Delivery as a Service Market Size, Share & Industry Analysis, By Service Type (Last-Mile Delivery, Reverse Logistics, Scheduled Delivery, On-Demand Delivery and Same-Day Delivery), By Delivery Model (Business-to-Business (B2B), Business-to-Consumer (B2C), and Consumer-to-Consumer (C2C)), By End-Use Industry (E-commerce & Retail, Healthcare & Pharmaceuticals, Food & Beverages, Manufacturing, Logistics & Transportation, and Others) and Regional Forecast, 2026-2034

DELIVERY AS A SERVICE MARKET SIZE

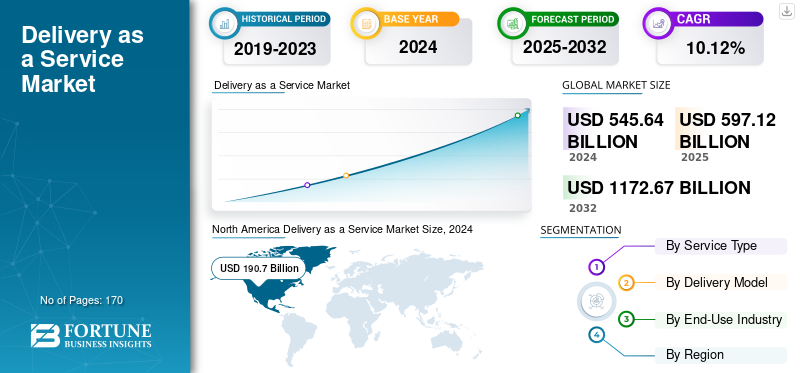

The global delivery as a service market size was valued at USD 597.12 billion in 2025. The market is projected to grow from USD 656.66 billion in 2026 to USD 1,415.19 billion by 2034, exhibiting a CAGR of 10.10% during the forecast period. North America dominated the global delivery as a service market with a market share of 34.70% in 2025.

Delivery as a service is referred to a logistics model where different firms outsource their delivery operations to a third-party provider. It enables businesses to provide fast, on-demand and effective delivery without incurring the cost of maintenance and infrastructure.

The market is noticing a rapid growth due to growth in e-commerce demand, consumers shifting to online shopping owing to its convenience, competitive pricing and variety. These factors have allowed businesses to rely on prominent delivery solutions to meet the growing consumer needs.

Few prominent key players operating in the market include Amazon.com, Inc., DHL International GmbH, United Parcel Service, Inc., FedEx Corporation, DPDgroup (La Poste S.A.), SF Express Co., Ltd., JD Logistics, Inc., Kuehne + Nagel International AG and others. These firms are looking for innovations, adopting new technologies and focusing on mergers and acquisitions.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Rapid Growth of E-Commerce Industry Drives the Market Development

Growth in global e-commerce section and consumers demanding next-day or same-day deliveries are major forces driving delivery as a service market growth. This growth allows retailers, logistics providers, and restaurants to adopt outsourced and technology based delivery solutions. It has enabled companies to optimize fleet utilization, reduce delivery times, and promote last-mile efficiency. Additionally, the increase in penetration of mobile ordering platforms and digital payments further support this growing demand across B2C and B2B sectors.

- For instance, according to the United Nations Conference on Trade and Development (UNCTAD), global e-commerce sales exceeded USD 5.8 trillion in 2023, with continued double-digit growth expected through 2030.

Market Restraints

High Operating Costs and Infrastructure Constraints Hampers the Market Growth

The market for Delivery as a Service faces challenges aligned with a high operational expenses and inconsistent infrastructure, especially in emerging markets. Despite its rapid expansion, the rising fuel costs, fluctuating urban logistics regulations and labor shortage increases the service costs for delivery operators.

Additionally, the lack of standardized technology platforms and limited cold-chain infrastructure deters the scalability of time-sensitive deliveries including groceries and pharmaceuticals. Compliance with carbon-emission regulations in North America and Europe also pushes different logistics providers to invest highly in electric vehicles and sustainable fleet modernization, thus adding to the cost.

Market Opportunities

Integration of Autonomous and Sustainable Delivery Solutions Offers Lucrative Growth Opportunities

Prominent opportunities for the market are evolving through the integration of advanced technologies including drones, autonomous delivery vehicles, and AI based route optimization system. Governments across the U.S., Europe, and Asia Pacific are also supporting pilot programs for the electric last-mile and drone based deliveries to enhance the urban logistics efficiency.

Additionally, different companies including UPS, Amazon and JP Logistics are vigorously investing in autonomous delivery landscape, thus generating new revenue streams and decreasing the cost of last-mile delivery costs. The growing focus on sustainability also offers opportunities by differentiating the product through green logistics and carbon neutral operations, thus appealing to environmentally conscious consumers and enterprises.

DELIVERY AS A SERVICE MARKET TRENDS

Platform Consolidation and Shift Toward Data-Driven Logistics Networks Has Emerged as a Prominent Market Trend

The market is noticing a significant trend with different key players adopting logistics, fulfillment and delivery services into a unified digital ecosystem. There is a rapid shift toward a data driven delivery landscape with the use of predictive analytics and AI to optimize route planning, delivery times and fleet management.

Additionally, partnerships among the retail platforms and logistics providers, including Amazon’s adoption of third party couriers as well as Uber’s global partnership with delivery as a service provider, tends to create a hybrid network that comprises crowd-sourced and specialized delivery modes. This trend highlights the transformation toward a technology based and flexible logistics network that is capable to supporting the future of urban mobility and global commerce.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Service Type

Surge in Urban Logistics Networks, Omnichannel Retailing and Surge in Investments Boosts Last-Mile Delivery Segment Growth

Based on service type, the market is segmented into last-mile delivery, reverse logistics, scheduled delivery, on-demand delivery and same-day delivery.

In 2026, last-mile delivery segment held the largest delivery as a service market share and with a revenue of USD 349.59 billion. This dominance is driven by the growing adoption of last-mile delivery solutions across the retail, e-commerce and food services where speed and reliable doorstep delivery fulfillment has emerged as a key differentiator among the players. This segmental growth is also supported by the surge in urban logistics networks, omnichannel retailing and surge in investments across the route optimization and fleet automation technologies by the logistics providers.

On the other hand, the same-day delivery segment held the highest CAGR of 14.19% in 2024. This growth is owing to the growing consumer expectations for a rapid order fulfillment, integration of advanced logistics technologies including real-time tracking and predictive delivery analytics, and growing penetration of digital marketplaces. Moreover, the expanding urban population and strategic investments by courier as well as e-commerce platforms across the micro-fulfillment centers are also augmenting the segmental growth.

To know how our report can help streamline your business, Speak to Analyst

By Delivery Model

Growing Expansion of Food Delivery, E-Commerce and Online Retail Platforms Drives Business-to-Consumer (B2C) Segment Growth

The market is divided into Business-to-Business (B2B), Business-to-Consumer (B2C) and Consumer-to-Consumer (C2C), based on delivery model.

Among these, Business-to-Consumer (B2C) segment dominated the market with a revenue share of USD 440.58 Billion in 2026. The segment also held highest CAGR of 11.36% in 2024. The segment’s growth is driven by growing expansion of food delivery, e-commerce and online retail platforms, where the direct-to-consumer’s logistics is core of delivery operations. This also benefits from the growing smartphone and internet penetration, with consumers preferring doorstep convenience and rapid investment in digital logistics infrastructure by companies. Moreover, strategic partnerships among the retailers, last-mile operators and courier services are also improving the delivery reliability, speed, and visibility, leading to the segment’s growth.

By End-Use Industry

Rise in Online Shopping Volumes Drives E-commerce & Retail Segment Growth

The market is divided into e-commerce & retail, healthcare & pharmaceuticals, food & beverages, manufacturing, logistics & transportation and others, based on end-use industry.

Among these, the e-commerce & retail segment dominated the market with a revenue share of USD 323.81 billion in 2026. This segment’s growth is driven by the rise in online shopping volumes and ongoing digitalization of retail operations. Different global and regional retailers are relying on the outsourced delivery services to optimize the logistics efficiency, enhance the customer experience and reduce last-mile costs. Additionally, the combination of offline and online sales with the growth in same and next day delivery has also strengthened segment’s growth.

The food & beverages segment held highest CAGR of 11.32% in 2024. This segmental growth is attributed to rapid adoption of online food ordering platforms, emergence of cloud kitchens and increased consumer preference for rapid meal delivery. Additionally, the expanding partnerships among aggregators, restaurants, and logistics companies are improving the delivery speed and reliability with growth in subscription based meal services and grocery delivery apps continue to augment the time-sensitive and specialized delivery models.

DELIVERY AS A SERVICE MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America Delivery as a Service Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

North America

In 2025, North America represented USD 206.91 Billion, accounting for 34.70% of the worldwide market, and is projected to grow to USD 224.71 Billion in 2026. The region’s growth is supported by a mature e-commerce ecosystem, advanced logistics infrastructure, and dense urban and suburban consumer bases. Major retailers and online marketplaces continue to invest in fulfillment networks, last-mile delivery solutions, and automation technologies to improve delivery efficiency. The U.S. market is projected to reach USD 172.77 Billion in 2026.

Europe

The Europe market generated USD 171.61 Billion in 2025, representing 28.70% of the global market landscape, and is expected to reach USD 187.39 Billion in 2026. Growth in the region is driven by increasing demand for rapid and flexible delivery services, rising e-commerce adoption, and expanding use of AI-enabled logistics and route optimization solutions. The U.K. market is projected to reach USD 35.97 Billion in 2026, while the Germany market is projected to reach USD 38.70 Billion in 2026.

Asia Pacific

Asia Pacific contributed 26.60% to the global market in 2025, with a valuation of USD 158.81 Billion, and is projected to reach USD 178.34 Billion in 2026. Rapid urbanization, strong digital adoption, expanding e-commerce activities, and increasing investments in advanced logistics technologies are supporting market growth across the region. The rising middle-class population and growing use of mobile commerce platforms continue to strengthen delivery service demand. The China market is projected to reach USD 98.36 Billion in 2026, while the India market is projected to reach USD 28.51 Billion in 2026 and the Japan market is projected to reach USD 21.18 Billion in 2026.

Latin America

The market in Latin America reached USD 30.13 Billion in 2025, representing 5.00% of total market revenue, and is projected to reach USD 33.32 Billion in 2026. Market growth is driven by increasing internet penetration, expanding e-commerce activities, and ongoing investments in logistics and transportation infrastructure across the region.

Middle East & Africa

The Middle East & Africa market was valued at USD 29.66 Billion in 2025, capturing 5.00% of global revenue, and is estimated to reach USD 32.89 Billion in 2026. Rising urbanization, growing digital commerce adoption, and investments in logistics modernization are contributing to regional growth. Continued development of delivery infrastructure and technology-enabled logistics services is further supporting market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Focusing on Adopting Innovative Strategies to Retain their Market Positions

The delivery as a service industry features different global giants including Amazon.com, Inc., DHL International GmbH, United Parcel Service, Inc., FedEx Corporation, DPDgroup (La Poste S.A.), SF Express Co., Ltd., JD Logistics, Inc., Kuehne + Nagel International AG and others. These firms focus on adopting new technologies, new service launches and partnerships with different firms to sustain the competition and retain market position.

LIST OF KEY DELIVERY AS A SERVICE COMPANIES PROFILED

- Amazon.com, Inc. (U.S.)

- DHL International GmbH (Germany)

- United Parcel Service, Inc. (U.S.)

- FedEx Corporation (U.S.)

- DPDgroup (La Poste S.A.) (France)

- SF Express Co., Ltd. (China)

- JD Logistics, Inc. (China)

- Kuehne + Nagel International AG (Switzerland)

- DoorDash, Inc. (U.S.)

- Uber Eats (U.S.)

- Delhivery Limited (India)

- Zomato Limited (India)

- Bundl Technologies Private Limited (Swiggy) (India)

KEY INDUSTRY DEVELOPMENTS

- In July 2025, E-commerce major Amazon has launched its 10-minute delivery service, Amazon Now, in parts of Delhi, weeks after its public debut in Bengaluru, marking a calculated but notable entry into India’s fiercely competitive quick commerce space.

- In April 2025, Following a successful launch in Bengaluru, Flipkart announced plans to expand its "Flipkart Minutes" same-day delivery service to New Delhi and Mumbai. This initiative includes establishing around 100 dark stores (small, local warehouses) to enable rapid order fulfillment.

- In January 2025, Delhivery has rolled out a new service called Rapid Commerce, aimed at meeting the growing demand for ultra-fast deliveries. This service, which offers delivery in under two hours, has been launched in Bengaluru and is already managing over 300 orders a day.

- In November 2024, Amazon India launched its quick commerce delivery service, codenamed Tez, as it looks to join the booming sector that notched up gross sales of about USD 5.5-6 billion this month led by Blinkit, Zepto and Swiggy Instamart.

- In June 2021, FedEx Corp. and Nuro announce a multi-year, multi-phase agreement to test Nuro’s next-generation autonomous delivery vehicle within FedEx operations. The collaboration between FedEx and Nuro launched with a pilot program across the Houston area. This pilot marks Nuro’s expansion into parcel logistics and allows FedEx the opportunity to explore various use cases for on-road autonomous vehicle logistics, including multi-stop and appointment-based deliveries. The Nuro pilot is the latest addition to the FedEx portfolio of autonomous same-day and specialty delivery devices.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, hardware type, deployment type and end user of the product. Besides this, it offers insights into the delivery as a service market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Attribute | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Growth Rate | CAGR of 10.10% from 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD billion)a |

| Segmentation | By Service Type, Delivery Type, End-Use Industry and Region |

| By Service Type |

|

| By Delivery Model |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 597.12 billion in 2025 and is projected to reach USD 1,415.19 billion by 2034.

The market is expected to exhibit steady growth at a CAGR of 10.10% during the forecast period (2026-2034).

Rapid growth of e-commerce industry drives the market growth

Amazon.com, Inc., DHL International GmbH, United Parcel Service, Inc., FedEx Corporation, DPDgroup (La Poste S.A.), SF Express Co., Ltd., JD Logistics, Inc., Kuehne + Nagel International AG, and others are some of the top players in the market.

The North America region held the largest market share.

North America was valued at USD 206.91 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 170

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us