In-vitro Diagnostics (IVD) Market Size, Share & Industry Analysis, By Product Type (Instruments and Reagents & Consumables), By Technique (Immunodiagnostics [Enzyme Linked Immunosorbent Assay, Fluorescence immunoassay, Rapid test], Clinical Chemistry, Molecular Diagnostics, Hematology), By Sample (Blood, Urine, Saliva, Tissue), By Setting (Laboratories, Point-of-Care), By Application (Infectious Diseases, Cardiology, Oncology, Gastroenterology, Allergy), By End-user (Clinical Laboratories, Hospitals, Physician’s Offices), & Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

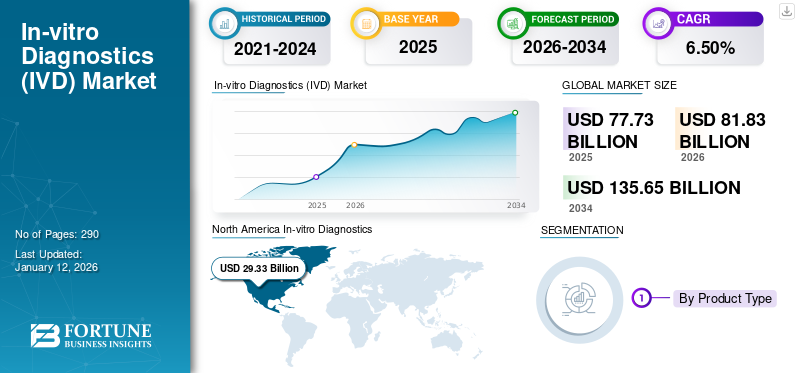

The global in-vitro diagnostics (IVD) market size was valued at USD 77.73 billion in 2025 and is expected to grow from USD 81.83 billion in 2026 to USD 135.65 billion by 2034, exhibiting a CAGR of 6.50% during the forecast period. North America dominated the in-vitro diagnostics market with a market share of 37.70% in 2025.

IVD are medical devices that perform diagnostic tests on biological samples, such as blood, urine, and tissues. These tests help detect and monitor infectious diseases, autoimmune diseases, and several other medical conditions and are also used to analyze drug therapy modifications from time to time. Furthermore, according to the British In-Vitro Diagnostic Association, these tests influence approximately 70% of clinical decisions.

The rising demand for and adoption of in-vitro diagnostic solutions has driven the market growth. This growth is further augmented by increasing investments by key players in research & development to innovate their products and explore new applications of IVD techniques.

- For instance, in May 2022, Cipla Inc. launched an advanced real-time RT-PCR kit to detect the SARS-CoV-2 pathogens in patients in 45 minutes.

There is an increasing focus of prominent market players, including F. Hoffmann-La Roche Ltd., Abbott, and Siemens Healthineers AG, among others, on the R&D activities to develop and introduce technologically advanced products and novel systems. This is expected to support the growth of the market globally.

The IVD market is poised for significant growth, driven by technological advancements, increasing disease prevalence, and a shift toward personalized medicine. While challenges, such as regulatory complexities and market competition, persist, the industry's trajectory remains positive, with ongoing innovations and strategic collaborations paving the way for a more efficient and accessible healthcare landscape.

Download Free sample to learn more about this report.

IN-VITRO DIAGNOSTICS (IVD) MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 77.73 Billion

- 2026 Market Size: USD 81.83 Billion

- 2034 Forecast Market Size: USD 135.65 Billion

- CAGR: 6.50% from 2026–2034

- North America dominated the in-vitro diagnostics market with a 37.70% share in 2025.

- The reagents & consumables segment is expected to account for 83.14% of the market in 2026.

- The molecular diagnostics segment is projected to hold a 30.54% share in 2026.

Europe

Europe held the second-largest market share, supported by advanced healthcare infrastructure and rising adoption of innovative diagnostic technologies.

Asia Pacific

Asia Pacific accounted for 23.00% of the global market in 2025 and is expected to witness strong growth driven by increasing healthcare spending and disease prevalence.

Latin America

Latin America is projected to experience steady growth due to rising healthcare expenditure and growing adoption of point-of-care diagnostic devices.

U.S.

The market is expected to reach USD 27.98 billion in 2026.

Japan

The in-vitro diagnostics market is projected to reach USD 4.32 billion in 2026.

Read More

Market Dynamics

Market Drivers

Increasing Prevalence of Chronic Diseases to Support Market Growth

The increasing prevalence of acute and chronic disorders, including cardiovascular, genetic, and neurological ailments, is resulting in the growing demand for in-vitro diagnostic products. The efficient use of IVD in the early diagnosis of such diseases allows doctors to work on appropriate treatments effectively.

- According to the 2022 statistics published by the U.S. Centers for Disease Control and Prevention (CDC), the cases of tuberculosis (TB) in the U.S. increased by 5% to 8,300 in 2022.

- According to a 2023 article published by the National Centers for Biotechnology Information (NCBI), the estimated global prevalence of chronic Hepatitis B virus (HBV) infection was around 3.2%, equivalent to 257 million cases.

Additionally, the growing geriatric population with increased susceptibility to health disorders, including liver, hypertension, cardiovascular disorders, and kidney diseases, among others, is expected to contribute to the market’s growth.

For instance, according to the 2023 statistics published by Time Magazine, about 297 million people are aged 60 and above in China. This is projected to boost the global IVD market growth in the coming years.

Increasing Funding and Government Support to Develop and Use IVD Devices Will Contribute to Market Growth

There is an increasing focus on raising awareness about government organizations, agencies, and associations encouraging the use of in-vitro diagnostic products by launching awareness initiatives, thereby driving the growth of the market. To clarify the priority of diseases based on burden and prevalence, the WHO released a model list of essential in-vitro diagnostics for primary healthcare and medical facilities with clinical laboratories. Both the categories are further sub-sectioned for general IVDs and specific diseases.

- In October 2023, the WHO released its 2023 Essential Diagnostics List (EDL), which is an evidence-based register of in vitro diagnostics (IVD) that supports countries to make national diagnostic choices.

Additionally, growing R&D initiatives to support funding are expected to contribute to product development that will further boost the market’s growth.

Thus, all the aforementioned factors, along with the growing number of IVD product launches, are expected to drive the growth of the market.

Market Restraints

High Cost of Instruments to Restrict Market Growth in Emerging Countries

There are numerous advantages associated with IVD products. However, the high cost of these in-vitro diagnostic instruments and their maintenance is likely to hinder their adoption. Additionally, these IVD products can be used only by skilled professionals, which also increases the maintenance cost of these products, subsequently limiting the market’s growth.

For instance, the cost of RT-PCR systems ranges from USD 15,000 to over USD 90,000. These cost factors have been responsible for the limited adoption of in-vitro diagnostic products in several emerging countries.

Market Opportunities

Gradual Shift of Preference Toward Adoption of Molecular Diagnostic Techniques

Molecular diagnostics is one of the most dynamic techniques in the in-vitro diagnostics industry, leading to advances in monitoring and revolutionizing healthcare across the world.

In the last decade, molecular diagnostics has become the most common practice for transplant and transfusion diagnostics and disease testing, and market players are currently focused on introducing new technologies.

- In March 2023, DiaSorin S.p.A. received the U.S. FDA approval for its Simplexa COVID-19 & Flu A/B Direct assay to strengthen its product portfolio globally.

Additionally, these techniques are comparatively more sensitive, allowing healthcare providers and laboratory physicians to detect infectious diseases even from a small number of samples. This has led to a shift of preference toward molecular diagnostic techniques in the global market.

Moreover, these techniques, which use nucleic acids and other cellular biomarkers, have facilitated medical advancements in diagnosing various diseases. They are also gaining huge popularity in the global market. The introduction of molecular biomarkers for cancer diagnosis has led to a substantial increase in diagnosed cases globally.

The advances in molecular diagnostic techniques, including next-gen sequencing, and the increasing prevalence of cancer and other chronic diseases, are anticipated to offer diverse opportunities to market players operating in the in-vitro diagnostics market.

The shift of preference from traditional diagnostic tools to advanced tools, including molecular diagnostics, is further anticipated to open new avenues for market players who can cater to these demands by introducing advanced tests.

Market Challenges

Unfavorable Reimbursement Policies for In-Vitro Diagnostics

The lack of adequate reimbursement policies for these tests, especially in emerging countries, such as Brazil, Mexico, and others, is a major factor responsible for the limited adoption of testing solutions. The reimbursement scenario for in-vitro diagnostic products has been unfavorable in many countries worldwide. Various regions and their changing reimbursement policies have impacted the growth of the in-vitro diagnostics market globally.

- For instance, according to a 2023 article published by the NCBI, the Rare Disease Reference Centers (RDRC) has USD 142 for coverage per patient every 3 months for any molecular testing. The coverage is insufficient for complex genetic testing, such as Exome Sequencing (ES), Whole Genome Sequencing (WGS), and others.

Thus, economic factors, such as inadequate reimbursement policies and others, are expected to impact healthcare spending, further affecting the adoption of advanced diagnostic technologies.

Other Prominent Challenges

- Regulatory Challenges - Navigating complex and varying regulations across different regions is expected to delay product development and market entry.

- Market Competition - The presence of numerous players in the IVD market intensifies competition, making differentiation and innovation crucial.

- Supply Chain Issues - Global supply chain disruptions are expected to impact the availability and cost of raw materials and finished products.

In-vitro Diagnostics Market Trends

Rising Penetration of Point-of-Care Testing Devices

The increasing prevalence of acute and chronic disorders is leading medical device companies to launch technologically advanced diagnostic devices. Due to the increasing prevalence of these diseases, medical device companies are focusing on the development of novel diagnostic devices. The benefits of point-of-care diagnostic tests, including lower costs, convenience & ease of testing, high efficiency, and others, are resulting in an increasing preference for these tests among the patient population. The increasing number of patients undergoing rapid diagnostics is leading to a growing demand for these tests and solutions.

Additionally, the increasing number of product launches by prominent market players and approvals by regulatory authorities will contribute to the growth of the market.

- For instance, in January 2023, Cipla Inc. launched Cippoint, a point-of-care testing device, to strengthen its product offerings.

- In June 2022, BD received the CE approval for BD Max combined COVID, Flu, and RSV panels. This approval strengthened its product portfolio for in-vitro diagnostics.

- In March 2021, Thermo Fisher Scientific launched ‘The Applied Biosystems QuantStudio 5 Dx Real-Time PCR System’, intended to analyze a large number of samples in a short duration. This resulted in increased efficiency in clinical laboratories and providing customizable output that can be used in molecular diagnostic testing.

Other Prominent Trends

- Technological Advancements - The integration of automation, artificial intelligence, and machine learning into IVD devices is enhancing diagnostic accuracy and efficiency.

- Personalized Medicine - IVD is being increasingly utilized to tailor medical treatments to individual genetic profiles, improving therapeutic outcomes.

- Regulatory Changes - Stricter regulatory frameworks are being implemented globally by the regulatory bodies to ensure the safety and efficacy of in-vitro diagnostic products.

Download Free sample to learn more about this report.

Impact of COVID-19

The COVID-19 pandemic positively impacted the market in 2020. A few segments witnessed a decline in their revenues in this year, while the molecular diagnostics segment observed a significant increase in its revenue.

- In 2020, Abbott generated a revenue of USD 4,376 million from its rapid diagnostics segment, witnessing a growth of around 113% as compared to the previous year.

The rising prevalence of COVID-19 globally impacted the demand for diagnostics tests. There was a marked decline in routine tests for chronic diseases, especially in clinical chemistry, hematology, and immunodiagnostic lab-based tests. However, the molecular diagnostics segment witnessed a positive impact due to increasing focus on the introduction of advanced test kits among key players. This, and the growing demand for point-of-care COVID-19 tests among patients, supported the market’s growth during the pandemic.

- For instance, according to statistics published in Science Direct, there was a 44% reduction in the diagnosis of invasive tumors during the first wave of the COVID-19 pandemic in 2020.

Segmentation Analysis

By Product Type

Reagents & Consumables Widely Adopted due to Advent of Advanced Products

Based on product type, the market is divided into instruments and reagents & consumables. The reagents & consumables segment will account for 83.14% market share in 2026 owing to an increase in the adoption of POC tests, self-testing kits, and several other products in in-vitro diagnosis. The growing number of R&D initiatives for diagnosing chronic conditions is one of the major factors supporting the demand for reagents & consumables. Moreover, the rising emphasis on early diagnosis globally further increases the number of patient admissions for routine tests, resulting in improved patient outcomes globally and supporting the segment’s growth.

- For instance, in February 2021, Thermo Fisher Scientific launched CE-IVD marked and applied Biosystems TaqPath COVID-19 HT kit to provide high-throughput solutions in the market.

On the other hand, the instruments segment is expected to record a considerable CAGR during the forecast period. The development and introduction of novel IVD instruments are expected to support the segment’s growth. For instance, in June 2023, BD launched a new instrument, the FACSDuet Premium Sample Preparation System, to strengthen its product portfolio for cellular diagnostics.

To know how our report can help streamline your business, Speak to Analyst

By Technique

Technological Advancements in Molecular Diagnostic Devices Drove their Demand

Based on technique, the market is divided into immunodiagnostics, clinical chemistry, molecular diagnostics, hematology, and others. The immunodiagnostics segment is further segmented into enzyme-linked immunosorbent assay (ELISA), fluorescence immunoassay (FIA), rapid test, and others. The clinical chemistry segment is further divided into electrolyte panels, basic and comprehensive metabolic panel, liver tests, renal tests, lipid panel, and others. Additionally, the molecular diagnostics segment is further divided into Polymerase Chain Reaction (PCR), in-situ hybridization, DNA sequencing & next-generation sequencing, and others.

The molecular diagnostics segment is expected to account for 30.54% of the market in 2026; it is also expected to record a considerable CAGR over the forecast period. The segment’s growth is owing to increasing launches and approvals of innovative molecular diagnostics-based tests by market players. These factors have been instrumental in the higher adoption of these tests for the diagnosis of various conditions.

- For instance, in December 2023, Seegene Inc. received the ISO45001 certification for PCR molecular diagnostics to strengthen its product portfolio globally.

The clinical chemistry segment will also record a considerable CAGR during the forecast period. The increasing prevalence of lifestyle and chronic disorders and growing initiatives by regional and national healthcare agencies toward routine diagnosis are leading to an increase in the number of patients undergoing tests in clinical laboratories globally. This, along with the increasing number of clinical laboratories in developing countries and realignment of reimbursement policies of developed and emerging countries, is driving the segment's growth.

By Sample

Increasing Number of Blood Tests for IVD Supported Segment’s Growth

On the basis of the sample, the market is segmented into blood, urine, saliva, tissue, and others.

The blood segment is projecteed to dominate the markt with a share of 33.24% in 2026. The benefits of blood tests, such as efficacy, improved diagnosis of the disease, and accurate monitoring of the condition, among others, are boosting the number of blood tests performed among patients.

- For instance, according to a 2018 article published by the National Center for Biotechnology Information (NCBI), about 2 billion blood tests are performed each year in the U.S.

The urine and saliva segments are also expected to record a considerable growth rate during the forecast period. The rising number of diagnostic tests performed with urine and saliva samples among the patient population is likely to support the segment’s growth in the market.

By Setting

Increasing Adoption of Advanced Instruments in Laboratories Fueled Growth of the Segment

Based on setting, the market is bifurcated into laboratories and point-of-care. The laboratories segment dominated the market in 2024 due to the growing demand for advanced instruments in laboratories and increasing investments by private and public sectors in laboratory infrastructure in emerging countries. Also, most of the complex and sensitive diagnostic tests are carried out in laboratories, requiring skilled lab staff, specialized equipment, and more time to run.

- For instance, in June 2023, BD launched a new robotic system that prepares samples for clinical diagnostics using flow cytometry to improve standardization and reproducibility in cellular diagnostics.

The point-of-care segment is also expected to record a substantial CAGR during the forecast period. Increasing demand for COVID-19 point-of-care tests that provide rapid results is one of the major factors contributing to the growth of the segment. This, along with the increasing number of acquisitions and mergers among the major players, is supporting the growth of the segment.

- For instance, in March 2021, BD announced that the U.S. FDA granted Emergency Use Authorization (EUA) for a new rapid antigen test that can detect SARS-CoV-2, influenza A, and influenza B in a single test.

Thus, growing product launches are expected to boost the growth of POC diagnostics. Additionally, point-of-care testing does not require highly skilled laboratory personnel or equipment. Therefore, it can be deployed in many different settings and at a large scale.

By Application

In-vitro Diagnostics Devices Found Robust Usage in Treatment of Infectious Diseases Due to Rising Prevalence

Based on application, the market is divided into infectious diseases, cardiology, oncology, gastroenterology, allergy, autoimmunity, prenatal screening, and others. The infectious disease segment will account for 32.34% market share in 2026 owing to the growing prevalence of infectious illnesses among the patient population globally.

- For instance, according to the 2023 statistics published by the World Health Organization (WHO), it was estimated that about 10.8 million people are suffering from tuberculosis globally.

The oncology segment is also expected to record a considerable growth rate during the forecast period. The segment’s growth is due to the rising prevalence of cancer, resulting in a growing diagnosis rate among the patient population. This, along with the growing number of key players focusing on R&D activities to launch new products, is likely to support the growth of the segment in the market.

- For instance, according to the 2022 data published by Macmillan Cancer Support, approximately 3 million people have cancer in the U.K., which is expected to rise to 3.5 million by 2025 and 5.3 million by 2050. Thus, the introduction of new lab-based IVD tests for biomarker identification in oncology and new POC tests for cancer screening are pivotal in the higher demand for and adoption of these tests in Europe.

By End-user

Higher Test Volume Boosted Adoption of IVDs at Clinical Laboratories

Based on end-user, the market is segmented into clinical laboratories, hospitals, physician's offices, and others. The clinical laboratories segment dominated the market in 2024 due to the increasing number of these laboratories, further supporting the growing number of diagnostic procedures among patients. Additionally, the outsourcing of clinical diagnostic services by public hospitals to independent clinical laboratories is a prime factor responsible for the high volume of tests being performed in these settings.

- For instance, according to the 2023 data published by the American Clinical Laboratory Association, there are approximately 322,488 clinical laboratories in the U.S.

Additionally, the hospital segment is also expected to register a considerable CAGR during the forecast period. The segment’s growth is attributed to the increasing demand for monitoring processes for diseases, such as diabetes, hypertension, and pregnancy, which has diverted a huge patient pool toward hospitals. This, coupled with the growing number of hospitals across the world, is also supporting the increasing adoption of these in-vitro diagnostic products.

- For instance, according to the 2021 data published by SANCTUARY PERSONNEL, there are approximately 1,257 hospitals in the U.K. Thus, the increasing number of hospitals is further supporting the growing adoption of these IVD tests.

IN-VITRO DIAGNOSTICS MARKET REGIONAL OUTLOOK

The global market has been segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America In-vitro Diagnostics (IVD) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Increasing Product Launches and Approvals by Key Players to Support the Region’s Growth

In 2025, North America represented USD 29.33 billion, accounting for 37.70% of the worldwide market, and is expected to reach USD 30.92 billion in 2026. Some of the prominent factors contributing to the region’s rapid growth include the presence of major companies, such as Abbott, Thermo Fisher Scientific Inc., BD, and Danaher Corporation, especially in the U.S., favorable government regulations, well-established diagnostic infrastructure, and adoption of technologically advanced diagnostic techniques.

- For instance, in January 2022, Sight Diagnostics received Health Canada’s approval for its Sight OLO analyzers for point-of-care settings. Through its distribution partner Inter Medico, Sight will bring the first and only 5-part differential CBC testing to emergency departments, hospitals, and other decentralized settings across Canada.

U.S. Market

The increasing prevalence of infectious and chronic diseases in the U.S. is one of the factors driving the growth of the market. The U.S. market size is estimated to hit USD 27.98 billion in 2026. This, along with the growing presence of a well-established healthcare infrastructure, favorable reimbursement scenario for in-vitro diagnostics tests, and higher awareness among the patient population about early diagnosis, is leading to the higher adoption of advanced tests and instruments by healthcare settings in the country.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe is anticipated to be the second-most dominant region in terms of market share. The Europe market generated USD 20.46 billion in 2025, representing 26.30% of the global market landscape, and is expected to reach USD 21.5 billion in 2026. The growth is owing to certain factors, including well-established infrastructure, healthcare expenditure, and an increasing prevalence of infectious diseases, cancer, and other disorders. This, coupled with the growing number of POC device launches, is likely to support the adoption of these instruments.

Germany dominated the European market in 2024. The market value in U.K. is expected to be USD 3.83 billion in 2026. On the other hand, Germany is projecting to hit USD 5.50 billion in 2026 and France is likely to hold USD 3.26 billion in 2025. The increasing prevalence of chronic diseases, such as diabetes and cancer, coupled with a well-established healthcare infrastructure, higher diagnosis rates, and increasing adoption of novel tests & instruments based on innovative techniques by healthcare settings are some of the factors fueling the growth of the in-vitro diagnostics market in the country.

- In June 2023, Sysmex Corporation launched its first point-of-care testing system to assess the effectiveness of antimicrobials using urine samples of patients in Europe.However, the regulatory challenges experienced in the region, especially in emerging countries, such as Poland, Romania, and Bulgaria, among others, also present a lucrative opportunity for the manufacturers to launch innovative devices to cater to the growing demand for IVD devices.

Key trends and innovations in the region

The rising preference for molecular diagnostics for transplant & transfusion diagnostics and disease testing, among others, is augmenting the demand for novel products. This, along with technological advancements in these devices, among other factors, is likely to support the use of these devices.

Asia Pacific

Asia Pacific contributed 23.00% to the global market in 2025, with a valuation of USD 17.86 billion, and is expected to reach USD 18.94 billion in 2026, especially in developing countries, such as India, South Korea, Australia, and China. Increasing disease prevalence, improving approval & reimbursement policies, and rising per capita healthcare expenditure in this region are projected to drive the market’s growth in Asia Pacific during 2026-2034.

- For instance, in April 2021, South Korea’s Seegene Inc. announced that it had secured an export permit from the country’s Ministry of Food and Drug Safety to export its COVID-19 variant tests to countries across the world. This permit was expected to fortify the company's sales and market position globally.

Moreover, the growing prevalence of chronic diseases, such as diabetes, cancer, gastrointestinal disorders, and others and increasing focus on the expansion of healthcare infrastructure among governmental and non-governmental organizations are likely to support the adoption of these devices. The market in China is expected to hit USD 6.61 billion in 2026, whereas India is likely to reach USD 3.37 billion and Japan is projected to hit USD 4.32 billion in 2026.

Latin America

The market in Latin America reached USD 5.99 billion in 2025, representing 7.70% of total market revenue, and is expected to reach USD 6.22 billion in 2026. However, the growing geriatric population, increasing prevalence of infectious diseases, improvements in healthcare expenditure, and increasing adoption of point-of-care devices in the region are expected to create strong growth prospects for the market in the future.

- According to the World Health Organization, the population aged 65 years and above in Chile is expected to double from 2010 to 2030. Also, according to The World Bank Group, in 2020, the population aged 65 and above was around 21.1 million in Brazil.

Middle East & Africa

The Middle East & Africa market was valued at USD 4.11 billion in 2025, capturing 5.30% of global revenue, and is expected to reach USD 4.25 billion in 2026. The Middle East & Africa is growing due to a rising focus on the development of healthcare infrastructure, increasing acquisitions & mergers among key players, and an increasing number of players expanding their presence in emerging countries, among others. The GCC market size is expected to be USD 4.25 billion in 2026.

- In July 2023, EDP Biotech Corp. and New Day Diagnostics, LLC entered a merger agreement to combine both the companies' qualities and technologies to develop innovative products in the cancer detection field.

Regulatory and Compliance Aspects

Overview of the Global Regulatory Landscape for IVD

The regulatory landscape of in-vitro diagnostics is rapidly evolving owing to the rising development, approval, and distribution of diagnostic tests used in the detection of various diseases. The U.S. FDA and Europe’s IVDR are prominent organizations that play a major role in shaping these regulations.

Regulatory Environment and Its Impact on the Market

In-vitro diagnostic devices are regulated by the Center for Devices and Radiological Health (CDRH). For a subset of medical devices, the Center for Biologics Evaluation and Research (CBER) is responsible for ensuring the safety and effectiveness of IVDs. Increasing focus on stringent regulatory guidelines for IVD devices ensures their safety and effectiveness and expands the scope of these devices in the market. However, overly stringent regulations can also deter innovation by imposing hurdles for smaller firms to compete, further slowing the pace of the development of new products.

Key Regulations in Major Markets

In-vitro diagnostics are defined as devices in section 201(h) of the Federal Food, Drug, and Cosmetic Act, and may also be biological products subject to section 351 of the Public Health Service Act. IVD devices are further subjected to premarket and post-market controls. According to the FDA Act, the devices are classified into Class I, II, or III according to the level of regulatory control that is necessary to ensure safety and effectiveness.

Challenges in navigating regulatory requirements

Manufacturers experience certain challenges while navigating regulatory requirements, such as the high cost of conformity assessment, difficulty in transitioning to new regulations, and meeting the complex documentation requirements for IVDs, among others.

Impact of compliance on market growth

Regulatory compliance ensures the safety and efficacy of the in-vitro diagnostic devices, further reducing the risks in in-vitro diagnostic techniques. However, overly stringent regulatory norms can slow the pace of the launch of IVD devices in the market.

Economic factors influencing market growth and investment:

The increasing prevalence of chronic diseases, such as gastrointestinal disorders, the rapidly increasing geriatric population, and rising technological advancements in IVD devices, among others, are some of the factors contributing to the market’s growth.

The role of public health initiatives in driving demand for IVD

There is a rising focus on government initiatives to raise awareness about the safety and efficacy of IVD procedures among the patient population. This, along with the rising number of key players focusing on research and development activities to launch novel products, is likely to support the adoption of these products.

Competitive Landscape

KEY INDUSTRY PLAYERS

Companies to Focus on Inorganic Growth Strategies to Strengthen Their Market Positions

The global in-vitro diagnostics market is semi-consolidated. A few prominent players, such as F. Hoffmann-La Roche Ltd., Abbott, and Siemens Healthineers AG, hold a majority share of the global market. F. Hoffmann-La Roche Ltd. is one of the major players operating in the global market. The rising focus of the company on R&D activities to develop and introduce technologically advanced products and novel systems is one of the significant factors contributing to the growing share of the company.

- In November 2023, F. Hoffmann-La Roche Ltd. launched Elecsys HBeAg quant, an immunoassay that is able to determine both the presence and quantity of the hepatitis Be antigen (HBeAg) in human serum and plasma.

Abbott is another leading player in the global market due to its diversified product portfolio and direct and indirect global presence. Additionally, partnerships with various key market players have further strengthened the company's market position. In September 2023, Abbott collaborated with LifeLabs, a company focused on health diagnostic services, to support the growing patient population.

Other market players include BD, QuidelOrtho Corporation, and several small-scale companies. These players are focusing on R&D to introduce new products, expand their geographic presence, and establish a strong brand presence, further supporting the global IVD market share.

LIST OF KEY IN-VITRO DIAGNOSTICS COMPANIES PROFILED

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Abbott (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Sysmex Corporation (Japan)

- Siemens Healthineers AG (Germany)

- BD (U.S.)

- Seegene Inc. (Republic of Korea)

- DiaSorin S.p.A. (Italy)

- Quest Diagnostics Incorporated (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2024 – Thermo Fisher Scientific Inc. launched a new ion chromatography instrument to improve the reliability, efficiency, and functional adaptability of labs.

- December 2023 – Thermo Fisher Scientific Inc. signed a distribution agreement with AESKU GROUP GmbH, a provider of innovative diagnostic solutions, to market IFA testing kits and instruments in the U.S.

- December 2023 – Sysmex Corporation received insurance coverage for its immunoassay reagent HISCL M2BPGi-Qt Assay Kit to cater to the growing cases of chronic hepatitis.

- November 2023 – Abbott received the U.S. FDA approval for its molecular human papillomavirus or HPV screening solution, with an aim to add a powerful cancer screening tool for detecting high-risk HPV infections to the Alinity m family of diagnostic assays.

- May 2023 – Siemens Healthineers AG launched next-generation hematology analyzers, Atellica HEMA 570 and 580 analyzers, to broaden its product portfolio in the hematology field.

REPORT COVERAGE

The report provides a detailed analysis and in-vitro diagnostics market forecast. It focuses on key aspects, such as an overview of the product, the prevalence of several diseases, key countries, and pricing analysis. Additionally, it includes an overview of reimbursement scenarios for diagnostic procedures, key industry developments, such as mergers, partnerships & acquisitions, the impact of COVID-19 on the market, and brand analysis. Besides these, the report offers insights into the latest market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market's growth in recent years. The report also covers the regional analysis of different segments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.50% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Technique

|

|

|

By Sample

|

|

|

By Setting

|

|

|

By Application

|

|

|

By End-user

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 77.73 billion in 2025 and is projected to reach USD 135.65 billion by 2034.

In 2025, North America was valued at USD 29.33 billion.

Registering a CAGR of 6.50%, the market will exhibit healthy growth during the forecast period of 2026-2034.

The reagents & consumables segment is expected to lead this market during the forecast period.

The increasing adoption of point-of-care testing devices and rising prevalence of chronic and infectious diseases are major factors driving the market growth.

F. Hoffmann-La Roche Ltd, Abbott, Danaher, Siemens Healthineers AG, Thermo Fisher Scientific Inc., and Sysmex Corporation are the major players in the global market.

North America held a dominant market share in 2026.

The rising use of advanced products in in-vitro diagnosis and increasing cases of chronic diseases around the globe are expected to drive the adoption of these products.

- 2021-2034

- 2025

- 2021-2024

- 290

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us