Non-Dairy Ice Cream Market Size, Share & Industry Analysis, By Source (Soy, Oats, Almond, Coconut, Rice, and Others), By Flavor (Chocolate, Vanilla, Caramel, Fruity, and Others), By Type (Impulse and Take-Home), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail, and Others), and Regional Forecast, 2026-2034

(Offer valid till 30th Jun 2026)

KEY MARKET INSIGHTS

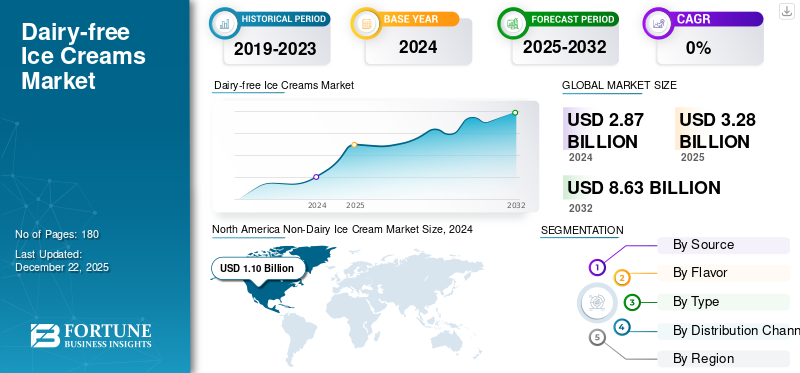

The global non-dairy ice cream market size was valued at USD 3.28 billion in 2025. The market is projected to grow from USD 3.75 billion in 2026 to USD 11.69 billion by 2034, exhibiting a CAGR of 15.25% during the forecast period. North America dominated the non-dairy ice cream market with a market share of 38.08% in 2025.

Non-dairy ice cream, a frozen dessert, is prepared using plant-sourced alternatives instead of animal-based milk. Coconut, soy, almond, and oat milk are popular ingredients used for vegan ice cream preparation. Likewise, milk-based ice creams, dairy-free ice creams are similar in taste and are available in numerous flavors. Specifically, this ice cream is an ideal option for celiac patients or those with dairy allergies, as this item is free from lactose/dairy proteins. Regarding consumption, North America and Asia Pacific are recognized as the biggest consumers of dairy-free ice cream. Surging awareness of the environmental and health advantages and rising prevalence of dairy sensitivities propels the market’s momentum.

A few key players in the industry include General Mills Inc., Nestlé S.A., and Unilever, among others.

Download Free sample to learn more about this report.

Global Non-Dairy Ice Cream Industry Key Takeaways

Market Size & Forecast:

- 2025 Market Size: USD 3.28 billion

- 2026 Market Size: USD 3.75 billion

- 2034 Forecast Market Size: USD 11.69 billion

- CAGR: 15.25% from 2026–2034

Market Share:

- North America dominated the non-dairy ice cream market with a 38.08% share in 2025, driven by rising health consciousness, adoption of vegan lifestyles, and demand for plant-based alternatives.

- By source, almond-based ice cream led the market in 2024, valued for its health benefits, low saturated fat, and high vitamin E content. The coconut segment emerged as the fastest-growing due to its creamy texture and growing popularity.

- By flavor, chocolate led the market in 2024 owing to its universal appeal, while vanilla is expected to grow at the highest CAGR, supported by health-conscious consumer preferences.

- By type, take-home ice cream held the largest share in 2024 due to convenience and customization, whereas impulse ice cream is the fastest-growing segment for on-the-go consumption.

- By distribution channel, supermarkets/hypermarkets led the market in 2024 for their broad product offerings and shopping convenience, while online retail is the fastest-growing segment, driven by ease of ordering and home delivery.

Key Country Highlights:

- United States: Growth is fueled by health-conscious consumers, increasing vegan adoption, and innovative plant-based product launches.

- Canada: Rising demand for dairy-free alternatives and strong retail networks support market expansion.

- Asia Pacific: Increased plant-based diet adoption, rising disposable income, and e-commerce expansion are driving growth.

- Europe: High vegan population and increasing prevalence of dairy allergies support steady market growth.

- South America: Market is developing rapidly due to expanding private-label dairy-free ice creams and affordability.

- Middle East & Africa: Early-stage market growth is supported by increasing health awareness and plant-based diet adoption.

MARKET DYNAMICS

Market Drivers

Growing Incidences of Dairy Allergies to Augment Sales of Vegan Ice Creams

The rising prevalence of dairy sensitivities is a crucial driver boosting the sales of non-dairy ice creams. Today, a large portion of the population is experiencing dairy sensitivities/lactose intolerance, making it challenging to consume traditional dairy ice creams. To maintain their health, lactose-intolerant individuals switch to non-dairy ice creams. Vegan ice creams comprise ingredients such as soy milk, almond milk, and cashew milk, which are lactose-free. Apart from condition-specific consumers, few individuals opt for dairy-free ice creams for health and other ethical reasons. Thus, increasing incidences of allergies pave the way toward the global non-dairy ice cream market growth.

Market Restraints

Challenges in Mimicking Taste and Texture and High Manufacturing Costs May Hinder Market Growth

One of the main hurdles ice cream producers face is replicating the texture and taste of dairy-based ice creams. Globally, most consumers expect a particular sensory experience from frozen items, including rich flavor and creamy texture. Non-dairy substitutes mostly use ingredients such as coconut, pea, almond, and soy, which have different textures and flavor profiles that do not align with the consumer's expectations. As a result, such inconsistency in sensory experience may deter consumers from switching to non-dairy items.

High production cost is another key obstacle in the global market. Compared to dairy ice creams, vegan ice creams are expensive due to the additional processing required to attain a desirable texture and taste, and the cost of procuring superior quality ingredients. Thus, such factors create challenges, especially for price-sensitive consumers across the globe.

Market Opportunities

Emerging Technology Adoption Unlocks Growth Possibilities

The rising adoption of advanced technology in the vegan ice cream industry creates various growth opportunities for superior-quality ice cream. In today's modern ice cream production, robotic systems are used to enhance the blending and mixing process's efficiency and strengthen the consistency, minimizing labor costs. To bolster the manufacturing process, CO2 technology is implemented to improve the texture of novelties. Moreover, ice cream producers can explore high-pressure processing (HPP) to process plant-centric ingredients. Using such technologies assists in strengthening the functionality and textural properties of ingredients. Additionally, machine learning and Artificial Intelligence (AI) are proven to be helpful in optimizing ingredient combinations and flavor profiles to replicate dairy-based ice cream.

Non-Dairy Ice Cream Market Trends

Increasing Inclination toward Gourmet Dairy-Free Ice Cream is a Prominent Trend

Gourmet vegan ice cream is recognized as the fastest-growing and substantial trend globally. This trend is augmented by a rising desire for premium quality ingredients and a strong inclination toward plant-based substitutes. Beyond conventional flavors, most global consumers seek exotic and unique flavor options, including salted caramel, cookie dough, and others. Moreover, the demand for gourmet ice cream with higher protein content, lower calories, and reduced sugar is soaring, fueling ice cream manufacturers to launch such products. As a result, this ongoing trend strengthens the overall consumer experience.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Source

Almond Segment Dominated Market Due to Various Health Benefits

On the basis of source, the market is distributed into soy, oats, almond, coconut, rice, and others.

The almond segment led the global market and generated the maximum share in 2024. Almond milk, when used in ice creams, provides numerous benefits, especially for those looking for a healthier option or with dietary limitations. Unsweetened milk comprises minimal saturated fat and calories, making it safer for consumers concerned about heart health and weight management. Moreover, this milk is a known source of Vitamin E and other beneficial nutrients. Thus, such advantages escalate the segment's growth.

The coconut segment has emerged as the fastest-growing segment in the global market. The creamy texture, healthy fats, and rising demand for plant-based items will escalate the sales of coconut milk.

By Flavor

Chocolate Flavor Led Market Owing to High Acceptability

Depending on flavor, the market is segmented into chocolate, vanilla, caramel, fruity, and others.

The chocolate segment leads the market and has secured the foremost position in 2024. Chocolate is a universally cherished flavor, appealing to a broad range of non-vegan and vegan consumers. Globally, chocolate-flavored ice cream is popular and is mostly recognized as a comfort item. Moreover, dark chocolate, when used, offers antioxidant properties and aids in reducing blood pressure. As a result, this popularity strengthens its consumption.

The vanilla segment held the highest CAGR and is expected to grow at the fastest pace in the near term. This flavor provides a creamy texture and subtle sweetness and offers numerous health advantages. Moreover, it is one of the renowned traditional flavors, boosting its growing potential.

By Type

Take-home Segment Dominated Market Due to Its Flexibility

Based on type, the market is distributed into impulse and take-home.

The take-home segment leads the market and held the largest share in 2024. Takeaway ice creams allow the population to enjoy their treat anywhere at home, the workplace, and outdoors. Furthermore, take-home ice creams offer flexibility in consumption without rushing. Moreover, take-home ice creams can be easily customized at home by adding flavored syrups and sprinklers. Thus, the aforementioned factors augment the sales of take-home non-dairy ice creams.

The impulse segment held the highest CAGR in the market and is anticipated to maintain the same growth pace in the future. These ice creams are designed for on-the-go consumption and are easily available, making them highly accessible. In addition, the single-serving format appeals to wider demographics.

By Distribution Channel

Supermarkets/Hypermarkets Segment Led Market Due to its Advantages of Shopping Experience

On the basis of distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail, and others.

The supermarkets/hypermarkets segment secured the foremost position and generated the highest share in 2024. These channels offer a one-stop shopping experience, allowing individuals to save time and find a range of local/international ice creams. Regular discounts, loyalty programs, and promotions are other key strategies retailers adopt to retain and attract customers. Moreover, these outlets have extended business hours, further promoting the market's momentum.

The online retail segment emerged as the fastest-growing segment and is predicted to attain higher growth in the near term. The easy return/exchange options, freedom of price comparison, and convenience of ordering spur the segment growth.

Non-Dairy Ice Cream Market Regional Outlook

Based on region, the market is segmented into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Non-Dairy Ice Cream Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America recorded a market size of USD 1.25 billion in 2025, capturing 38.08% of the global market share, and is projected to reach USD 1.42 billion in 2026. In this region, the growth is backed by the surging popularity of plant-centric diets and growing health consciousness. Most Americans are focused on health and wellness trends and are looking for ice creams with minimal fat, making non-dairy ice creams an appealing option. The increasing adoption of a vegan lifestyle is another factor supporting the consumption of dairy-free ice creams. Moreover, new product innovation using plant-based milk in the regional market captivates a wider consumer base. Additionally, the growing sustainability and ethical concerns further escalate the sales of non-dairy ice creams.

Among all countries, the U.S. is recognized as the leading nation, followed by Canada and Mexico. The increasing health consciousness trend and a large presence of established players propel the growth potential of the market in the nation.

Asia Pacific

The Asia Pacific market generated USD 1.16 billion in 2025, representing 35.31% of the global market landscape, and is expected to reach USD 1.33 billion in 2026. Factors such as the increasing popularity of plant-centric diets and growing awareness of animal welfare are the main reasons behind the growth. Following this, the large population base, coupled with improved disposable income, offers substantial opportunities for non-dairy ice creams. Moreover, the surging online retail expansion in the region facilitates the intake of plant-sourced ice creams. Additionally, the high adoption of advanced technology in the ice cream sector augments the production of high-quality vegan ice creams.

Europe

In 2025, Europe represented USD 0.79 billion, accounting for 24.04% of the worldwide market, and is projected to grow to USD 0.91 billion in 2026. Europe is a prominent region in the global industry, experiencing considerable growth in the dairy-free ice cream sector. This region is known for its high vegan followers, always seeking sustainable and healthy ice cream. Likewise, in other regions, dairy allergies are also at their peak in Europe, which influences food producers to introduce dairy-free products, including ice creams. Moreover, such plant-centric products offer several health advantages and are lower in saturated fats and cholesterol. Additionally, the wide availability of numerous vegan ice cream flavors and the rising sustainability trend further propel the regional growth.

South America

The market in South America is at its progressing stage and is expected to soar at a higher pace in the coming years. The growing private label players of dairy-free ice creams and increasing affordability upgrade the market's momentum. In 2025, Latin America held 2.50% of the global market, reaching a valuation of USD 0.08 billion, and is projected to grow to USD 0.09 billion in 2026.

Middle East & Africa

The Middle East & Africa region is at its nascent stage and is projected to maintain the same pace in the future. The rising awareness of health consciousness and increasing demand for a plant-based diet enhance the growth possibilities.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Major Players to Aim at Base Expansion to Consolidate Their Market Positions

The key players in the global industry include Nestlé S.A., Danone S.A., and Ben & Jerry's, among others. The firms operating in the market aim for new launches that enhance their market reach. Moreover, companies are entering partnerships that help expand their business base globally.

List of Key Non-Dairy Ice Cream Companies Profiled

- Unilever (U.K.)

- Eclipse Foods (U.S.)

- Oatly (Sweden)

- Danone S.A. (France)

- Frankie & Jo's (U.S.)

- Nestlé S.A. (Switzerland)

- Oregon Ice Cream, LLC (U.S.)

- Van Leeuwen Ice Cream (U.S.)

- Perry's Ice Cream (U.S.)

- HP Hood LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Oppo Brothers, a U.K.-based ice cream producer, introduced vegan ice cream sticks under the "Oppo Refreshed" brand. The item offers low-calorie options and is available in three flavors; Alphonso Mango & Passionfruit, Sicilian Lemon & Strawberry, and Raspberry Coulis Swirl across retailers in the U.K.

- February 2025: Magnum, a well-known ice cream brand of U.K.-based Unilever, announced its replacement of pea protein with soy for the production of ice cream. Magnum Vegan Almond, Magnum Vegan Classic, and Magnum Blueberry Cookie are three flavors available across the U.K.

- January 2025: KSE Limited, an Indian enterprise, released its first dairy-free ice cream through its subsidiary, Vesta. This ice cream is formulated using coconut milk, a plant-centric substitute, for Indian consumers.

- January 2024: Ben & Jerry, a brand of Unilever based in the U.K., launched its latest vegan flavor across the U.S. market. The new Strawberry Cheezecake ice cream comprises oat milk and can be purchased by U.S.-based consumers.

- May 2023: Kale United, a Swedish plant-based enterprise, acquired Lily & Hanna's, a vegan brand of ice cream in Sweden. Kale claimed its acquisition of more than 95% of the shares of Lily's brand.

REPORT COVERAGE

The market research report includes quantitative and qualitative insights into the market. It also offers a detailed analysis of the market size and growth rate for all possible market segments. Key insights in the global market report include an overview of related markets, a competitive landscape, recent industry developments such as mergers & acquisitions, the regulatory environment in critical countries, and current global non-dairy ice cream market trends.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 15.25% from 2026 to 2034 |

|

Segmentation |

By Source

|

|

By Flavor

|

|

|

By Type

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 3.28 billion in 2025.

The market is expected to grow at a CAGR of 15.25% during the forecast period (2026-2034).

By distribution channel, the supermarkets/hypermarkets led the market in 2025.

The growing incidences of dairy allergies and a surge in vegan ice cream sales are key factors propelling industry expansion.

General Mills Inc., Nestle S.A., and Unilever are a few of the top players in the market.

North America held the highest share of the market.

The adoption of emerging technologies to enhance manufacturing processes offers key opportunities, unlocking growth possibilities for industry players.

- 2021-2034

- 2025

- 2021-2024

- 180

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us