Defense Electronics Market Size, Share & Industry Analysis, By Vertical (Navigation, Communication, and Display, Electronic Warfare, Optronics, Radars, & C4ISR), By Navigation, Communication, and Display (Avionics, Vetronics, & Integrated Bridge Systems), By Electronic Warfare (Jammers, Self-protection EW Suites, Directed Energy Weapons, Directional Infrared Countermeasures, Antennas, IR Missile Warning Systems, Identification Friend or Foe Systems, Laser Warning Systems, & Radar Warning Receivers), By Optronics (Handheld Systems & Other), By Radars, By C4ISR, and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

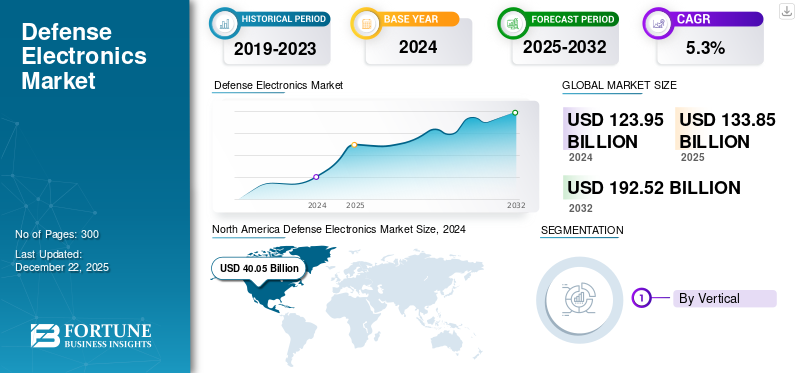

The global defense electronics market size was valued at USD 133.85 billion in 2025. The market is projected to grow from USD 143.20 billion in 2026 to USD 209.04 billion by 2034, exhibiting a CAGR of 4.80% over the forecast period.

The defense electronics industry includes the creation, development, and production of cutting-edge electronic systems that give national defense and military operations a technological advantage. Military electronics are made up of a variety of devices and systems, including radar, communication solutions, avionics, sensors, navigation systems, surveillance equipment, electronic warfare technologies, and cybersecurity solutions, all of which work together to improve the precision, survivability, and efficacy of contemporary military forces.

Critical components include surveillance systems employing drones and unmanned aerial vehicles (UAVs), encrypted satellite communications, software-defined radios, and safe communication networks. Precision-guided missile systems, electronic countermeasures, autonomous land and air platforms, battlefield management systems, and navigation and guidance systems for vehicles and weapons are also included in defense electronics. Modern cybersecurity and electronic warfare systems are essential for safeguarding military information, interfering with enemy communications, and enabling real-time battlefield decision-making.

The market is highly competitive and features several prominent global players, including Lockheed Martin, Northrop Grumman, Raytheon Technologies, BAE Systems plc, and Thales Group. These companies invest heavily in research and development, partnerships, and technology upgrades to address evolving national security threats and the integration of emerging technologies such as autonomous systems and network-centric warfare solutions.

The COVID-19 pandemic had a mixed impact on the market. Initial disruptions in the supply chain, manufacturing slowdowns, and reprioritization of government spending temporarily affected project timelines and new orders.

Download Free sample to learn more about this report.

Defense Electronics Market Key Takeaways

- 2025 Market Size: USD 133.85 billion

- 2026 Market Size: USD 143.20 billion

- 2034 Forecast Market Size: USD 209.04 billion

- CAGR: 4.80% from 2026–2034

- North America dominated the defense electronics market with a 32.34% share in 2025.

- The Navigation, Communication, and Display segment accounted for a 25.42% market share in 2026.

- The Land platform segment is projected to hold a 36.08% share in 2026.

North America

North America held a 32.34% share in 2025, valued at USD 43.29 billion.

Asia Pacific

Asia Pacific accounted for a 26.98% share in 2025, valued at USD 36.12 billion.

Europe

Europe held a 19.13% share in 2025, valued at USD 25.61 billion.

U.S.

The market projected to reach USD 32.04 billion by 2026.

Japan

The market projected to reach USD 6.66 billion by 2026.

Read More

Market Dynamics

Market Drivers

Military Modernization and Multi-Domain Operations are Expected to Bolster Market Growth

Modernization initiatives, especially in developed and developing nations, are converting outdated defense systems into multi-domain operational platforms. The move toward integrated, interoperable forces is reflected in the drive for next-generation radar systems, communication modules, and electronic warfare solutions. A robust and secure electronic infrastructure is becoming increasingly important for maintaining tactical advantages in various conflict zones as multi-domain operations, which coordinate land, air, sea, cyber, and space domains, become more prevalent. The need to constantly improve and expand military electronic capabilities is further highlighted by geopolitical instability boosts the defense electronics market growth.

Market Restraints

Stringent Export Controls and Regulatory Compliance Ought to Restrict Market Expansion

The defense sector continues to face significant challenges from export restrictions and stringent regulatory frameworks. The necessity of adhering to changing government regulations and security procedures, which differ by jurisdiction, can impede design cycles, impede cross-border cooperation, and restrict the movement of technology. Regulations designed to safeguard sensitive dual-use technologies, in particular, may result in compliance obligations that impede international cooperation or push program deadlines back. Reengineering supply chains and development procedures necessitates both administrative competence and a willingness to overcome these limitations.

Market Opportunities

Space and Satellite-Based Defense Electronics Offer Major Growth Opportunity

The militarization of space is creating a major opportunity for the military electronics industry. The development of secure satellite communications, electronic payloads for reconnaissance and anti-jamming, and resilient space-borne sensors is receiving significant government funding. These investments are a deliberate requirement for acquiring space-based situational awareness, missile warning capabilities, and satellite-based networking, which rely on state-of-the-art electronic systems designed specifically to endure the severe conditions of orbit.

Market Challenges

Escalating Cybersecurity Threats Can Lead to Growth Challenges

The military electronics industry is facing a significant growth hurdle due to the growing cybersecurity risks, as cyberattacks grow more complex and sophisticated, constantly raising the standard for system protection. The nature of risk for military and defense applications has been transformed by advanced persistent threats, ransomware, AI-driven assaults, and the spread of fake technologies. Malicious actors using state-sponsored methods and quickly evolving malware are now focusing on defense electronics, which are in charge of vital infrastructure, command and control systems, and battlefield communications.

Defense Electronics Market Trends

Network-Centric Warfare and Digitization in Defense Electronic Systems is a Market Trend

Network-centric warfare (NCW) and digitization are reshaping defense electronic systems by leveraging distributed information networks to boost military effectiveness. In this paradigm, advanced electronic systems—including sensors, communication modules, and command-and-control solutions—are interconnected, forming a dynamic and shared information environment. This networked approach allows geographically dispersed units, from individual soldiers to satellites and unmanned platforms, to share real-time data for enhanced situational awareness, rapid decision-making, and coordinated action. The operational architecture of NCW links sensors, weapons platforms via high-performance digital networks. This configuration encourages self-synchronization, shortens operational timelines, and makes it possible for more adaptable, dispersed forces. Consequently, mission execution is speedier and more accurate, with higher lethality and survivability, and an increased capacity to respond to changing threats.

Impact of Russia-Ukraine War

The military electronics sector has been severely impacted by the conflict between Russia and Ukraine, which has presented difficult problems while simultaneously serving as a catalyst for rapid innovation. The rising significance of electronic warfare skills such as GPS jamming, communication disruption, and signals intelligence has been revealed by the fierce and disputed electromagnetic environment during the conflict. The use of frequency-agile systems and electronic countermeasures by both Russia and Ukraine demonstrates the importance of electronic warfare in contemporary battlefields. Manufacturers are being driven to innovate quickly to satisfy shifting military demands, as this dynamic has raised the need for advanced military electronics that can function effectively in severely contested and jammed environments.

Additionally, the war has disrupted global supply chains for defense electronics, especially in components such as semiconductors and advanced chips. Sanctions against Russia and the reconfiguration of supply networks to avoid conflict zones have created challenges in sourcing critical electronic components. Such disruptions have forced greater emphasis on localization and supply chain resilience for defense manufacturers worldwide. At the same time, the conflict has drawn attention to the strategic importance of space-based electronic systems and satellite communications, as these technologies have been crucial in maintaining situational awareness and command-and-control capabilities in the conflict zone.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Vertical

Navigation, Communication, and Display Dominated Market Owing to Its Increased Focus on Real-time Situational Awareness

By vertical, the market is classified into navigation, communication, and display, electronic warfare, optronics, radars, and C4ISR.

The navigation, communication, and display segment led the market accounting for 25.42% market share in 2026. The segment is experiencing robust expansion as armed forces increasingly require real-time situational awareness and resilient communications in contested domains. Advanced navigation electronics—including GPS-denied, inertial, and quantum positioning systems are pivotal for enabling precision on platforms operating in electromagnetic or physically-challenged environments.

The electronic warfare segment is anticipated to show significant growth during the study period. Electronic warfare (EW) is emerging as one of the most dynamic verticals, reflecting the escalating complexity of threats to electronic and cybercrime.

To know how our report can help streamline your business, Speak to Analyst

By Navigation, Communication, and Display

Owing to Innovation and Multifunctionality Avionics Segment is Anticipated to Dominate Market

Based on navigation, communication, and display, the market is segmented into avionics, vetronics, and integrated bridge systems.

The avionics segment dominated the defense electronics market share in 2024 and is the fastest-growing segment for the 2025-2032 period. Avionics systems are leading innovation in defense electronics, transforming airborne platforms through integration of multifunctional radars, next-generation communication nodes, and advanced sensor fusion for both manned and unmanned aircraft.

The vertronics segment is anticipated to witness significant growth during the study period. Vetronics (vehicle electronics) propel modernization across military fighting vehicles, incorporating ruggedized command-and-control displays, secure communications, and sensor networks.

By Electronic Warfare

Self-protection EW Suites to Lead Owing to Rapid Adoption and Usage in Various Applications,

By electronic warfare, the segment is categorized into jammers, self-protection EW suites, directed energy weapons, directional infrared countermeasures, antennas, IR missile warning systems, identification friend or foe systems, laser warning systems, radar warning receivers, and others.

The self-protection EW suites segment dominated the global market in 2024. Self-protection EW suites are rapidly evolving, empowering military platforms to autonomously detect and counteract electronic threats such as radar-targeted missiles and hostile jamming attempts. These suites leverage sensor fusion, advanced signal processing, and real-time threat classification to optimize platform survivability in dense electronic environments.

The jammers segment is anticipated to show moderate growth during the study period. Modern jammers have seen significant advances, deploying adaptive and cognitive capabilities to deny, deceive, or manipulate enemy sensors, communications, and weapons guidance systems.

By Optronics

Growing Demand for Real-Time and High-Definition Data Delivery Contributes to Handheld Systems Segment Growth

By optronics, the segment is categorized into handheld systems and EO/IR payloads.

The handheld systems segment dominated the global market in 2024. Handheld optronic devices, such as thermal imagers and multispectral scopes, deliver real-time, high-definition sensor data to individual soldiers, enhancing night vision, reconnaissance, and targeting accuracy on fast-moving battlefields. Their compact design and improved power efficiency drive adoption across infantry and special forces.

The EO/IR Payloads segment is anticipated to show significant growth during the study period. EO/IR payloads are seeing accelerated adoption on unmanned platforms (UAVs), manned aircraft, and ground vehicles, where persistent surveillance, autonomous targeting, and long-range detection are crucial.

By Radars

Growing Upgrades in Defense Electronics Contribute to Surveillance and Airborne Early Warning Radars Segment Growth

By radars, the market is categorized into surveillance and airborne early warning radars, tracking and fire control radars, ground penetrating radars, weather radars, counter-drone radars, air traffic control radars, and others.

The surveillance and airborne early warning radars segment dominated the global market in 2024. Surveillance and airborne early warning radar upgrades focus on AESA (Active Electronically Scanned Array) and multi-band technologies. These radars extend detection ranges, offer greater resilience against jamming, and provide real-time situational awareness across increasingly complex airspaces.

The tracking and fire control radars segment is anticipated to show significant growth during the study period. These radars are crucial for precision engagement capabilities in both offensive and defensive roles. Their integration with modern fire control systems ensures effective target acquisition, real-time ballistic computation, and others.

By C4ISR

Growing Demand for Cyber Resilience and Data Sharing in Defense Electronics Contributes to Communication and Network Technologies Segment Growth

By C4ISR, the market is categorized into sensor systems, communication & network technologies, display & peripherals, and others.

The communication & network technologies segment dominated the global market in 2024. Communication and network technologies in military electronics are progressing toward cyber-resilience, high-bandwidth data sharing, and seamless multi-domain connectivity. Secure, software-defined radios and adaptive networking platforms empower both tactical and strategic communications, driving the demand for real-time coordination between distributed assets and command centers.

The sensor system segment is anticipated to show significant growth during the study period. Sensor systems under C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) deliver continuous improvements in battlefield transparency and information reliability.

By Platform

Increased Investment in Vehicles for Defense Electronics Contributes to Land Segment Growth in 2024

By platform, the market is categorized into land, marine, airborne, and space.

The land segment will account for 36.08% market share in 2026. Land platforms benefit from advanced electronics in soldier systems and fighting vehicles, reflecting increased digitization, networked mission operations, and investment in counter-UAS solutions and battlefield automation.

The airborne segment is anticipated to show significant growth during the study period. Airborne platforms, including manned aircraft and UAVs, are at the forefront of adoption for state-of-the-art avionics, sensors, and electronic warfare, maintaining dominance in both market share and technological innovation.

By Land

Integration of Augmented Reality, Improved Communication Contributes to Dismounted Soldier Systems Segment Growth

By land, the market is categorized into dismounted soldier systems, military fighting vehicles, and command centers.

The dismounted soldier systems segment is forecast to represent 11.88% of total market share in 2026. Dismounted soldier systems in the market are rapidly advancing with the integration of augmented reality, improved communication, and enhanced situational awareness technologies. Soldiers on the ground are now equipped with wearable sensors, smart ballistic protection, and mission support tools that enable real-time data sharing, target detection, and threat avoidance.

The military fighting vehicles segment is anticipated to show significant growth during the study period. Military fighting vehicles are increasingly electronic-centric, embedding advanced vetronics, active protection systems, and networked communications. Modern vehicles utilize adaptive electronic warfare setups, multi-functional radars, and sensor suites to ensure crew protection and superior tactical performance.

By Marine

Enhanced Stealth, Survivability, And Multi-Domain Operational Reach Boosted Submarines Segment

By marine, the segment is categorized into aircraft carriers, amphibious ships, destroyers, frigates, submarines, and unmanned maritime vessels.

The submarines segment is expected to lead the market, contributing 5.65% globally in 2026. Submarines require sophisticated sonar and fire control systems, electronic warfare solutions, and advanced navigation to conduct covert, long-endurance missions in contested waters.

The destroyers segment is anticipated to show significant growth during the study period. The segmental growth is owing to a rise in the adoption of next-generation radars, missile defense suites, and integrated command platforms capable of responding to simultaneous air, surface, and asymmetrical maritime threats.

By Airborne

Military Aircraft Dominated Owing to Their Role in Rapid-response, ISR, AIR Superiority, and Strategic Strike Missions

By airborne, the market is categorized into military aircraft, military helicopters, and unmanned aerial vehicles.

The military aircraft segment dominated the global market in 2024. The segmental growth is owing to an increase in various applications such as rapid-response, ISR, air superiority, and strategic strike missions. The adoption of networked avionics, adaptive electronic warfare platforms, and advanced sensor suites is driven by the demand for stealth, multi-role capabilities, and contested airspace survivability.

The unmanned aerial vehicles segment is anticipated to show significant growth during the study period. Unmanned Aerial Vehicles (UAVs) are in high demand for their ability to conduct persistent surveillance, intelligence gathering, and precision targeting at lower risk and cost.

By Space

LEO Dominated Owing to Rapid Deployment in Space Missions

By space, the segment is categorized into LEO satellites, MEO satellites, and GEO satellites.

The LEO Satellite segment dominated the global market in 2024. LEO satellites are favored for rapid deployment and constellation scalability, enabling real-time imagery, data relay, and electronic intelligence across global theaters. Their growth also reflects a drive for resilient, low-latency communications and flexible coverage in dynamic operational environments.

The GEO Satellites segment is anticipated to show significant growth during the study period. GEO satellites support continuous, wide-area surveillance, missile early warning, and secure strategic communications over long timeframes.

DEFENSE ELECTRONICS MARKET REGIONAL OUTLOOK

Geographically, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Defense Electronics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America represented USD 43.29 billion, accounting for 32.34% of the worldwide market, and is projected to grow to USD 46.36 billion in 2026. North America remains the dominant player in the market, driven by its extensive military infrastructure, significant defense budgets, and advanced R&D capabilities. The U.S., in particular, leads with cutting-edge technological development in electronic warfare, cybersecurity, and unmanned systems. The strong presence of major defense contractors and extensive governmental support for innovation have established a robust ecosystem for military electronics in this region. The U.S. market is projected to reach USD 32.04 billion by 2026.

The U.S. dominated the market as government and defense agencies invested heavily in avionics, defense platforms, and others.

Europe

The Europe market generated USD 25.61 billion in 2025, representing 19.13% of the global market landscape, and is expected to reach USD 27.37 billion in 2026. Europe's market is characterized by its focus on upgrading legacy systems and strengthening collaborative defense efforts among member states. The geopolitical environment, marked by evolving security threats and NATO commitments, drives investments in electronic warfare, cybersecurity, and surveillance technologies. Key European nations prioritize developing indigenous capabilities while promoting joint procurement initiatives to enhance interoperability. The UK market is projected to reach USD 6.72 billion by 2026, while the Germany market is projected to reach USD 5.46 billion by 2026.

Asia Pacific

Asia Pacific contributed 26.98% to the global market in 2025, with a valuation of USD 36.12 billion, and is projected to reach USD 38.83 billion in 2026. The Asia Pacific defense electronics market is experiencing rapid growth fueled by rising defense budgets, geopolitical tensions, and ongoing military modernization in countries such as China, India, Japan, and South Korea. These nations are investing heavily in indigenous development of advanced electronic systems, including cyber defense, surveillance, and autonomous platforms, reflecting a strategic push for self-reliance. The Japan market is projected to reach USD 6.66 billion by 2026, the China market is projected to reach USD 9.34 billion by 2026, and the India market is projected to reach USD 8.05 billion by 2026.

Middle East & Africa

The Middle East & Africa market was valued at USD 12.58 billion in 2025, capturing 9.40% of global revenue, and is estimated to reach USD 13.42 billion in 2026. Many Middle Eastern nations are collaborating with international defense contractors to introduce sophisticated electronic platforms while fostering local manufacturing capabilities.

Latin America

The market in Latin America reached USD 10.01 billion in 2025, representing 7.48% of total market revenue, and is projected to reach USD 10.67 billion in 2026.

COMPETITIVE LANDSCAPE

Key Market Players

Key Players Focus on Offering Innovative Solutions and Catering to Specific Niches Within Industry

The competitive landscape in the military electronics market is characterized by the presence of several global giants and numerous specialized manufacturers delivering advanced technological solutions across various military domains. Leading players such as Raytheon Technologies, Lockheed Martin, Northrop Grumman, Boeing, BAE Systems, Thales Group, and Leonardo dominate the market with extensive portfolios covering radar systems, electronic warfare, communication devices, sensors, and avionics. These companies invest heavily in research and development to maintain technological superiority, focusing on emerging areas such as artificial intelligence, unmanned systems, network-centric warfare, and cybersecurity.

LIST OF KEY DEFENSE ELECTRONICS COMPANIES PROFILED

- Lockheed Martin Corporation (U.S.)

- Raytheon Technologies Inc. (U.S.)

- Saab AB (Sweden)

- Northrop Grumman (U.S.)

- BAE Systems (U.K.)

- Thales Group (France)

- Leonardo SpA (Italy)

- L3Harris Technologies Inc (U.S.)

- General Dynamics (U.S.)

- Elbit System (U.K.)

- HENSOLDT (Germany)

- Bharat Electronics Limited (BEL) (India)

KEY INDUSTRY DEVELOPMENTS

- July 2025 – At the International Defence Industry Fair (IDEF) 2025 in Istanbul, ASELSAN unveiled state-of-the-art technologies for increasing air superiority, such as tactical data link systems from the T-Link family and the ASELFLIR 600 next-generation electro-optical targeting system for HALE-class UAVs. With these recent releases, the company has increased its leadership in intelligent solutions for air supremacy.

- May 2025 – The Israeli Air Force (IAF), the Israel Ministry of Defense (IMOD) Directorate of Defense Research & Development (DDR&D), and RAFAEL Advanced Defense Systems carried out an expedited development plan. This initiative allowed IAF Aerial Defense Array troops to use high-power laser system prototypes in the field, which were able to effectively counter dozens of enemy threats.

- February 2025 – The French defense procurement agency (DGA) signed a seven-year framework agreement with KNDS France and Safran Electronics & Defense to develop the DROIDE program: autonomous, robotic systems for reconnaissance, combat, and logistics targeting 2030–35 deployment.

- December 2024 – British soldiers effectively tested a possibly revolutionary weapon that uses radio waves to defeat a swarm of drones. Through Project Ealing, the Radio Frequency Directed Energy Weapon (RFDEW) demonstrator was created, which is capable of identifying, tracking, and countering a variety of threats from land, air, and sea.

- January 2023 – Epirus secured a USD 666.1 million U.S. Army contract to deliver the Leonidas high-power microwave system for counter-drone operations under the IFPC‑HPM program, with prototypes delivered through early 2025.

REPORT COVERAGE

The report outlines competitive dynamics by assessing market segmentations, product offerings, target market earnings, geographical reach, and significant strategic initiatives by leading manufacturers. The global market research analysis provides a detailed insight into the market segmentation. Besides this, the report offers insights into the global market trends, Porter’s five forces analysis, supply chain trends, factors increasing demand for defense electronics, company profile, and highlights key space industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.80% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vertical

|

|

By Navigation, Communication, and Display

|

|

|

By Electronic Warfare

|

|

|

By Optronics

|

|

|

By Radars

|

|

|

By C4ISR

|

|

|

By Platform

|

|

|

By Land

|

|

|

By Marine

|

|

|

By Airborne

|

|

|

By Space

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the global market size was valued at USD 143.20 billion in 2026 and is anticipated to reach USD 209.04 billion by 2034.

The market is projected to grow at a CAGR of 4.80% during the forecast period.

The top leading players in the industry are Lockheed Martin Corporation, Raytheon Technologies Inc., Saab AB, Northrop Grumman Corporation, BAE Systems Plc, Thales Group, and Leonardo SpA.

North America dominated the market in 2025.

Military modernization and multi-domain operations are expected to bolster the market growth.

Network-centric warfare and digitization in defense electronic systems are market trends.

- 2021-2034

- 2025

- 2021-2024

- 300

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us