Counter-UAS Market Size, Share & Industry Analysis, By Platform (Fixed, Mobile & vehicle-mounted, Portable, and Naval/maritime), By Component (Detection & Tracking, AI Fusion, Soft-kill Mitigation, Hard-kill Mitigation, and Others), By Threat Class, By Neutralization Technology (RF Jamming, GNSS Jamming/Spoofing, Directed-energy Lasers, High-power Microwave, and Others), By Application (Military Base & Force Protection, Critical infrastructure, and Others), By End User (Defense & Military Forces, Homeland Security & Border Agencies, and Others), and Regional Forecast, 2026-2034

Counter-UAS Market Size and Future Outlook

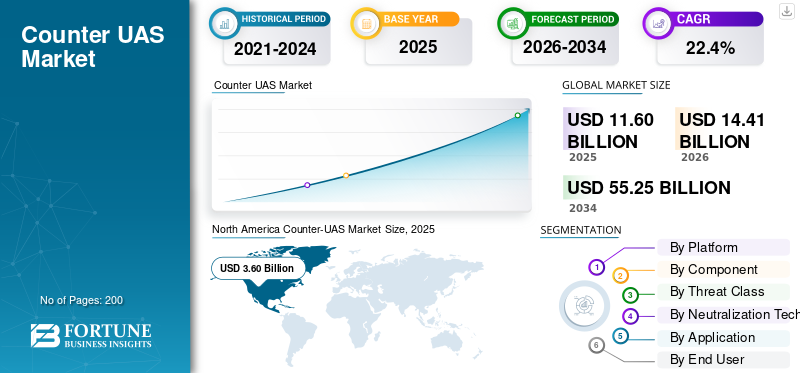

The counter-UAS market size was valued at USD 11.60 billion in 2025. The market is projected to grow from USD 14.41 billion in 2026 to USD 55.25 billion by 2034, exhibiting a CAGR of 22.4% during the forecast period. North America dominated the counter-UAS market with a market share of 31.03% in 2025.

Counter-UAS refers to layered C-UAS systems designed to detect, track, identify, and neutralize unauthorized or hostile unmanned aerial systems before they pose safety or security damage. Market growth is being driven by rising drone threats around military bases, airports, borders, energy assets, ports, and public events. Buyers are moving from basic jammers to integrated counter-UAS technologies that combine radar systems, RF sensors, electro-optical infrared, detection tracking, command and control, and real-time mitigation capabilities to address evolving aerial threats more effectively.

Key players in the market are Elbit Systems Ltd., HENSOLDT AG, Israel Aerospace Industries Ltd., Leonardo S.p.A., Lockheed Martin Corporation, Northrop Grumman Corporation, Rafael Advanced Defense Systems Ltd., and RTX Corporation. These companies offer integrated counter-UAS solutions, hard-kill interceptors, AI-enabled sensor technologies, high-power microwave solutions, and advanced software-led response architectures.

Download Free sample to learn more about this report.

COUNTER-UAS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 11.60 billion

- 2026 Market Size: USD 14.41 billion

- 2034 Forecast Market Size: USD 55.25 billion

- CAGR: 22.4% from 2026–2034

- North America dominated the counter-UAS market with a 31.03% share in 2025.

- The small commercial/Group 1–2 segment held the largest market share in 2025.

- RF jamming accounted for the largest share of the market by neutralization technology in 2025

North America

North America led the market in 2025, supported by strong investments in military base protection, homeland security, border surveillance, and critical infrastructure defense.

Europe

Europe accounted for 27.98% of the global market in 2025, driven by NATO rearmament efforts and increasing demand for layered counter-drone systems.

Asia Pacific

Asia Pacific is projected to grow at a CAGR of 19.6% through 2034, fueled by military modernization programs and rising border-security requirements across major economies.

U.S.

The market was valued at approximately USD 3.38 billion in 2025 and benefits from one of the world's most advanced and well-funded counter-drone ecosystems

Japan

The market reached around USD 0.27 billion in 2025, accounting for approximately 11.58% of Asia Pacific revenues, supported by growing air-base and critical infrastructure protection needs.

Read More

Counter-UAS MARKET TRENDS

AI-Enabled Layered Counter-UAS Architectures Drive Market Growth.

A major trend in the market is the shift from standalone jamming solutions and sensor-only systems toward integrated, AI-enabled architectures. Buyers increasingly prefer counter-UAS systems that combine radar, RF sensing, electro-optical infrared payloads, detection tracking, command and control, and multiple mitigation options within an operational interface. This shift is being driven by faster, smaller, and more coordinated drone threats, which need real-time classification and response rather than manual detection and delayed engagement. As hostile drones and swarm-style aerial threats become harder to counter with a single tool, demand is moving toward modular counter-UAS technologies capable of integrating with wider air-defense systems, military base-security networks, and critical-infrastructure protection platforms.

For instance, in December 2025, Lockheed Martin and Microsoft announced a collaboration to develop Sanctum, a next-generation Counter-UAS capability combining Lockheed Martin’s mission systems expertise with Microsoft cloud and AI technologies.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Drone-related Threats to Drive Market Growth

The primary driver of the market is the rapid increase in drone-related threats targeting military bases, borders, airports, ports, energy assets, and critical infrastructure. Low-cost unmanned aerial systems are now being used for surveillance, disruption, smuggling, and attack missions, creating urgent demand for layered counter-UAS systems. Buyers are therefore investing in advanced detection and mitigation technologies that combine radar, RF sensors, electro-optical infrared, detection tracking, command and control, and hard-kill or soft-kill response tools. This trend is fueling counter-UAS market growth, as unauthorized drone activities are no longer viewed as isolated security incidents but are increasingly utilized as persistent operational risks requiring continuous monitoring and rapid-response capabilities.

For instance, in December 2024, the U.S. Department of Defense stated that unmanned aerial systems pose an urgent and enduring threat to U.S. personnel, facilities, and overseas assets, while also becoming an increasing homeland security concern. The department’s strategy for Countering Unmanned Systems further aligned Counter-UAS efforts with the Joint Counter-Small UAS Office, Replicator 2 programs, and broader protection of critical installations and concentrated military forces.

MARKET RESTRAINTS

Legal Restrictions on Active Mitigation to Restrain Market Growth

A major restraint affecting the market is the legal restriction surrounding many active mitigation systems, especially RF jamming, GNSS jamming/spoofing, cyber takeover systems, and solutions that interfere with communications links. These restrictions limit deployment for airports, private infrastructure operators, local authorities, and some law enforcement agencies, thereby hindering the large-scale deployment of C-UAS systems. As a result, several buyers prioritized detection tracking, electro-optical infrared sensors, and command and control software ahead of full neutralization capability. This slows the adoption of complete C-UAS systems and pushes many customers toward passive monitoring or government-led response models instead of fully integrated C-UAS solutions.

MARKET OPPORTUNITIES

Growing Demand for Products in Homeland Security and Critical Infrastructure Creating Major Market Opportunities

A key opportunity in the market is the expanding demand beyond traditional defense applications into homeland security, airports, ports, energy assets, public venues, and critical infrastructure. These end-users increasingly need C-UAS solutions that provide early warning, detection, tracking, electro-optical infrared confirmation, command and control, and real-time integration with law enforcement before unauthorized drone activities disrupt operations. This opens room for scalable, modular counter-UAS systems that can be deployed without disrupting civilian airspace while still addressing the growing threat posed by drones around public and commercial assets.

MARKET CHALLENGES

Difficulty in Detecting Low-Emission and Small Drone Threats Challenges Market Growth

A major challenge in the market is that many small and low-emission unmanned aerial systems are hard to detect, classify, and neutralize in cluttered environments. Commercial drones, autonomous drones, and low-RF or dark drones can avoid basic RF-based systems, while birds, buildings, terrain, radio interference, and dense urban activity can create false alarms. This makes detection tracking, electro-optical infrared confirmation, and command and control integration more complex, especially when operators need real-time decisions against fast-moving aerial threats. However, the higher cost and operational complexity associated with these integrated solutions can slow adoption among smaller defense, airport, and law enforcement users.

Impact of Ongoing Conflicts

Rising Need to Protect Naval Vessels and Other Critical Assets Fuels Market Growth

The Russia-Ukraine War and Middle East conflicts have made drone threats a central defense-planning issue rather than a niche security threat. In Ukraine, the widespread deployment of low-cost unmanned aerial systems, FPV drones, loitering munitions, and battlefield reconnaissance drones has pushed armies toward layered Counter-UAS systems that combine detection, tracking, electronic warfare, command and control, and hard-kill options. In the Middle East, Houthis' one-way attack UAVs, Red Sea maritime attacks, and wider regional drone activity have increased demand for Counter-UAS solutions designed to protect naval vessels, ports, air bases, energy infrastructure, and other critical assets. These conflicts are driving substantial investment in advanced detection and mitigation technologies, especially systems that can respond in real time against hostile drones and saturation-style aerial threats.

For instance, in September 2024, NATO held its Counter-UAS Technical Interoperability Exercise in the Netherlands, where 450 participants from 19 Allied Nations and three Partner Nations, including Ukraine, tested more than 60 systems and technologies, including sensors, effectors, jammers, and threat drones, to improve allied ability to detect, identify, and neutralize malicious drone activity.

Segmentation Analysis

By Platform

Fixed Segment Dominated the Market Due to High-Value Site Protection Requirements

In terms of platform, the market is categorized into fixed, mobile & vehicle-mounted, portable, and naval/maritime.

The fixed segment dominated the global market in 2025, as most early-stage and high-value deployments are built around protecting static assets such as military bases, airfields, command centers, airports, ports, energy facilities, ammunition depots, and critical infrastructure. These sites require continuous coverage, integrated detection tracking, electro-optical infrared confirmation, command and control, and layered mitigation against unauthorized drone activities. Compared with portable and mobile systems, fixed counter-UAS systems carry higher contract values due to the inclusion of advanced radar systems, EO/IR cameras, electronic warfare, kinetic interceptors, software, installation, training, and lifecycle support.

The naval/maritime segment is expected to grow at the highest CAGR of 24.0% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Detection & Tracking Segment Dominated the Market Due to the Continuous Need for Tracking Potential Aerial Threats

On the basis of component, the market is classified into detection & tracking, C2/software/AI fusion, soft-kill mitigation, hard-kill mitigation, and services.

Detection & tracking dominated the market in 2025, as effective counter-drone operations start with the early identification and continuous tracking of potential aerial threats before mitigation measures can be authorized. This segment includes radar, RF detection, acoustic sensors, electro-optical infrared systems, sensor-fusion software, and advanced tracking tools that help operators to monitor and respond to drone threats in real time. Although buyers are increasingly procuring jammers, interceptors, and directed-energy systems, a strong detection tracking layer remains essential for enabling accurate threat assessment. As a result, the segment continues to form the operational foundation of most counter-UAS systems deployed across defense, airports, borders, critical infrastructure, and law enforcement applications.

The soft-kill mitigation segment consists of EW/jamming/ spoofing components, whereas Hard-kill mitigation consists of Kinetic interceptors and Directed energy/HPM.

The C2/software/AI fusion is expected to show the fastest growth, registering a CAGR of 22.4% over the forecast period.

By Threat Class

Small Commercial/Group 1–2 Segment Dominated the Market due to its Widespread Availability

On the basis of threat class, the market is classified into small commercial/Group 1-2, Tactical UAS/Group 3, loitering munitions, and drone swarms.

The small commercial/Group 1–2 segment dominated the market in 2025, as these drones are cheap, widely available, easy to modify, and difficult to differentiate from harmless civilian drone activity in crowded airspace. These drones are frequently used for surveillance, smuggling, payload delivery, battlefield reconnaissance, and disruption around military bases, airports, borders, prisons, ports, and public events. As a result, most buyers first prioritize C-UAS systems that can detect, classify, track, and respond to small drone threats in real time. This has strengthened demand for RF sensing capabilities, electro-optical infrared, detection tracking, and command and control layers.

Drone swarms are expected to register a CAGR of 26.1% over the forecast period.

By Neutralization Technology

RF Jamming Segment Dominated the Market, Driven by its Faster Deployment

On the basis of neutralization technology, the market is classified into RF jamming, GNSS jamming/spoofing, cyber takeover/protocol exploitation, kinetic interceptors, directed-energy lasers, high-power microwave, net/capture systems, and passive protection.

RF jamming held the largest Counter-UAS market share in 2025, as it is one of the most widely deployable types of C-UAS systems that are used to interrupt small commercial drones and Group 1–2 unmanned aerial systems. Most low-cost drone threats still depend on RF links for command, control, telemetry, or video transmission, making RF jamming a logical first-response layer for military bases, borders, airports, prisons, ports, and critical infrastructure. Compared with kinetic interceptors or directed-energy systems, RF jamming is faster to deploy, lower in cost per engagement, and easier to integrate into layered C-UAS systems with detection tracking, command and control, and real-time operator workflows.

High-power microwave is expected to register a CAGR of 31.7% over the forecast period.

By Application

Military Base & Force Protection Segment Dominated the Market Due to Rising Defense Needs

By application, the market is divided into military base & force protection, battlefield/forward tactical protection, critical infrastructure, and others.

Military base & force protection held the largest market share in 2025, as defense organizations continue to represent the largest and most urgent buyers of layered counter-drone capabilities. Air bases, command centers, ammunition depots, radar sites, forward operating locations, naval bases, and troop concentrations face direct exposure to drone threats, loitering munitions, and small unmanned aerial systems used for surveillance, targeting, and attack operations. As a result, persistent detection and tracking capabilities, electro-optical/infrared confirmation systems, command-and-control, and real-time mitigation technologies have become operational necessities for modern military environments. Compared with civilian or commercial applications, military deployments usually require fuller Counter-UAS systems with sensors, software, jammers, interceptors, training, and sustainment, which supports the segment’s leading market share.

The critical infrastructure segment is expected to register a CAGR of 20.9% over the forecast period.

By End User

High-Frequency Exposure of Military Operations to Evolving Drone Threats Boosted Defense & Military Forces Segment Growth

Based on end user, the market is segmented into defense & military forces, Homeland security & border agencies, airport/critical infrastructure operators, and others.

Defense & military forces held the largest share of the market in 2025 due to the direct and high-frequency exposure of military operations to evolving drone threats, including small commercial drones and FPV systems to tactical UAS, loitering munitions, and swarm-style aerial threats. Military users require full-layer counter UAS systems, including detection tracking, electro-optical infrared confirmation, command and control, RF jamming, kinetic interceptors, and real-time response capability. This makes defense procurement larger and more system-heavy than civil use cases, especially for air bases, naval bases, forward operating locations, border posts, ammunition depots, command centers, and force concentrations.

The homeland security & border agencies segment is expected to register a CAGR of 23.2% over the forecast period.

Counter-UAS Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Middle East, and the Rest of the World.

North America

North America Counter-UAS Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the largest market share and is anticipated to grow at a CAGR of 16.1% during the study period. The U.S. has one of the most structured and well-funded counter-drone ecosystems globally. Demand is supported by military base protection, homeland security, border surveillance, airport safety, critical infrastructure protection, and rapid testing of advanced C-UAS technologies. The region is also ahead in integrating detection tracking, electro-optical infrared, command and control, RF mitigation, kinetic interceptors, and real-time response architectures into layered C-UAS systems. Strong involvement from companies such as Lockheed Martin, RTX/Raytheon, Northrop Grumman, Anduril, L3Harris, and other U.S.-based defense firms further strengthens the region’s leading position.

U.S. Counter-UAS Market

Based on the strong contribution of North America to the market and the dominance of the U.S. within the region, the U.S. market stood at around USD 3.38 billion in 2025, growing at a CAGR of 15.9%.

Europe

Europe held around 27.98% share of the global market in 2025, supported by the Russia-Ukraine war, NATO rearmament, and the need to protect air bases, ammunition depots, ports, borders, command sites, and forward-deployed forces. The region is moving from basic jamming toward layered C-UAS systems that combine detection tracking, electro-optical infrared sensors, command and control, electronic warfare, kinetic interceptors, and real-time response against hostile drones and loitering munitions. SIPRI reported that Europe’s military expenditure rose 14.00% in 2025 to USD 864.00 billion, while NATO’s 2024 C-UAS interoperability exercise tested more than 60 systems and technologies with participants from 19 Allied nations and three Partner nations, including Ukraine.

Ukraine Counter-UAS Market

France market reached approximately USD 0.47 billion in 2025, equivalent to around 14.59% of Europe's revenues.

U.K. Counter-UAS Market

The U.K. market stood at around USD 0.38 billion in 2025, representing roughly 11.85% of Europe's revenues.

Asia Pacific

Asia Pacific is anticipated to grow at a CAGR of 19.6% over the forecast period. Region growth is attributed to China’s military modernization, India’s border-security needs, Japan and South Korea’s air-base protection requirements, Taiwan’s island-defense posture, and Australia’s increasing focus on counter-drone capability. The region’s demand is shifting toward mobile, naval, and AI-enabled C-UAS technologies as buyers prepare for drone threats across land borders, ports, naval bases, island facilities, airports, and critical infrastructure. According to SIPRI, military expenditure across Asia and Oceania reached USD 681.00 billion in 2025, representing an increase of 8.10%. Within the region, in 2025, China accounted for USD 336.00 billion, India for USD 92.10 billion, Japan for USD 62.20 billion, and Taiwan for USD 18.20 billion in defense spending.

China Counter-UAS Market

The Chinese market revenues stood at around USD 0.82 billion in 2025, representing roughly 35.42% of the global sales.

Japan Counter-UAS Market

The Japanese market in 2025 stood at around USD 0.27 billion, accounting for roughly 11.58% of Asia Pacific revenues.

Middle East

The Middle East is anticipated to grow at a CAGR of 19.7% over the forecast period. The Middle East remains one of the most operationally visible Counter-UAS regions due to repeated drone, missile, loitering munition, and maritime threats across the Gulf, Red Sea, Israel, Türkiye, and wider conflict zones. Demand is strongly linked to military bases, oil & gas assets, airports, ports, desalination plants, border posts, and naval facilities. The region is moving toward integrated C-UAS solutions that combine detection tracking, command and control, RF/GNSS disruption, hard-kill interceptors, directed energy, and high-power microwave options. According to SIPRI, Middle East military expenditure reached USD 218.00 billion in 2025. In addition, CENTCOM reported strikes against a Houthi UAV ground-control station and 10 one-way UAVs assessed as threats to merchant vessels and U.S. Navy ships.

Saudi Arabia Counter-UAS Market

The Saudi Arabia market stood at around USD 0.58 billion in 2025, representing roughly 29.26% of the global sales.

Rest of the World

The rest of the World (Africa and Latin America) holds a comparatively smaller market share, but it is expected to grow at a CAGR of 23.6% during the forecast period. Growth in Africa is expected to grow faster due to Sahel-region instability, rising North African defense demand, insurgency-linked drone risks, and coastal infrastructure exposure. Meanwhile, Latin America is witnessing growing demand driven by border security threats, organized crime response, ports, and critical infrastructure. SIPRI reported that Africa’s military spending rose by 8.50% in 2025, reaching USD 58.20 billion.

Latin America Counter-UAS Market

The market in Latin America reached around USD 0.19 billion in 2025, accounting for roughly 41.74% of Rest of the World Counter-UAS revenues.

Africa Counter-UAS Market

Africa market stood at around USD 0.27 billion in 2025 and is expected to reach USD 2.10 billion by 2034.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Focus on Innovations to Meet Various Defense Needs

The global market is led by players such as Elbit Systems Ltd., HENSOLDT AG, Israel Aerospace Industries Ltd., Leonardo S.p.A., Lockheed Martin Corporation, Northrop Grumman Corporation, Rafael Advanced Defense Systems Ltd., and RTX Corporation. Competition is shifting from standalone jammers to integrated Counter-UAS systems that combine detection tracking, electro-optical infrared sensors, RF detection, command and control, and real-time protection against hostile drones and wider aerial threats.

Key players are strengthening their market positions through investments in AI-enabled software, hard-kill interceptors, RF mitigation, sensor fusion, and modular C-UAS solutions designed for defense, law enforcement, airport security, and critical infrastructure protection applications. Lockheed Martin is focusing on the development of modular counter-drone architectures, while RTX/Raytheon continues to expand its Coyote interceptor and KuRFS-linked detect-and-defeat systems, whereas Anduril and DroneShield are expanding their presence through software-led defense platforms and electronic-warfare-based advanced counter-drone technologies.

LIST OF KEY COUNTER-UAS COMPANIES PROFILED

- Anduril Industries, Inc. (U.S.)

- ASELSAN A.Ş. (Türkiye)

- Dedrone by Axon (U.S.)

- D-Fend Solutions AD Ltd. (Israel)

- DroneShield Limited (Australia)

- Elbit Systems Ltd. (Israel)

- HENSOLDT AG (Germany)

- Israel Aerospace Industries Ltd. (Israel)

- Leonardo S.p.A. (Italy)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- QinetiQ Group plc (U.K.)

- Rafael Advanced Defense Systems Ltd. (Israel)

- RTX Corporation (U.S.)

- Saab AB (Sweden)

- SRC, Inc. (U.S.)

- Teledyne FLIR LLC (U.S.)

- Thales Group (France)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Australia issued an initial rolling wave of approximately USD 11.09 million in contracts to 11 vendors under Project LAND 156 to rapidly introduce at least 120 threat detectors and drone-defeating technologies into ADF service.

- October 2024: Anduril Industries secured a USD 249.98 million U.S. Department of Defense contract to deliver more than 500 Roadrunner-M interceptors and additional Pulsar electronic warfare systems for counter-drone protection of U.S. forces.

- October 2024: The U.S. Marine Corps awarded Invariant Corp. and Anduril Federal a combined USD 400.00 million IDIQ contract for integration and delivery of a Counter-Unmanned Aircraft System Engagement System, including associated hardware, software, and services.

- February 2024: Leonardo was awarded a contract by Public Services and Procurement Canada to supply Falcon Shield C-UAS systems to the Canadian Armed Forces, with a 10-year sustainment package and options for additional equipment and capability upgrades.

- January 2024: The U.S. Army awarded RTX Corporation a USD 75.00 million contract for the production of 600 Coyote 2C interceptors in direct support of the U.S. counter-unmanned aircraft systems mission.

- January 2024: EDGE Group announced a contract with the UAE Ministry of Defence to deliver multi-layered counter-UAS systems, including SKYSHIELD C-UAS and NAVCONTROL-G systems for critical infrastructure and border protection.

- July 2023: DroneShield received a USD 33.00 million order from a U.S. Government agency for counter-UAS equipment and multi-year services, marking one of its largest contract wins at the time.

- November 2022: The U.S. State Department approved a possible USD 1.00 billion FMS to Qatar for 10 Fixed Site-Low, Slow, Small UAS Integrated Defeat Systems, including 200 Coyote Block 2 interceptors, Ku-band radars, EO/IR, EW systems, FAAD C2, training, software, and sustainment.

REPORT COVERAGE

The global counter-UAS market analysis provides an in-depth study of market size, market segmentation, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market during the forecast period. It offers information on the technological advances, new product launches, key industry developments, and details on strategic partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of the market key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 22.4% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation

|

By Platform

|

|

By Component

|

|

|

By Threat Class

|

|

|

By Neutralization Technology

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 11.60 billion in 2025 and is projected to reach USD 55.25 billion by 2034.

In 2025, the North American market value stood at USD 3.60 billion.

The market is expected to exhibit a CAGR of 22.4% during the forecast period.

By platform, the fixed segment led the market.

Rising drone-related threats are the key factor driving market growth.

Key players in the include Elbit Systems Ltd., HENSOLDT AG, Israel Aerospace Industries Ltd., Leonardo S.p.A., Lockheed Martin Corporation, Northrop Grumman Corporation, Rafael Advanced Defense Systems Ltd., and RTX Corporation.

North America dominates the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us