Dehumidifier Market Size, Share & Industry Analysis, By Product Type (Portable and Fixed/Mounted), By Application (Residential, Commercial, Industrial, and Others), By Technology (Refrigerative and Desiccant), By Distribution Channel (Offline Retail, Online Retail, Direct Sales/B2B Contracts, Distributors/Dealers), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

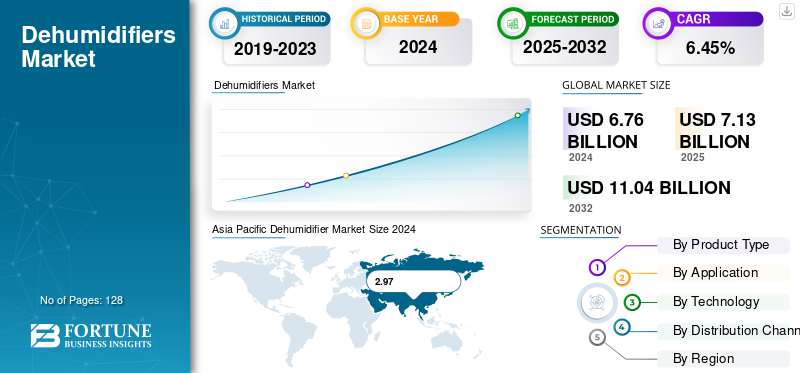

Dehumidifier Market Size and Future Outlook

The global dehumidifier market size was valued at USD 7.13 billion in 2025. The market is projected to grow from USD 7.54 billion in 2026 to USD 15.37 billion by 2034, exhibiting a CAGR of 9.32% during the forecast period. Asia Pacific dominated the dehumidifier market with a market share of 44.17% in 2025.

The dehumidifier is an electrical home appliance intended to remove excess moisture from the air and maintain ideal humidity levels in indoor spaces. Popular varieties include compressor-based refrigerant and desiccant dehumidifiers, which are utilized in commercial, industrial, and domestic settings, including food and beverage, pharmaceutical, and other industries. The IEA (International Energy Agency) noted that global energy usage for air treatment and space cooling rose by over 6% between 2020 and 2021. Additionally, dehumidifiers are opted for more often to maintain healthy humidity levels inside residences and other commercial spaces as a consequence of rising consumer awareness regarding allergies and dust mite prevention. According to the World Meteorological Organization (WMO), global atmospheric humidity is increasing by 1.1% every ten years, fueling demand for humidity control devices. Moreover, industrial data from UNIDO (United Nations Industrial Development Organization) suggests a 4% annual rise in industries necessitating moisture management, which further boosts product adoption globally.

Major players in the market include Munters Group (Sweden), Honeywell International (U.S.), Midea Group (China), Panasonic Corporation (Japan), Whirlpool Corporation (U.S.), Daikin Industries (Japan), and Ebac Ltd. (U.K.). These businesses prioritize product innovation and energy efficiency to remain competitive, creating intelligent, sensor-based dehumidifiers that are connected to HVAC and IoT devices.

Download Free sample to learn more about this report.

Dehumidifier Market KEY TAKEAWAYS

- 2025 Market Size: USD 7.13 billion

- 2026 Market Size: USD 7.54 billion

- 2034 Forecast Market Size: USD 15.37 billion

- CAGR: 9.32% from 2026–2034

- Asia Pacific dominated the dehumidifier market with a 44.17% share in 2025.

- The portable segment is projected to dominate the market with a 55.44% share in 2026.

- The residential segment is expected to lead the market, contributing 54.64% globally in 2026.

Asia Pacific

Asia Pacific recorded a market size of USD 3.15 billion in 2025 and is projected to reach USD 3.35 billion in 2026, maintaining its market leadership.

North America

North America generated USD 2.05 billion in 2025 and is expected to grow to USD 2.16 billion in 2026, supported by strong residential demand.

Europe

Europe accounted for USD 1.51 billion in 2025 and is projected to reach USD 1.59 billion in 2026, reflecting steady market expansion.

U.S.

U.S. The market is valued at USD 1.81 billion by 2026, driven by increasing adoption of indoor air quality solutions.

Japan

Japan The market is valued at USD 0.28 billion by 2026, supported by growing demand for humidity control in residential and commercial spaces.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Growing Awareness of Indoor Air Quality and Humidity Levels Fuels Market Growth

Increasing knowledge of people regarding the importance of maintaining indoor air quality and rising concerns over humidity levels are likely to boost the demand for dehumidifiers in the coming years. As climate change intensifies, humidity and increased indoor air-quality concerns, the global adoption of dehumidifiers is accelerated. Approximately 30% of newly constructed or remodeled buildings face mold or moisture problems, according to the WHO (World Health Organization), highlighting the growing importance of dehumidifiers in preserving hygienic indoor settings.

MARKET RESTRAINTS:

Increased Energy Consumption and Operational Costs Limiting Broader Adoption

Growing electricity usage is the primary factor that restricts budget-conscious buyers from investing in the product, indirectly obstructing the dehumidifier market growth. A regular household dehumidifier can use up to 1,000 kilowatt-hours of electricity per year, compared to running a refrigerator year-round, according to U.S. Department of Energy (DOE) statistics. Subsequently, this increases the working costs, especially in regions with high electricity tariffs. Furthermore, the IEA cited that residential electric appliance energy consumption has spiked by 3% annually, magnifying distresses over sustainability and efficiency. Therefore, dehumidifiers, particularly energy-demanding models, face lower demand, prompting manufacturers to develop energy-efficient, low-power substitutes to overcome this hurdle.

MARKET OPPORTUNITIES:

Combination of Energy-Proficient and Cutting-Edge Technologies into Dehumidifiers Generating Growth Opportunities

The global transition toward advanced, connected, and energy-competent air treatment solutions, including dehumidifiers, offers a potential growth opportunity. According to the IEA data, adopting efficient and connected appliances can help reduce global household energy consumption by up to 25% by 2030, thereby boosting demand for intelligent humidity-control systems. Major players, including Midea and Panasonic, are unveiling IoT-empowered dehumidifiers with adaptive humidity sensors and remote monitoring to improve energy savings and user convenience. Connecting dehumidifiers into smart home ecosystems is the potential key growth prospect for both residential and commercial segments, as the global smart home penetration exceeds 16% in 2024, offering numerous market growth opportunities.

DEHUMIDIFIER MARKET TRENDS:

Embracing Eco-Friendly and Low-Global Warming Potential Refrigerants Emerging as a Key Market Trend

A growing trend in the market is the shift toward environmentally friendly refrigerants with low global warming potential. Conventional refrigerant, including R-410A, is being phased out in favor of R-290 and R-32, which have up to 68% lower GWP, according to the U.S. EPA (Environmental Protection Agency). This strategy aligns with the Kigali Amendment to the Montreal Protocol, aiming for an 80-85% decrease in hydrofluorocarbon emissions by 2047. Key players in the market, such as Midea and Daikin, have introduced dehumidifiers incorporating sustainable refrigerants, demonstrating a successful transition toward climate-conscious and energy-efficient appliance design across global markets.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Higher Household Adoption and Affordability Propel Portable Segment Growth

On the basis of product type, the market is segmented into portable and fixed/mounted.

The portable segment is projecteed to dominate the market with a share of 55.44% in 2026. The segment’s growth is mainly led by its low cost, extensive usage in households, and the simplicity of its mechanism. These movable electronic devices need no professional setup or ducting, which makes it suitable for residences and small to mid-scale offices. As per UN Comtrade data, more than 85% of dehumidifiers that are exported are plug-and-play models and compact, highlighting their mass-market appeal. Moreover, growing sales of electronic devices via online distribution channels and rising metropolitan housing density remain a strong pillar to an increasing demand for portable units compared to mounted or fixed models.

The fixed/mounted segment is projected to expand at a CAGR of 6.15% over the projected period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Rising Humidity Levels and Home Comfort Demand Boosted Residential Segment Growth

By application, the market is categorized into residential, commercial, industrial, and others.

The residential segment is expected to lead the market, contributing 54.64% globally in 2026. Growing residencies adopting humidifiers for mold deterrence and retaining good indoor air quality have contributed to the segment’s growth. With rapid urbanization, growing humidity levels in tropical regions, and compact living spaces, the need to uphold sustainable air quality drives the demand for appliances such as dehumidifiers. According to statistics presented by the WHO, around 30% of construction faces mold and dampness issues, encouraging individuals to spend on dehumidifiers for health and comfort. Additionally, easy accessibility to global brands and availability of economic models have made residential applications more prominent and the most swiftly expanding user category globally.

The industrial segment is expected to grow at a CAGR of 7.30% over the forecast period.

By Technology

High Efficiency in Warm and Humid Climates Supported Growth of Refrigerative Technology

Based on technology, the market is segmented into refrigerative and desiccant.

The refrigerative segment is expected to lead the market, contributing 56.23% globally in 2026. This compressor-based technology is energy-efficient, the most inexpensive, and provider greater performance in warm, humid conditions. Refrigerative technology is extensively favored since it employs condensation to extract moisture and has found several applications in subtropical and tropical regions. Data from UN Comtrade signifies that around 90% of exported dehumidifiers are compressor-based, showcasing their mass production and consumption.

Conversely, desiccant systems, which are increasingly used in industries and largely adopted in low-temperature or cold environments to maintain precise humidity levels, remain prohibitively expensive in terms of cost. The segment is projected to grow at the fastest CAGR of 7.10% over the forecast period.

By Distribution Channel

Strong Consumer Trust and Wider Product Accessibility Fueled Offline Retail Segmental Growth

Based on distribution channel, the market is segmented into offline retail, online retail, direct sales/B2B contracts, and distributors/dealers.

The offline retail segment is projecteed to dominate the market with a share of 43.10% in 2026 due to its reliable and resilient, deeply penetrated network of supermarkets, appliance stores, and specialty HVAC outlets. The growth is primarily driven by the benefits offered by offline purchases, such as immediate product availability, in-person product assessments, and the guidance provided by knowledgeable staff in these stores. The big box stores hold a significant share of appliance sales globally. According to the OECD Retail and E-Commerce Statistics (2024), more than 70% of durable household items are still purchased via physical retail shops, despite growing e-commerce penetration.

Furthermore, shoppers who require dehumidifiers for the entire house or have larger-capacity needs should visit offline retail stores, as they often necessitate installation and consultation services, thereby consolidating the segment’s dominance in both developed and developing markets. The segment is likely to hold a 43.63% share in 2025.

In addition, online retail is the fastest-growing channel and is projected to grow at a CAGR of 7.29% during the study period.

DEHUMIDIFIER MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and Middle East & Africa.

Asia Pacific

Asia Pacific Dehumidifier Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific recorded a market size of USD 3.15 Billion in 2025, capturing 44.17% of the global market share, and is projected to reach USD 3.35 Billion in 2026. Market growth is led by factors such as growing urbanization, higher population and residential densities, growing humidity intensity, and increasing disposable income levels, mainly in countries such as China, India, and Indonesia. Increasing awareness among the population associated with indoor air quality and dehumidifiers’ role in mold prevention has further reinforced product demand. As per World Bank data, the urban Asian population is mounting at over 2% every year, while the World Meteorological Organization (WMO), records steady rises in regional humidity levels, triggering production adoption. In addition, expanding e-commerce and building industries enhance product accessibility, which supports market expansion. In 2025, The Japan market is valued at USD 0.28 billion by 2026, the China market is valued at USD 1.15 billion by 2026, and the India market is valued at USD 1.04 billion by 2026.

North America

In 2025, North America generated USD 2.05 Billion, contributing 28.79% to global market revenue, and is projected to grow to USD 2.16 Billion in 2026. A high adoption rate, growing cases of indoor dampness, and a strong understanding of the connection between indoor air quality and health drive the growth of the dehumidifier market in North America. The U.S. government agency, EPA, estimates that more than 20% of U.S. houses face mold and moisture concerns, boosting steady residential demand. The demand for products in the U.S. is rising due to factors including the prevalence of humid climates in several U.S. states, growing awareness of the importance of indoor air quality, and expansion in new residential and commercial construction. Moreover, rising consumer emphasis on comfort, health, and mold prevention is supplementing market growth in the U.S. The U.S. market is valued at USD 1.81 billion by 2026.

Europe

The Europe market accounted for USD 1.51 Billion in 2025, representing 21.12% of the global industry, and is expected to reach USD 1.59 Billion in 2026 and secure the position of the third-largest region in the market. In the region, Germany and U.K. both are estimated to reach USD 0.34 and USD 0.30 billion each in 2026. The regional market growth is driven by growth in basement construction, HVAC integration, and energy-efficient home retrofits support product replacement cycles. Moreover, expanding commercial and industrial applications, particularly in data centers and pharmaceuticals, further drive the global dehumidifier market size.

South America and Middle East & Africa

The Middle East & Africa market generated USD 0.12 Billion in 2025, representing 1.79% of the global market landscape, and is expected to reach USD 0.13 Billion in 2026. The market in South America reached USD .29 Billion in 2025, representing 4.13% of total market revenue, and is projected to reach USD .31 Billion in 2026. Humid tropical climates, increasing urbanization, and rising demand for home comfort appliances in countries such as Brazil and Argentina, supported by expanding construction and retail infrastructure, drive market growth. In the Middle East & Africa, UAE is set to attain the value of USD 0.04 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players:

Technological Innovation and Sustainable Expansion Strategies Driving Robust Competition

The market is consolidated in nature and experiences fierce competition, as it comprises a mix of international brands and dedicated industrial climate control appliance manufacturers. These players distinguish themselves on multiple factors, such as the reach of their distribution networks, the adoption of cutting-edge technology, and the unveiling of product innovations, including low-GWP refrigerants or low-electricity-consuming models. Market players, including Midea Group, Munters Group, Honeywell International, Whirlpool, and Panasonic Corporation, emphasize designing IoT-enabled, energy-saving, smart dehumidifiers to fulfill every changing consumer and regulatory demand. Brands are also expanding their regional presence, particularly in the Asia Pacific, capitalizing on online channels to reinforce their offline presence and integrate sustainable materials that align with global environmental standards. Additionally, strategic partnerships with industrial clients and HVAC installers help expand B2B penetration. Continued investments in research and development, and product miniaturization, are likely to further supplement long-term growth prospects in both commercial and residential categories.

LIST OF KEY DEHUMIDIFIER COMPANIES PROFILED:

- Munters Group AB (Sweden)

- Condair Group (Switzerland)

- Midea Group (China)

- Honeywell International Inc. (U.S.)

- Whirlpool Corporation (U.S.)

- Ebac Ltd. (U.K.)

- Friedrich Air Conditioning Co. (U.S.)

- OASIS International (U.S.)

- DST (U.S.)

- AprilAire (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- September 2024: Meaco introduced the MeacoDry Arete Two, its most advanced and user-centric dehumidifier to date. The model is equipped with an intuitive LCD display and mobile app connectivity, enabling users to monitor and control humidity levels remotely. Designed for enhanced air quality management and dampness prevention, the Arete Two combines energy efficiency with ultra-quiet operation, reflecting Meaco’s focus on innovation and user comfort in modern indoor environments.

- July 2024: Midea America announced a 400% expansion of its U.S. research and development center in Louisville, Kentucky, adding new laboratory and office facilities, a customer showroom, and a consumer research center. The expansion is expected to create approximately 110 new jobs and bolster innovation capabilities for air treatment and home appliance product development.

- October 2023: Munters completed the acquisition of ZECO Aircon, officially integrating ZECO into its global operations. The deal brought ZECO’s local manufacturing capacity and product portfolio under Munters’ umbrella, enhancing its access to the Indian market. It also strengthens Munters’ regional supply chain and accelerates the deployment of its dehumidification solutions across South Asia.

- September 2023: Munters Group AB signed an agreement to acquire ZECO Aircon of India for an enterprise value of MSEK 790, aiming to bolster its dehumidification business in India. With ZECO’s three Indian manufacturing facilities and established sales network, the acquisition provides Munters with enhanced local production, product complementarity, and stronger access to industries such as pharmaceuticals, food and beverage, and battery manufacturing.

- November 2022: Munters Group AB, a provider of energy-efficient air treatment and climate solutions, acquired Hygromedia LLC and Rotor Source Inc., strategically expanding its portfolio in desiccant dehumidification technologies. These acquisitions enhance Munters’ sourcing of desiccant media and rotor components, strengthening its vertical integration and innovation capabilities in industrial moisture control.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.32% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Application, Technology, Distribution Channel, and Region |

|

By Product Type |

· Portable · Fixed / Mounted |

|

By Application |

· Residential · Commercial · Industrial · Others |

|

By Technology |

· Refrigerative · Desiccant |

|

By Distribution Channel |

· Offline Retail · Online Retail · Direct Sales / B2B Contracts · Distributors / Dealers |

|

By Region |

· North America (By Product Type, Application, Technology, Distribution Channel, and Country) o U.S. o Canada o Mexico · Europe (By Product Type, Application, Technology, Distribution Channel, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Rest of Europe · Asia Pacific (By Product Type, Application, Technology, Distribution Channel, and Country/Sub-region) o China o Japan o India o Australia o Rest of Asia Pacific · South America (By Product Type, Application, Technology, Distribution Channel, and Country/Sub-region) o Brazil o Argentina o Rest of South America · Middle East & Africa (By Product Type, Application, Technology, Distribution Channel, and Country/Sub-region) o South Africa o UAE o Rest of Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.13 billion in 2025 and is projected to reach USD 15.37 billion by 2034.

In 2025, the market value stood at USD 3.15 billion.

The market is expected to exhibit a CAGR of 9.32% during the forecast period of 2026-2034.

The portable segment led the market by product type.

The key factors driving the market growth are rapid urbanization, increasing household incomes, rising demand for indoor air quality, and humidity-related concerns.

Munters Group, Honeywell International, Midea Group, Daikin Industries, Panasonic Corporation, and Whirlpool are some of the prominent players in the market.

Asia Pacific dominated the market in 2025

A growing shift toward smart, connected, and energy-efficient dehumidifiers is expected to favor the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 128

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us