Data Center Interconnect Market Size, Share, and Industry Analysis, By Component (Hardware, Software and Services), By Connectivity Type (Short-Haul and Long-Haul), By Application (Disaster Recovery, Shared Data and Resource Clustering, Data (Storage) Mobility, and Other Applications), By End-user (Communications service providers (CSPs), Internet content providers and carrier-neutral providers, government, research and education, and Enterprises), and Regional Forecast, 2026-2034

Data Center Interconnect Market Overview

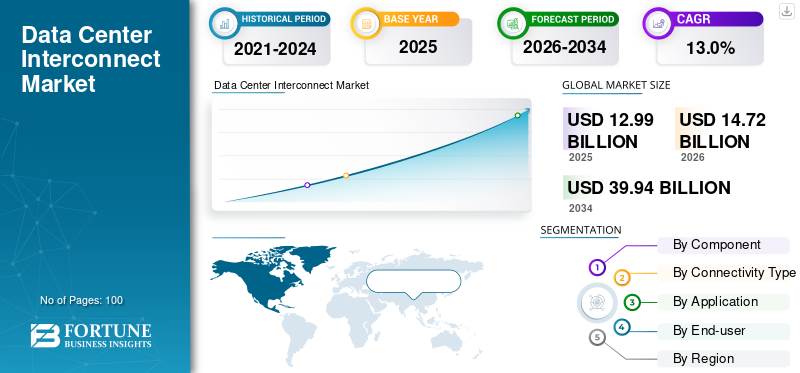

The global data center interconnect market is witnessing moderate growth, and it was valued at ~USD 17.10 billion in 2025. The market is projected to grow ~USD 52.00 billion by 2034, exhibiting a CAGR of ~ (12.5% - 13.0%) during the forecast period (2026-2034). This shift is driven by the need for elastic scalability, real-time analytics, AI-ready workloads, and reduced infrastructure overhead. The rising volume of data generated from digital transactions, IoT devices, cloud applications, and user interactions has surpassed the capacity of conventional data storage solutions, fueling demand for high-capacity, low-latency interconnect solutions.

As enterprises and service providers expand their data center networks, the market for robust, secure, and efficient interconnect infrastructure continues to gain momentum.

Download Free sample to learn more about this report.

Data Center Interconnect Market Driver

Growth of Hyperscale Data Center Models Drives Market Growth

The expansion of hyperscale data centers is driving the data center interconnect market as providers deploy multiple, geographically distributed facilities to handle AI workloads, cloud services, and streaming traffic simultaneously. For instance,

- According to Programs, Data center demand is set to grow by 18 GW next year, followed by about 20 GW annually between 2027 and 2029. A significant surge of 31 GW is expected between 2029 and 2030.

Each new site requires dense, high-speed interconnections to synchronize data in real time and maintain operational continuity, creating repeated, large-scale demand for optical links and switches. Unlike traditional data centers, hyperscale facilities operate as an interconnected ecosystem rather than isolated nodes, making interconnect infrastructure central to their design.

Data Center Interconnect Market Restraint

High Capital Expenditure May Hinder Market Growth

High capital expenditure is a significant restraint for the data center interconnect market, as deploying advanced interconnect infrastructure requires substantial upfront investment. Components such as optical transceivers, DWDM systems, high-capacity switches, and routers are expensive, and scaling them across multiple data centers further increases costs. For smaller enterprises or developing markets, these costs can be prohibitive, delaying adoption or limiting deployment to only critical links. Even large organizations must carefully plan investments to balance capacity needs with budget constraints, which can slow overall market growth.

Data Center Interconnect Market Opportunity

Growing Demand for Green and Energy-Efficient Data Interconnect Solutions Aids the Market Growth

Rising energy costs and global sustainability mandates are driving demand for energy-efficient, high-performance data interconnects. Hyperscale and edge data centers generate massive traffic, yet traditional interconnect hardware consumes substantial power, increasing operational costs and carbon footprints. Providers that design optical transceivers, switches, and routers optimized for both throughput and energy efficiency can secure premium market segments. Incorporating intelligent power management and adaptive traffic routing allows operators to maintain ultra-low latency while meeting environmental goals, making green interconnect solutions a key differentiator in the market.

Segmentation

|

By Component |

By Connectivity Type |

By Application |

By End-user |

By Region |

|

· Hardware · Software · Services |

· Short-Haul · Long-Haul |

· Disaster Recovery and Business Continuity · Shared Data and Resource Clustering · Data (Storage) Mobility · Other Applications |

· Communications service providers (CSPs) · Internet content providers and carrier-neutral providers (ICPs/CNPs) · Government, Research and Education · Enterprises |

· North America (U.S., Canada, and Mexico) · Europe (U.K., Germany, France, Spain, Italy, Russia, Benelux, Nordics, and Rest of Europe) · Asia Pacific (Japan, China, India, South Korea, ASEAN, Oceania, and Rest of Asia Pacific) · Middle East & Africa (Turkey, Israel, GCC, South Africa, North Africa, and Rest of Middle East & Africa) · South America (Brazil, Argentina, and Rest of South America) |

Key Insights

The report covers the following key insights:

- Micro Macro Economic Indicators

- Drivers, Restraints, Trends, and Opportunities

- Business Strategies Adopted by the Key Players

- Consolidated SWOT Analysis of Key Players

Analysis by Component

By component, the market is divided into hardware, software, and services.

Hardware holds the largest share in the data center interconnect market as it forms the backbone of all connectivity infrastructure. Investments in optical transceivers, switches, routers, and DWDM systems dominate spending, as these components are essential for high-capacity, low-latency, and reliable data transmission. The growing demand for faster speeds and long-haul connections further reinforces hardware’s market dominance.

Analysis by Connectivity Type

By connectivity type, the market is bifurcated into short-haul and long-haul.

Short-haul connectivity holds the majority share of the data center interconnect market, as most data centers are concentrated in metro regions. High-bandwidth, low-latency links between nearby facilities drive frequent deployments, making short-haul connections the most used. Long-haul links, used for connecting distant regional centers, are fewer and less frequent, resulting in a smaller market share.

Analysis by Application

By application, the market is classified into disaster recovery and business continuity, shared data and resource clustering, data (storage) mobility, and others.

Disaster recovery and business continuity hold the largest share in the market by application, as ensuring uninterrupted access to critical data and services is a top priority for enterprises and service providers. This application drives significant investment in DCI solutions as organizations require seamless data replication, failover capabilities, and minimal downtime in the face of outages, cyberattacks, or system failures.

Analysis by End-user

By end-user, the market is categorized into communication service providers, internet content providers and carrier-neutral providers, government, research and education, and enterprises.

Internet Content Providers and Carrier Neutral Providers (ICPs/CNPs) hold the largest share in the data center interconnect market by end user, as they operate the most extensive distributed data center networks and generate massive data traffic that must be interconnected. Hyperscale cloud platforms, streaming services, and neutral colocation hubs continuously invest in high-capacity interconnects to support content delivery, cloud access, and peering requirements across regions.

Regional Analysis

Request for Customization to gain extensive market insights.

In terms of geography, the global market is segmented into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America accounted for the largest share of the global data center interconnect market in 2025. It is due to its unique traffic concentration and interconnection-driven network architecture. The region generates and consumes disproportionately high volumes of east–west data traffic due to enterprise SaaS usage, financial trading networks, content platforms, and AI-driven analytics, all of which depend heavily on low-latency interconnects. Unlike other regions that rely more on centralized hubs, North America has a mature ecosystem of carrier-neutral colocation facilities and internet exchange points, which structurally increases demand for data interconnect solutions. Additionally, recent acquisitions in the region also support this trend. For instance,

- In February 2026, H5 Data Centers acquired three carrier-dense interconnection facilities in Buffalo, Nashville, and Tampa from 365 Data Centers, strengthening its regional interconnect footprint. The sites act as key hubs linking metro networks, long-haul fiber, and cloud on-ramps. The move supports growing demand for low-latency cloud, AI, and enterprise workloads beyond major hyperscale markets.

Europe holds the second-largest share in the data center interconnect market due to its fragmented geographic structure and a strong regulatory environment that increases interconnection demand. Data must frequently move across national markets to support financial services, cloud platforms, content delivery, and compliance with data protection regulations. This creates a sustained need for high-capacity, low-latency links between major data center hubs such as Frankfurt, London, Amsterdam, and Paris.

Asia Pacific is expected to grow at the highest CAGR as the region’s digital transformation is leapfrogging traditional stages of connectivity. Rapid urbanization, rising internet penetration, and the explosion of mobile-first services are creating entirely new data traffic patterns, rather than just expanding existing networks. Many countries are building interconnect infrastructure almost simultaneously with cloud adoption, AI deployment, and content delivery growth, which drives unusually high demand. For instance,

- In August 2025, Empyrion Digital announced the deployment of Nokia’s 7250 Interconnect Routers and 7210 Service Access Systems to power its KR1 Gangnam Data Center in Seoul, enhancing its data center interconnect network.

Key Players Covered

The global data center interconnect market is fragmented, with a large number of groups and standalone providers. In the U.S., the top 5 players account for only around 29% of the market.

The report includes the profiles of the following key players:

- Cisco Systems. Inc. (U.S.)

- Ciena Corporation (U.S.)

- Huawei Technologies Co., Ltd (China)

- Juniper Networks, Inc. (U.S.)

- Nokia Corporation (Finland)

- Arista Networks, Inc. (U.S.)

- Broadcom Inc. (U.S.)

- Infinera Corporation (U.S.)

- Extreme Networks, Inc. (U.S.)

- Fujitsu (Japan)

- IBM Corporation (U.S.)

Key Industry Developments

- December 2025: Marvell Technology announced its acquisition of Celestial AI for USD 3.25 billion to advance optical data center interconnects. Celestial AI’s Photonic Fabric enables high-bandwidth, low-latency, and energy-efficient rack-to-rack and intra-rack connections, replacing copper links. The move strengthens Marvell’s leadership in scale-up connectivity and supports next-generation AI data center architectures.

- October 2025: Arista Networks unveiled its R4 series 800G routers to enhance data center interconnects (DCIs) for AI workloads. The modular 7800R4 supports up to 576 ports with HyperPort for high-speed connections between data centers, while the compact 7280R4 offers a fixed alternative. Along with the 7020R4 Ethernet leaf switches for fast server connectivity, these platforms enable simpler two-tier network architectures across distributed data centers.

- 2021-2034

- 2025

- 2021-2024

- 100

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us