Contrast Media Injectors Market Size, Share & Industry Analysis, By Product (Injector Systems {CT Injector Systems, MRI Injector Systems, Cardiovascular/Angiography Injector Systems, and Others} and Consumables {Tubing, Syringe, and Others}), By Type (Single Head Injectors, Dual-Head Injectors, and Syringeless Injectors), By Application (Radiology, Interventional Cardiology, and Interventional Radiology), By End-user (Hospitals and ASCs, Diagnostic Centers, and Others), and Regional Forecast, 2026-2034

Contrast Media Injectors Market Size and Future Outlook

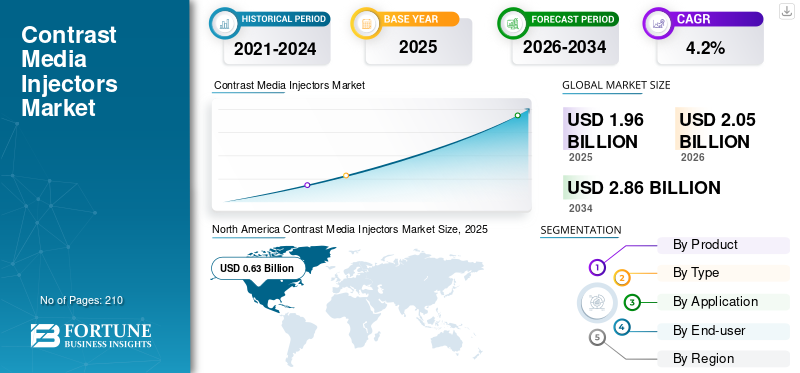

The global contrast media injectors market size was valued at USD 1.96 billion in 2025. The market is projected to grow from USD 2.05 billion in 2026 to USD 2.86 billion by 2034, exhibiting a CAGR of 4.2% during the forecast period. North America dominated the contrast media injectors market with a market share of 32.14% in 2025.

Contrast media injectors are powered delivery systems that administer contrast and saline during CT, MRI, and angiography procedures to achieve consistent timing, flow rates, and image quality. The market is expanding as the imaging demand continues to rise, while radiology teams are under pressure to perform more scans with fewer staff. Across OECD (Organisation for Economic Cooperation and Development) countries, CT and MRI use remains high and continues to be tracked as a core diagnostic-technology indicator. At the same time, vendors are refreshing their portfolios to focus on throughput, ease of setup, and safety features.

Furthermore, Bayer, Guerbet, Bracco Imaging, and GE HealthCare held the largest market share, driven by growing investments and tactical initiatives, such as new product launches and partnerships.

Download Free sample to learn more about this report.

CONTRAST MEDIA INJECTORS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.96 Billion

- 2026 Market Size: USD 2.05 Billion

- 2034 Forecast Market Size: USD 2.86 Billion

- CAGR: 4.2% from 2026–2034

- North America dominated the contrast media injectors market with a 32.14% share in 2025.

- The dual-head injectors segment is projected to hold 66.3% of the market in 2026.

- The radiology segment is expected to account for 79.7% of the market in 2026.

North America

North America reached USD 0.63 billion in 2025, accounting for 32.14% of global market revenue.

Asia Pacific

Asia Pacific is projected to reach USD 0.53 billion by 2026, ranking as the third-largest regional market.

Europe

Europe is projected to reach USD 0.60 billion by 2026, growing at a CAGR of 3.2%.

U.S.

The market is projected to reach USD 0.60 billion by 2026, accounting for 29.2% of global revenue.

Japan

The market is projected to reach USD 0.09 billion by 2026, representing 4.4% of global revenue.

Read More

CONTRAST MEDIA INJECTORS MARKET TRENDS

Syringeless Designs, Multi-Patient Systems, and Sustainability Features to Boost the Market

A significant trend is the move toward designs that streamline setup, reduce waste, and maintain safety and consistency. Syringeless and rapid-exchange concepts are gaining traction as they can mitigate refilling steps and support more continuous operation in busy MRI suites.

- In December 2024, Bracco and Ulrich Medical announced FDA 510(k) clearance for the Bracco-branded Max 3 syringeless MRI injector. This highlights direct injection from original contrast vials and a cassette-based approach intended to improve workflow and reduce plastic burden, an explicit nod to sustainability priorities in radiology operations.

In CT, multi-patient and high-throughput capabilities remain a focus. Bayer noted that its Centargo CT injector had already been launched broadly internationally and was being introduced to U.S. radiology departments, framing it as a system designed to automate tasks and support high-volume settings. Furthermore, hardware also features connectivity by default, where injectors are designed to fit within a more connected ecosystem, including traceability, cybersecurity posture, and interoperability. As these trends converge, hospitals increasingly evaluate injectors on pressure ratings and reliability, total workflow impact, turnover time, documentation, and how cleanly the injector fits into standardized protocols across multiple scanners and sites.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Imaging Volumes and Chronic Disease Prevalence to Push Scan Demand

The strongest demand driver is the steady rise in contrast-enhanced imaging tied to chronic disease and acute care pathways. Cardiovascular disease remains the world’s leading cause of death.

- For instance, as per an update in July 2025, the WHO reported an estimated 19.8 million CVD deaths in 2022 and these patients frequently undergo CT angiography, cardiac CT, and interventional procedures where injector performance and dose control matter.

The rising cancer prevalence is another major driver, propelling contrast media injectors market growth. IARC’s Global Cancer Observatory update highlighted the growing global cancer burden, supporting sustained use of contrast CT/MRI for diagnosis, staging, and therapy monitoring. On the supply side, OEM roadmaps align with this demand. At the system level, OECD continues to track CT/MRI examination rates and diagnostic-technology capacity, reflecting the continued centrality of imaging in modern care pathways. As procedure volumes grow, recurring consumables pull-through increases alongside injector replacements, making demand resilient even when capital budgets tighten.

MARKET RESTRAINTS

Contrast Safety Concerns and Protocol Restrictions to Limit Product Utilization

Even when imaging demand is strong, it does not imply a corresponding usage of contrast. Clinical risk management can restrain market growth, especially in higher-risk patients. A key limiter is that renal risk and CKD patients are more likely to trigger conservative contrast protocols, additional screening, or alternative imaging. Safety communications and labeling updates also influence practice. For MRI contrast agents, the FDA required class warnings and other safety measures for gadolinium-based contrast agents due to retention in the body, which continues to shape hospital policies, product selection, and informed-consent workflows. For iodinated agents, U.S. product labeling includes warnings on contrast-induced acute kidney injury and other precautions, reinforcing the need for monitoring and protocol compliance.

These clinical safeguards can reduce the addressable volume of contrast-enhanced studies in certain cohorts, add administrative steps, and increase time per patient. In practice, that can delay injector upgrades, shift purchasing toward lower-cost consumables, or push sites to standardize protocols to reduce variability and temper short-term growth even as long-term imaging demand rises.

MARKET OPPORTUNITIES

Connected and Automated Injector Ecosystems that Reduce Burden on Busy Departments to Create Significant Growth Opportunities

A significant opportunity lies in shifting from standalone injector hardware to connected workflow ecosystems that reduce manual steps, improve traceability, and simplify protocol execution. Radiology departments increasingly want injectors that integrate with broader digital infrastructure, including dose documentation, interoperability, and cybersecurity controls, as these features directly affect throughput and compliance.

This matters as staffing constraints are a practical limit on imaging growth. RSNA programming has pointed to access and workforce pressures, particularly in resource-constrained settings, making automation and simplification valuable for maintaining capacity. The commercial advantage is dual. Hospitals and imaging networks can standardize injector fleets to reduce training time and errors and OEMs can attach higher-value software/connectivity modules and recurring disposables. As health systems expand outpatient imaging, injector vendors that offer fast changeover, strong traceability, and reduced contamination risk are well-positioned to win both new installs and replacements.

MARKET CHALLENGES

Capital Budget Pressure, Standardization Complexity, and Cybersecurity Expectations to Challenge Market Growth

Despite strong demand fundamentals, injector vendors face practical adoption hurdles. Capital budgets are often cyclical and tender-driven, creating intermittent purchasing patterns even when procedure volumes are stable. Standardization is another challenge. Large health systems may run mixed fleets across CT, MRI, and angio, and harmonizing disposables, connectors, and protocols across sites can be difficult, especially when safety teams demand strict traceability.

Connectivity adds value, but it also raises expectations around cybersecurity, data governance, and interoperability testing, which can slow procurement and extend validation timelines. Furthermore, workforce constraints compound these issues. RSNA has highlighted access challenges and workforce pressure in radiology settings, and when staffing is tight, hospitals may defer changeovers that require training or workflow redesign. For manufacturers, the challenge is balancing innovation, such as automation, syringeless, and connectivity, with compatibility, ease of adoption, and cost, while keeping consumable supply reliable and compliant across regions.

Segmentation Analysis

By Product

Wide Adoption of Consumables in Several Imaging Procedures to Drive the Segment Growth

Based on product, the market is segmented into injector systems and consumables. Injector systems are further sub-segmented into CT injector systems, MRI injector systems, cardiovascular/angiography injector systems, and others. Similarly, the consumables segment is sub-segmented into tubing, syringe, and others.

To know how our report can help streamline your business, Speak to Analyst

The consumables segment holds the largest share as they are used repeatedly with every contrast-enhanced procedure, creating predictable “pull-through” demand that scales with imaging volumes. As CT and MRI utilization remains high across many developed systems, each incremental scan results in additional tubing sets, syringes/cassettes, and related disposables.

Additionally, the injector systems segment is projected to grow at a CAGR of 2.9% during the forecast period.

By Type

Dual-Head Injectors Segment Dominates due to Standard Protocols Support

By type, the market is classified into single head injectors, dual-head injectors, and syringeless injectors.

The dual-head injectors segment leads the global contrast media injectors market share as they support standard protocols that require both contrast and saline without manual workarounds. This improves bolus shaping, consistency, and workflow efficiency in high-throughput radiology environments. Dual-head systems also standardize protocols across scanners and technologist teams, which matters when departments are managing staffing constraints and want fewer steps per patient. Moreover, the segment is projected to hold a share of 66.3% in 2026.

Additionally, the syringeless injectors segment is estimated to grow at a CAGR of 15.9% during the forecast period.

By Application

Wide Application of Contrast-enhanced Procedures to Boost the Radiology Segment Growth

By application, the market is classified into radiology, interventional cardiology, and interventional radiology.

The radiology segment dominates as the largest volume of contrast-enhanced procedures occurs in diagnostic CT and MRI, which are used across oncology, cardiovascular, and emergency pathways. Further, radiology departments generate the highest recurring demand for injectors and consumables, particularly in large hospitals and outpatient imaging networks that run high patient throughput. Moreover, the segment is projected to hold a 79.7% share in 2026.

Additionally, the interventional radiology segment is estimated to grow at a CAGR of 6.9% during the forecast period.

By End-user

Advanced Healthcare Infrastructure to Impel Hospitals & ASCs Segment Growth

On the basis of end-user, the market is classified into hospitals & ASCs, diagnostic centers, and others.

The hospitals & ASCs segment accounts for the largest share owing to the broadest mix of CT, MRI, and angiography capabilities and help manage both emergency and complex chronic disease workloads. High-acuity pathways such as stroke, trauma, and cardiac events, among others, and oncology imaging sustain consistent use of contrast-enhanced studies, supporting steady consumable consumption. Additionally, hospitals are often early adopters of advanced injector features, such as automation, traceability, and connectivity, as these capabilities help manage compliance and throughput at scale. Furthermore, the segment is set to hold a share of 75.8% in 2026.

In addition, the diagnostic centers segment is projected to grow at a CAGR of 6.3% during the forecast period.

Contrast Media Injectors Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Contrast Media Injectors Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, accounting for a valuation of USD 0.60 billion. The region also dominated in 2025, reaching a value of USD 0.63 billion. The market growth in North America is propelled by the high utilization of CT and MRI and in the large installed base of imaging infrastructure, which keeps injector utilization and consumables pull-through consistently strong. OECD health-system benchmarking continues to show that diagnostic imaging remains a core pillar of care delivery, supporting steady demand for contrast-enhanced protocols that rely on injector performance and the repeated use of consumables. In addition, radiology departments are actively prioritizing workflow efficiency and automation as they manage high scan volumes and staffing pressure.

U.S. Contrast Media Injectors Market

In 2026, the U.S. market is estimated to touch a value of USD 0.60 billion, capturing 29.2% of the global revenue.

Europe

The Europe market is expected to depict a CAGR of 3.2% over the forecast period, the second-highest globally, and is set to reach USD 0.60 billion by 2026. The regional market growth is driven more by replacement cycles, standardization initiatives, and incremental upgrades than by first-time adoption. Many provider networks use procurement frameworks and fleet harmonization to reduce training complexity and variability across sites, which favors established injector platforms with strong protocol support and traceability. Europe also benefits from ongoing, high baseline diagnostic imaging activity, and OECD reporting continues to track CT/MRI utilization and capacity as key system indicators, underscoring the role of imaging as routine care infrastructure rather than discretionary spend.

U.K. Contrast Media Injectors Market

The U.K. market is projected to reach USD 0.09 billion by 2026, accounting for 4.4% of the global market revenue.

Germany Contrast Media Injectors Market

The Germany market is slated to reach about USD 14.1 billion by 2026, representing roughly 5.1% of global revenue.

Asia Pacific

In 2026, the Asia Pacific market is predicted to be valued at USD 0.53 billion, ranking as the third-largest globally. The region is growing at the fastest pace as imaging capacity is expanding across both public and private settings, increasing the number of sites running contrast-enhanced CT and MRI and the installed base of injector systems. As capacity expands, procedure volumes rise, and the market becomes increasingly consumables-driven given that every incremental contrast scan adds recurring demand for tubing sets, syringes/cassettes, and related disposables.

Japan Contrast Media Injectors Market

The Japan market is projected to generate approximately USD 0.09 billion in revenue by 2026, contributing nearly 4.4% of the global market.

China Contrast Media Injectors Market

The China market is forecast to reach approximately USD 0.18 billion by 2026, contributing about 8.8% of global revenues.

India Contrast Media Injectors Market

The India market is forecast to account for approximately USD 0.07 billion by 2026, corresponding to about 3.2% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa markets are anticipated to witness moderate growth, with Latin America expected to reach around USD 0.15 billion by 2026. The market growth in Latin America is driven by a combination of improving access to imaging, the expansion of private diagnostic chains, and tender-driven purchasing in public systems, which makes the market more cyclical for capital equipment but steadier for consumables.

In the Middle East and Africa, the market growth is closely linked to the build-out of healthcare infrastructure. New hospitals, specialty centers, and diagnostic hubs increase imaging capacity and create first-time demand for injector systems, followed by a growing annuity-like stream of consumables as utilization rises.

GCC Contrast Media Injectors Market

By 2026, the GCC market is expected to generate approximately USD 0.03 billion, accounting for nearly 1.5% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Emphasize Product Innovation to Consolidate their Foothold in the Market

The contrast media injectors market is moderately concentrated. A handful of global brands dominate, holding high-value hospital accounts. Once a hospital standardizes on a platform, it tends to stay with the same vendor due to familiarity with the protocol, service coverage, and most importantly, proprietary consumables such as patient sets, tubing, and syringes/cassettes. Key players such as Bayer, Guerbet, Bracco Imaging, and GE HealthCare held the largest market share in 2025.

Moreover, other key players, such as Ulrich Medical, Nemoto Kyorindo, MEDTRON AG, and Siemens Healthineers, compete through ongoing technologically advanced developments. The growing demand for improved healthcare infrastructure and efforts to improve therapy outcomes are additional factors influencing market competition.

LIST OF KEY CONTRAST MEDIA INJECTORS COMPANIES PROFILED

- Bayer (Germany)

- Guerbet (France)

- Bracco Imaging (Italy)

- GE HealthCare (U.S.)

- Ulrich Medical (Germany)

- Nemoto Kyorindo (Japan)

- MEDTRON AG (Germany)

- Siemens Healthineers (Germany)

- Shenzhen Seacrown Electromechanical (China)

- Antmed (China)

KEY INDUSTRY DEVELOPMENTS

- December 2025: MEDTRON launched new CT and MRI disposables sets for 24-hour multi-use, supporting high-throughput injector operations.

- December 2025: Bayer secured 510(k) clearance from the U.S. FDA for its MEDRAD Centargo multi-patient CT injector. The clearance has been granted for expanding the adoption of compatible contrast agent presentations for including single-dose vials along with Imaging Bulk Package (IBP) presentations that were previously cleared for Optiray (ioversol), Ultravist (iopromide), Omnipaque (iohexol), and Isovue (iopamidol).

- November 2025: Bracco Diagnostics Inc., the U.S. subsidiary of Bracco Imaging S.p.A., announced that the U.S. FDA expanded the indication for the Bracco-branded Max 3 Rapid Exchange and Syringeless Injector for use in magnetic resonance imaging (MRI) procedures.

- May 2025: MEDTRON AG expanded its portfolio with two new reusable syringe models, the ELS 200 ml Syringe MU (314626-100) and the Day Safe Syringe 200 (312426-100).

- November 2024: Bayer announced 510(k) clearance from the U.S. Food and Drug Administration (FDA) for its MEDRAD Centargo CT Injection System. This innovative multi-patient injector improves workflow efficiency through design features that integrate with Bayer’s product portfolio, especially in high-volume CT suites.

- November 2023: Bracco, a global leader in diagnostic imaging, and Ulrich GmbH & Co. KG, a renowned German medical device manufacturer specialized in spinal implants and contrast media injectors, announced a new long-term partnership. The deal would bring a Bracco-branded, state-of-the-art MR injector to the U.S. under an exclusive private label arrangement.

- May 2023: Guerbet, a global leader in contrast media and solutions for medical imaging, and MEDTRON AG, one of Europe’s leading manufacturers of state-of-the-art contrast media injectors, announced a collaboration for the German and Austrian markets.

REPORT COVERAGE

The market report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Type, Application, End-user, and Region |

| By Product |

|

| By Type |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.96 billion in 2025 and is projected to reach USD 2.86 billion by 2034.

In 2025, the North America market value stood at USD 0.63 billion.

The market is expected to exhibit a CAGR of 4.2% during the forecast period of 2026-2034.

The consumables segment leads the market by product.

The key factors driving the market are the rising imaging volumes and chronic disease prevalence.

Bayer, Guerbet, Bracco Imaging, and GE HealthCare are some of the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us