Blood Transfusion Diagnostics Market Size, Share & Industry Analysis, By Product (Instruments and Reagents & Kits), By Application (Blood Screening and Blood Group Typing), By End-user (Hospital-based Laboratories and Independent Laboratories & Blood Banks), and Regional Forecast, 2026-2034

Blood Transfusion Diagnostics Market Size

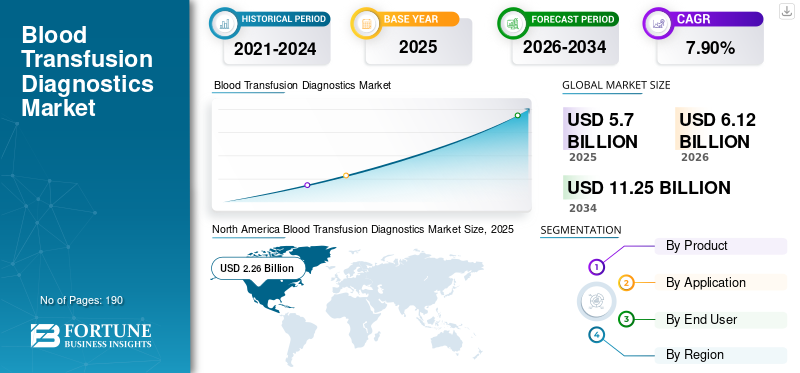

The global blood transfusion diagnostics market size was valued at USD 5.70 billion in 2025. The market is projected to grow from USD 6.04 billion in 2026 to USD 8.98 billion by 2034, exhibiting a CAGR of 5.1% during the forecast period. North America dominated the blood transfusion diagnostics market with a market share of 34.91% in 2025.

Blood transfusion diagnostics refers to tests performed on blood and blood components before transfusion to patients. Each blood unit must be tested for blood typing and disease screening to prevent adverse reactions or the transmission of infections. It is a crucial part of transfusion therapy, providing critical information to healthcare professionals and confirming the compatibility of donor and recipient blood samples.

The market’s growth is mainly driven by rising demand for safe transfusions amid rising rates of chronic blood disorders and higher surgical volumes. Furthermore, technological advancements and regulatory pressures that enhance blood screening accuracy are also anticipated to augment growth.

Immucor, Inc., Grifols, S.A., and Ortho Clinical Diagnostics held the largest market share globally in 2025 due to their strong global footprints and broad portfolios.

Download Free sample to learn more about this report.

Blood Transfusion Diagnostics Market Key Takeaways

- 2025 Market Size: USD 5.70 billion

- 2026 Market Size: USD 6.04 billion

- 2034 Forecast Market Size: USD 8.98 billion

- CAGR: 5.1% from 2026–2034

- North America dominated the blood transfusion diagnostics market with a 34.91% share in 2025.

- The reagents & kits segment held the largest market share in 2025.

- The blood screening segment is expected to account for 67.4% of the market in 2026.

North America

North America the market reached USD 1.99 billion in 2025, driven by high blood donation rates, advanced healthcare infrastructure, and widespread adoption of blood screening.

Europe

Europe the market is projected to reach USD 1.83 billion in 2026, expanding at a 4.6% CAGR due to increasing adoption of CE-approved diagnostic assays.

Asia Pacific

Asia Pacific the market is expected to reach USD 1.49 billion in 2026, supported by growing blood donation awareness and rising prevalence of blood disorders.

U.S.

The market is projected to reach USD 1.92 billion in 2026, driven by a well-established blood transfusion system and strong donor participation.

Japan

The market is expected to generate USD 0.30 billion in 2026, supported by advanced diagnostic capabilities and increasing demand for safe blood transfusions.

Read More

BLOOD TRANSFUSION DIAGNOSTICS MARKET TRENDS

Shift toward Automated Molecular Platforms to Accelerate Market Growth

The introduction of advanced molecular platforms by key market players is driving a shift away from manual tests and instruments toward semi-automated and fully automated systems. These automated platforms have been pivotal in the rapid detection of Transfusion Transmissible Infections (TTIs) in blood samples and can precisely eliminate human error during transfusion.

Introducing new technologies, such as DG Gel technology for pretransfusion compatibility testing, enables laboratories and blood banks to optimize the workflow.

The launch of such advanced automated systems has been instrumental in fueling the adoption of blood transfusion diagnostics and is expected to drive market growth during the forecast period. The automation trend improves the speed and reliability of blood testing.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Demand for Blood and Blood Components to Boost Demand

The growing prevalence of blood-related disorders, such as hemophilia, cancer, thrombocytopenia, chronic kidney disease (CKD), and others has propelled the demand for blood products and complete blood transfusions. Patients diagnosed with these conditions often require periodic blood transfusions to manage their conditions. In addition, the increasing number of childbirths, surgeries, and trauma cases being performed globally is also contributing to the demand for blood transfusions.

- For instance, according to the data published by the Centers for Disease Control and Prevention (CDC) in May 2024, approximately 14.0% of U.S. adults, or 35.5 million individuals, have chronic kidney disease (CKD), affecting more than 1 in 7 people as of 2023.

Also, the increasing number of patients suffering from anemia, which requires red blood cell transfusion for its treatment, is anticipated to increase the demand for blood transfusion diagnostics.

- For instance, according to data from the Institute for Health Metrics and Evaluation in September 2023, nearly 2 billion people worldwide were affected by anemia.

This, along with the increasing awareness regarding blood safety from infectious diseases through several programs in developed and emerging countries, is resulting in high demand for blood screening tests and other diagnostic tools.

MARKET RESTRAINTS

High Cost of Instruments and Lack of Infrastructure May Restrict Growth in Emerging Countries

Increasing prevalence of chronic blood diseases and higher demand for blood products and transfusions are primary factors limiting market growth. Other factors include lack of spending on healthcare infrastructure and stringent government policies, especially in emerging countries, as compared to developed countries.

Blood transfusion testing requires specialized equipment and testing kits. The high cost of these instruments, lack of infrastructure, and storage facilities in emerging countries limit market growth. Additionally, the high cost associated with the tests, instruments, and reagents, coupled with the lack of skilled professionals to handle automated diagnostic solutions, is one of the factors limiting the blood transfusion diagnostics market growth.

MARKET OPPORTUNITIES

Expansion in Low- and Middle-Income Countries to Offer Lucrative Opportunities

Improving blood screening capacity in low- and middle-income countries presents significant opportunities, as testing coverage and quality systems lag behind those in high-income markets. Several organizations, such as the World Health Organization, state that all donated blood should be screened for HIV, hepatitis B, hepatitis C, and syphilis under quality-assured conditions. However, some countries cannot screen all donations for one or more required infections, and screening performed under basic quality procedures remains materially lower in lower-income settings.

This gap is expected to create room for suppliers of immunoassays, NAT platforms, blood grouping reagents, and workflow automation to support modernization programs in national blood services and hospital-based transfusion laboratories. Vendors that offer affordable analyzers, stable reagent supply, training, and service support can benefit most.

MARKET CHALLENGES

Residual Risk Despite Testing Advances May Pose a Significant Challenge to Market Expansion

Although there are significant advances in testing technology, the bacterial contamination of platelet components remains a leading infectious threat. Several reports by healthcare organizations such as the CDC, state that sepsis can still occur despite bacterial mitigation strategies, including cases involving pathogen-inactivated platelets or negative rapid detection results.

This places pressure on the manufacturers and laboratories to continue improving sensitivity, add additional testing layers, and refine screening algorithms, further increasing overall costs, and posing a major challenge to market growth.

Segmentation Analysis

By Product

Reagents & Kits Dominate the Global Market Due to Repeated Sales

To know how our report can help streamline your business, Speak to Analyst

Based on segment, the market is segmented into instruments and reagents & kits. The reagents & kits segment held the dominant blood transfusion diagnostics market share in 2025, owing to the recurring sales of these products, which are required for screening and blood group typing of both donor and recipient samples.

The instruments segment is expected to expand at a CAGR of 4.3% over the forecast period.

By Application

Blood Disease Screening to Hold a Dominant Position Due to Increasing Incidence Of Transfusion-Transmissible Infections (TTIs)

On the basis of application, the market is segmented into blood screening and blood group typing. The blood screening segment dominated the global market in 2025 due to the increasing incidence of transfusion-transmissible infections (TTIs) worldwide. The huge number of blood transfusions worldwide increases the demand for accurate and reliable blood screening tests. In addition, regulatory bodies mandate blood screening as a standard procedure to ensure patient safety. Furthermore, technological advancements, high sensitivity, and specific blood screening assays are driving the segment's growth.

Overall, the emphasis on blood safety and the need to prevent the spread of infections through blood transfusions have propelled the blood screening segment to dominate the global market. Moreover, the segment is projected to hold a 67.4% market share in 2026.

The blood group typing segment is expected to grow at a CAGR of 4.8% over the forecast period.

By End-user

Increasing Number of Stand-Alone Blood Banks & Laboratories to Boost Segment’s Growth

Based on end-user, the market includes hospital-based laboratories and independent laboratories & blood banks.

The independent laboratories & blood banks segment dominated the market in 2025. The dominance is attributed to a large number of blood transfusions performed in these settings, along with the increasing number of stand-alone blood banks & laboratories in developed as well as emerging countries. Moreover, the segment is projected to hold a 60.2% share in 2026.

The hospital-based laboratories segment is anticipated to register a 4.8% CAGR over the forecast period.

Blood Transfusion Diagnostics Market Regional Outlook

Geographically, the market is studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Blood Transfusion Diagnostics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest revenues in 2024, valued at USD 1.90 billion, and increased to USD 1.99 billion in 2025. The dominance is due to higher adoption of the blood transfusion process, increasing awareness among the general population about blood donations, and an established healthcare infrastructure in the region.

- For instance, according to data published by the Centers for Disease Control and Prevention (CDC) in September 2025, the U.S. observed about 7 million blood donors annually, supporting over 14 million units of blood transfused each year.

U.S Blood Transfusion Diagnostics Market

In 2026, the U.S. is anticipated to reach USD 1.92 billion, accounting for approximately 31.8% of the global market.

Europe

Europe is projected to record a 4.6% growth rate during the forecast period, the second-highest globally, reaching USD 1.83 billion in 2026. The market’s growth in Europe is fueled by the availability of CE-approved instrument assays for serological and Nucleic Acid Test (NAT) based methods in European countries.

U.K Blood Transfusion Diagnostics Market

The U.K. market is projected to reach USD 0.23 billion in 2026, representing approximately 3.9% of global revenues.

Germany Blood Transfusion Diagnostics Market

Germany's market is predicted to reach around USD 0.36 billion in 2026, representing around 5.9% of global revenue.

Asia Pacific

In 2026, Asia Pacific is projected to reach approximately USD 1.49 billion, making it the third-largest market globally. The rapid growth is due to ongoing initiatives by governments and NGOs in emerging countries to raise awareness of blood donation, coupled with the presence of large populations suffering from severe blood disorders.

Japan Blood Transfusion Diagnostics Market

Japan is projected to generate approximately USD 0.30 billion in revenue in 2026, representing nearly 4.9% of the global market.

China Blood Transfusion Diagnostics Market

China’s market is anticipated to achieve USD 0.47 billion in 2026, accounting for nearly 7.8% of global revenues.

India Blood Transfusion Diagnostics Market

India’s market is expected to reach approximately USD 0.09 billion by 2026, accounting for around 1.5% of global market revenue.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate growth, with Latin America estimated to acquire USD 0.34 billion in 2026. Latin America and the Middle East & Africa are expected to register a moderate CAGR during the forecast period, driven by a large untapped market.

GCC Blood Transfusion Diagnostics Market

In 2026, the GCC market is estimated to reach approximately USD 0.10 billion, representing around 1.7% of global revenues.

COMPETITIVE LANDSCAPE

Immucor, Inc., Grifols, S.A., and Ortho Clinical Diagnostics Maintain Dominance with R&D and Strong Distribution Networks

The global blood transfusion diagnostics market is fragmented, with players such as Immucor, Inc., Ortho Clinical Diagnostics, and Grifols, S.A., accounting for a major share in 2025. The robust product portfolio for blood transfusion diagnostics, a strong distribution network, and a constant focus on research and development are key factors behind these players' market position.

Grifols S.A., one of the leading players, boasts a strong diversified portfolio of test kits and products for blood transfusion diagnostics. Other players include Bio-Rad Laboratories, Inc., F. Hoffmann-La Roche Ltd., QUOTIENT, Abbott Laboratories, and Merck KGaA.

LIST OF BLOOD TRANSFUSION DIAGNOSTICS COMPANIES PROFILED

- Grifols, S.A. (Spain)

- Immucor, Inc. (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- QuidelOrtho Corporation (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- QUOTIENT (Switzerland)

- Merck KGaA (Germany)

- Abbott (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Tianlong launched a fully automated nucleic acid blood screening solution using its Aurora PANA X6 extractor and Gentier 96 PCR system on World AIDS Day 2025.

- October 2025: Grifols, S.A. began manufacturing DG Gel cards and reagent red blood cells (RRBCs) at its new 73,541-square-foot facility in San Diego, California, following FDA approvals. This expansion nearly doubles the campus size, boosting U.S. production of critical pre-transfusion testing tools alongside Procleix Panther reagents to meet growing demand.

- March 2025: Grifols, S.A. and Inpeco announced a strategic alliance to deliver fully automated "labs of the future" for transfusion medicine, integrating Grifols' diagnostic tools with Inpeco's robotics.

- November 2023: Grifols S.A. launched the Grifols sCD38 solution to facilitate pre-transfusion compatibility testing in multiple myeloma patients.

- October 2022: Hoffmann-La Roche Ltd and Apollo Hospitals launched the IPledgeRED campaign to promote voluntary blood donation among college students across eight Indian cities. The initiative highlights nucleic acid testing (NAT) for early detection of infections, ensuring safer transfusions for patients such as thalassemia cases, with support from TPAG and Thalassemia India.

- March 2022: Mylab Discovery Solutions Pvt. Ltd. launched the NATSpert ID tripleH detection kit, an RT-PCR test to detect infection in donated blood.

REPORT COVERAGE

The blood transfusion diagnostics market research report provides a detailed analysis of the market and focuses on key aspects, including leading companies, products, applications, and end-users. In addition, it offers insights into market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the advanced market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.1% from 2026-2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Product

|

|

By Application

|

|

|

By End-user

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 5.70 billion in 2025 and is projected to reach USD 8.98 billion by 2034.

In 2025, North America’s market value stood at USD 1.99 billion.

The market will exhibit steady growth at a CAGR of 5.1% during the forecast period (2026-2034).

Among the products, the reagents & kits segment will lead the market.

The rising prevalence of blood-related disorders and the increasing incidence of transfusion-transmissible infections (TTIs) are the key drivers of the market.

Immucor, Inc., Ortho Clinical Diagnostics, and Grifols, S.A., are the top players in the market.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us