Counter-Hypersonic Defense Market Size, Share & Industry Analysis, By Solution Layer (Space-Based Tracking & Custody, Terrestrial/Maritime Sensors, Bmc3 / C2 & Data Fusion, Transport / Data Backbone, Effectors/Interceptors, and Integration, & Others), By Threat Type (Hypersonic Glide Vehicles, Hypersonic Cruise Missiles), By Range (Point Defense, Area Defense, Theater Missile Defense, and Strategic / Homeland Defense), By Component (Sensors, Interceptors / Effectors, Launch Systems, & Others), By Deployment Platform (Space, Land, Sea, & Air), By End User, and Regional Forecast, 2026-2034

Counter-Hypersonic Defense Market Size and Future Outlook

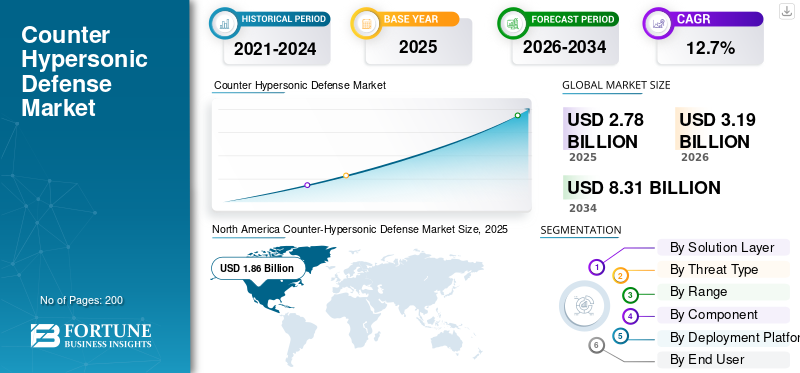

The counter-hypersonic defense market size was valued at USD 2.78 billion in 2025. The market is projected to grow from USD 3.19 billion in 2026 to USD 8.31 billion by 2034, exhibiting a CAGR of 12.7% during the forecast period. North America dominated the counter hypersonic defense market with a market share of 66.90% in 2025.

The counter-hypersonic defense market includes technologies designed to detect, track, and defeat hypersonic threats. These threats include hypersonic missiles, cruise missiles, and hypersonic glide vehicles. The market is expanding as the U.S. and its allies are investing heavily in missile defense systems that respond faster, stronger strike capabilities, and next-generation hypersonic systems.

Key players such as Northrop Grumman, Lockheed Martin, RTX, and L3Harris are pushing the market forward through active weapons development, interceptor programs, sensor upgrades, and participation in broader defense programs. Growth is also backed by efforts to build a stronger industrial base and supply chains. Major U.S. initiatives, such as the Long Range Hypersonic Weapon (LRHW) and projects connected to the Defense Advanced Research Projects Agency, continue to shape future weapon systems and readiness against hypersonic threats.

Download Free sample to learn more about this report.

Counter Hypersonic Defense Market Key Takeaways

- 2025 Market Size: USD 2.78 billion

- 2026 Market Size: USD 3.19 billion

- 2034 Forecast Market Size: USD 8.31 billion

- CAGR: 12.7% from 2026–2034

- North America dominated the counter-hypersonic defense market with a 66.90% share in 2025.

- The Space-Based Tracking & Custody segment dominated the market in 2025.

- The Effectors/Interceptors segment is projected to grow at the highest CAGR of 19.6% during the forecast period.

Asia Pacific

Asia Pacific is the second-largest market and is projected to grow at the highest regional CAGR of 16.2%.

North America

North America leads the market, driven by high defense spending, advanced missile defense programs, and large-scale investments in interceptors.

Europe

Europe is strengthening its counter-hypersonic defense capabilities through multinational programs such as HYDEF and broader NATO and EU defense initiatives.

U.S.

U.S. market was valued at approximately USD 1.81 billion in 2025 and is projected to grow at a 10.0% CAGR during the forecast period.

Japan

Japan market was valued at approximately USD 0.14 billion in 2025.

Read More

COUNTER-HYPERSONIC DEFENSE MARKET TRENDS

Space-Based Tracking and Layered Interception Emerges as a Key Market Trend

Shift from standalone interceptor programs to a broader layered counter-hypersonic structure centered on space-based tracking, fire-control quality sensing, and quicker battle management is an emerging trend in the market. This shift is attributed to hypersonic weapons’ ability to move fast and change direction sharply for outdated missile defense networks tracking and destroying such advanced missiles is not possible. In such case space-based tracking and layered interception plays important role. As a result, defense agencies are focusing more on collections and integrated sensor-to-shooter systems that can detect, track, and assist interception earlier in flight.

In February 2024, the Missile Defense Agency (MDA) and the Space Development Agency (SDA) announced the successful launch of Tranche 0 Tracking Layer satellites. They also launched two Hypersonic and Ballistic Tracking Space Sensor (HBTSS) satellites. This event represents a significant step toward using space-based tracking to address hypersonic threats.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Hypersonic Weapon Deployments and Increasing Threat Complexity Are Fueling the Market Growth

Increasing awareness of the inadequacy of traditional missile defense against hypersonic threats is the main factor driving this market. Rising global investment in hypersonic technology is transforming the battlefield, creating a threat-driven market. To counter these high-speed, maneuvering weapons, defense planners are prioritizing advanced, integrated, and layered defense systems to maintain tactical advantage.

In April 2024, the U.S. Space Development Agency (SDA) awarded Boeing-owned Millennium Space Systems a firm-fixed-price contract valued at approximately USD 414 million to build and deliver eight satellites for the Fire-control On Orbit-support-to-the-war Fighter (FOO Fighter or F2) program.

MARKET RESTRAINTS

High Technical Complexity and Long Development Timelines Are Restraining Market Growth

The primary hurdle in this sector is that defending against hypersonic threats is one of the hardest problems in modern defense. It demands near-perfect, synchronized performance across the entire kill chain sensors, tracking, and engagement. As this requires high technical precision, it slows development and makes it more expensive than traditional missile defense upgrades.

MARKET OPPORTUNITIES

Expanding Multinational Co-Development and Joint Procurement Programs Are Creating a Major Market Opportunity

The major shift in the defense market is the move toward multinational co-development, where nations join forces to share technology and funding, as creating effective counter-hypersonic defenses is too complex and expensive to do alone. By agreement, joint development, shared testing, and collaborative procurement, governments are creating a more sustainable model. For suppliers, this offers an opportunity to build larger-scale programs that serve multiple countries, rather than relying on a single market.

MARKET CHALLENGES

Real-Time Tracking and Insight of Maneuvering Hypersonic Threats Remains a Major Market Challenge

A primary challenge in this market is overcoming the operational hurdle of maintaining continuous custody, and generating precise, real-time targeting data on highly maneuverable, high-speed threats. Advanced interceptors are not sufficient to counter hypersonic threats. The entire detection-to-engagement process needs to work with high speed, so integrating all necessary systems to counter the hypersonic threat presents challenges. The key issue lies in the need for space sensors, terrestrial tracking, command-and-control, and weapons handoff to work together without delay, which hinders counter-hypersonic defense market growth.

Impact of Russia Ukraine War

Russia-Ukraine War Accelerated Demand for Layered Counter-Hypersonic and Advanced Missile Defense Systems

The Russia-Ukraine war advanced the market. It pushed governments to refer to high-end air and missile defense as an urgent operational need rather than a long-term goal. The scale of Russian missile strikes increased the demand for faster tracking, better interception, stronger industrial capacity, and more reliable supply chains, especially in the U.S. and Europe. NATO states that Russia’s war has highlighted the need for credible and strong air and missile defense. Meanwhile, the European Commission has increased support for joint procurement of air and missile defense systems.

Segmentation Analysis

By Solution Layer

Growing Reliance on Orbital Tracking for Hypersonic Detection Drives Space-based Tracking & Custody Segment Growth

By solution layer, the market is categorized into space-based tracking & custody, terrestrial/maritime sensors, BMC3 / C2 & data fusion, transport / data backbone, effectors / interceptors, and Integration, test & sustainment.

The space-based tracking & custody segment dominated the market in 2025. It is hard to detect and track hypersonic weapons using only ground-based systems. Space-based setups offer wider coverage, faster warning, and steady monitoring of fast-moving targets. Defense planners are increasingly focusing on orbital tracking layers as the foundation for future counter-hypersonic networks. The U.S. Space Development Agency states that its Tracking Layer provides global warning, tracking, and targeting of advanced missile threats, including hypersonic missile systems.

In January 2024, the U.S. Space Development Agency (SDA) awarded contracts to build 54 Tranche 2 Tracking Layer satellites for the Proliferated Warfighter Space Architecture. SDA stated that these satellites will provide missile warning, missile tracking, and fire-control quality infrared sensing to support missile defense.

Effectors / interceptors segment is expected to grow at a CAGR of 19.6% over the forecast period.

By Threat Type

Hypersonic Glide Vehicles (HGVs) Segment Dominates Due to High Maneuverability and Urgent Need for Glide-Phase Interception

By threat type, the market is classified into Hypersonic Glide Vehicles (HGVs), Hypersonic Cruise Missiles (HCMs), advanced maneuvering hypersonic threats, and emerging reentry and boost-glide hybrid threats.

The Hypersonic Glide Vehicles (HGVs) segment held the largest counter-hypersonic defense market share in 2025. These systems are first-tier hypersonic threats to stop with traditional missile defense systems. Unlike regular ballistic paths, HGVs can move within the atmosphere at very high speeds. This reduces warning time and makes interception more complicated. As a result, defense agencies are prioritizing detection, tracking, and glide-phase interception capabilities designed specifically for this type of threat.

Advanced maneuvering hypersonic threats segment is expected to grow at a CAGR of 15.7% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Range

Rising Focus on Layered Defense Against Hypersonic Threats Drives Strategic/Homeland Defense Segment Growth

By range, the market is segmented into point defense, area defense, theater missile defense, and strategic / homeland defense.

The strategic/homeland defense segment led the market in 2025, as investment in countering hypersonic threats is mainly focused on protecting national command structures, population centers, and key military infrastructure. Hypersonic threats are tactical risks on the battlefield and are also considered strategic weapons that can undermine homeland security, the credibility of deterrence, and decision-making time. Governments are focusing more on layered homeland defense systems that integrate tracking, command and control, and next-generation interceptors.

Point defense is the fastest growing segment expected to record a CAGR of 16.6% over the forecast period.

By Component

Critical Role of Real-time Sensing in Hypersonic Defense Drives Radar and Tracking Systems Segment Growth

By component, the market is segmented into sensors, interceptors / effectors, launch systems, radar and tracking systems, command and control systems, software, AI, and data fusion modules, and support, integration, and sustainment services.

The radar and tracking systems segment held the largest market share in 2025, as every counter-hypersonic setup depends on reliable sensing and tracking at the front end. Hypersonic threats move at high speeds, can change direction in flight, and shorten reaction times. Defense networks rely on radar and tracking systems to detect launches, maintain awareness, identify targets, and relay usable fire-control data to interceptors. This component serves as the operational backbone of the market, and interceptors, command systems, and other layers depend on it for effective functioning, resulting in segment dominance.

Interceptors/effectors is fastest growing segment in the market, expected to grow at a CAGR of 19.2% during the forecast period.

By Deployment Platform

Integration with Existing Defense Infrastructure Drives Reliable Deployment and Readiness Drives Land Segment Growth

By deployment platform, the market is segmented into space, land, sea, and air.

The land segment held the largest market share in 2025. Land-based counter-hypersonic systems are easier to integrate with existing command networks, fixed radar systems, interceptor sites, and layered homeland defense setups. Additionally, they provide ongoing readiness to protect strategic bases, critical facilities, and national territory, resulting land based deployment platforms that are the reliable and practical option for early operational deployment. In real-world defense planning, land platforms are key for both homeland protection and long-range fire integration.

Sea segment is expected to grow with a CAGR of 15.6% over the forecast period.

By End User

Centralized Procurement and Strategic Oversight by Defense Bodies Drive National Missile Defense Agencies Segment Growth

By end user, the market is segmented into national missile defense agencies, air defense forces, navies, and joint / coalition IAMD operators.

The national missile defense agencies segment held the largest market share in 2025. These agencies focus on threat assessment, program funding, interceptor development, sensor integration, and operational deployment. Counter-hypersonic defense is mostly managed by states and involves high costs and sensitive strategic considerations. Procurement decisions are primarily made by national missile defense bodies instead of being spread across commercial or civil users. Moreover, these agencies influence the market by setting requirements, organizing major competitions, and promoting layered structures for homeland and regional defense.

Navies segment is expected to grow at a CAGR of 15.7% during the forecast period.

Counter-Hypersonic Defense Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and rest of the world (Middle East & Africa, and Latin America).

North America

North America Counter-Hypersonic Defense Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market in 2025. In this region, the U.S. has a strong defense budget, urgent operational needs, and established missile defense systems. Additionally, major counter-hypersonic projects are funded in this region, including interceptors, space-based tracking, command and control, and modernization of homeland defense. This provides the region with strong advantage in program size, testing, and readiness for deployment compared to other markets. The U.S. Missile Defense Agency defines its mission as developing and deploying a layered missile defense system. This system aims to protect the U.S., its deployed forces, allies, and friends from missile attacks during all flight phases.

U.S. Counter-Hypersonic Defense Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1.81 billion in 2025, growing at a CAGR of 10.0% over the forecast period.

Asia Pacific

Asia Pacific is the second largest market and is anticipated to grow at a CAGR of 16.2% during the forecast period. For instance, in May 2024, the U.S. and Japan signed the Glide Phase Interceptor (GPI) agreement. The U.S. Department of Defense stated that this project will offer hypersonic missile defense capability during the glide phase and enhance regional deterrence. This demonstrates that the Asia Pacific is focusing on awareness and developing counter-hypersonic capabilities.

China Counter-Hypersonic Defense Market

China’s market is projected to be one of the largest in Asia pacific, with 2025 revenues valued at around USD 0.16 billion, representing roughly 29.28% of global sales.

Japan Counter-Hypersonic Defense Market

The Japanese market in 2025 was valued at around USD 0.14 billion, accounting for roughly 25.54% of global revenues.

Europe

Europe holds a smaller share compared to North America, but it is shifting from discussions to developing structured programs. Multinational cooperation, such as NATO and the European Union, is driving this progress, especially through HYDEF. OCCAR describes HYDEF as Europe’s first program for defense against hypersonic threats. It is funded by the European Defence Fund and connected to the broader TWISTER architecture. The region is still in the build-up phase rather than fully operational, highlighting significant market growth potential.

France Counter-Hypersonic Defense Market

France market reached USD 0.07 billion in 2025, equivalent to around 23.46% of industry revenues.

Germany Counter-Hypersonic Defense Market

The Germany’s market size was estimated at around USD 0.08 billion in 2025, representing roughly 25.58% of global revenues.

Rest of the World

Rest of the world (Middle East & Africa and Latin America), has a comparatively smaller share, growing at a CAGR of 12.1% over the forecast period. Middle East & Africa region is active, due to the recent conflict between Israel & U.S. and Iran. Countries with established missile defense systems, such as Israel, fuel the market growth in this region. Rafael reports that it is developing the SkySonic interceptor specifically for hypersonic missile defense. Meanwhile, the Israel Ministry of Defense is expanding advanced missile-defense programs through the IMDO and the Arrow family. On the other hand, the Latin America region is focused on a few technologically advanced defense countries instead of being widespread across all markets.

Latin America Counter-Hypersonic Defense Market

The Latin America market was estimated at around USD 0.01 billion in 2025, accounting for roughly 12.54% of global revenues.

Middle East & Africa Counter-Hypersonic Defense Market

Middle East & Africa market size was estimated at around USD 0.07 billion in 2025, and is expected to reach USD 0.20 billion in 2034, representing roughly 87.46% of global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Integrated Hypersonic Defense Capabilities Across Systems to Gain Market Advantage

The global counter-hypersonic defense market is led by a few major defense companies with strong positions in missile defense, sensors, interceptors, and command and control integration. The market is shaped by players such as Northrop Grumman, RTX, Lockheed Martin, L3Harris Technologies, and Rafael Advanced Defense Systems. These companies are connected to valuable government programs and can support the entire process from tracking to interception. The market growth is also driven by strong technical skills, lasting defense relationships, and the ability to fit into national missile defense plans.

These companies are propelling the market growth through real program activity. Northrop Grumman and RTX are key players in glide-phase interceptor efforts. Lockheed Martin is becoming more important through strategic missile defense programs. L3Harris is gaining traction with space-based tracking and sensing layers. Meanwhile, Rafael is increasing its presence with targeted hypersonic interceptor development. Briefly, competition in this market comes down to companies that can deliver effective counter-hypersonic capabilities in tracking, discrimination, interception, and system integration, rather than companies having the largest product catalog.

LIST OF KEY COUNTER-HYPERSONIC DEFENSE COMPANIES PROFILED

- Northrop Grumman Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- RTX (Raytheon Technologies) (U.S.)

- Boeing Defense, Space & Security (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- Rafael Advanced Defense Systems Ltd. (Israel)

- General Atomics Aeronautical Systems, Inc. (U.S.)

- Leidos Holdings, Inc. (U.S.)

- MBDA (France)

- Thales S.A. (France)

- Israel Aerospace Industries Ltd. (Israel)

- Mitsubishi Heavy Industries, Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- November 2024: Japan’s Ministry of Defense awarded Mitsubishi Heavy Industries a contract worth USD 366.25 million for Japan’s share of the Glide Phase Interceptor (GPI) joint development.

- May 2024: Japan’s Ministry of Defense announced the signing of the U.S. Japan Glide Phase Interceptor project agreement. This formally launched the joint development of the GPI and strengthened allied efforts in counter-hypersonic defense.

- April 2024: The Missile Defense Agency awarded Lockheed Martin to continue developing the Next Generation Interceptor (NGI). This includes the critical design review, qualification, integration into the Ground-Based Midcourse Defense Weapon System, and testing.

- April 2024: The Space Development Agency awarded Millennium Space Systems a contract valued at about USD 414 million to build eight Foo Fighter (F2) satellites. These satellites aim to demonstrate advanced missile defense capability using high-quality fire-control sensors in orbit.

- February 2024: The Missile Defense Agency and Space Development Agency confirmed the successful launch of two Hypersonic and Ballistic Tracking Space Sensor (HBTSS) satellites. They also launched the last four SDA Tranche 0 Tracking Layer satellites. This development is for tracking advanced missile threats in orbit.

- January 2024: The U.S. Space Development Agency awarded contracts to create 54 Tranche 2 Tracking Layer satellites. These satellites will support missile warning, tracking, and defense sensing. This move reinforces the shift toward space-based tracking as a key part of counter-hypersonic strategy.

- December 2023: The U.S. Missile Defense Agency completed Flight tested Ground-Based Midcourse Defense-12 (FTG-12). This test was an important milestone in U.S. homeland missile defense. It highlighted ongoing progress in strategic interception capability.

- June 2022: The U.S. Missile Defense Agency awarded Northrop Grumman and Raytheon Missiles & Defense to advance in the Glide Phase Interceptor (GPI) prototype project. This decision marked a significant early development step in dedicated defense against regional hypersonic missile threats.

REPORT COVERAGE

The global counter-hypersonic defense market analysis provides an in-depth study of market size, company profiling and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on strategic partnerships, mergers, and acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of market key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.7% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Solution Layer

|

|

By Threat Type

|

|

|

By Range

|

|

|

By Component

|

|

|

By Deployment Platform

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.78 billion in 2025 and is projected to reach USD 8.31 billion by 2034.

In 2025, North Americas market value stood at USD 1.86 billion.

The market is expected to exhibit a CAGR of 12.7% during the forecast period.

Space-based tracking & custody led the market by solution layer.

Rising hypersonic weapon deployments and increasing threat complexity are the key factors driving the market.

Key players in the market include Northrop Grumman, Lockheed Martin, RTX, General Dynamics, L3Harris, General Atomics, Rafael Advanced Defense Systems Ltd., and Israel Aerospace Industries Ltd.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us