Defense Electronics Obsolescence Market Size, Share & Industry Analysis, By System (Communication System, Navigation System, Flight Control System, Electronic Warfare System, and Others), By Platform (Land, Naval, and Air), By Type (Supply Chain Obsolescence, Functional Obsolescence, and Technical Obsolescence), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

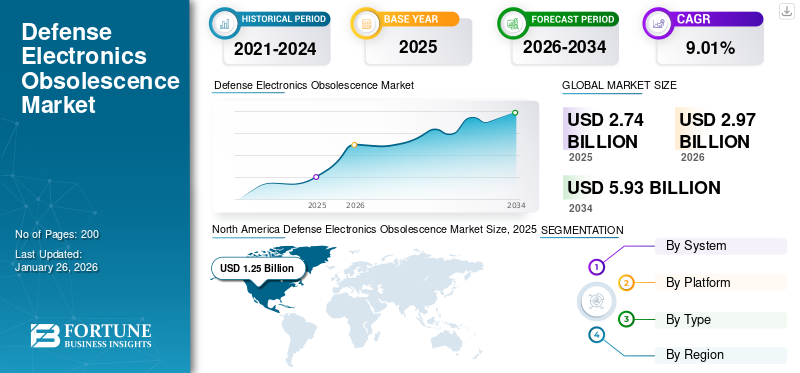

The global defense electronics obsolescence market size was valued at USD 2.74 billion in 2025. The market is projected to grow from USD 2.97 billion in 2026 to USD 5.93 billion by 2034, exhibiting a CAGR of 9.01% over the forecast period. North America dominated the defense electronics obsolescence market with a market share of 45.69% in 2025.

The military electronics obsolescence market addresses the challenges posed by aging electronic components and systems in defense infrastructure. Obsolescence occurs when electronic systems, parts, or technologies are no longer available or sustainable due to advancements in technology, manufacturing discontinuations, or the unavailability of replacement parts. This market plays a critical role in maintaining national security by ensuring that defense systems remain operationally effective despite the rapid pace of technological change and the long operational life of defense programs compared to the shorter lifecycle of electronic components.

Applications of defense electronics obsolescence include reverse engineering, retrofitting outdated systems with modern components, and lifecycle management to ensure operational readiness. The adoption of modular and open architecture designs has further simplified upgrades and reduced vendor dependency. Key players such as BAE Systems, Raytheon Technologies, Lockheed Martin Corporation, and Northrop Grumman are leading innovation in this space by offering AI-driven predictive analytics for obsolescence management.

The COVID-19 pandemic disrupted global supply chains, exacerbating challenges in sourcing replacement parts for aging defense systems. However, it also accelerated investments in digital transformation and predictive analytics for obsolescence management as governments prioritized maintaining operational readiness amidst uncertainties.

Download Free sample to learn more about this report.

GLOBAL DEFENSE ELECTRONICS OBSOLESCENCE MARKET KEY TAKEAWAYS

Market Size & Forecast:

- 2025 Market Size: USD 2.74 billion

- 2026 Market Size: USD 2.97 billion

- 2034 Forecast Market Size: USD 5.93 billion

- CAGR: 9.01% (2026–2034)

Market Share:

- North America held the largest market share in 2025 at 45.69%, valued at USD 1.25 billion.

Key Country Highlights:

- U.S.: FY2025 defense budget exceeds USD 800 billion; major investments in predictive analytics and lifecycle forecasting led by BAE Systems, Raytheon, and Lockheed Martin.

- India: FY2025 defense budget projected to surpass USD 70 billion, focusing on indigenization and tech-driven obsolescence solutions.

- Germany, France, U.K.: Combined defense budgets expected to exceed USD 300 billion by 2025, backed by the European Defence Fund promoting interoperability and obsolescence programs.

MARKET DYNAMICS

Market Drivers

Operational Readiness and Lifecycle Management are Expected to Bolster Market Growth

Operational readiness and lifecycle management are critical factors driving the defense electronics obsolescence market growth. As defense systems increasingly rely on sophisticated electronic components, managing obsolescence has become a priority to ensure the continued functionality and reliability of mission-critical systems. Operational readiness demands that defense equipment remain functional and up-to-date, even as technological advancements render older components obsolete. Lifecycle management addresses this by forecasting obsolescence, integrating new technologies, and ensuring supply chain resilience to maintain the longevity of defense systems.

Moreover, the growing demand for modernization in military systems is fueling investments in innovative solutions that support operational readiness. Strategic partnerships between defense contractors and technology providers are emerging as key enablers for addressing obsolescence challenges. These collaborations focus on developing interoperable solutions that align with stringent military standards while enhancing supply chain agility. As a result, the market is expected to witness sustained growth, driven by the dual imperatives of maintaining operational readiness and effective lifecycle management.

Market Restraints

Complex Supply Chains and High Costs Associated with Obsolescence Management Ought to Restrict Market Expansion Globally

The market faces significant challenges due to complex supply chains and the high costs associated with obsolescence management. Defense systems often rely on specialized components with limited manufacturing sources, making the supply chain vulnerable to disruptions. As technology evolves rapidly, many components become obsolete, requiring replacements or upgrades that are difficult to source globally. This complexity is further compounded by the need to adhere to stringent military standards and regulations, which slow cases innovation and makes integration more challenging.

The financial burden of managing obsolescence is another major restraint on market expansion. The costs involved in this go beyond replacing outdated components, as they include research and development for new technologies, integration into existing systems, rigorous testing, and certification processes. These activities demand substantial investments, often reaching billions of dollars for large-scale system overhauls. Defense budgets are finite and must balance these expenses against other priorities such as personnel costs, maintenance, and acquisitions of new systems. This financial constraint limits the frequency and extent of upgrades, forcing defense organizations to maintain outdated systems longer than desired.

Market Opportunities

Lifecycle Extension Programs Offer Major Growth Opportunity

Lifecycle extension programs represent a significant growth opportunity in the market, addressing the challenges posed by aging systems and rapid technological advancements. These programs focus on extending the operational lifespan of critical defense systems by remanufacturing or reversing engineering obsolete components. By refurbishing outdated parts or creating functionally equivalent replacements, defense organizations can maintain readiness and operational capability without the high costs associated with acquiring entirely new systems. This approach not only ensures continuous functionality but also mitigates supply chain vulnerabilities and reduces dependency on external suppliers.

The demand for lifecycle extension programs is driven by the long operational lifespans of defense platforms, such as aircraft and naval vessels, which often exceed the availability of their electronic components. Programs such as these allow for cost-effective modernization by updating only essential parts, thereby reducing lifecycle costs and environmental impact. Additionally, reverse engineering enables the recreation of critical components when original manufacturers cease production, ensuring that legacy systems remain viable. However, these strategies require specialized skills, advanced technologies, and careful navigation of intellectual property issues, posing initial investment challenges.

Defense Electronics Obsolescence Market Trends

Shift Toward Predictive Analytics is the Latest Trend in the Market

The global market is witnessing a significant shift toward predictive analytics, marking a transformative trend in how defense organizations manage aging systems and component obsolescence. As technological advancements accelerate, the need for proactive strategies to anticipate and mitigate obsolescence risks has become paramount. Stakeholders are increasingly investing in predictive analytics tools that utilize machine learning algorithms to forecast potential obsolescence issues, optimize inventory management, and support timely decision-making. This proactive approach enhances operational readiness and reduces the risks associated with relying on outdated technology, ultimately leading to more efficient defense operations.

The adoption of predictive analytics is also closely tied to the growing complexity of defense systems, which often include sophisticated electronic components that can become obsolete quickly. By leveraging data analytics, defense organizations can better understand the lifecycle of their systems and components, allowing them to implement timely upgrades and replacements. This shift not only helps in maintaining the effectiveness of mission-critical systems but also aligns with broader trends in agile development methodologies and collaborative supply chain partnerships. These strategies enhance agility and resilience against obsolescence challenges, ensuring that defense capabilities remain robust in an evolving threat landscape.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By System

Navigation System Leads Owing to its Increased Upgradation Projected with SAR, GPS, and others to Improve Operational Efficiency

The system classifies the market into communication system, navigation system, flight control system, electronic warfare system, and others.

The navigation system segment dominated the global market share by 10% in 2024 and is anticipated to be the fastest-growing segment for 2026-2034 period. Navigation systems are critical for military operations, enabling precise movement and situational awareness. These systems are increasingly integrated with advanced technologies, including GPS, synthetic aperture radar, and geospatial solutions. Their significant market share is driven by the demand for reliable navigation in both air and land platforms, which are essential for the success of the mission. The communication system segment is projected to dominate the market with a share of 24.09% in 2026.

The communication system segment is anticipated to show significant growth during the study period. Communication systems facilitate secure and real-time information exchange. The rise of cyber-secure communication technologies and command-control software has solidified their importance. The growing reliance on network-centric warfare and situational awareness boosts their market share and CAGR.

By Platform

Advancements in Unmanned Aerial Vehicles (UAVs), Sensors, and Cybersecurity Solutions Boost Air Platform

The market is segmented based on platform into land, naval, and air.

The air segment dominated the global defense electronics obsolescence market share in 2024 and is anticipated to be the fastest-growing segment for 2025-2032 period. This is due to advancements in Unmanned Aerial Vehicles (UAVs), sensors, and cybersecurity solutions. These innovations cater to modern warfare demands, making air systems highly competitive. The CAGR for air platforms reflects the increasing adoption of UAVs and synthetic aperture radars for intelligence gathering. The air segment is expected to lead the market, contributing 43.66% globally in 2026.

The land segment is anticipated to witness significant growth during the study period. Land platforms hold the second largest market share due to the replacement demand for outdated systems. They include vetronics (vehicle electronics) that enhance mobility, protection, and weapon control. The segment is anticipated to exhibit a CAGR of 8.54% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Type

Increased Technical Upgradation to Maintain Competitive Edge is Anticipated to Drive Technical Obsolescence Segment

By type, the segment is categorized into supply chain obsolescence, functional obsolescence, and technical obsolescence.

The technical obsolescence segment dominated the global market in 2024. Technological obsolescence occurs when newer technologies outperform existing ones. In defense electronics, rapid advancements lead to frequent upgrades in navigation and communication systems. Manufacturers focus on technical refreshment strategies to maintain competitiveness. The technical obsolescence segment is expected to account for 43.19% of the market in 2026.

The functional obsolescence segment is anticipated to depict moderate growth during the study period. Functional obsolescence arises when systems fail to meet operational requirements or become inefficient over time. For example, outdated avionics may lack compatibility with modern standards. While functional obsolescence poses challenges, it drives replacement demand, ensuring sustained market activity. The segment is likely to showcase a strong CAGR of 8.94% during the forecast period.

DEFENSE ELECTRONICS OBSOLESCENCE MARKET REGIONAL OUTLOOK

Geographically, the market is segmented into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Defense Electronics Obsolescence Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market was valued at USD 1.25 billion in 2025, capturing 45.69% of global revenue, and is estimated to reach USD 1.36 billion in 2026. The region's dominance is largely attributed to substantial defense budgets, with the U.S. Department of Defense allocating over USD 800 billion for fiscal year 2025 to enhance military capabilities and modernization efforts. Key players such as BAE Systems, Raytheon Technologies, and Lockheed Martin are leading innovation in obsolescence management solutions, focusing on predictive analytics and lifecycle forecasting to mitigate risks associated with aging systems. The U.S. military's emphasis on integrating new technologies while managing existing systems has resulted in a robust demand for advanced obsolescence management strategies. The U.S. market size is estimated to be USD 1.0 billion in 2026.

Europe

In 2025, Europe held 21.77% of the global market, reaching a valuation of USD 0.6 billion, and is projected to grow to USD 0.65 billion in 2026. Europe held a significant market share in 2024 owing to increasing defense budgets among NATO member states in response to geopolitical tensions. The region is expected to be the second-largest market with a value of USD 0.51 billion in 2025, exhibiting the second-fastest CAGR of 9.07% during the forecast period. Germany, France, and the U.K. are enhancing their military capabilities, with budgets projected to exceed USD 300 billion collectively by 2025. Additionally, initiatives, including the European Defence Fund, aim to foster collaboration among member states for joint defense projects, including obsolescence management strategies that enhance interoperability and reduce reliance on single-source suppliers. The market size in U.K. is likely to be USD 0.2 billion in 2026. Germany is expected to hit USD 0.16 billion in 2026. France is likely to hit USD 0.11 billion in 2025.

Asia Pacific

The market in Asia Pacific reached USD 0.48 billion in 2025, representing 17.41% of total market revenue, and is projected to reach USD 0.52 billion in 2026. The Asia Pacific defense electronics obsolescence market is expected to register the fastest CAGR during the forecast period. The region is expected to be the third-largest market with a value of USD 0.52 billion in 2026. China, India, and South Korea are significantly increasing their defense spending to modernize armed forces and enhance technological capabilities. For instance, India's defense budget for 2025 is projected to surpass USD 70 billion, focusing on indigenization and self-reliance in defense manufacturing. The rapid advancements in technology within the region enable local companies to develop innovative obsolescence management solutions tailored to specific defense needs. The growing domestic defense industries present opportunities for partnerships between global players and local firms to address obsolescence challenges effectively. The market size in China is likely to be USD 0.17 billion in 2026. Japan is expected to hit USD 0.1 billion and India is likely to hit USD 0.12 billion in 2026 .

Rest of the World

In 2025, Rest of the World generated USD 0.41 billion, contributing 15.13% to global market revenue, and is projected to grow to USD 0.45 billion in 2026. The rest of the world includes Latin America and the Middle East & Africa for the defense electronics obsolescence market. The rest of the world is likely to be the fourth-largest market with a value of USD 0.38 billion in 2025. Brazil and Saudi Arabia, are investing in modernization efforts but face budget constraints that limit extensive upgrades. However, initiatives aimed at enhancing regional security capabilities are gradually increasing demand for obsolescence management solutions. For example, Saudi Arabia's Vision 2030 plan emphasizes localizing military production and enhancing technological capabilities in defense sectors. The ROW market is valued at USD 0.45 billion by 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players are Focused on Developing Lifecycle Management Solutions to Ensure Operational Readiness of Defense Systems

Leading players in the market are developing comprehensive lifecycle support services that include forecasting, supply chain monitoring, and rapid technological advancements to ensure the operational readiness of defense systems. Forming strategic alliances with other technology firms and defense contractors to leverage complementary strengths and expand market reach in the long term is one of the prominent strategies adopted by the companies. Key players include BAE Systems, Lockheed Martin Corporation, Northrop Grumman, Thales Group, and among others.

LIST OF KEY DEFENSE ELECTRONICS OBSOLESCENCE COMPANIES PROFILED

- Raytheon Technologies Corporation (U.S.)

- BAE Systems (U.K.)

- L3 Harris Technologies Inc. (U.S.)

- Thales Group (France)

- Elbit Systems Ltd (Israel)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- General Dynamics Corporation (U.S.)

- Bharat Electronics Ltd (India)

- Leonardo SPA (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2024 – A contract was awarded for the acquisition of six Next-Generation Missile Vessels (NGMVs) at USD 1.2 billion, scheduled to enhance naval capabilities with stealth and offensive features.

- December 2024 – The Directorate of Defense Research and Development (DDR&D) at the Israel Ministry of Defense (IMOD) declares the conclusion of a series of cumulative agreements with Elbit Systems for the provision of advanced communication systems to the IDF, amounting to roughly USD 130 million.

- August 2024 – Officials from the U.S. Defense Logistics Agency (DLA) are requesting SRI International in Menlo Park, California, to persevere in producing obsolete and unattainable essential microelectronics components for military use under the conditions of a USD 125.6 million five-year contract revealed in July.

- January 2024 – The Commonwealth of Australia awarded BAE Systems a contract to upgrade the Mk 45 Mod 2 naval gun systems on Anzac class frigates, highlighting ongoing modernization efforts in defense systems.

- March 2023 – The Indian Ministry of Defence signed a contract worth approximately USD 730 million for two regiments of upgraded Akash air defense missile systems. This is part of a larger package of contracts totaling USD 4.9 billion aimed at enhancing India's defense capabilities across all military branches.

REPORT COVERAGE

The report outlines competitive dynamics by assessing business segments, product offerings, target market earnings, geographical reach, and significant strategic initiatives by leading manufacturers. The global defense electronics obsolescence market research analysis provides a detailed insight into the market segmentation. Besides this, the report offers insights into the global market trends, Porter’s five forces analysis, supply chain trends, factors increasing demand for the product, and company profile and highlights key industry developments. In addition to the factors above, the report encompasses several factors that have contributed to the growth of the developed market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.01% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By System

|

|

By Platform

|

|

|

By Type

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was valued at USD 2.74 billion in 2025 and is anticipated to be USD 5.93 billion by 2034.

The market is likely to grow at a CAGR of 9.01% during the forecast period.

The leading players in the industry are BAE Systems, Lockheed Martin Corporation, Northrop Grumman, and Thales Group, among others.

North America dominated the market with a share of 45.69% in 2025.

Operational readiness and lifecycle management are expected to bolster the market growth.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us