Data Processing Unit Market Size, Share & Application Analysis, By Component (Hardware, Software, and Services), By Deployment (On‑premise, Cloud, and Hybrid), By Type (Programmable DPUs, Fixed Function DPUs, and Custom DPUs), By Application (Data Centers, Telecommunications, Cloud Service Providers, Enterprise IT, Government & Defense, Healthcare, and Others), and Regional Forecast, 2026 – 2034

DATA PROCESSING UNIT MARKET SIZE AND FUTURE OUTLOOK

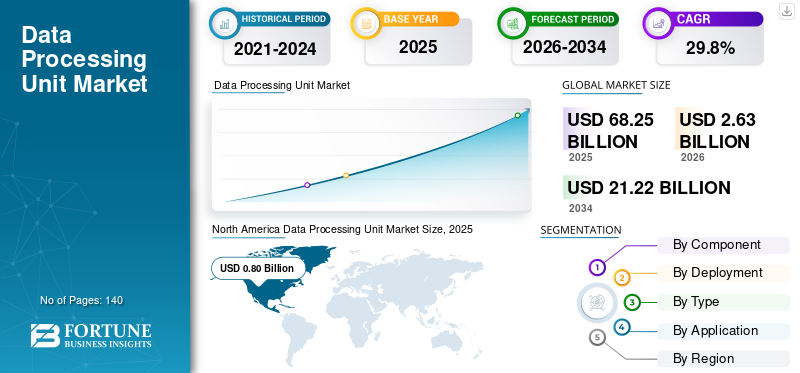

The global data processing unit market size was valued at USD 2.03 billion in 2025. The market is projected to grow from USD 2.63 billion in 2026 to USD 21.22 billion by 2034, exhibiting a CAGR of 29.8% during the forecast period. North America dominated the data processing unit market with a market share of 39.40% in 2025.

The global Data Processing Unit (DPU) market comprises hardware, software, and services that accelerate and offload data-centric infrastructure tasks such as networking, storage processing, security, and data movement from the host CPU. DPUs are designed to improve server efficiency, enhance workload performance, and strengthen infrastructure security in modern computing environments. These solutions are widely adopted across data centers, telecommunications networks, cloud service providers, enterprise IT, government organizations, healthcare institutions, and other industries to support high data traffic, virtualization, and distributed computing architectures. Market growth is driven by the rapid adoption of cloud computing, rising deployment of AI and high-performance workloads, increasing data center virtualization, and the need to optimize infrastructure efficiency while reducing CPU workload.

NVIDIA Corporation, Intel Corporation, Advanced Micro Devices, Inc., Marvell Technology, Inc., Broadcom Inc., Amazon Web Services, Inc., Microsoft Corporation, Fungible, Inc., Netronome Systems, Inc., and Napatech A/S are the top players in the market.

Download Free sample to learn more about this report.

DATA PROCESSING UNIT MARKET TRENDS

Increasing Integration of DPUs in Next-Generation Data Center Architectures is a Key Market Trend

The growing integration of data processing units in next-generation data center architectures is emerging as a key trend in the market. Organizations are increasingly adopting DPUs to support modern infrastructure models such as software defined data centers, cloud native environments, and large scale virtualization platforms. DPUs enable the separation of infrastructure tasks such as networking, storage management, and security processing from the main CPU, improving operational efficiency and system scalability. This architectural shift helps data centers manage increasing data traffic and complex workloads more effectively. As enterprises and hyperscale cloud providers modernize their infrastructure to support AI, high performance computing, and edge workloads, the role of DPUs is expected to expand significantly in future data center deployments.

According to Dell’Oro Group (2024), the global SmartNIC and DPU market is expected to exceed USD 4 billion by 2027, reflecting the increasing integration of DPUs into next generation data center architectures to support cloud and AI workloads.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rapid Growth of Cloud Computing and AI Workloads to Drive Market Growth

The rapid growth of cloud computing and artificial intelligence workloads is a major factor driving the adoption of Data Processing Units (DPUs). Modern data centers handle massive volumes of data traffic generated by cloud services, AI training, and demand for high performance computing applications. These workloads require efficient management of networking, storage, security, and data movement within server infrastructure. DPUs help offload these data processing tasks from the CPU, allowing servers to allocate more computing power to core application workloads. This improves overall server performance, reduces latency, and increases infrastructure efficiency. As enterprises and cloud providers continue expanding large scale data centers, the demand for DPUs is expected to rise to support scalable and efficient computing environments.

- According to The Network Installers, about 33% of global data center capacity was expected to be dedicated to AI workloads in 2025, underscoring the rising demand for advanced infrastructure technologies, such as DPUs, to efficiently manage networking, storage, and data processing.

MARKET RESTRAINTS

High Integration Complexity and Software Ecosystem Dependence Limiting Adoption

The complexity of integrating data processing units is a key restraint on market growth. DPU deployment often requires changes across networking, security, virtualization, and storage layers, which can increase implementation time and operational risk. Many enterprises also face challenges in aligning DPUs with existing server platforms, hypervisors, and management tools. In addition, the overall value depends heavily on software maturity, including drivers, orchestration, monitoring, and update management. If software support is limited or inconsistent across environments, organizations may delay adoption. This complexity is more noticeable for mid-sized enterprises with limited infrastructure engineering resources.

MARKET OPPORTUNITIES

Expansion of Edge Computing Infrastructure Creating Opportunities for DPU Adoption

The growing expansion of edge computing infrastructure presents a significant opportunity for the Data Processing Unit (DPU) market. Edge environments require efficient processing of large volumes of data close to the source to reduce latency and support real time applications. DPUs help manage networking, security, and data movement tasks at the edge while allowing CPUs to focus on application workloads. This improves system efficiency and supports the performance requirements of emerging applications such as autonomous systems, smart cities, industrial automation, and 5G networks. Therefore, organizations are increasingly deploying distributed computing infrastructure and edge data centers, fueling the data processing unit market growth.

- According to Gartner (2024), 75% of enterprise-generated data was expected to be created and processed outside traditional centralized data centers or cloud environments in 2025, highlighting the rapid expansion of edge computing infrastructure and the growing need for technologies such as DPUs to manage distributed data processing efficiently.

SEGMENTATION ANALYSIS

By Component

Hardware Segment Leads the Market Owing to the Increasing Demand for Infrastructure Acceleration

Based on the component, the market is divided into hardware, software, and services.

Hardware segment dominates the market with a 71.5% share, as DPUs are primarily deployed as physical accelerator cards or integrated into servers to handle networking, storage, and security workloads. The growing deployment of cloud infrastructure and AI-driven data centers is increasing demand for hardware solutions that improve server efficiency and reduce CPU workload.

Software segment holds the second largest market share. It is expected to grow at a CAGR of 28.8% over the forecast period, as it enables the configuration, monitoring, orchestration, and integration of DPUs with existing cloud, virtualization, and networking environments. The increasing deployment of programmable infrastructure platforms is driving demand for software tools that support workload management, automation, and performance optimization.

By Deployment

Cloud Segment Dominates the Market Owing to the Rapid Expansion of Hyperscale Infrastructure

Based on deployment, the market is divided into on-premises, cloud, and hybrid.

Cloud segment dominates the market with a 39.2% share, driven by the increasing adoption of DPUs by hyperscale cloud providers to improve workload isolation, infrastructure efficiency, and scalability across large data center environments. The rapid growth of cloud computing, AI workloads, and distributed applications is further accelerating the adoption of DPU-enabled cloud infrastructure.

On-premise segment holds the second largest share and is projected to grow at a CAGR of 28.0% over the forecast period, as large enterprises and regulated industries continue to maintain private data centers for greater control over security, compliance, and system performance. These organizations adopt DPUs to optimize networking, storage, and processing workloads within their existing IT infrastructure.

By Type

Programmable DPUs Lead the Market Owing to Their Flexibility and Scalability

Based on type, the market is segmented into programmable DPUs, fixed function DPUs, and custom DPUs.

Programmable DPUs segment leads the market with 55.5% of share as they allow organizations to customize data processing tasks such as networking, storage, and security based on evolving infrastructure requirements. Their ability to support multiple workloads and adapt to changing data center architectures is driving strong adoption across cloud and enterprise environments.

Custom DPUs segment holds the second highest share. It is expected to grow at the second fastest CAGR of 29.3% during the forecast period, as large technology companies and hyperscale operators develop specialized processors tailored to their specific infrastructure architectures and workload requirements. These solutions provide optimized performance, improved efficiency, and enhanced security for large scale data processing environments.

By Application

To know how our report can help streamline your business, Speak to Analyst

Cloud Service Providers Lead the Market Owing to Large Scale Infrastructure Deployment

By application, the market is segmented into data centers, telecommunications, cloud service providers, enterprise IT, government & defense, healthcare, and others.

Cloud service providers segment holds the largest data processing unit market share of 35.6%, due to their growing operations in large scale data centers that require efficient management of networking, storage, and security workloads. The increasing demand for scalable cloud services and AI computing is encouraging providers to adopt DPUs to improve infrastructure efficiency and performance.

Data centers segment holds the second largest share. It is expected to record a CAGR of 30.3% over the forecast period, as organizations continue to generate and process large volumes of data across digital platforms and enterprise applications. DPUs help data centers manage high data traffic, enhance virtualization performance, and improve overall system efficiency.

Data Processing Unit Regional Outlook

By geography, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

North America

North America Data Processing Unit Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market with a valuation of USD 0.80 billion in 2025. This growth is driven by the strong presence of hyperscale cloud service providers and advanced data center ecosystems that adopt DPUs early to improve infrastructure efficiency. High spending on AI infrastructure, cybersecurity, and high performance computing increases the need for offload and acceleration solutions. Strong vendor presence, mature partner ecosystems, and faster adoption of new server architectures further support market dominance.

- According to CBRE, in 2024, data center capacity in major North American markets grew by 34% year over year, reaching 6,922.6 MW, reflecting the strong expansion of hyperscale cloud infrastructure in the region. This rapid growth in data center capacity supports early adoption of advanced technologies such as DPUs.

U.S. Data Processing Unit Market

The U.S. market was valued at USD 0.48 billion in 2025, accounting for roughly 23.7% of global sales.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe holds a large share due to strong enterprise IT modernization and increasing investments in data center capacity across key countries. A stricter focus on data protection and security is strengthening demand for infrastructure solutions that improve isolation and inline security processing. Broad adoption of hybrid and private cloud models across regulated industries supports consistent deployment.

- According to Cloudscene, Europe hosts more than 1,200 data centers in 2024, with major hubs located in the U.K., Germany, France, and the Netherlands. This robust data center infrastructure supports enterprise IT modernization and the growing adoption of advanced computing technologies.

U.K Data Processing Unit Market

The U.K. market in 2025 was valued at USD 0.09 billion, representing roughly 4.4% of global revenues.

Germany Data Processing Unit Market

Germany’s market reached approximately USD 0.06 billion in 2025, equivalent to around 2.8% of global sales.

Asia Pacific

Asia Pacific holds a significant share due to rapid cloud adoption, large-scale data center expansion, and the rise of digital services across major economies. Telecom modernization, 5G rollout, and increasing enterprise virtualization drive demand for higher throughput and secure data movement. Growth in regional cloud players and expanding manufacturing and online platforms also supports steady DPU uptake.

- According to the GSMA (2024), 5G connections in the Asia Pacific are expected to reach about 1.4 billion by 2030, representing nearly 41% of total mobile connections in the region. The rapid expansion of telecom networks and digital services is increasing demand for high-performance data infrastructure.

Japan Data Processing Unit Market

The Japan market in 2025 was valued at USD 0.10 billion, accounting for roughly 5.1% of global revenues.

China Data Processing Unit Market

China’s market was valued at USD 0.14 billion in 2025, representing roughly 6.8% of global sales.

India Data Processing Unit Market

The Indian market in 2025 was valued at USD 0.08 billion, accounting for roughly 4.2% of global revenues.

Middle East & Africa

The Middle East & Africa are expected to grow at the fastest CAGR during the forecast period, driven by accelerating investments in new data centers, cloud regions, and national digital transformation programs. Many deployments are greenfield or modernization-led, creating opportunities to adopt newer infrastructure architectures that include DPUs from the start. Expansion of telecom networks, edge computing, and government-led cloud initiatives further support high growth.

GCC Data Processing Unit Market

The GCC market was valued at USD 0.04 billion in 2025, representing roughly 1.9% of global revenues.

South America

South America is projected to grow strongly as cloud adoption increases and more regional data center capacity is added to improve latency and service availability. Enterprises are gradually modernizing legacy infrastructure, which creates demand for solutions that improve networking, security, and virtualization efficiency. Growth in digital banking, e-commerce, and telecom upgrades supports the expansion of DPU adoption.

Brazil Data Processing Unit Market

The Brazil market in 2025 was valued at USD 0.10 billion, accounting for roughly 4.7% of global revenues.

COMPETITIVE LANDSCAPE

Key Market Players

Key Players Launch New Solutions to Strengthen Market Positioning

Market players launch new solutions to enhance their market positioning by leveraging technological advancements, addressing diverse consumer needs, and staying ahead of competitors. They prioritize portfolio enhancement, strategic collaborations, and acquisitions and partnerships to strengthen their offerings. Such strategic launches enable technology companies to maintain and expand their market share in a rapidly evolving landscape.

LIST OF KEY DATA PROCESSING UNIT COMPANIES PROFILED

- NVIDIA Corporation (U.S.)

- Intel Corporation (U.S.)

- Advanced Micro Devices, Inc. (U.S.)

- Marvell Technology, Inc. (U.S.)

- Broadcom Inc. (U.S.)

- Amazon Web Services, Inc. (U.S.)

- Microsoft Corporation (U.S.)

- Fungible, Inc. (U.S.)

- Netronome Systems, Inc. (U.S.)

- Napatech A/S (Denmark)

KEY INDUSTRY DEVELOPMENTS

- October 2025: NVIDIA unveiled the BlueField-4 Data Processing Unit (DPU) to accelerate AI data centers with networking throughput of up to 800 Gb/s. The platform offloads networking, storage, and security workloads from CPUs to improve efficiency in large scale AI infrastructure.

- February 2025: Cisco introduced a family of data center Smart Switches that integrate programmable AMD Pensando DPUs. The architecture embeds networking and security services directly within the network to simplify data center operations.

- November 2024: Microsoft introduced the Azure Boost DPU at its Ignite conference as part of its new in-house silicon portfolio for cloud infrastructure. The chip improves cloud performance and security while supporting low-power data-centric workloads in Azure data centers.

- October 2024: AMD announced the Pensando Salina 400 DPU, designed to support next generation AI infrastructure and hyperscale networking environments. The processor delivers up to 400G networking capability and improved performance for data center networking services.

- October 2024: AMD expanded its DPU portfolio with new Pensando solutions aimed at hyperscale cloud and AI workloads. The launch highlighted increasing demand for programmable DPUs to manage networking, encryption, and infrastructure workloads in modern servers.

- June 2024: VMware announced vSphere 8 Update 3, adding dual DPU support through vSphere Distributed Services Engine to improve resilience and security for DPU enabled virtualization. The update strengthens the adoption of DPUs in enterprise data centers by expanding platform level support for offload architectures.

- May 2024: Intel launched the IPU Adapter E2100, a data processing unit designed for large scale cloud and enterprise data centers. The platform enables offloading of networking, storage, and security processing from CPUs to improve infrastructure efficiency.

REPORT COVERAGE

The global market analysis provides an in-depth study of the size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, key Application developments, and details on partnerships, mergers, and acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 29.8% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, By Deployment, By Type, By Application, and By Region |

| By Component |

|

| By Deployment |

|

| By Type |

|

| By Application |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.03 billion in 2025 and is projected to reach USD 21.22 billion by 2034.

In 2025, the North Americas market value stood at USD 0.80 billion.

The market is expected to grow at a CAGR of 29.8% over the forecast period.

By application, the cloud service providers segment led the market.

The market is driven by the rapid expansion of cloud computing, increasing AI workloads, and the need to improve data center efficiency by offloading networking, storage, and security tasks from CPUs.

NVIDIA Corporation, Intel Corporation, Advanced Micro Devices, Inc., and Marvell Technology, Inc. are some of the prominent players in the market.

North America dominated the market in 2025 with the largest share.

Rapid cloud expansion, increasing AI workloads, rising data center virtualization, and the need to improve infrastructure efficiency are major factors expected to favor DPU adoption.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us