Syringes Market Size, Share & Industry Analysis By Product Type (Conventional Syringes and Safety Syringes), By Volume Capacity (Up to 1 mL, 1 mL – 5 mL, 6 mL – 10 mL, 11 mL – 20 mL, and Above 20 mL), By Material (Plastic Syringes and Glass Syringes), By Usage (Disposable Syringes and Reusable Syringes), By End User (Hospitals & ASCs, Clinics, Clinical Laboratories, Pharmaceutical & Biotechnology Companies, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

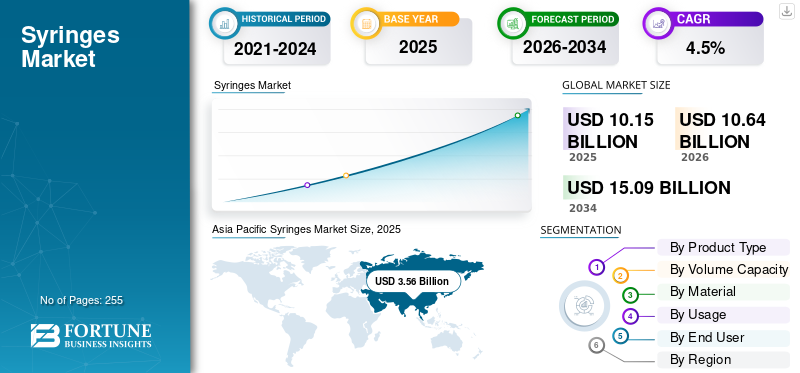

The global syringes market size was valued at USD 10.15 billion in 2025. The market is projected to grow from USD 10.64 billion in 2026 to USD 15.09 billion by 2034, exhibiting a CAGR of 4.5% during the forecast period. Asia Pacific dominated the syringes market with a market share of 35.07% in 2025.

A syringe is a simple pump with a plunger in a barrel used to inject or withdraw fluids, commonly featuring a needle for medical injections, blood draws, or IV therapy. The increasing prevalence of chronic conditions, including neurological conditions, cardiovascular conditions, and others, is resulting in a growing patient population. The rising patient population increases the demand for syringes for drug administration and blood withdrawal for diagnostic purposes, thereby contributing to the growth of the market.

- For instance, according to the 2024 data published by the Centers for Disease Control & Prevention (CDC), an estimated 129 million individuals in the U.S. have at least one major chronic disease (e.g., hypertension, obesity, heart disease, diabetes, cancer) as defined by the U.S. Department of Health and Human Services.

The increasing preference for technologically advanced drug delivery products contributes to the growing demand for these products in healthcare settings. This, coupled with the increasing focus on acquisitions and mergers among key players, is driving the focus of major companies, including Becton, Dickinson and Company (BD), Terumo Corporation, Nipro Corporation, Gerresheimer AG, and Cardinal Health, and is expected to support the growth of the global market.

Download Free sample to learn more about this report.

SYRINGES MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 10.15 Billion

- 2026 Market Size: USD 10.64 Billion

- 2034 Forecast Market Size: USD 15.09 Billion

- CAGR: 4.5% from 2026–2034

- Asia Pacific dominated the syringes market with a 35.07% share in 2025.

- The safety syringes segment is projected to grow at a CAGR of 8.6% during the forecast period.

- The up to 1 mL segment is expected to expand at a CAGR of 6.2% during the forecast period.

North America

North America is estimated to reach USD 2.51 billion in 2026, supported by strong healthcare infrastructure and widespread adoption of advanced injection devices.

Europe

Europe is expected to witness steady growth, supported by aging demographics, universal healthcare systems, and rising demand for injectable therapies.

Asia Pacific

The Asia Pacific syringes market held the dominant share in 2025, valued at USD 3.56 billion, and maintained its leading position in 2026, with a value of USD 3.79 billion.

U.S.

The U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 2.20 billion in 2026.

Japan

The Japan market, in 2026, is estimated to reach around USD 0.54 billion, accounting for roughly 5.1% of global syringes revenues.

Read More

Syringes Market Trends

Preferential Shift toward Plastic and Safety Syringes to Boost Product Demand

One of the most prominent trends in the market is the global dominance of disposable plastic syringes, which continue to replace glass and reusable alternatives. Plastic syringes offer advantages such as lower cost, reduced risk of contamination, and compatibility with mass manufacturing, making them the preferred choice in most applications. By 2024, plastic syringes will account for the vast majority of global syringe consumption, a trend expected to continue strengthening further by 2034.

Another key trend is the steady rise in the adoption of safety syringes, even beyond regulatory mandates. Hospitals and clinics are increasingly prioritizing occupational safety, particularly in regions with high healthcare worker density. This has accelerated the uptake of safety-engineered designs in both public and private healthcare facilities. Additionally, there is a growing interest in dose-optimized and low-dead-space syringes, particularly in vaccination programs where minimizing waste is crucial.

Regionally, manufacturing capacity is shifting toward the Asia Pacific, particularly China and India, which have emerged as major global suppliers of empty hypodermic syringes. These countries benefit from cost-efficient production, expanding domestic demand, and strong export capabilities. Meanwhile, developed markets are focusing more on product differentiation, compliance, and premium safety features, rather than volume expansion alone.

Market Dynamics

Market Drivers

Rise in Injection-Based Therapies and Immunization Programs to Drive Market Growth

The global syringes market is primarily driven by the steady rise in injection-based therapies and immunization programs worldwide. According to public health literature, an estimated 15–16 billion injections are administered each year globally, underscoring the essential role of syringes in routine healthcare delivery. The growing prevalence of chronic diseases such as diabetes, cancer, and autoimmune disorders continues to increase the demand for therapeutic injections, particularly in outpatient and homecare settings.

- For instance, the International Diabetes Federation estimates that over 530 million adults globally were living with diabetes in 2023, many of whom require regular injectable treatment.

Another major driver is the increasing emphasis on injection safety. Governments and healthcare authorities across developed markets have introduced policies mandating or strongly encouraging the use of safety-engineered syringes to reduce needle-stick injuries. The World Health Organization reports that unsafe injection practices historically contributed to millions of preventable infections annually, prompting the widespread adoption of single-use and safety syringes. Additionally, large-scale national immunization programs, particularly in the Asia Pacific, Africa, and Latin America, continue to generate sustained volume demand. Even after the peak of COVID-19 vaccination campaigns, routine childhood and adult immunization schedules remain a stable growth pillar for the market.

Market Restraints

Intense Price Pressure and Commoditization to Limit the Market Growth

Despite its essential nature, the syringes market faces several structural restraints, most notably intense price pressure and commoditization. In many regions, syringes are procured through government tenders and bulk purchasing programs, where price often outweighs brand differentiation. This is particularly evident in emerging economies, where public healthcare systems prioritize affordability, resulting in thin margins for manufacturers. Even in developed markets, hospital group purchasing organizations (GPOs) exert significant downward pressure on pricing.

Another key restraint is the environmental burden associated with single-use plastic syringes. With billions of disposable syringes used annually, healthcare waste management has become a growing concern. Improper disposal poses environmental risks and also raises public health issues in low-resource settings. While reusable syringes exist, strict infection control standards have significantly limited their adoption. Additionally, regulatory compliance costs, including product registration, quality audits, and post-market surveillance, can be prohibitive for smaller manufacturers, particularly when entering highly regulated markets such as the U.S. and Europe.

Supply chain volatility has also emerged as a restraint in recent years. Disruptions in the availability of medical-grade plastic resin, logistics bottlenecks, and geopolitical trade restrictions have exposed vulnerabilities in syringe manufacturing and distribution, resulting in delays in supply and instability in costs.

Market Opportunities

Increasing Investments to Upgrade Healthcare Infrastructure

The syringes market offers significant growth opportunities driven by healthcare expansion in emerging economies and product innovation. Countries across the Asia Pacific, the Middle East, and Africa are investing heavily in primary healthcare infrastructure, including rural clinics and vaccination centers. As healthcare access improves, per-capita injection rates rise, directly translating into higher syringe consumption. The gradual replacement of informal or unsafe injection practices with standardized disposable syringes further expands the addressable market.

A major opportunity lies in the continued transition from conventional to safety syringes. Although adoption is already high in North America and parts of Europe, the penetration remains relatively low in several emerging markets. As governments align more closely with WHO injection safety guidelines, the demand for auto-disable and retractable syringes is expected to increase. This shift improves patient and healthcare worker safety and also allows manufacturers to move toward higher-value product mixes.

Additionally, the expansion of biologics, biosimilars, and injectable specialty drugs presents new growth opportunities. Many of these therapies require precise dosing and frequent administration, which supports the demand for advanced syringe designs and smaller volume capacities. The expansion of homecare and self-administration, particularly for insulin and chronic therapies, also creates room for user-friendly syringe formats tailored to non-clinical settings.

Market Challenges

Strong Medical Waste Management Guidelines to Limit the Market Growth

The syringes market faces persistent challenges related to balancing affordability, safety, and sustainability. While safety syringes reduce occupational hazards, their higher cost can be a barrier in low- and middle-income countries, where healthcare budgets are constrained. Bridging this gap without compromising safety remains a key challenge for policymakers and manufacturers alike.

Another challenge is managing medical waste, particularly in regions with limited disposal infrastructure. The improper handling of used syringes continues to pose risks of infection transmission and environmental contamination. Although international organizations promote safe disposal practices, the implementation remains uneven across geographies. From a manufacturing perspective, ensuring consistent quality at high volumes is becoming increasingly complex, especially as the demand fluctuates in response to public health priorities.

The market also faces limited product differentiation, making it difficult for companies to sustain long-term competitive advantages. As syringes are often viewed as standardized consumables, their innovation cycles are slower compared to those of other medical devices. Ultimately, regulatory fragmentation across regions complicates global expansion strategies, necessitating manufacturers to navigate diverse standards, approval timelines, and compliance costs.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product Type

Cost Advantage and Widespread Availability to Drive Conventional Syringes Segment’s Dominance

Based on product type, the market is classified into conventional syringes and safety syringes.

To know how our report can help streamline your business, Speak to Analyst

The conventional syringes segment held the largest global syringes market share in 2025. The dominance of the segment is primarily due to their cost advantage, widespread availability, and entrenched usage, particularly in emerging and price-sensitive markets. While safety syringes are gaining traction, conventional syringes remain the default choice in government tenders, routine therapeutic injections, and public hospitals, where budget constraints outweigh safety-driven upgrades.

The safety syringes segment is expected to grow at a CAGR of 8.6% over the forecast period.

By Volume Capacity

Rising Adoption in Outpatient Procedures and Therapeutic Injections Led to the 1mL – 5mL Segment’s Dominance

Based on volume capacity, the market is segmented into up to 1 mL, 1 mL – 5 mL, 6 mL – 10 mL, 11 mL – 20 mL, and above 20 mL.

The 1 mL – 5 mL segment dominated the global market with a share of 35.3% in 2025. This is due to its broad applicability across therapeutic injections, vaccinations, and outpatient procedures. Most commonly administered injectable drugs, including antibiotics, analgesics, vaccines, and insulin, fall within this dosing range. Healthcare providers favor this capacity for its dose accuracy, ease of handling, and reduced drug wastage, making it the most versatile and frequently used syringe size across all care settings.

The up to 1 mL segment is set to flourish with a growth rate of 6.2% during the forecast period.

By Material

Increasing Preference for Single-Use Medical Devices Led to the Dominance of the Plastic Syringes Segment

Based on material, the market is segmented into plastic syringes and glass syringes.

The plastic syringes segment dominated the global market and held a share of 89.1% in 2025. Plastic syringes account for the majority share as they offer a combination of low cost, disposability, and infection control benefits. Unlike glass syringes, plastic variants are lightweight, shatter-resistant, and suitable for high-speed mass production. The regulatory emphasis on single-use medical devices and growing concerns around cross-contamination have further reinforced plastic syringes as the industry standard across both developed and emerging markets.

Additionally, the glass syringes segment is projected to grow at a CAGR of -3.3% during the study period.

By Usage

Global Infection Prevention Protocols and Regulatory Mandates Led to the Dominance of the Disposable Syringes Segment

Based on usage, the market is segmented into disposable syringes and reusable syringes.

The disposable syringes segment dominated the global market and held a share of 92.1% in 2025. The segment led the market due to global infection prevention protocols and regulatory mandates discouraging reuse. Healthcare authorities and hospitals strongly prefer single-use syringes to minimize the risk of disease transmission and needle-stick injuries.

Additionally, the reusable syringes segment is projected to grow at a CAGR of -4.7% during the study period.

By End-user

Growing Number of Hospitals & ASCs Led to the Segment’s Dominance

Based on end-user, the market is segmented into hospitals & ASCs, clinics, clinical laboratories, pharmaceutical & biotechnology companies, and others.

The hospitals and ASCs segment dominated the market in 2025. The increasing prevalence of several chronic disorders, as well as the growing number of hospitals, are key factors contributing to the segment's growth in the market. Furthermore, the segment is set to hold a 58.9% share in 2026.

- For instance, according to 2025 data published by the American Hospital Association, there are about 6,093 hospitals in the U.S.

Additionally, the pharmaceutical & biotechnology companies segment is projected to grow at a CAGR of 7.8% during the study period.

Syringes Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Syringes Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific syringes market held the dominant share in 2025, valued at USD 3.56 billion, and maintained its leading position in 2026, with a value of USD 3.79 billion. Asia Pacific is the largest and most structurally dynamic growth engine for the market. The rapid expansion of population, urbanization, and expanding healthcare access across China, India, and Southeast Asia are significantly increasing per-capita injection volumes. Governments across the region are investing heavily in primary healthcare infrastructure, vaccination coverage, and disease screening programs, all of which rely heavily on disposable syringes.

Japan Syringes Market

The Japan market, in 2026, is estimated to reach around USD 0.54 billion, accounting for roughly 5.1% of global syringes revenues.

China Syringes Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 1.31 billion, representing roughly 12.3% of global syringes sales.

India Syringes Market

The India market, in 2026, is estimated to touch around USD 0.85 billion, accounting for roughly 8.0% of global syringes revenues.

North America

North America is estimated to reach USD 2.51 billion in 2026 and secure the position of the second-largest region in the market. The regional expansion is driven primarily by replacement demand, safety upgrades, and chronic disease management, rather than volume expansion. The region has one of the highest per-capita injection rates globally, supported by a large population of patients with diabetes, cancer, autoimmune disorders, and cardiovascular diseases that require regular injectable therapies.

U.S. Syringes Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 2.20 billion in 2026, accounting for roughly 20.7% of global syringes sales.

Europe

Europe is projected to record a growth rate of 3.0% in the coming years, which is the third highest among all regions, and reach a valuation of USD 2.27 billion by 2026. Aging demographics, universal healthcare coverage, and consistent public procurement volumes support Europe’s syringes market growth. Many European countries face a rising elderly population, leading to an increased use of injectable therapies for chronic and age-related conditions.

U.K. Syringes Market

The U.K. market, in 2025, reached USD 0.35 billion, representing approximately 3.4% of global syringes revenues.

Germany Syringes Market

Germany’s market reached approximately USD 0.44 million in 2025, equivalent to around 4.3% of global syringes sales.

Latin America and Middle East & Africa

Growth in Latin America and the Middle East & Africa is driven by gradual expansion of the healthcare system, improving immunization coverage, and rising rates of chronic disease diagnosis. Countries such as the UAE, Saudi Arabia, Brazil, and Mexico continue to enhance public healthcare access, with a focus on increasing the use of standardized disposable syringes in hospitals and clinics.

GCC Syringes Market

The GCC market is projected to reach approximately USD 0.28 billion by 2026, accounting for roughly 2.7% of global syringes revenues.

Competitive Landscape

Key Industry Players

Increasing Focus on Capacity Expansion by Prominent Companies to Support Their Dominance

The global syringes market is moderately consolidated, characterized by the presence of a few large multinational players alongside a wide base of regional and local manufacturers. Tier-1 companies such as Becton, Dickinson and Company (BD), Terumo Corporation, and Nipro Corporation command a significant share of the market due to their broad product portfolios, global manufacturing footprints, and strong relationships with hospitals and government procurement agencies. These players benefit from scale, regulatory expertise, and the ability to supply both conventional and safety-engineered syringes across multiple regions.

- For instance, in January 2025, BD (Becton, Dickinson and Company) announced additional investments in its U.S. manufacturing network for enhancing capacity for critical medical devices, including IV catheters, needles, and syringes, to meet the ongoing needs of the nation's healthcare system.

Other key players, including Gerresheimer AG, Cardinal Health, Smiths Medical, B. Braun Melsungen AG, and others, are also expanding in the market. This is primarily due to their increasing emphasis on R&D activities to develop advanced products and strengthen their market presence.

List of Key Syringes Companies Profiled

- Becton, Dickinson and Company (BD) (U.S.)

- Terumo Corporation (Japan)

- Nipro Corporation (Japan)

- Gerresheimer AG (Germany)

- Cardinal Health (U.S.)

- Smiths Medical (ICU Medical) (U.S.)

- Braun Melsungen AG (Germany)

- Hindustan Syringes & Medical Devices (HMD) (India)

- Weigao Group (China)

- Retractable Technologies (U.S.)

KEY INDUSTRY DEVELOPMENTS

- May 2024 - Sharps Technology, Inc. announced the signing of a 5-year, USD 200 million syringe Sales Agreement (SA) with Nephron Pharmaceuticals to complement the Company’s Asset Purchase Agreement (APA) to acquire the InjectEZ specialty syringe manufacturing assets in West Columbia, South Carolina.

- November 2023 - Gerresheimer AG celebrated the start of construction of the plant expansion at its facility in Querétaro, Mexico. The new 7,500 m² production building would enable Gerresheimer to increase its manufacturing capacity for syringes for the North American market by several hundred million “ready-to-fill” (RTF) syringes annually.

- October 2022 - Terumo Pharmaceutical Solutions (TPS), a division of Terumo Corporation (TSE: 4543) and a leading manufacturer of injection, primary container, and infusion therapy devices, announced its expansion of contract development and manufacturing services for parenteral drugs to global customers.

- January 2022 - ICU Medical Inc. announced that it completed its acquisition of Smiths Medical from Smiths Group plc. The Smiths Medical business encompasses syringes and ambulatory infusion devices, vascular access products, and vital care solutions.

- October 2021 - BD (Becton, Dickinson and Company) announced that it strengthened the U.S. government's access to safety injection devices through increased manufacturing capacity and domestic supply. The new syringe and needle manufacturing lines, which were completed on an accelerated timeline, represent the public-private partnership between BD and the Department of Health and Human Services' (HHS) Assistant Secretary for Preparedness and Response (ASPR).

REPORT COVERAGE

The market report provides a detailed global syringes market analysis and focuses on key aspects such as leading companies, product type, volume capacity, material, usage, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.5% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Volume Capacity, Material, Usage, End User, and Region |

|

By Product Type |

|

|

By Volume Capacity |

|

|

By Material |

|

|

By Usage |

|

|

By End User |

|

|

By Region |

North America (By Product Type, By Volume Capacity, By Material, By Usage, By End User, and by Country)

Europe (By Product Type, By Volume Capacity, By Material, By Usage, By End User, and by Country/Sub-region)

Asia Pacific (By Product Type, By Volume Capacity, By Material, By Usage, By End User, and by Country/Sub-region)

Latin America (By Product Type, By Volume Capacity, By Material, By Usage, By End User, and by Country/Sub-region)

Middle East & Africa (By Product Type, By Volume Capacity, By Material, By Usage, By End User, and by Country/Sub-region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 10.15 billion in 2025 and is projected to reach USD 15.09 billion by 2034.

In 2025, the Asia Pacific regional market value stood at USD 3.56 billion.

The market will exhibit steady growth at a CAGR of 4.5% over the forecast period (2026-2034).

By product type, the conventional syringes segment was the leading segment in this market in 2025.

The rise in injection-based therapies and immunization programs is one of the major factors driving the market's growth.

Becton, Dickinson and Company (BD), Terumo Corporation, Nipro Corporation, Gerresheimer AG, and Cardinal Health are the major players in the global market.

Asia Pacific dominated the market share in 2025.

The combination of low cost, disposability, infection control benefits, and new product approvals, among other factors, is expected to boost the adoption of these products worldwide.

- 2021-2034

- 2025

- 2021-2024

- 255

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us