buyer Decision Cycles

By operation type, the segment is divided into parallel hybrid propulsion systems and serial hybrid propulsion systems.

The parallel hybrid propulsion system segment dominated the global marine hybrid propulsion market share in 2025 with a value of 55.97% and is expected to holds 56.18% market share in 2026. OEM integrated hybrid packages are pulling parallel hybrids into mainstream newbuild specs, especially yachts + high-end workboats. This matters commercially because it compresses integration risk (one OEM controls the stack) and shortens buyer decision cycles.

The serial hybrid propulsion system sub-segment is estimated to be the fastest growing with the highest CAGR of 11.96% during the forecast period, and accounted for the 44.03% market share.

By RPM

Above 1000 Segment Dominates the Market Owing to High-Speed Propulsion Machinery

By RPM, the segment is segregated into 0-250, 250-500, 500-750, 750-1000, and above 1000.

Above 1000 segment dominated the market share in 2025 with 31.37% and is anticipated to be the fastest growing segment at a CAGR of 12.30% during the forecast period. This band corresponds to high-speed propulsion machinery (fast ferries, patrol/service craft, high-cycle workboats) where hybrid wins on power density, rapid response, and reduced idling. The biggest adoption driver is that the hybrid is moving into fleet orders, not prototypes.

The 750-1000 segment is estimated to be the second fastest growing during the forecast period, with a CAGR of 11.67% from 2026-2034, and accounted for the 24.98% market share.

By Power Rating

Above 1,000 Segmented Led the Market Due to Large Ports and Operators with Emissions Capability

By power rating, the segment is categorized into up to 100, 100–500, 500–1,000, and above 1,000.

Above 1,000 segment dominated the global market in 2025, accounting for 40.80% revenue, and is anticipated to be the fastest growing segment at a CAGR of 12.03% during the forecast period. The commercial driver in this band is ports and large operators treating emissions capability as contract competitiveness, not marketing. The TechCrunch coverage explicitly mentions >4,000 horsepower motors drawing from a ~6 MWh battery onboard. This is hard scale data that signals the shift to high-power operational capability.

The 500–1,000 segment is experiencing robust growth with a CAGR of 11.08% during the forecast period and accounts for the 31.53% market share in 2025.

To know how our report can help streamline your business, Speak to Analyst

By Component

Battery Segment Fuels the Market Due to Capacity Expansions On In-Service Vessels

By component, the segment is classified into I.C. engine, generator, power management system, battery, gearbox, and others.

The battery sub-segment dominated the global marine hybrid propulsion market in 2025. It accounts for 31.87% market share in 2025 and is anticipated to grow at a highest CAGR of 13.18% during the forecast period. Battery growth is accelerating from "pilot installs" to capacity expansions on in-service vessels, which is the clearest signal that ROI is proven. Wärtsilä's 27 August 2025 announcement for Wasaline's Aurora Botnia increases battery capacity by 10.4 MWh (2.2 → 12.6 MWh), a material expansion order booked in Q3 2025.

Power management system sub-segment is projected to be the second fastest growing with the highest CAGR of 12.35% during the forecast period and accounted for 12.20% in 2025.

By Ship Type

Ferries Ship Type Leads the Market Owing to High Public Visibility Conditions for Electrification Economics

By ship type, the segment is segmented into container ship, passenger ship, fishing vessel, tugs, offshore support vessels, ferries, yacht, tanker, and others.

The ferries sub-segment dominated the global market in 2025, accounting for19.79% share and is anticipated to grow at a CAGR of 12.11% during the forecast period. Ferries dominate hybrid adoption because they combine predictable routes, frequent port calls, and high public visibility conditions for electrification economics. Washington State Ferries' electrification program and ABB propulsion awards (publicly communicated in July 2024) reinforce that ferries are being procured as fleet programs, not pilots.

The offshore support vessels sub-segment is projected to be the fastest growing with the highest CAGR of 12.88% during the forecast period, and accounted for the 15.61% market share.

By Installment

Line Fit Installment Leads the Segmentation Owing to Fleet Buyers Using Hybrid as a Requirement

By installment, the segment is bifurcated into line fit and retrofit.

Line fit segment is expected to dominate the global market in 2026 as it accounting for 58.55% share and is anticipated to grow at a CAGR of 10.54% during the forecast period. Line-fit rising demand because fleet buyers are now writing hybrid as a design-in requirement (not an option), which locks propulsion electrification into the shipyard contract from the bid stage.

The retrofit sub-segment is estimated to be the fastest growing with the highest CAGR of 12.04% during the forecast period and accounted for the 40.33% market share in 2025.

Marine Hybrid Propulsion Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, the Middle East & Africa, and Latin America.

North America

The North America region captured 19.28% of the global market in 2025, generating USD 1.37 billion in revenue, and is projected to reach USD 1.54 billion in 2026. The North American marine hybrid propulsion market is experiencing rapid growth, driven by stringent emission regulations (IMO 2020), high demand for operational efficiency, and increased investment in eco-friendly maritime technologies. The market is shifting toward hybrid systems to reduce fuel costs and carbon footprints, with key applications in commercial, passenger, and offshore vessels.

U.S. Marine Hybrid Propulsion Market

Based on North America's strong contribution and the U.S. dominance within the region, the U.S. market is valued at USD 0.94 billion in 2025, and an estimated CAGR of 6.68% during the forecast period.

Europe

Europe maintained a strong presence in the global market, reaching USD 1.82 billion in 2025, accounting for 25.55% share, and is expected to reach USD 2.07 billion in 2026. Europe's hybrid market is being pulled by battery uprate programs; operators are buying more MWh post-delivery once economics and infrastructure mature.

U.K. Marine Hybrid Propulsion Market

The U.K. market share in 2025 was estimated at USD 0.34 billion and is expected to grow at a rate of 12.61% during the forecast period.

Norway Marine Hybrid Propulsion Market

The Norwegian market growth in 2025, valued at USD 0.68 billion, is expected to grow at a rate of 13.69% during the forecast period.

Germany Marine Hybrid Propulsion Market

The German market in 2025 is estimated at around USD 0.56 billion and is expected to grow at a rate of 11.29% during the forecast period.

Asia Pacific

In 2025, Asia Pacific generated USD 2.27 billion, contributing 31.88% to global market revenue, and is projected to grow to USD 2.56 billion in 2026. Asia Pacific’s demand is led by China's industrial-scale electrification of inland/coastal shipping, where operating profiles are predictable, and infrastructure can be controlled.

Asia Pacific Marine Hybrid Propulsion Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

China Marine Hybrid Propulsion Market

The Chinese market in 2025 is valued at USD 1.51 billion and is expected to grow at a rate of 12.13% during the forecast period.

India Marine Hybrid Propulsion Market

India's market in 2025, valued at USD 0.44 billion, is expected to grow at a rate of 14.35% during the forecast period.

Japan Marine Hybrid Propulsion Market

Japan's market in 2025 is valued at USD 0.67 billion and is expected to grow at a rate of 10.62% during the forecast period.

Middle East & Africa and Latin America

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market generated USD 0.73 billion in 2025, representing 10.17% of the global market landscape, and is expected to reach USD 0.78 billion in 2026. Middle East & Africa recorded a market size of USD 0.94 billion in 2025, capturing 13.12% of the global market share, and is projected to reach USD 1.03 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Niche Innovators and Battery Specialists Aid the Industry Leaders to Strengthen the Market Position

Tier-1 players such as Wärtsilä, ABB Marine, Siemens Energy, MAN Energy Solutions, and Caterpillar command over 60% share through end-to-end hybrid packages combining engines, batteries, propulsion, and digital energy management tailored for ferries, OSVs, and naval vessels. These firms leverage global service footprints, retrofit expertise, and partnerships with class societies to lock in long-term contracts, as evidenced by Wärtsilä's 150+ hybrid references by 2025. Their scale enables standardized modules that reduce CAPEX by 15–20% versus bespoke designs.

Emerging specialists such as Corvus Energy, Vard Electro, Torqeedo, and AKASOL target high-growth segments including short-sea ferries, workboats, and superyachts with compact, high-density lithium systems and peak-shaving controls that deliver 20–30% fuel savings in variable-duty cycles.

LIST OF KEY MARINE HYBRID PROPULSION COMPANY PROFILED

- BAE Systems (U.K.)

- Caterpillar Inc. (U.S.)

- General Electric Company (U.S.)

- Nidec Industrial Solutions (Italy)

- MAN Energy Solutions (Germany)

- Siemens (Germany)

- Mitsubishi Heavy Industries (Japan)

- Steyr Motors (Austria)

- Rolls-Royce (U.K.)

- SCHOTTEL GmbH (Germany)

- Torqeedo GmbH (Germany)

- AB Volvo Penta (Sweden)

- Cummins Inc. (U.S.)

KEY DEVELOPMENT

- January 2026: Chartwell Marine secures design contract for lifeline ferry. Designed in close collaboration with the ferry operator and local stakeholders, Chartwell has created a ferry with a highly customised, robust catamaran hull and a hybrid propulsion system. This will enable it to efficiently carry up to 100 passengers and cargo around the islands in an environmentally friendly way.

- January 2026: Engineering company ABB has been selected to supply various systems for four hybrid-electric vessels being built for ferry operator BC Ferries. The company will provide power, propulsion, and control systems. The ferries are part of the operator's New Major Vessels programme to replace ageing ships and reduce emissions and underwater noise in the Strait of Georgia.

- December 2025: ABB will supply comprehensive hybrid-electric propulsion packages for the Washington State Hybrid-Electric 160 Auto Ferry Program. An end-to-end system will optimize vessel reliability and efficiency and enable zero-emission operations in port and on short routes. The order initiates a Washington State Ferries' newbuild plan that recommends 16 hybrid-electric vessels by 2040.

- November 2025: Technology group Wärtsilä will supply an integrated hybrid propulsion system for a bulk carrier vessel being built at the Royal Bodewes shipyard in the Netherlands for Norwegian shipowner Aasen Shipping. This will be the latest in a series of six such vessels to operate with a similar Wärtsilä scope of supply. This order was booked by Wärtsilä in Q3 2025.

- July 2025: Finnish marine and energy equipment manufacturer Wärtsilä will supply an integrated hybrid propulsion system for four new vessels being built for Dutch ship owner and maritime service provider Vertom. The solution includes the Wärtsilä 25 engine, NOx reducer, gearbox, controllable pitch propeller (CPP), transverse thruster, and the Wärtsilä ProTouch remote propulsion control system.

REPORT COVERAGE

The global marine hybrid propulsion market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and growth expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advances, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.17% from 2026-2034 |

| Unit | USD Billion |

| Segmentation | By Operation Type, By RPM, By Power Rating, By Component, By Ship Type, By Installment |

|

By Operation Type

By RPM

By Power Rating

By Component

By Ship Type

By Installment

|

|

| Region |

North America (By Operation Type, By RPM, By Power Rating, By Component, By Ship Type, By Installment, By Country)

Europe (By Operation Type, By RPM, By Power Rating, By Component, By Ship Type, By Installment, By Country)

Asia Pacific (By Operation Type, By RPM, By Power Rating, By Component, By Ship Type, By Installment, By Country)

Middle East & Africa (By Operation Type, By RPM, By Power Rating, By Component, By Ship Type, By Installment, By Country)

Latin America (By Operation Type, By RPM, By Power Rating, By Component, By Ship Type, By Installment, By Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 8.87 billion in 2025 and is projected to reach USD 22.45 billion by 2034.

In 2025, the European market value stood at USD 2.83 billion.

The market is expected to exhibit a CAGR of 11.17% during the forecast period.

The Above 1,000 segment is expected to hold the highest CAGR over the forecast period.

The growing IMO Regulatory Pressure for Decarbonisation Drives the Market Growth.

BAE Systems, Oshkosh Defense, General Dynamics, Leonardo S.p.A., Krauss-Maffei Wegmann, Textron, QinetiQ Group, Nexter Group, General Motors Defense, and so on.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 430

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us