Cyber Warfare Market Size, Share & Industry Analysis, By Warfare Type (Offensive & Defensive Cyber Warfare), By Capability (Cyber Espionage & Reconnaissance, Cyber Attack & Sabotage, Psychological & Information Operations, Command & Control Warfare, & Others), By Solution (Hardware, Software, & Managed Services), By Deployment Mode (On-Premise/On-Platform, Cloud-Based, Hybrid, and Edge/Tactical), By Operational Level (Strategic, Operational, & Tactical), By Target Environment (Enterprise/Government IT, Industrial Control System, & Others), By Revenue Model, and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

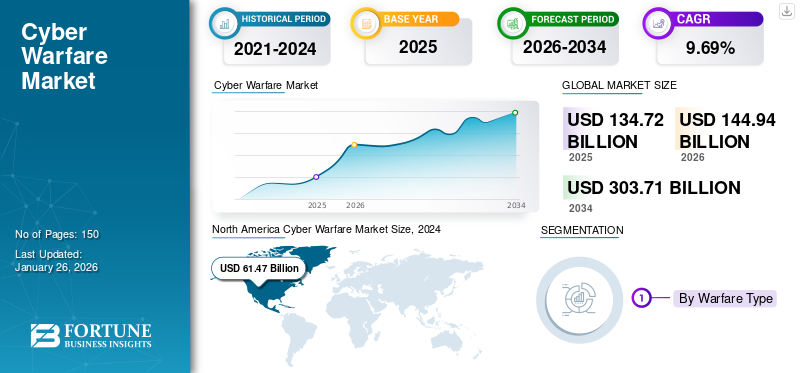

The global cyber warfare market size was valued at USD 134.72 Billion in 2025. The market is projected to grow from USD 144.94 Billion in 2026 to USD 303.71 Billion by 2034, exhibiting a CAGR of 9.69% during the forecast period. North America dominated the cyber warfare market with a market share of 48.22% in 2025.

Cyber warfare is a key area of contemporary defense policy, addressing both defense and offense in terms of protecting countries against cyber threats that can target critical digital infrastructure, governments, and military command systems. The marketplace is generally categorized into offensive cyber warfare (OCW), which entails focused attacks, sabotage, and intelligence, and defensive cyber warfare (DCW), which entails the protection of assets, resilience maintenance, and facilitation of continuity of operations.

Capabilities are extensive across cyber espionage, C2 (command and control) warfare, psychological and information operations, and cross-domain support that bridge tactical and strategic functions. Deployment structures range from on-premise defense platforms to cloud-based protection and tactical edge solutions based on the level of operations. At the same time, streams of revenue consist of GovCloud SaaS platforms and conventional enterprise contracts. Support for the market comes in the form of increasing digitalization in defense and government IT networks, prompting the need to secure industrial control systems, weapons platforms, and telecommunication infrastructure.

Major contenders including Lockheed Martin, Northrop Grumman, Raytheon Technologies, BAE Systems, and Thales are using technologies such as artificial intelligence and machine learning, quantum-resistant encryption, and cloud-native cyber defense solutions to solidify their footholds, with governments globally stepping up investments in modernization initiatives in incident response to emerging cyber threats.

Download Free sample to learn more about this report.

Cyber Warfare Market Key Takeaways

- 2025 Market Size: USD 134.72 billion

- 2026 Market Size: USD 144.94 billion

- 2034 Forecast Market Size: USD 303.71 billion

- CAGR: 9.69% from 2026–2034

- North America dominated the cyber warfare market with a 48.22% share in 2025.

- Command & Control (C2) Warfare is expected to contribute 68.26% of the market in 2026.

- Software held a 34.22% share in 2024.

North America

North America was valued at USD 64.97 Billion in 2025 and is projected to reach USD 69.61 Billion in 2026, supported by strong defense spending and advanced cybersecurity capabilities.

Europe

Europe is projected to reach USD 4.16 Billion in 2026, driven by increasing investments in cyber defense infrastructure and growing geopolitical tensions.

Asia Pacific

Asia Pacific is projected to witness substantial growth, supported by rising investments in cyber security and expanding digital infrastructure across major economies.

U.S.

The U.S. market is projected to reach USD 66.52 Billion in 2026, owing to significant investments in AI-powered cybersecurity and defense modernization programs.

Japan

The Japan market is projected to reach USD 2.87 Billion in 2026, supported by increasing focus on cyber resilience and national security initiatives.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increasing Cyber Attacks Leading to High Growth Of Appropriate Counter Cyber Warfare

The global cyber warfare market growth is being driven by an escalation in the intensity and sophistication of cyber-attacks and growing governmental spends and public–private partnerships. As the geopolitical competition and online skirmishes escalate, nations increase spending on robust cyber capabilities especially for defense purposes while embracing proactive policies and regulations that require increased cybersecurity preparedness.

- In June 2025 – Italy’s Leonardo announced the acquisition of a European cybersecurity company to bolster its multi-domain warfare capabilities, highlighting the critical role of cyber defense specialists in modern military ecosystems.

MARKET RESTRAINTS

Requirement for Highly Skilled Labor to Constrain Market Growth

Though the cyber warfare market is booming, its growth is restrained by the persistent skills gap and limited progress in real-time information sharing among stakeholders. The shortage of cybersecurity professionals capable of addressing evolving threats remains a major bottleneck across both public and private sectors. Likewise, the reluctance or inability to share threat intelligence swiftly reduces collective responsiveness to emerging attacks.

- In April 2025, the U.S. Congress debated renewal of protections under the Cybersecurity Information Sharing Act (CISA), with the WIMWAG bill aiming to extend provisions but facing privacy and implementation concerns

MARKET OPPORTUNITIES

Growth Opportunities through AI-Powered Systems and Solutions

The cyber warfare market presents substantial growth opportunities, driven by the proliferation of AI, machine learning, quantum technologies, and expanding digital surfaces, including IoT, cloud platforms, and hybrid warfare domains. Governments and enterprises alike are increasingly focused on safeguarding critical infrastructure, national assets, and civilian systems, accelerating demand for advanced cyber defense and offensive tools.

AI-powered systems offer transformative potential capable of real-time anomaly detection, orchestrated threat response, and predictive incident prevention. Meanwhile, deepfake and disinformation operations, cloud vulnerabilities, and IoT exposure create niches for tailored cybersecurity solutions.

- In March 2025, Accenture acquired CyberCX for over USD 1 billion, combining AI-driven defense tools with regional expertise to strengthen Australia’s national cybersecurity posture. This demonstrates the lucrative demand and strategic value of sophisticated cyber defense integration.

CYBER WARFARE MARKET TRENDS

Shift to Smart and Emerging Technologies to Act as a Major Market Trend

Technology continues to reshape cyber warfare tactics through AI, machine learning, quantum computing, autonomous systems, and advanced data synthesis tools. AI-driven automation increasingly powers both offense and defense enabling adaptive malware, faster threat detection, and autonomous containment. Concurrently, the impending quantum era threatens existing encryption, while opening avenues for quantum-resilient cryptography and defense systems.

Furthermore, commercial tech firms are entering the defense domain. Legacy cybersecurity firms such as Nokia, Oracle, and Dell are now deploying battlefield-grade data systems leveraging 5G, cloud analytics, and ruggedized hardware for real-time intelligence operations. This trend amplifies the technology arms race across cyber warfare.

- In February 2025, Nokia, Oracle, and Dell introduced military-grade battlefield data solutions, underscoring the trend of tech giants supplying next-generation cyber warfare infrastructure.

- In July 2024 – Ukraine deployed AI-powered drone swarms for reconnaissance and strikes, showcasing how emergent technologies redefine battlefield cyber-kinetic integration

MARKET CHALLENGES

High Attribution of Attacks Present Threats to Market Growth

One of the key challenges in the cyber warfare market is attribution of attacks and the difficulty of accurately identifying perpetrators behind cyber incidents. Unlike conventional warfare, cyber-attacks often originate from anonymous networks, proxies, or state-sponsored groups operating under covert channels, making retaliation and policy enforcement highly complex. This ambiguity undermines international trust and delays coordinated responses. Moreover, the blurred line between criminal cyber activity and state-sponsored operations raises challenges in setting legal and ethical frameworks for deterrence. The lack of standardized global norms for cyber conflict escalates risks of misinterpretation and unintended escalation among nation states.

Download Free sample to learn more about this report.

Segmentation Analysis

By Warfare Type

Rising State-Sponsored Threats Drive Growth of Defensive Cyber Warfare (DCW)

On the basis of warfare type, the market is classified into offensive cyber warfare (OCW) and defensive cyber warfare (DCW).

The increasing sophistication of cyber adversaries, particularly state-sponsored actors, has amplified the demand for defensive cyber warfare. Governments and enterprises are prioritizing defensive measures to shield critical infrastructure, sensitive data, and military assets from disruptive attacks. Defensive capabilities encompass advanced firewalls, intrusion detection, and AI-powered anomaly detection systems, all tailored to mitigate both kinetic and non-kinetic attacks. The rise of hybrid warfare where cyber operations accompany conventional military action further cements the need for comprehensive defensive solutions. Nations are also formalizing defense doctrines to position cyber defense as a national security imperative, underscoring the strategic shift toward resilience.

- For instance, in May 2024, the U.S. Cyber Command launched its “Persistent Engagement” strategy, reinforcing defensive postures by conducting continuous monitoring of foreign cyber actors and enhancing resilience across critical U.S. defense networks.

By Capability

Expanding Digital Battlefields Fueled Adoption of Command & Control (C2) Warfare Segment

In terms of capability, the market is categorized into cyber espionage & reconnaissance, cyber- attack & sabotage, psychological & information operations, command & control (c2) warfare, and cross-domain support.

The command & control (C2) warfare segment is expected to lead the market, contributing 68.26% globally in 2026. The segment is expected to maintain its leadership with a share of above 25% in the year 2025. As the militaries get modernized, the importance of C2 warfare has amplified ever since. Through C2, forces can be coordinated across domains while integrating real-time data, secure communications, and decision-support tools. With threats spanning space, cyber, and land-based domains, seamless systems integration for commanding becomes crucial. Cyber-enabled C2 systems are solvent in providing increased battlefield awareness, faster decision-making, and coordinated responses against aggressors. The second generation of AI-enabled C2 tools now allows automated prioritization of threats and on-the-fly deployment of countermeasures. Relying on digital C2 systems also means opening a new set of vulnerabilities, with the protection of these systems becoming foremost. The merging of C2 with cyber warfare provides the operational backbone in which future combat shall take place.

- In June 2025, NATO launched its Allied Future Surveillance program, integrating AI-powered C2 systems to enhance multinational coordination, particularly in hybrid cyber and electronic warfare

To know how our report can help streamline your business, Speak to Analyst

By Solution

Military Digitization Accelerated Demand for Software Solutions

Based on the solution, the market is segmented into hardware, software, and managed services.

The software segment held the dominating position in 2024 by holding a share of 34.22%. The transition to digital-first methods of waging war has placed software solutions at the core of cyber warfare ecosystems. From malware analysis platforms to advanced encryption suites, software provides the scalability and adaptability for cyber defense and operations. Custom-developed software applications for situational awareness, cyber threat modeling, and penetration testing are being procured by militaries. Software solutions are also heavily utilized for the simulation of enemy tactics, providing proactive defensive mechanisms to the armed forces. In addition, the modularity of software solutions allows for swift updates to address emerging vulnerabilities at a quicker pace than hardware cycles. This establishes a sturdy market for niche software vendors as well as defense contractors.

- February 2025 – Lockheed Martin announced a new AI-driven software suite designed to simulate adversarial cyber-attacks, helping defense organizations enhance training and resilience across mission-critical networks.

By Deployment Mode

Legacy Infrastructure Concerns Accelerated Shift to On-Premise/On-Platform Deployment

Based on deployment mode, the market is segmented into on-premise/on-platform, cloud-based, hybrid, and edge/tactical.

The on-premises segment held the dominating position in 2026 and held more than 50.12% share in 2026. Due to security, sovereignty, and mission-critical needs, cyber warfare operations continue to use on-premise or on-platform installations, despite the world moving toward the cloud. Generally, defense organizations prefer on-premise systems with absolute control over the sensitive data, so cloud vendors cannot dispute their rights. Such deployments would involve many fewer cloud-based vulnerabilities when applied to classified operations. In cyber warfare, where latency and breach of security can destroy the objective of the mission, having on-platform solutions physically closer remains a necessity. However, coupled with scalability, security considerations are now promoting approaches that accommodate on-premise resilience alongside trial cloud adoptions.

- July 2024 – The Indian Ministry of Defense unveiled its Defense Cyber Agency operations center with fully on-premise systems to manage classified threat intelligence, emphasizing sovereignty and national data security.

By Operational Level

Operational Segment Led Market Due to its Cyber Warfare Aims for Sustained Campaign Impact

Based on operational level, the market is segmented into strategic, operational, and tactical.

The operational segment held the dominating position in 2024 and held more than 40% share in 2024. Operational-level cyber warfare bridges the gap between tactical engagements and strategic planning. It involves translating national cyber strategies into deployable campaigns that can neutralize adversaries during conflicts. Operational cyber units conduct joint missions, integrating with conventional forces to disrupt command structures, communications, or logistics chains of adversaries. This mid-tier level has become critical in hybrid wars, where timing, coordination, and precision shape mission outcomes. Unlike purely tactical actions, operational cyber warfare aims for sustained campaign impact, targeting adversary vulnerabilities across critical infrastructure and supply lines.

- July 2024 – The Indian Ministry of Defense unveiled its Defense Cyber Agency operations center with fully on-premise systems to manage classified threat intelligence, emphasizing sovereignty and national data security.

By Target Environment

Digital Sovereignty Demands Spurred Adoption in Enterprise/Government IT Segment

Based on the target environment, the market is segmented into enterprise/government IT, industrial, control system (ICS), weapons & platforms, telecom & satcom, elections & civil infrastructure, financial infrastructure, and military base & IoT infrastructure.

The enterprise/government IT segment held the dominating position in 2024 and held more than 28% share in 2024. Government and business IT infrastructures continue to be prime targets of cyber war as they contain sensitive information that includes everything from classified intelligence to citizen records. Enemies seek to subvert governance, undermine critical decision-making, and erode institutional trust. Governments are retaliating by making investments in secured IT networks, sophisticated monitoring, and cyber resilience processes. Businesses particularly in defense supply chains are similarly strengthening defenses to protect intellectual property and operational continuity. This industry's vulnerability to espionage and sabotage means that it is among the biggest spenders on cyber warfare defense.

- January 2025 – The European Union launched a USD 1.41 Billion cyber defense initiative to secure government IT systems against espionage and sabotage, strengthening resilience across its member states.

By Revenue Model

Cloud Expansion Catalyzed Growth of Software-as-a-Service (SaaS) (GovCloud)

Based on the revenue model, the market is segmented into license/seat-based, software-as-a-service (SaaS) (govcloud), enterprise agreements, consumption-based, retainers, and training & certifications.

The software-as-a-service (SaaS) (GovCloud) segment held the dominating position in 2024 and held more than 20% share in 2024. The use of Software-as-a-Service (SaaS) via government cloud (GovCloud) platforms is gaining momentum in cyber operations. SaaS enables defense agencies to utilize scalable, cost-efficient, and real-time updated tools without depending on legacy infrastructure. GovCloud maintains sovereignty and data security requirements with strict compliance while introducing flexibility for collaboration among allied nations. The emergence of edge-cloud integration further enhances SaaS adoption, which empowers the processing of real-time intelligence. SaaS is also increasingly vital for sharing threat intelligence, vulnerability management, and coordinated cyber defense exercises among government agencies.

- October 2024 – The U.S. Department of Defense announced the expansion of its Joint Warfighting Cloud Capability (JWCC) program, integrating SaaS-based solutions across military networks to enhance operational readiness and secure collaboration.

Cyber Warfare Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

NORTH AMERICA

North America Cyber Warfare Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valued at USD 64.97 billion, and also took the leading share in 2026 with USD 69.61 billion. North America dominates global cyber warfare, supported by gigantic defense expenditures, a robust technology base, and a concentration of defense contractors. The U.S. Department of Defense has put the highest priority on cyber operations as the foundation of its modernization of defense, devoting billions to AI-powered cybersecurity, cloud-enabled intelligence, and cyber resilience for military and government networks. Canada is also growing its cyber defense forces to target state-sponsored attacks. The region's focus on public–private cooperation bolsters overall resilience, making North America the leading hub for cyber warfare capabilities. The U.S. market is projected to reach USD 66.52 billion by 2026.

EUROPE

Europe is seeing fast-tracked investments in cyber warfare capabilities being fueled by increasing geopolitical tensions and hybrid warfare threats. The European Union has initiated multi-billion-euro initiatives to bolster its cyber defense infrastructure, targeting government IT infrastructure, critical infrastructure, and cross-border threat intelligence. NATO's collective defense stance also helps support European nations in enhancing cyber command structures and upgrading C2 systems. Nations such as Germany, France, and the U.K. are leading the way with indigenous cyber warfare capabilities, while pooled funding schemes support smaller EU members. The UK market is projected to reach USD 3.78 billion by 2026, while the Germany market is projected to reach USD 4.16 billion by 2026.

- January 2025 – The European Commission announced a USD 1.5 billion cyber defense initiative to enhance the resilience of government IT and critical infrastructure across member states, reinforcing Europe’s commitment to collective digital sovereignty (European Commission).

Asia Pacific

The Japan market is projected to reach USD 2.87 billion by 2026, the China market is projected to reach USD 12.83 billion by 2026, and the India market is projected to reach USD 2.7 billion by 2026.

MIDDLE EAST & Africa

Middle Eastern countries, especially Saudi Arabia, the UAE, and Israel, are heavily investing in AI-based cyber capabilities and defensive infrastructures for protecting oil & gas and financial sectors. The growth of cyber warfare in the Middle East and Africa is driven by geopolitical tensions, economic competition, and the rapid digital transformation of governments and critical infrastructure. Increasing reliance on digital networks for energy, banking, and government services exposes vulnerabilities that state and non-state actors exploit. Political instability and regional conflicts further incentivize cyber operations as low-cost, high-impact tools for intelligence gathering, disruption, and propaganda. Additionally, limited cybersecurity capacity and outdated regulations in many countries make these regions attractive targets. The rise of sophisticated hacking groups and international cyber alliances amplifies the intensity and frequency of attacks.

Latin America

Over the forecast period, the Latin America region would witness a moderate growth in this market. The Latin America market in 2025 is set to record USD 7.45 billion as its valuation. In Latin America, nations such as Brazil and Mexico are enhancing cybersecurity infrastructure to safeguard government IT and election systems. Though investment levels are not as high as in advanced economies, the increasing occurrence of cyber events is compelling governments to make cyber defense part of national security plans.

COMPETITIVE LANDSCAPE

Key Industry Players

Wide Range of Product Offerings, Coupled with a Strong Distribution Network of Key Companies, Supported their Leading Position

The market for cyber warfare is extremely competitive, with defense contractors, cybersecurity companies, and technology vendors vying to provide cutting-edge offensive and defensive capabilities. Major competitors including BAE Systems, Lockheed Martin, Raytheon Technologies, Northrop Grumman, Thales Group, Leonardo S.p.A., General Dynamics, and Israel Aerospace Industries drive the market through extensive integration into military modernization initiatives. These companies use collaboration with national defense organizations to provide customized cyber defense solutions, command and control (C2) systems with AI capabilities, and GovCloud-based threat intelligence. Meanwhile, cybersecurity vendors such as Palo Alto Networks and Check Point Software are moving into the defense sector, presenting cross-domain security offerings and managed services. Government contracts, R&D expenditures, and localization of cyber solutions for the infrastructure of strategic importance are increasingly dictating competition. Strategic mergers and acquisitions and partnerships are prevalent, as companies seek to consolidate knowledge in cloud security, edge tactical systems, and cyber training. The competitive target is not only the development of advanced cyber weapons but also resilience—providing secure operating environments for militaries and governments.

- March 2025 – Lockheed Martin announced a collaboration with Microsoft to enhance classified GovCloud and AI-driven cyber defense platforms for the U.S. Department of Defense, reinforcing industry partnerships in the evolving cyber warfare domain.

LIST OF KEY CYBER WARFARE COMPANIES PROFILED

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman (U.S.)

- Raytheon Technologies Corporation (U.S.)

- The Boeing Company (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- General Dynamics Corporation (U.S.)

- BAE Systems (U.K.)

- Airbus (Netherlands)

- Booz Allen Hamilton (U.S.)

- IBM Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In May 2025, the U.S., U.K., France, Germany, and other NATO allies issued an advisory warning of a Russian cyber campaign specifically targeting defense support systems destined for Ukraine and other NATO tech sectors. This highlights growing cross-border cyber espionage and reconnaissance threats and is driving increased investment in allied defensive cyber warfare and supply chain protection.

- In July 2025, the city of St. Paul, Minnesota, suffered a coordinated ransom ware attack by the “Interlock” group, leading to widespread disruption of city services, payment portals, and internal systems. The attack forced a state of emergency and involved the deployment of the National Guard, emphasizing how local infrastructure is becoming a target in operational cyber warfare contexts.

- In August 2025, 27 major cybersecurity M&A (mergers and acquisitions) deals were announced globally, including Accenture’s acquisition of CyberCX. These moves indicate consolidation among cyber-defense providers and reflect a push for integrated capabilities in both managed services and threat intelligence across nations.

- In August 2025, multiple critical infrastructure organizations in the Netherlands were breached through a memory overflow vulnerability (CVE-2025-6543) in Citrix NetScaler ADC and Gateway systems. Attackers exploited the flaw to access systems retroactively, demonstrating how vulnerabilities in widely deployed enterprise/Government IT platforms can translate into large-scale risk.

- In January 2025, K. startup Goldilock published a NATO-backed report warning that within two years (i.e., by 2027), AI-powered cyber weapons capable of evading many current security tools will likely become operational. This forecast is pushing governments and defense firms to accelerate R&D in AI-driven defensive technologies.

- In February 2025, Lockheed Martin announced the development of an AI-driven cyber simulation software suite designed to help defense organizations train for adversarial cyber-attacks and strengthen their resilience. The announcement reflects increasing demand for operational-level solutions and simulated environments for cyber training.

- In September 2025, it emerged that Chinese cyber spies impersonated the chair of the U.S. House China Select Committee in a phishing campaign targeting individuals involved in U.S.-China trade negotiations. This incident underlines ongoing cyber espionage efforts aimed at government / policy-making environments and drives focus on defensive countermeasures in Government IT and intelligence sectors.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.69% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Warfare Type

|

By Capability

|

|

By Solution

|

|

By Deployment Mode

|

|

By Operational Level

|

|

By Target Environment

|

|

By Revenue Model

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 144.94 billion in 2026 and is projected to reach USD 303.71 billion by 2034.

In 2025, the market value stood at USD 64.97 billion.

The market is expected to exhibit a CAGR of 9.69% during the forecast period of 2026-2034.

The Defensive Cyber Warfare (DCW) segment led the market by warfare type.

Increasing Cyber Attacks Leading to High Growth Of Appropriate Counter Cyber Warfare.

Lockheed Martin Corporation, Northrop Grumman, and Raytheon Technologies Corporation are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us