Critical Infrastructure Anti-Drone Systems Market Size, Share & Industry Analysis, By Deployment (Fixed/Permanent Installation, Rapidly Deployable/Mobile, and Vehicle-Mounted), By Detection Sensor (RF detection/DF, Radar, EO/IR, Acoustic, and Multi-sensor Fusion), By Coverage (Short Range (0-3 Km), Medium Range (3-10 Km), Long Range (10-30 Km), and Wide-area/Extended (30-60 Km)), By Vertical (Energy & Utilities, Oil & Gas, Transportation, Government & Public Safety, Defense, and Others), and Regional Forecast, 2026-2034

Critical Infrastructure Anti-Drone Systems Market Size and Future Outlook

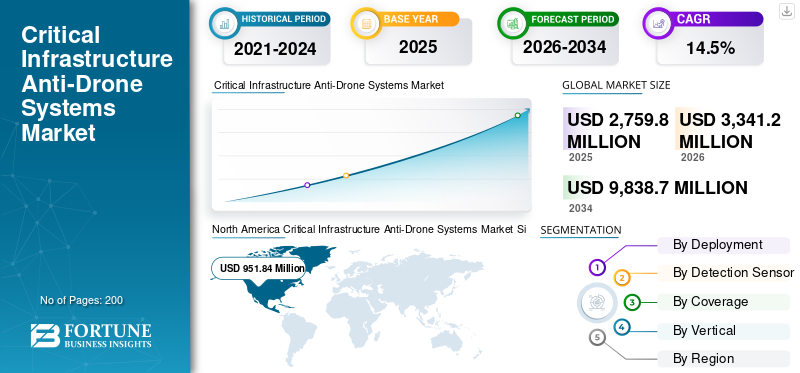

The global critical infrastructure anti-drone systems market size was valued at USD 2,759.8 million in 2025. The market is projected to grow from USD 3,341.2 million in 2026 to USD 9,838.7 million by 2034, exhibiting a CAGR of 14.5% during the forecast period. North America dominated the critical infrastructure anti-drone systems market with a market share of 34.49% in 2025.

The critical infrastructure anti-drone systems market focuses on technologies protecting vital assets such as power plants, airports, refineries, ports, and government facilities from unauthorized drones. These systems employ radar, radio frequency detection, electro-optical infrared cameras, acoustic sensors, and AI-driven analytics for real-time threat identification, tracking, and neutralization through jamming, kinetic interception, or cyber takeover. Driven by rising rogue drone incursions for espionage, smuggling, and sabotage, the sector sees rapid adoption in defense alongside expanding civilian use for smart cities and events. Key players integrate multi-layered solutions emphasizing non-kinetic methods to minimize collateral risks in urban settings.

Key players including BAE Systems, RTX/Raytheon, Thales, Rheinmetall, Leonardo, Saab, Lockheed Martin, Northrop Grumman, Diehl Defence, and Elbit Systems are expanding C-UAS portfolios through sensor fusion, autonomy, and layered defeat options. Growth is driven by airport, energy, and government infrastructure demand, plus recurring software, upgrades, and sustainment contracts.

Download Free sample to learn more about this report.

CRITICAL INFRASTRUCTURE ANTI-DRONE SYSTEMS MARKET TRENDS

Rapid Adoption of Advanced Detection Technologies is Shaping Evolution in Market

The market shows strong momentum from increasing unauthorized drone activities near airports, military bases, and energy sites. Defense modernization and investments in electronic warfare boost deployment of counter-unmanned aerial systems using radar, radio frequency, and electro-optical sensors. Artificial intelligence and machine learning improve threat detection accuracy and response times. Smart city surveillance and border security drive scalable solutions across defense and civilian sectors. Multi-layered systems for urban high-risk areas enhance airspace safety and threat management.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Security Threats to Key Assets Driving Market Growth

Frequent rogue drone incursions at airports and bases heighten demand for robust protection. Military and defense agencies increasingly adopt anti-drone solutions amid illegal activities including smuggling and terrorism. Government regulations on no-fly zones and airspace security mandate counter-systems. Integration of AI for real-time tracking addresses evolving aerial risks to power plants, refineries, and ports. Heightened vigilance against espionage and sabotage propels widespread implementation.

MARKET RESTRAINTS

Substantial Capital and Integration Demands Hinders Market Growth

High initial investments for equipment and maintenance limit uptake by smaller organizations. Complex merging with existing security networks requires specialized skills. Regulatory hurdles on interference technologies restrict civilian use. Lack of uniform global standards complicates procurement and deployment. These factors slow expansion in non-defense settings.

MARKET OPPORTUNITIES

Expansion into Civilian and Urban Sectors to Create Lucrative Opportunities

Opportunities emerge in civilian applications such as commercial aviation, energy utilities, and public events needing intellectual property safeguards. Modular portable systems suit mid-sized facilities and emerging smart cities. Public-private partnerships foster adoption for stadiums, medical centers, and arenas. Non-kinetic radio frequency cyber solutions enable safe mitigation without collateral damage. Policy evolution supports tools for state and local protectors of infrastructure skies.

MARKET CHALLENGES

Countering Advanced and Swarm Threats to Challenge Market Growth

Evolving drone capabilities including stealth and swarm formations challenge current detection limits. Urban signal clutter triggers false alarms, while networked systems face hacking risks. Distinguishing threats from authorized operations demands agile, adaptable tech. Dense areas amplify collision risks from operator errors or malfunctions. Ongoing innovation is essential for resilient urban airspace defense.

Segmentation Analysis

By Deployment

Fixed/Permanent Installation Segment to Dominate Due to Nonstop Site Protection Needs

Based on deployment, the market is segmented into fixed/permanent installation, rapidly deployable/mobile, and vehicle-mounted.

The fixed/permanent installation segment is anticipated to account for the largest critical infrastructure anti-drone systems market share. Fixed installations are chosen for airports, substations, refineries, and data centers needing 24/7 coverage. Buyers prioritize multi-sensor stacks, hardened mounts, SOC integration, and predictable uptime with long-term sustainment contracts.

The rapidly deployable/mobile segment is anticipated to rise with a CAGR of 15.3% over the forecast period.

By Detection Sensor

RF Detection/DF Segment Led Due to Fast Deployment and Low-Cost Detection Value

Based on detection sensor, the market is segmented into RF detection/DF, radar, EO/IR, acoustic, and multi-sensor fusion.

In 2025, the RF detection/DF segment dominated the global market. RF detection/DF demand stays strong as it quickly spots common drones and can help locate operators. It’s favored for layered architectures, rapid deployment, and cost-effective scaling across many sites.

The multi-sensor fusion segment is projected to grow at a CAGR of 15.9% over the forecast period.

By Coverage

Short Range (0–3 Km) Segment to Dominate Due to Perimeter Intrusion Risks

Based on coverage, the market is segmented into short range (0-3 Km), medium range (3-10 Km), long range (10-30 Km), and wide-area/extended (30-60 Km).

The short range (0-3 Km) segment is anticipated to witness a dominating market share over the forecast period. Short-range systems dominate as most threats occur near the perimeter. They’re easier to permit, cheaper to deploy, and effective for facilities needing immediate alerts, fast handoff, and close-in mitigation options.

The wide-area/extended (30-60 Km) segment is projected to grow at a high CAGR of 15.7% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Vertical

Energy & Utilities Segment Dominated Due to High-Consequence Outage Risk

Based on vertical, the market is segmented into energy & utilities, oil & gas, transportation, government & public safety, defense, and others.

The energy & utilities segment dominated the segmental market share. Energy and utilities drive demand as drones can disrupt substations, plants, and transmission nodes with outsized impact. Operators invest in reliable detection, low false alarms, and resilient monitoring tied to incident response.

In addition, transportation segment is projected to grow at a CAGR of 15.3% during the study period.

Critical Infrastructure Anti-Drone Systems Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and rest of the world.

North America

North America Critical Infrastructure Anti-Drone Systems Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 777.16 million, and also maintained the leading share in 2025, with USD 951.84 million. North America is scaling fixed-site and mobile counter-drone deployments at airports, energy assets, and government facilities. Strong budgets, fast operational feedback loops, and integrator capacity accelerate upgrades toward sensor fusion and managed monitoring.

U.S. Critical Infrastructure Anti-Drone Systems Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1,051.0 million in 2026, accounting for roughly 14.1% of global sales. The U.S. demand is anchored by airports, federal facilities, defense-adjacent infrastructure, and energy sites. Programs emphasize layered detection, operator location, and scalable monitoring, with strong interest in fusion software and recurring support.

Europe

Europe is estimated to reach USD 960.7 million in 2026 and secure the position of second largest region in the market. Europe’s demand is led by airport protection, critical energy nodes, and large public events. Buyers prioritize compliant, non-kinetic options, integrated command-and-control, and interoperable systems that can work across different national rules.

U.K. Critical Infrastructure Anti-Drone Systems Market

The U.K. market growth is estimated at around USD 152.5 million in 2026, representing roughly 14.2% CAGR over the forecast period. The U.K. demand centers on airports, city-critical nodes, and major event protection. Operators favor integrated sensor fusion, rapid-response mobile kits, and compliant mitigation, increasingly tied into security operations centers and policing workflows.

Germany Critical Infrastructure Anti-Drone Systems Market

Germany’s market is projected to reach approximately USD 187.8 million in 2026. Germany’s demand is driven by industrial sites, transport hubs, and power infrastructure. Buyers prioritize high-reliability detection in clutter, precise classification, and integration with existing security systems rather than aggressive mitigation methods.

Asia Pacific

Asia Pacific is projected to record a growth rate of 15.1% during the forecast period, which is the third highest among all regions, and is set to reach a valuation of USD 859.8 million by 2026. Asia Pacific’s demand is expanding across airports, ports, utilities, and industrial zones. Adoption is pushed by high site density, growing drone activity, and government-led modernization, with strong pull for scalable multi-site deployments.

Japan Critical Infrastructure Anti-Drone Systems Market

The Japan market share is estimated at around USD 157.6 million in 2026, accounting for roughly 15.7% of CAGR during the forecast period. Japan’s demand is shaped by airport disruption risk, dense urban environments, and strict operational controls. Priority is on detection accuracy, low false alarms, and seamless integration into security command centers.

China Critical Infrastructure Anti-Drone Systems Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 306.7 million. China’s demand is fueled by airports, ports, utilities, and industrial parks at massive scale. Procurement favors networked, multi-site systems and high production capacity, with rapid iteration toward automation and autonomy.

India Critical Infrastructure Anti-Drone Systems Market

The India market in 2026 is estimated at around USD 117.4 million. India’s demand is accelerating around military installations, airports, and strategic infrastructure. Buyers prefer layered, autonomous systems and faster deployment cycles, with increasing domestic development and integration to meet scale and urgency.

Rest of the World

The rest of the world include Middle East & Africa and Latin America. These regions are expected to witness moderate growth in this market during the forecast period. The Middle East & Africa and Latin America market is set to reach a valuation of USD 250.5 million and USD 119.4 million each in 2026. Rest of the world demand concentrates in high-value assets such as oil & gas, ports, VIP zones, and power sites. Buyers want rapid deployment, ruggedized systems, and services-led models where local integration skills are limited.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players to Focus on R&D to Strengthen their Market Position

Key players in the critical infrastructure anti-drone systems market are making substantial investments in research and development to broaden their product portfolios, which is expected to support further market growth. Companies are also pursuing a range of strategic initiatives to strengthen their market presence, including product launches, contracts, mergers and acquisitions, increased investments, and partnerships with other organizations. To remain competitive in a growing and increasingly challenging market, participants in the critical infrastructure anti-drone industry must provide cost-effective solutions. One of the main strategies adopted by manufacturers is local production, which helps reduce operational costs, improve customer value, and strengthen their position in the market. In recent years, the anti-drone sector has delivered major advantages to the defense industry.

LIST OF KEY CRITICAL INFRASTRUCTURE ANTI-DRONE SYSTEMS COMPANIES PROFILED

- BAE Systems (U.K.)

- Diehl Defence (Germany)

- RTX / Raytheon (U.S.)

- Thales Group (France)

- Rheinmetall (Germany)

- Leonardo (Italy)

- Saab (Sweden)

- Lockheed Martin (U.S.)

- Northrop Grumman (U.S.)

- Elbit Systems (Israel)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Sigma Advanced Systems has signed a long-term strategic partnership with Indrajaal Drone Defence, under which Sigma will provide key radar and electronic warfare subsystems that will be integrated into Indrajaal’s counter-drone solutions.

- January 2026: India’s Ministry of Defence has awarded Indrajaal (Hyderabad) a USD 11 million contract to deliver multi-layered autonomous anti-drone systems to secure selected Indian Army and Indian Navy sites.

- December 2025: DroneShield has won an USD 8.2 million order placed via a regional reseller to supply counter-drone equipment and support services to a Western military customer, including handheld systems, accessories, spares kits, and ongoing software updates.

- June 2025: Ondas Holdings announced a strategic partnership between its subsidiary American Robotics and Mistral Inc. to collaborate on business development and defense contracting efforts linked to autonomous drone and industrial wireless solutions.

- April 2022: Amentum has received a five-year contract from the DHS S&T Directorate, worth up to USD 260 million, to develop and field emerging counter-unmanned systems capabilities and prototypes, awarded through the DoD IAC multiple-award contract vehicle.

REPORT COVERAGE

This critical infrastructure anti-drone systems market research report offers a detailed analysis of emerging trends and rapidly adopted technologies in the industry across key regions. The report outlines key drivers of market growth and challenges to expansion, delivering a detailed overview of the industry landscape. The study highlights recent advancements to boost industry insights and support stakeholders in making well-informed decisions.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.5% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Deployment, By Detection Sensor, By Coverage, By Vertical, and Region |

| By Deployment |

|

| By Detection Sensor |

|

| By Coverage |

|

| By Vertical |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2,759.8 million in 2025 and is projected to reach USD 9,838.7 million by 2034.

In 2025, North Americas market value stood at USD 951.84 million.

The market is expected to exhibit a CAGR of 14.5% during the forecast period.

By fixed/permanent installation segment is expected to dominate the market.

Rising security threats to key assets to drive the market growth.

BAE Systems (U.K.), Diehl Defence (Germany), RTX / Raytheon (U.S.), Thales Group (France), Rheinmetall (Germany), and Leonardo (Italy) are few major players in the global market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us