Corrugated Board Packaging Market Size, Share & Industry Analysis By Material (Virgin and Recycled), By Wall Type (Single Wall, Double Wall, and Triple Wall), By Product Type (Boxes, Trays, Inserts & Dividers, Octabins, Clamshells, Pallets, and Others), By End-use Industry (Food & Beverage {Fruits & Vegetables, Meat, Poultry & Seafood, Bakery & Confectionary, Ready-to-eat Food, and Others}, Healthcare, Personal Care & Cosmetics, E-commerce, Electrical & Electronics, Retail, Transportation & Logistics, Automotive, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

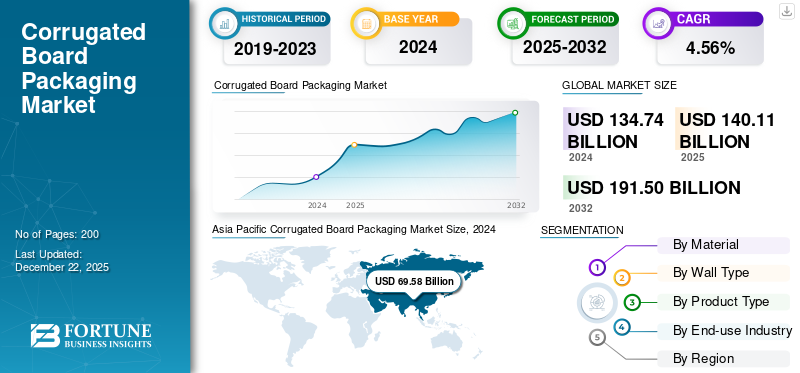

The global corrugated board packaging market size was valued at USD 140.11 billion in 2025. It is projected to be worth USD 145.94 billion in 2026 and reach USD 210.91 billion by 2034, exhibiting a CAGR of 4.71% during the forecast period. Asia Pacific dominated the corrugated board packaging market with a market share of 72.83% in 2025.

Corrugated board packaging provides a variety of advantages, mainly centered around safety, eco-friendliness, and affordability. It is a favored option due to its durability, adaptability, and ability to be recycled, which makes it ideal for diverse products and sectors. Rapidly escalating demand from the industries such as food and beverages and e-commerce sector majorly drives the market growth.

DS Smith and International Paper are the leading manufacturers, accounting for the majority of the market share globally.

Download Free sample to learn more about this report.

Corrugated Board Packaging MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 140.11 billion

- 2026 Market Size: USD 145.94 billion

- 2034 Forecast Market Size: USD 210.91 billion

- CAGR: 4.71% from 2026–2034

- Asia Pacific dominated the corrugated board packaging market with a 72.83% share in 2025.

- The virgin segment is projected to account for 67.81% of the market in 2026.

- The food & beverage segment is expected to hold 46.57% of the market in 2026.

North American

Reached USD 28.19 billion in 2025 and is expected to grow to USD 29.36 billion in 2026.

Europe

Accounted for USD 19.73 billion in 2025 and is projected to reach USD 20.40 billion in 2026.

Asia Pacific

Valued at USD 72.83 billion in 2025 and projected to reach USD 76.32 billion in 2026.

U.S.

The market is projected to reach USD 23.06 billion in 2026.

Japan

The market is projected to reach USD 14.54 billion in 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Expansion of E-commerce Sector to Drive Market Growth

The e-commerce industry is witnessing substantial expansion, fueled by greater internet access, rising smartphone adoption, and the ease of shopping online. This expansion leads to various advantages for both consumers and businesses. Corrugated board is a favored option for e-commerce packaging due to its affordability, strength, and sustainability. It offers outstanding protection for products during transport, can be tailored for branding purposes, and is easily recyclable, meeting the demand from environmentally conscious consumers. The fluted design of corrugated cardboard delivers excellent cushioning and safeguards against jolts and vibrations throughout shipping. It ensures impressive product protection while enhancing branding and improving the unboxing experience, resulting in heightened customer satisfaction and loyalty. Henceforth, the growing e-commerce sector drives the global corrugated board packaging market growth.

Rapidly Growing Demand from Food & Beverage Sector to Drive Market Growth

There is a growing demand for corrugated food packaging across fresh produce, takeout, frozen foods, and ready-to-eat meals. The packaging is cost effective, robust, and increases the demand for sustainable packaging solutions. The increase in the use of corrugated packaging in dairy, meat, and seafood sectors is due to its moisture resistance and protective characteristics—innovations, such as corrugated insulated boxes designed for temperature-sensitive items, present fresh business prospects. The food and beverage sector relies on corrugated packaging for storing, handling, and transporting processed foods, non-perishable items, and fresh produce. Different types of corrugated packages are needed depending on the perishability of the food products.

Online grocery and meal delivery services need strong, protective, and adaptable packaging. Fast food and restaurant deliveries commonly utilize corrugated pizza boxes, takeout containers, and beverage carriers. Properly sized packaging advancements assist in minimizing material waste and enhancing shipping efficiency. Henceforth, the growing demand for corrugated boards and packaging from the food and beverage sector drives the global corrugated board packaging sector.

MARKET RESTRAINTS

Fluctuating Raw Material Prices & Environmental Regulations Could Hamper Market Expansion

Key players in the market are encountering challenges such as variable raw material costs, stringent environmental regulations, and sustainability issues, which are projected to hinder the growth of the corrugated packaging sector. Governments around the globe are enforcing strict environmental laws regarding packaging waste and deforestation, which affects production processes. The demand for sustainable inks, adhesives, and coatings drives up production expenses. Businesses are under pressure to lower their carbon footprints, necessitating investments in renewable energy, and more environmentally friendly manufacturing processes.

MARKET OPPORTUNITIES

Technological Advancements to Open Doors to New Opportunities for Expansion

The integration of intelligent technologies in corrugated packaging is improving supply chain effectiveness and consumer interaction. Elements such as QR codes, RFID tags, and NFC technology facilitate real-time monitoring, verification, and engaging experiences for customers. This development is especially advantageous for managing inventory and addressing the issue of counterfeit goods. Smart packaging combines technology with conventional packaging to improve its functionality, communication, and overall user experience. This involves adding elements such as sensors, RFID tags, QR codes, and wireless communication to monitor products, assess conditions, and deliver up-to-date information to both consumers and businesses. It thus generates lucrative growth opportunities.

MARKET CHALLENGES

Limited Strength for Heavy Items and Moisture Sensitivity Create Challenges for Market Growth

Although corrugated board provides adequate cushioning and protection for a variety of products, it may not be appropriate for extremely heavy items or those that need exceptional stacking strength, particularly when exposed to rough handling. The strength of corrugated boxes is limited for heavier products, which varies based on the box's construction (ply) and the weight of the packaged item. Generally, single-wall corrugated boxes are meant for lighter products, while double- or triple-wall boxes are more suitable for heavier or delicate items. Moreover, corrugated board is not waterproof and can be damaged by moisture, potentially losing its structural integrity or causing damage to the contents. Thus, the limited strength for heavy items and moisture sensitivity challenge the market growth.

CORRUGATED BOARD PACKAGING MARKET TRENDS

Rising Demand for Sustainability and Eco-Friendly Packaging Products

Growing environmental awareness is pushing the industry to embrace more sustainable methods. Businesses are progressively utilizing recyclable resources, minimizing waste, and creating biodegradable packaging options. For example, advancements in paper-based packaging and reusable designs are becoming popular in line with consumer preferences for eco-conscious products. Consumers are more drawn to companies that show dedication to sustainability. As the importance of sustainability rises, businesses that employ eco-friendly packaging are more likely to thrive in the future. Henceforth, the rising demand for sustainability and eco-friendly packaging products emerges as a key market trend.

Download Free sample to learn more about this report.

IMPACT OF COVID-19

Substantial Surge in Online Shopping Pushed Product Demand during the Pandemic

The global corrugated packaging industry faced challenges due to the outbreak of the COVID-19 health crisis. During the COVID-19 pandemic, there was a significant increase in online shopping, making corrugated boxes an ideal choice for packaging. Corrugated boxes are available in various levels of strength, making them suitable for shipping everything from fragile glass items to sturdy electronic devices. Thus, the growing online shopping trend during COVID-19 boosted the market expansion.

SEGMENTATION ANALYSIS

By Material

Virgin Segment Leads Owing to Superior Strength and Durability

Based on material, the market is segmented into virgin and recycled.

The virgin segment is expected to lead the market, contributing 67.81% globally in 2026. Virgin corrugated fibers are longer and stronger than recycled fibers, providing better bursting strength and edge crush resistance. This makes it suitable for heavy products, long shipping routes, and situations requiring high stacking strength. The material also offers more predictable performance due to the consistent quality of virgin fibers, impelling the segment’s growth.

The recycled segment is the second-dominating material segment and is expected to grow at a rapid pace over the forthcoming years. It is a sustainable packaging choice due to its high recyclability, biodegradability, and ability to be made from renewable resources, enhancing segmental development.

By Wall Type

Remarkable Advantages of Single Wall Corrugated Board Propels Segment Growth

Based on wall type, the market is subdivided into single wall, double wall, and triple wall.

The single walls segment will account for 45.26% market share in 2026. Single-wall corrugated board packaging provides a durable and lightweight option for packaging and transporting various products. It is recognized for its affordability, recyclable nature, and capability to safeguard items during shipment. They require less material to manufacture compared to double or triple-wall boxes, making them a more budget-friendly option.

Double wall is the second-leading wall type segment and will surge over the coming years. Double-wall corrugated packaging offers enhanced strength and durability compared to single-wall options, making it ideal for heavier or more fragile items. It provides better protection against impacts, compression, and punctures during shipping and storage, further leading to rapid growth.

By Product Type

Increasing Demand from Varied End-use Industries Boosts Boxes Segment Growth

Based on product type, the market is divided into boxes, trays, inserts & dividers, octabins, clamshells, pallets, and others.

The boxes segment led the market accounting for 72.32% market share in 2026. Corrugated boxes provide a variety of advantages, which is why they are favored for packaging and transportation. These advantages encompass resilience and long-lasting quality, affordability, options for customization, and ecological sustainability. Their capacity to safeguard items while in transit, along with their flexibility and user-friendliness, plays a significant role in their extensive use across different end-use industries.

The trays segment is the second-dominating product type segment and is expected to expand at a rapid rate over the coming years. They provide numerous advantages, such as outstanding product safeguarding, affordability, and environmental friendliness, which contribute to their popularity as a packaging solution. They are durable, lightweight, and can be tailored to accommodate a range of product dimensions and forms, making them adaptable for various uses.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Rapidly Expanding Food & Beverages Industry to Cushion Segment’s Growth

Based on end-use industry, the market is fragmented into food & beverage, healthcare, personal care & cosmetics, e-commerce, electrical & electronics, retail, transportation & logistics, automotive, and others.

The food & beverage segment is expected to account for 46.57% of the market in 2026. The industry is a major consumer of corrugated board packaging for both shipping and retail display. The growth of this sector, particularly in developing countries, fuels the demand for corrugated board packages. The multi-layered structure of corrugated cardboard provides excellent cushioning, protecting food and beverages from damage during shipping and handling. The massive growth of the food and beverage sector thus increases demand and drives the segment’s growth.

The e-commerce segment is the second-leading segment and will grow at a significant rate. The rising internet penetration, innovations by manufacturers, and online shopping trends amongst the young population cushions the segment’s growth.

CORRUGATED BOARD PACKAGING MARKET REGIONAL OUTLOOK

North America, Europe, Latin America, Asia Pacific, and the Middle East & Africa are the five main regions across which the market has been analyzed geographically.

North America

Asia Pacific Corrugated Board Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Growing Consumer Inclination toward Food Drive North America Industry Growth

The North America market accounted for USD 28.19 billion in 2025, representing 20.12% of the global industry, and is expected to reach USD 29.36 billion in 2026. North America ranks as the second-largest region in the market. It also emerges as the fastest-expanding market, primarily due to ongoing growth driven by consumer preferences that emphasize convenience and sustainability in corrugated packaging solutions. Manufacturers are channeling investments into food and beverage products to satisfy consumer needs. Specifically, Canada and the U.S. boast a well-established and substantial consumer base with high levels of disposable income. This leads to a robust demand for a variety of packaged goods, such as cosmetics, food and beverages, consumer electronics, and pharmaceuticals. The U.S. market is projected to reach USD 23.06 billion by 2026.

- According to data from the USDA Economic Research Service (ERS), the average allocation of disposable income to food by American consumers stood at 11.2% in 2023. This figure is in alignment with the 2022 level. A decline from 5.6% to 5.3% has been recorded in the percentage of income allocated to food purchase for consumption at home, whereas the spending on dining out depicted a surge from 5.6% to 5.9%.

Asia Pacific

Massive Growth in the Food Sector Drives the Asia Pacific Market Progress

In 2025, Asia Pacific represented USD 72.83 billion, accounting for 51.98% of the worldwide market, and is projected to grow to USD 76.32 billion in 2026. Factors such as swift industrial growth, urban expansion, and an increasing middle-class demographic stimulate the need for packaged goods, which in turn enhances the demand for corrugated board packaging. The ready-to-eat food industry, which utilizes significant quantities of corrugated packaging, serves the fast-moving consumer lifestyle by reducing preparation times. Stringent food safety regulations enforced in Asian nations affect the market in the region. The Japan market is projected to reach USD 14.54 billion by 2026, the China market is projected to reach USD 24.87 billion by 2026, and the India market is projected to reach USD 20.93 billion by 2026.

- According to the Ministry of Consumer Affairs, Food & Public Distribution (MCF), the significant factors contributed to escalated food consumption comprise the lack of time for preparing food, surging number of working individuals, and the rising elderly population in India. The changing consumer lifestyles and preferences are influencing the higher demand for ready-to-eat meals and processed foods.

Europe

Single-use Plastic Ban Majorly Boosts Market Growth in Europe

Europe recorded a market size of USD 19.73 billion in 2025, capturing 14.08% of the global market share, and is projected to reach USD 20.4 billion in 2026. European manufacturers are at the forefront of developing sustainable packaging solutions. The region enforces some of the strictest regulations globally regarding chemicals, emissions, and packaging waste (for instance, REACH, the Green Deal, and the Single-Use Plastics Directive). Moreover, the European Union (EU) is phasing out certain single-use plastics with a ban that targets items such as plastic cutlery, plates, straws, and polystyrene food containers. This initiative is part of a broader strategy to reduce plastic waste and promote sustainable alternatives. The ban is being implemented through the Single-Use Plastics Directive, which also sets targets for recycling and recycled content in packaging. The UK market is projected to reach USD 3.23 billion by 2026, while the Germany market is projected to reach USD 4.4 billion by 2026.

- The European Union states that single-use plastic products are more likely to end up in our seas than reusable options. 70% of all marine litter in the EU constitutes the 10 single-use plastic items that are most commonly found on European beaches, alongside fishing gear.

Latin America

Growing Demand for Corrugated Boxes from Several Sectors Enhances Market Growth in Latin America

The Latin America market was valued at USD 10.67 billion in 2025, capturing 7.61% of global revenue, and is estimated to reach USD 10.97 billion in 2026. This area has a substantial premium market for food, e-commerce, cosmetics, and pharmaceuticals, resulting in a need for corrugated boxes and cartons, as well as packaging that is visually appealing and safe for brands. These sectors require corrugated packaging that complies with health and safety standards while also offering a strong shelf presence.

- According to the Merchant Risk Council, businesses that engage in online sales are discovering Brazil as an excellent option for global growth. Sectors such as retail and digital products experienced a significant surge in sales amid the COVID-19 pandemic, further speeding up a shift that was already underway in the nation: they recorded a 44% and 50% rise in sales volumes from 2019 to 2020.

Middle East & Africa

Surging Demand from Retail Sector Propels Market Expansion in the Middle East & Africa

Middle East & Africa contributed 6.21% to the global market in 2025, with a valuation of USD 8.7 billion, and is projected to reach USD 8.89 billion in 2026. The growing retail market in several countries due to the high consumer spending, a thriving tourism sector, and a growing e-commerce industry boost market expansion. Robust consumer spending, fueled by a growing economy and rising disposable incomes, is a major contributor to the retail sector's expansion.

- According to the Middle East Council of Shopping Centres & Retailers, the retail industry had a crucial impact on the growth of non-oil GDP, accounting for almost 23% in 2023. Although experiencing challenges in 2024, the Saudi retail sector is showing strength by capitalizing on the robust performance observed in 2023.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Leading Market Participants Introduce New Products to Embrace Significant Growth Avenues

The global corrugated board packaging market is highly competitive and fragmented. A few significant players are introducing innovative packaging products to dominate the market. These pivotal players are constantly emphasizing the expansion of their clientele base across various regions by bringing innovation in their existing product portfolios. Major developments by manufacturing companies have also been underpinned in the market report. International Paper and Mondi Group are the leading manufacturers, accounting for the largest global market share.

Major industry players include Cascades, DS Smith, Georgia-Pacific, Green Bay Packaging, International Paper, Mondi Group, and others. A number of other market players are focused on providing advanced packaging solutions and adopting strategies as per market scenarios.

List of Key Corrugate Board Packaging Companies Profiled

- Alliabox (Italy)

- Arvco Container (U.S.)

- Cascades (Canada)

- DS Smith (U.K.)

- Georgia-Pacific (U.S.)

- Green Bay Packaging (U.S.)

- International Paper (U.S.)

- Mondi Group (U.K.)

- Nine Dragons Paper (China)

- Oji Holdings (Japan)

- Packaging Corporation of America (U.S.)

- Pratt Industries (U.S.)

- Progroup (Germany)

- Rengo (Japan)

- SCG Packaging (Thailand)

- Smurfit Kappa (Ireland)

- Stora Enso (Finland)

- U-Pack (U.S.)

- Visy Industries (Australia)

- WestRock (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In January 2025, Biedronka partnered with Mondi in a circular program aimed at supplying, collecting, and recreating its corrugated packaging in accordance with the retailer’s goals for plastic usage and CO2 emissions. The produced paper is then sent to one of Mondi’s six factories in Poland, where it is converted into corrugated cardboard packaging, such as crates for fruits and vegetables.

- In June 2024, Saica Group, a prominent player in packaging solutions, partnered with Mondelez, a major manufacturer of fast-moving consumer goods, to introduce a new paper-based product aimed at multipack items in the confectionery, biscuits, and chocolate sectors. This new packaging made from paper is intended to be recyclable within the paper waste stream. It is compatible with heat-sealable packing processes, offering the choice to be produced either coated or uncoated based on the desired final look.

- In January 2024, Cascades Inc. introduced new designs for produce baskets aimed at the produce industry. Constructed with up to 100% recycled fibers, the company claims that these new baskets featuring flaps provide a sustainable option for produce growers, serving as a replacement for packaging that is difficult to recycle.

- In September 2022, VPK Group launched its fit2size® brand as part of its growth strategy aimed at expanding Fanfold corrugated packaging solutions throughout Europe. To meet the rising demand for e-commerce and logistics packaging, the company developed a new product utilizing the latest Fanfold innovation to reinforce its commitment to providing outstanding sustainable packaging solutions.

- In July 2020, Sabert Corporation, a prominent global producer of cutting-edge food packaging products and solutions, unveiled its latest product line, the Kraft Collection. The Kraft Collection by Sabert features a diverse range of corrugated and paperboard food packaging options crafted from various materials that are recyclable and compostable, and include post-consumer fiber content, highlighting Sabert's enduring dedication to sustainability.

INVESTMENT ANALYSIS AND OPPORTUNITIES

Several manufacturers are focusing on investing in corrugated packaging. Investing in the corrugated board packaging industry presents a compelling opportunity, driven by both its inherent advantages as a packaging material and current market trends.

- In March 2022, Mondi, a global leader in the packaging and paper industry, is allocating USD 294.43 million to enhance corrugated packaging operations across four nations to increase production and improve customer service. This investment includes approximately USD 194.53 million dedicated to its network of corrugated solutions plants in central and eastern Europe, along with USD 99.89 million directed toward Mondi Świecie’s containerboard mill in Poland, highlighting Mondi’s dedication to its customers, workforce, and sustainable production practices. Collectively, these investments form a significant component of Mondi’s previously announced USD 1.05 billion in capital investment projects this year aimed at promoting growth in sustainable packaging.

REPORT COVERAGE

The market research report provides a detailed market analysis. The market overview focuses on key aspects, such as top players, competitive landscape, product types, market segments, Porter's five forces analysis, and leading segments of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.71% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material

|

|

By Wall Type

|

|

|

By Product Type

|

|

|

By End-use Industry

|

|

|

By Region

|

Frequently Asked Questions

As per a study by Fortune Business Insights, the market size stood at USD 145.94 billion in 2026.

The market is likely to grow at a CAGR of 4.71% over the forecast period (2026-2034).

The food and beverages end-use industry segment will lead the market over the forecast period.

Asia Pacifics market size stood at USD 72.83 billion in 2025.

The key market drivers are rising growth of e-commerce sector and rapidly growing demand from food & beverage sector.

Some of the top players in the market are Cascades, DS Smith, Georgia-Pacific, Green Bay Packaging, International Paper, Mondi Group, and others.

The global market size is expected to reach USD 210.91 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us