"Shaping The Future Of BFSI With Data-Driven Intelligence And Strategic Insights"

Corporate Bond Market Size, Share & Industry Analysis, By Type (Investment Grade and High-Yield), By Issuer Type (Large Corporate, SMEs/Private Issuers, and Startups Issuing Through Private Placement), By Term/Duration (Short-term (<3 years), Medium-term (3-7 years), and Long-term (>7 years)), By Sector (Financial Institutions, Energy & Power, High Technology, Healthcare, and Others), and Regional Forecast, 2026-2034

Last Updated: June 08, 2026

| Format: PDF

| Report ID:

FBI113826

Thank you for your interest in the

"United States Medical Devices Market!"

To receive a sample report, please provide the following details:

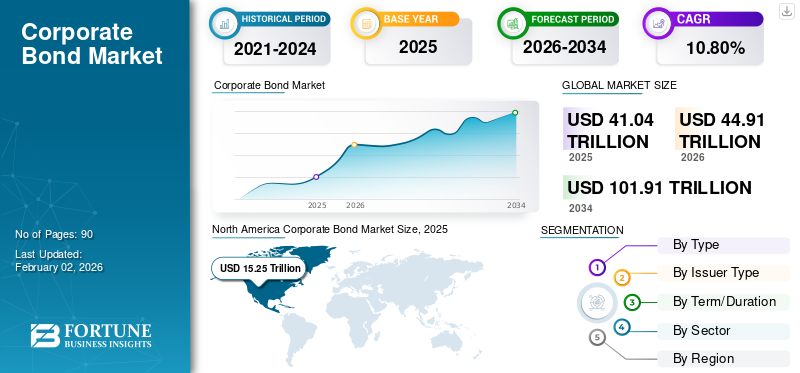

The global corporate bond market size was valued at USD 41.04 trillion in 2025, and the market is projected to grow from USD 44.91 trillion in 2026 to USD 101.91 trillion by 2034, exhibiting a CAGR of 10.80% during the forecast period. North America dominated the corporate bond market with a market share of 37.20% in 2025. Industry growth is driven by expanding institutional investment demand, corporate refinancing cycles, rising capital market participation, regulatory transparency, and evolving credit risk management frameworks.

A corporate bond is a type of debt security issued by a corporation to investors to raise capital for business needs such as operations, expansion, or acquisitions. It defines a legal responsibility by the corporation to repay the principal amount on a definite maturity date. In return, the bondholder accepts regular interest payments, known as coupons, typically semiannually. Corporate bonds are traded in the secondary market and vary in maturity, credit risk, and yield. The issuer's creditworthiness affects the bond's interest rate and investor demand.

The corporate bond market is mainly driven by increasing capital requirements of companies to fund expansion and infrastructure investments. Rising investor demand for fixed-income securities and stability, particularly during periods of equity market volatility. Additionally, favorable interest rate environments and supportive monetary policies boost corporations to raise funds through bonds, thereby propelling the market growth.

Corporate bond issuers, including JPMorgan Chase & Co., Goldman Sachs Group, Inc., and Morgan Stanley, implement multiple strategies, such as managing refinancing risks and timing, to diversify maturity profiles in the market. For instance, JPMorgan Chase & Co. is a global financial services firm that underwrites and trades corporate bonds. The other issuers may also pursue credit rating upgrades to lower borrowing costs and attract institutional investors.

The global corporate bond market represents one of the most significant segments of the fixed-income capital markets, enabling companies to raise long-term funding from institutional and retail investors without relying solely on bank financing. Corporate bonds function as debt securities issued by corporations to finance capital expenditures, refinance existing liabilities, or support strategic expansion initiatives.

The corporate bond industry plays a central role in modern financial systems. It facilitates capital allocation between institutional investors seeking stable income and corporations requiring structured financing. Pension funds, insurance companies, sovereign wealth funds, and asset managers represent the primary investors in this market. Their long-term investment horizons align well with corporate bond maturity structures.

Several macroeconomic forces shape corporate bond market size and activity levels. Interest rate cycles, monetary policy direction, credit spreads, and inflation expectations significantly influence issuance volumes and investor demand. During periods of lower interest rates, corporations typically increase bond issuance to lock in favorable borrowing costs. Conversely, tightening monetary conditions may temporarily reduce issuance activity while increasing refinancing costs. Corporate bond market trends also reflect evolving investor behavior. Institutional investors increasingly emphasize credit risk analysis, environmental, social, and governance (ESG) integration, and portfolio diversification across sectors and geographies.

Regional capital markets influence market dynamics differently. North America remains the largest corporate bond market due to deep institutional investor participation and a highly developed capital markets infrastructure. Europe maintains strong regulatory frameworks supporting cross-border bond issuance. Asia-Pacific markets continue expanding as corporate financing increasingly shifts toward capital market instruments.

The COVID-19 pandemic caused major disruptions in the market, leading to a widened yield spread and liquidity crisis in early 2020. Economic shutdowns and investor uncertainty prompted a sharp decline in demand. Central banks, particularly the Federal Reserve, intervened by purchasing corporate bonds to stabilize the market. This support helped restore investor confidence and facilitated a market recovery in the latter half of 2020.

North America dominated the corporate bond market with a 37.20% share in 2025.

The high-yield segment is expected to capture the largest market share of 53.99% in 2026.

Large corporations are expected to account for the largest market share of 68.73% in 2026.

Key Regional Highlights

North America

North America was valued at USD 15.25 trillion in 2025 and is projected to reach USD 16.66 trillion in 2026.

Asia Pacific

Asia Pacific accounted for USD 15.79 trillion in 2025 and is expected to reach USD 17.74 trillion in 2026.

Europe

Europe reached USD 7.04 trillion in 2025 and is projected to grow to USD 7.41 trillion in 2026.

U.S.

The corporate bond market is expected to reach USD 12.08 billion by 2026.

Japan

The corporate bond market is expected to reach USD 3.43 billion by 2026.

Read More

IMPACT OF GENERATIVE-AI

Rising Adoption of Gen-AI by Multiple Trading Platforms will Help Market Growth.

Generative AI transforms the market by defining credit risk modeling, powering document analysis (e.g., bond prospectuses), and creating real-time issuer insights. Various trading platforms integrate Generative AI capabilities into their systems to remain competitive. These advancements aim to enhance decision-making, trading efficiency, and user experience. For instance,

In June 2024, LTX, an AI-driven corporate bond trading platform, introduced a new GenAI-powered List Trading feature. This functionality uses GPT technology to help users seamlessly create and execute multi-directional trade lists and multi-asset classes through its RFQ+ system.

The adoption of GenAI is becoming a key differentiator in the evolving financial technology landscape. Further, AI-driven chatbots also improve investor engagement and streamline bond issuance workflows.

Corporate Bond Market Trends

Growing Demand from Foreign Investors is a Major Market Trend

The growing demand from foreign investors is emerging as a major trend in the market. As interest rates in developed countries remain low, foreign investors gradually seek higher yields from corporate bonds in other regions, specifically emerging markets. This demand is driven by better returns, search for diversification, and attractive currency exchange rates.

Additionally, the global availability of bonds through digital platforms and reduced transaction costs has facilitated foreign investments. Foreign capital inflows contribute to market liquidity, allowing companies to issue bonds at highly favorable terms. However, geopolitical risks and currency fluctuations are other factors that investors consider when allocating capital across borders. Therefore, these factors are key contributors to the market's overall growth.

The corporate bond market is undergoing a structural transformation as global capital markets continue evolving in response to regulatory changes, investor expectations, and technological developments. One of the most notable corporate bond market trends involves the increasing role of institutional investors in shaping market liquidity and pricing dynamics.

Institutional asset managers, pension funds, and insurance companies collectively account for a large share of corporate bond holdings. Their portfolio allocation strategies influence issuance demand, yield spreads, and maturity structures. As institutional capital pools expand globally, demand for diversified corporate bond portfolios continues to increase.

Another significant trend involves the growing importance of environmental, social, and governance (ESG) considerations within fixed-income investment strategies. Many investors now evaluate corporate bond issuers based on sustainability performance, governance transparency, and long-term risk management practices. This trend has contributed to the emergence of sustainability-linked bonds and green corporate bonds.

Key Market Dynamics

Market Drivers

The Growth of Electronic Trading in Major Countries to Drive the Market Growth

The expansion of electronic trading is significantly advancing the global market by enhancing efficiency, increasing accessibility, and adopting higher transparency. Different market participants accept electronic platforms, allowing a wider range of individual and institutional investors to contribute to the corporate bond market.

Further, electronic trading systems simplify the trading process by minimizing the costs and time associated with executing transactions. This improved efficiency helps traders respond more effectively to market fluctuations and results in tighter bid-ask spreads, ultimately enabling better pricing for all market participants. For instance,

According to the industry expert, nearly USD 15.00 billion of corporate bonds were traded electronically daily in 2022.

As per the Greenwich survey, in 2020, over 40% of investment-grade and 33% of high-yield corporate bonds are traded electronically.

The continued growth of electronic trading in major economies is helping in smooth bond transactions, increasing transparency, and growing market liquidity, collectively serving as a driver of corporate bond market growth. Several structural drivers contribute to the expansion of the corporate bond market as companies increasingly diversify funding sources beyond traditional bank lending. Capital market financing offers corporations greater flexibility in structuring debt maturities, managing interest costs, and accessing global investor pools.

One of the primary growth factors involves the ongoing expansion of institutional investment capital. Pension funds, insurance companies, and sovereign wealth funds collectively manage trillions of dollars in long-term assets. These investors often seek stable income-generating instruments, making corporate bonds an attractive component of diversified portfolios. Corporate refinancing cycles also stimulate bond issuance. Many corporations periodically replace short-term bank loans with longer-term bond financing to stabilize their capital structures. This refinancing activity increases issuance volumes during periods of favorable interest rate conditions.

Macroeconomic growth also influences corporate bond market growth. Expanding corporate investment in infrastructure, technology, and industrial capacity often requires significant financing. Bond issuance allows companies to raise capital without diluting equity ownership. Regulatory reforms have also improved transparency and investor protection within fixed-income markets. Enhanced disclosure standards and credit rating methodologies help investors evaluate issuer risk more effectively.

Market Restraints

Rising Credit and Default Risk by Multiple Investors Can Restrict Market Growth

Rising default and credit risks considerably restrict market growth by increasing risk premiums and reducing investor confidence. When multiple investors anticipate potential defaults, it demands higher yields, making it more expensive for companies to raise funds through bonds.

This often reduces issuance and tighter credit conditions, particularly in the high-yield segment. Small companies may face demotions, pushing them out of the shrinking eligible investor pool and investment-grade territory. These conditions boost market volatility and deter long-term investment. Ultimately, sustained credit concerns can restrict overall corporate bond market liquidity and activity.

Despite its structural importance within global financial systems, the corporate bond market faces several constraints that influence issuance activity and investor participation. Interest rate volatility remains one of the most significant factors affecting corporate bond market dynamics.

When central banks increase policy interest rates, borrowing costs for corporations typically rise. Higher yields can reduce bond issuance volumes as companies delay financing decisions or seek alternative funding sources. Rising rates may also reduce bond prices in secondary markets, influencing investor sentiment.

Credit risk represents another critical constraint within the corporate bond industry. Investors closely evaluate issuer creditworthiness, particularly during periods of economic uncertainty. Companies with weaker financial positions may face higher borrowing costs or limited market access. Liquidity constraints occasionally affect secondary market trading. Corporate bond markets tend to be less liquid than government bond markets due to the large number of issuers and varying credit profiles. Reduced liquidity can lead to wider bid-ask spreads and pricing volatility.

Market Opportunities

Technological Integration Presents a Lucrative Opportunity for the Market in the Future

Technological integration, specifically through blockchain, AI, and electronic trading platforms, offers significant opportunities for the market. AI-powered tools develop decision-making, boost the credit risk assessment, and automate bond issuance, making the process efficient and faster.

Blockchain helps to streamline settlement processes, reducing risks and transaction costs associated with errors and fraud. These technologies increase market liquidity by connecting a broader range of institutional and retail investors and improving price transparency. For instance,

In March 2025, the Inter-American Development Bank (IDB) issued its inaugural digital bond in pound sterling, utilizing HSBC Orion, a blockchain-based platform for digital assets. The issuance was governed by Luxembourg law, which enables the issuance, transfer, and secure holding of bonds and other securities in digital format.

These advancements also enable efficient bond pricing and facilitate cross-border trading. As a result, the market becomes more accessible, efficient, and dynamic, attracting more investors and issuers. The corporate bond market continues to present several strategic opportunities as global capital markets expand and investor demand for diversified fixed-income instruments increases. One notable opportunity involves the continued growth of emerging market corporate bond issuance.

Many corporations in developing economies are increasingly accessing international capital markets to finance infrastructure development, industrial expansion, and technological investment. Improved financial regulation and credit rating frameworks have strengthened investor confidence in these markets. Another opportunity lies in the expansion of sustainability-linked corporate bonds. Institutional investors increasingly allocate capital toward investments aligned with environmental and governance objectives. Companies issuing bonds tied to sustainability targets often attract broader investor participation.

Technological innovation also creates opportunities within the corporate bond industry. Digital trading platforms, data analytics systems, and automated pricing technologies enhance transparency and improve market efficiency. These tools enable investors to evaluate credit risk more effectively.

Based on type, the market is divided into investment-grade and high-yield.

High-Yield Corporate Bonds

The high-yield segment is expected to capture the largest market share of 53.99% in 2026. owing to investors' search for higher returns in a low-interest-rate environment. Low default rates and economic recovery are boosting investor confidence in riskier bonds. Companies with higher control progressively turn to high-yield bonds for financing, driving the issuance. For instance,

In 2024, according to LCD data, companies such as Royal Caribbean Cruises and US Foods raised a record of USD 109.7 billion in high-yield bonds and loans, denoting the third-largest monthly record.

High-yield corporate bonds represent a more risk-tolerant investment-grade segment of the corporate bond market. These securities are issued by corporations with lower credit ratings or limited operating histories. As compensation for higher perceived risk, high-yield bonds offer investors higher interest rates compared with investment-grade securities. This segment attracts investors seeking higher returns within fixed-income portfolios. Hedge funds, specialized credit funds, and certain institutional investors often allocate capital to high-yield bonds as part of diversified investment strategies.

Issuers within the high-yield bond market frequently include companies undergoing restructuring, leveraged buyouts, or rapid expansion phases. These corporations may not qualify for investment-grade credit ratings, but still require substantial capital to support operational growth.

Economic conditions strongly influence high-yield bond market performance. During periods of economic expansion, investor confidence typically increases, leading to greater demand for higher-yielding securities. Conversely, economic downturns may raise default risk concerns and reduce investor appetite for riskier credit instruments.

Credit risk assessment plays a central role in this segment. Investors carefully evaluate issuer balance sheets, revenue stability, and industry conditions before purchasing high-yield bonds. Credit spreads between high-yield and investment-grade bonds often serve as indicators of broader market risk sentiment.

Investment Grade Corporate Bonds

Investment grade is anticipated to grow at the highest CAGR over the forecast period. It is driven by strong demand for stable returns and lower risk, particularly in uncertain economic environments. With low interest rates and economic recovery, companies with solid credit ratings increasingly issue bonds to capitalize on favorable borrowing conditions.

Investment-grade corporate bonds represent the largest and most stable segment of the corporate bond market. These securities are issued by corporations with strong credit ratings and relatively low default risk. Credit rating agencies typically classify these bonds within the highest credit categories, reflecting the issuer’s capacity to meet interest and principal repayment obligations.

Institutional investors play a dominant role in this segment. Pension funds, insurance companies, sovereign wealth funds, and asset managers often allocate a substantial portion of fixed-income portfolios to investment-grade corporate bonds due to their predictable income streams and lower credit risk exposure.

Large corporations frequently rely on this market segment to finance long-term capital expenditures, acquisitions, and refinancing of existing debt obligations. Investment-grade bonds typically carry lower interest rates compared with high-yield bonds because investors perceive lower risk associated with the issuing companies.

Interest rate conditions strongly influence issuance activity within this segment. When borrowing costs decline, corporations often increase bond issuance to lock in favorable long-term financing conditions. In contrast, periods of rising interest rates may temporarily slow issuance volumes.

Sector diversification also characterizes this segment of the corporate bond industry. Investment-grade bonds are issued across multiple industries, including financial services, manufacturing, healthcare, and technology. Diversified sector participation contributes to stability and liquidity within the market.

By Issuer Type

Strong Credit Ratings by Large Corporations Have Enhanced Segment Growth

Based on issuer type, the market is studied into large corporates, SMEs/private issuers, and startups issuing through private placement.

Large Corporations

Large corporations are expected to capture the largest market share of 68.73% in 2026. Large corporations have the ability to issue bonds with favorable terms, supported by substantial market presence and strong credit ratings. These companies benefit from economies of scale, easier access to capital markets, and lower borrowing costs. Their bonds attract institutional investors seeking stable, low-risk returns. Additionally, large corporations can tap into global corporate bond markets, offering high liquidity and attracting diverse investor groups.

SMEs and Private Issuers

SMEs/private issuers are anticipated to grow at the highest CAGR during the forecast period, owing to their increasing reliance on debt financing as they expand. As traditional bank lending becomes more stringent, SMEs use corporate bonds to access capital. The growth of digital bond platforms and investor appetite for higher yields also contributes to this rise.

Small and medium-sized enterprises (SMEs) represent a growing issuer segment within the corporate bond industry. While SMEs traditionally relied on bank lending for financing, capital market access has gradually expanded in many regions. Private bond placements allow SMEs to raise capital from institutional investors without undertaking a full public issuance process. These placements often involve fewer regulatory requirements and lower issuance costs.

Investors participating in SME bond offerings typically conduct detailed credit assessments before allocating capital. Private placements often involve customized financing structures tailored to the issuer’s financial capacity and growth plans. SME bond issuance has increased in several emerging economies where governments encourage capital market development. Regulatory reforms and credit guarantee programs have helped smaller companies access alternative financing sources beyond bank loans.

Despite this progress, SME participation in the corporate bond market remains relatively smaller compared with large corporate issuers. Credit risk evaluation and limited financial transparency may restrict investor participation in certain cases.

Startups Issuing Through Private Placement

Startups represent a niche yet emerging issuer category within the corporate bond market, primarily through private placement structures. Early-stage companies rarely issue public bonds due to limited financial track records and higher credit risk profiles. Private placement arrangements allow startups to raise capital directly from institutional investors, venture debt funds, or specialized credit providers. These financing structures often combine debt instruments with equity-linked features.

Startup bond issuance frequently supports growth initiatives such as product development, market expansion, and technological innovation. Investors participating in such placements typically accept higher risk in exchange for potentially higher returns. Private debt markets have become an important financing channel for startups, particularly within technology and innovation-driven sectors. Venture debt structures often include convertible features that provide investors with equity participation opportunities.

By Term/Duration

Rising Acceptance of Medium-Term Bonds for Its Balanced Risk-Return Profile has Accelerated the Segment’s Dominance.

Based on term/duration, the market is analyzed into Short-term (<3 years), Medium-term (3-7 years), and Long-term (>7 years).

Medium-Term Corporate Bonds (3–7 Years)

The medium-term segment is expected to capture the largest corporate bond market share of 51.67% in 2026. owing to its balanced risk-return profile. It offers a favorable maturity range for issuers and investors, typically providing higher yields than short-term bonds while maintaining less interest rate risk than long-term bonds. Corporate issuers often prefer medium-term bonds to match their financing needs and investment horizons.

Medium-term corporate bonds represent a widely used financing instrument for corporations seeking balanced maturity structures. Bonds within this maturity range allow companies to secure financing for medium-term investments without committing to very long-term debt obligations.

Corporations frequently issue medium-term bonds to finance business expansion initiatives, equipment purchases, and infrastructure investments. These maturities provide sufficient time for companies to generate returns from financed projects. Institutional investors also find medium-term bonds attractive due to their balanced risk-return characteristics. Duration exposure remains manageable while still offering higher yields than short-term securities.

Many corporate bond issuance programs include medium-term maturities as part of diversified funding strategies. This approach allows companies to stagger debt maturities and reduce refinancing risk concentration. Medium-term bonds, therefore, represent an important component of corporate debt capital structures across various industries.

Short-Term Corporate Bonds (<3 Years)

Short-term growth is anticipated at the highest CAGR during the forecast period, owing to their attractiveness in a rising interest rate environment. Short-term duration allows investors to minimize interest rate risk by offering quicker reinvestment opportunities. Companies also increasingly issue short-term bonds to manage liquidity needs efficiently and avoid long-term commitments.

Short-term corporate bonds typically have maturities of less than three years. These instruments are often issued to support immediate liquidity needs, working capital requirements, or short-term refinancing strategies. Corporations frequently use short-term bonds to manage cash flow fluctuations or fund temporary operational expenses. Because of their shorter maturity periods, these bonds generally carry lower interest rate risk compared with long-term debt instruments.

Investors seeking liquidity and reduced duration risk often favor short-term corporate bonds. Money market funds, treasury management portfolios, and institutional investors frequently allocate capital to these instruments. Interest rate expectations also influence investor demand. When interest rates are expected to rise, investors may prefer shorter-term bonds to maintain portfolio flexibility.

Long-Term Corporate Bonds (>7 Years)

Long-term corporate bonds represent the longest maturity segment within the corporate bond market. These securities typically finance large-scale capital investments such as infrastructure projects, industrial facilities, and technological development. Corporations often issue long-term bonds to secure stable financing conditions over extended periods. Locking in long-term borrowing costs helps companies manage interest rate risk and maintain predictable financing structures.

Institutional investors such as pension funds and insurance companies frequently invest in long-term corporate bonds. Their long investment horizons align well with extended bond maturities. Long-term bonds generally offer higher yields compared with shorter maturities to compensate investors for duration risk. Changes in interest rates can significantly influence long-term bond prices.

By Sector

To know how our report can help streamline your business, Speak to Analyst

Rising Need of Corporate Bonds in Financial Institutions Propelled the Segment Growth

Based on sectors, the market is analyzed into financial institutions, energy & power, high technology, healthcare, and others.

Financial Institutions

Financial institutions are expected to capture the largest market share of 49.50% in 2026. Financial institutions are frequent issuers of corporate bonds, as they require funding for loans, investments, and regulatory capital reserves. The large size and scope of financial institutions make them attractive to investors seeking low-risk, liquid investments. Additionally, the diversified nature of their operations and global presence provides them access to a broad investor base, further driving their dominance in the market.

Financial institutions represent one of the largest issuing sectors within the corporate bond market. Banks, insurance companies, and financial service providers regularly issue bonds to strengthen capital structures and support lending activities. Regulatory capital requirements often encourage financial institutions to raise long-term funding through bond issuance. Subordinated bonds and hybrid capital instruments are common within this sector. Investor demand for financial sector bonds remains strong due to their liquidity and established credit ratings.

Energy and Power

The energy & power sector is anticipated to grow at a prominent CAGR during the forecast period, owing to increasing demand for infrastructure development, renewable energy projects, and modernization of power grids. Rising capital requirements to fund large-scale projects, including energy transition and green initiatives, are driving the issuance of bonds in this sector. As governments globally introduce supportive regulations and funding for clean energy, companies in this sector are tapping into corporate bond markets for financing.

Energy and power companies frequently issue corporate bonds to finance large-scale infrastructure investments. Power generation facilities, energy transmission networks, and renewable energy projects often require substantial capital investment. Bond financing allows companies to spread repayment obligations over long periods aligned with project revenue generation cycles.

High Technology

Technology companies increasingly participate in the corporate bond market to finance research, product development, and acquisitions. Even highly profitable technology firms often issue bonds to maintain flexible capital structures and preserve equity ownership.

Healthcare

Healthcare companies, including pharmaceutical firms and medical device manufacturers, issue corporate bonds to support research and development and global expansion strategies.

Regional Insights

Geographically, the market is divided into North America, Asia Pacific, Europe, South America, and the Middle East & Africa.

North America Corporate Bond Market Analysis

North America Corporate Bond Market Size, 2025 (USD Trillion)

North America dominated the market with a valuation of USD 15.25 trillion in 2025 and is projected to reach USD 16.66 trillion in 2026. North America dominated the market in 2024. It is primarily driven by major countries such as the U.S. and Canada, which include various issuers and investors. The market has seen significant expansion, with recent valuations reaching trillions of dollars and thousands of issuers, from major multinational corporations to smaller businesses. Key factors fueling North American market growth drivers include low interest rates, strong economic conditions, and a rising preference among corporations for debt financing over equity financing.

North America represents the largest and most mature corporate bond market globally, supported by deep institutional investor participation and sophisticated capital market infrastructure. Corporations across sectors actively use bond issuance to diversify financing beyond bank lending. Pension funds, insurance companies, and asset managers remain dominant investors. Stable regulatory oversight and high secondary market liquidity continue to reinforce North America’s leading corporate bond market share.

The U.S. accounts for the largest share of the North American market. Many companies in the U.S. are capitalizing on the relatively low cost of borrowing, locking in attractive long-term rates. For instance, in 2024, major corporations such as Microsoft and Apple issued bonds at favorable terms to finance expansion projects. The U.S. market is expected to reach USD 12.08 billion by 2026. The United States accounts for the largest portion of the global corporate bond market size due to its highly developed capital markets and broad investor participation. Corporations regularly access bond markets for refinancing, acquisitions, and capital expenditures. Investment-grade issuance dominates overall volume, although the high-yield segment remains significant. Strong institutional demand, transparent disclosure requirements, and deep secondary market liquidity sustain U.S. corporate bond market growth.

Europe Corporate Bond Market Analysis

The market in Europe reached USD 7.04 trillion in 2025, representing 17.10% of total market revenue, and is projected to reach USD 7.41 trillion in 2026. European regulators have supported corporate bond market liquidity through various initiatives, such as easing capital requirements for banks investing in corporate debt. Further, there is an increasing demand for green and ESG (Environmental, Social, and Governance) bonds as European investors prioritize sustainable investments. This trend has contributed significantly to European market growth. The U.K. market is expected to reach USD 1.45 billion by 2026, while the German market is expected to reach USD 1.13 billion by 2026.

Europe maintains a well-regulated corporate bond market supported by strong institutional investors and integrated financial markets. European corporations increasingly rely on bond issuance to complement bank financing structures. Cross-border issuance within the euro area enhances market accessibility for both issuers and investors. Regulatory frameworks emphasizing transparency and investor protection continue to strengthen market stability and support steady corporate bond market growth.

Germany Corporate Bond Market

Germany represents one of the largest corporate bond markets in continental Europe, driven by strong industrial and manufacturing sectors. Large multinational companies frequently issue bonds to finance capital-intensive investments and global expansion strategies. The presence of institutional investors, including pension funds and insurance companies, supports stable demand. Regulatory clarity and financial discipline reinforce Germany’s role within the European corporate bond industry.

United Kingdom Corporate Bond Market

The United Kingdom corporate bond market plays a significant role in global capital markets due to London’s position as a major financial center. Corporations benefit from access to international investors and sophisticated financial intermediaries. Sterling-denominated corporate bonds attract institutional investors seeking diversification. Financial services, infrastructure, and telecommunications sectors remain active bond issuers within the United Kingdom corporate bond industry.

Asia-Pacific Corporate Bond Market Analysis

Asia Pacific contributed approximately USD 15.79 trillion to the global market in 2025, accounting for 38.50% share, and is expected to reach USD 17.74 trillion in 2026. Asia Pacific will grow at the highest CAGR among other regions. Strong economic growth, particularly in emerging markets such as China and India, drives corporate investment and the need for financing. As companies seek capital for expansion, M&A activities, and infrastructure projects, there is an uptick in corporate bond issuance. Major players in the technology and manufacturing sectors utilized bonds to fund their growth strategies. The Indian market is expected to reach USD 2.94 billion by 2026.

Asia-Pacific represents one of the fastest-expanding corporate bond markets as regional economies strengthen domestic capital markets. Governments across the region increasingly promote bond financing as an alternative to bank lending. Institutional investor participation continues rising, particularly among pension funds and insurance companies. Expanding corporate financing needs, infrastructure investment, and regulatory improvements are supporting long-term corporate bond market growth across the Asia-Pacific.

Japan Corporate Bond Market

The Japan market is expected to reach USD 3.43 billion by 2026, and the China market is expected to reach USD 7.07 billion by 2026. Japan’s corporate bond market reflects strong participation from large industrial and technology companies seeking diversified financing sources. Japanese corporations frequently issue bonds to refinance debt and support international expansion. Domestic institutional investors, including pension funds and life insurance companies, provide stable demand. Low-interest-rate conditions historically encouraged bond issuance, although monetary policy changes increasingly influence market activity.

China Corporate Bond Market

China’s corporate bond market has expanded rapidly as domestic capital markets continue to develop. Corporations increasingly rely on bond financing to support industrial growth and infrastructure investment. Regulatory reforms have improved transparency and credit evaluation standards, attracting broader investor participation. State-owned enterprises remain dominant issuers, although private companies are gradually increasing market participation within China’s evolving corporate bond industry.

Latin America Corporate Bond Market Analysis

Latin America’s corporate bond market continues to develop as regional companies seek alternatives to traditional bank financing. Large corporations in sectors such as energy, mining, and telecommunications frequently access international bond markets. Investor participation remains concentrated among institutional investors seeking higher yields. Economic stability, regulatory development, and improved financial transparency will influence long-term corporate bond market growth across the region.

The South American market is growing due to increased demand for financing from local and international corporations. Key drivers include a stable macroeconomic environment, low interest rates in certain countries, and infrastructure development needs. Companies in Brazil and Argentina issued bonds to fund expansion, with a growing focus on sustainable investments.

Middle East & Africa Corporate Bond Market Analysis

The Middle East & Africa region captured 3.00% of the global market in 2025, generating USD 1.23 trillion in revenue, and is projected to reach USD 1.27 trillion in 2026. The market in the Middle East & Africa region is expanding due to economic diversification, particularly in countries such as the UAE and Saudi Arabia, which are reducing their dependence on oil revenues. Governments and corporations are issuing bonds to fund large-scale infrastructure projects, such as the Saudi Vision 2030 initiative.

The Middle East and Africa corporate bond market remains relatively smaller but demonstrates increasing development potential. Governments and corporations gradually expand capital market financing structures to support infrastructure investment and economic diversification. Energy companies represent major bond issuers. Improving regulatory frameworks and growing institutional investor participation are expected to strengthen regional corporate bond market development over time.

Competitive Landscape

Key Industry Players

Broader Service Portfolio among Key Players to Propel Market Growth

The market is fragmented owing to the presence of various major players in the market. The key players are focusing on strategic partnerships, acquisitions, and developing comprehensive corporate bonds to grow their market share. These strategies include enhancing compliance, offering broader service portfolios, and expanding into new markets.

The corporate bond market operates within a complex financial ecosystem involving issuers, investment banks, institutional investors, credit rating agencies, and trading platforms. Unlike traditional product markets, competition within the corporate bond industry primarily revolves around capital access, credit credibility, underwriting capacity, and investor distribution networks.

Investment banks play a central role in facilitating bond issuance. These institutions structure bond offerings, assess investor demand, and coordinate placement with institutional investors. Major global investment banks maintain strong positions due to their extensive investor relationships and global capital market expertise.

Institutional investors represent another critical component of the competitive landscape. Pension funds, insurance companies, mutual funds, and asset managers collectively influence demand for corporate bonds across various credit categories. Their portfolio allocation strategies significantly impact issuance volumes and pricing conditions.

Credit rating agencies also shape market dynamics by evaluating issuer creditworthiness. Independent credit assessments provide investors with standardized risk indicators, helping determine yield spreads and investor confidence. Issuers with stronger credit ratings generally access capital at lower borrowing costs.

Competition among corporate issuers frequently reflects sector-specific financing needs. Large multinational companies often dominate issuance volumes due to their strong credit profiles and established investor relationships. However, smaller companies increasingly access capital through private placement markets and specialized credit funds.

Technology is also reshaping competitive structures within the corporate bond industry. Electronic trading platforms and automated pricing tools enhance market transparency and improve secondary market liquidity. These technologies enable institutional investors to access broader bond inventories and execute transactions efficiently.

Strategic partnerships between investment banks, asset managers, and financial technology firms continue strengthening market infrastructure. Collaborative platforms improve trading efficiency, credit analytics, and risk management capabilities.

March 2025: JPMorgan Chase & Co. expanded its electronic corporate bond trading platform to enhance institutional trading efficiency. The initiative introduced advanced pricing analytics and automated liquidity aggregation to improve transparency and execution speed across global fixed-income markets.

January 2025: Goldman Sachs Group Inc. launched an expanded corporate bond origination platform designed to support cross-border issuance. The program integrates advanced credit analytics tools and digital investor distribution systems to facilitate multinational bond placements.

October 2024: BlackRock Inc. introduced a new institutional corporate bond investment strategy focused on diversified global credit exposure. The strategy integrates advanced risk modeling technologies and portfolio analytics to optimize fixed-income allocation across investment-grade and high-yield segments.

June 2024: Morgan Stanley expanded its corporate bond underwriting capabilities through enhanced digital issuance infrastructure. The platform incorporates automated investor allocation systems and data-driven demand forecasting technologies designed to improve bond issuance efficiency.

February 2024: Bloomberg LP upgraded its corporate bond analytics platform to support real-time credit spread monitoring and enhanced liquidity analysis. The update integrates machine learning-based pricing models to improve institutional investor decision-making within the global corporate bond market.

INVESTMENT ANALYSIS AND OPPORTUNITIES

The corporate bond market presents significant investment opportunities due to its stability and predictable returns, especially in the investment-grade segment. With interest rates expected to stabilize, investors can capitalize on attractive yields, particularly in high-quality, low-risk bonds issued by top-tier companies. Emerging markets also offer higher yields, though with increased risk, providing opportunities for diversification. Additionally, green and ESG bonds are gaining higher traction, offering sustainable investment options. The market is bolstered by companies' strong balance sheets and a growing trend of refinancing debt at favorable terms, providing investors with low default risks and potential capital appreciation.

REPORT COVERAGE

The report provides a detailed market analysis and focuses on key aspects such as leading companies, issuer type, and leading sector. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the market's growth in recent years.

The global corporate bond market size is projected to grow from $44.91 trillion in 2026 to $101.91 trillion by 2034, at a CAGR of 10.80% during the forecast period.